Author: Kuai Shu Chang (Contributing Writer)

Editor: Qiu Kai Jun

BYD’s rapid expansion in 2022 is clear to all. But a detailed annual report can explain everything.

On March 28th, BYD released its 2022 financial report, with the company’s total revenue reaching RMB 424.06 billion, a YoY increase of 96.20%. Car sales amounted to 1.8035 million units, a YoY increase of 152.65%. Automotive business revenue reached RMB 324.69 billion, a YoY increase of 309.67%. The company’s net profit was RMB 16.622 billion, a YoY increase of 445.86%.

Such performance can be considered explosive for the automobile industry in 2022, with growth in sales, revenue, and particularly profits.

Let’s take a quick look at the four key highlights of BYD’s 2022 financial report, and then briefly analyze why BYD can achieve success to this day.

Four “Rapid Expansions” of BYD’s 2022 Financial Report

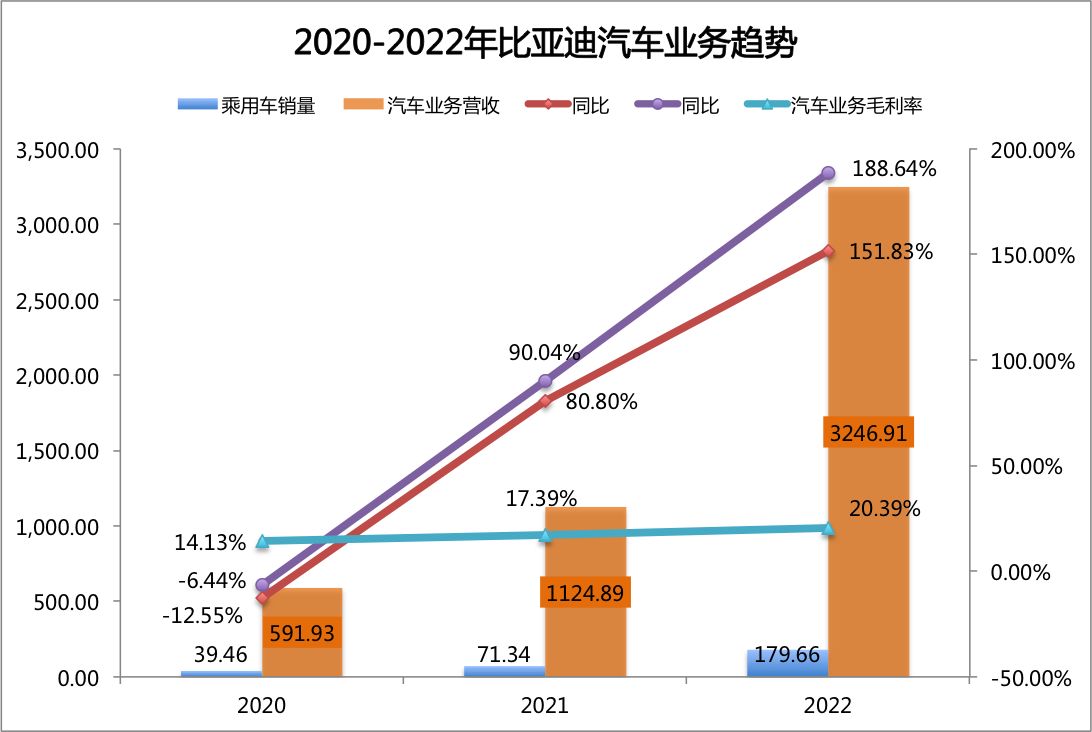

1. “Rapid Expansion” in the Automotive Sector

Looking at data from the last 3 years, from 2020 to 2022, BYD’s automotive business has seen rapid expansion in terms of sales, revenue and gross profit.

Rapid Expansion in Sales: In 2020, BYD’s passenger car sales were 394,600 units, a YoY decline of 12.55%. From 2021 to 2022, BYD’s passenger car sales increased nearly 3.55 times from under 400,000 units to nearly 1.8 million, achieving this growth in just two years.

Rapid Expansion in Revenue: In 2020, BYD’s automotive business revenue was only RMB 59.193 billion (excluding mask revenue), a YoY decline of 6.44%. In just two years, BYD increased its automotive business revenue from less than RMB 60 billion to RMB 324.69 billion, achieving a growth rate of 4.88 times.

Rapid Expansion in Gross Profit: In 2020, BYD’s automotive business gross margin was 14.13% (excluding the gross profit from masks). By 2022, BYD’s automotive business gross margin had increased to 20.39%, which, according to Li Xiang’s Weibo post, “BYD’s Q4 automotive gross margin was 22.8% (dealer system). Assuming the expenses incorporated into the dealer system, BYD’s Q4 gross margin is on par with Tesla’s Q4 gross margin of 25.9% (direct system) or even better. Considering the factor of lower average selling price, BYD’s vehicle cost management is significantly better than Tesla’s. Finance is the most rational exam question, and BYD’s answer is excellent.”

By relying mainly on dealers, the gross profit margin of BYD’s automotive business in the Chinese passenger car market is undoubtedly in the top tier.

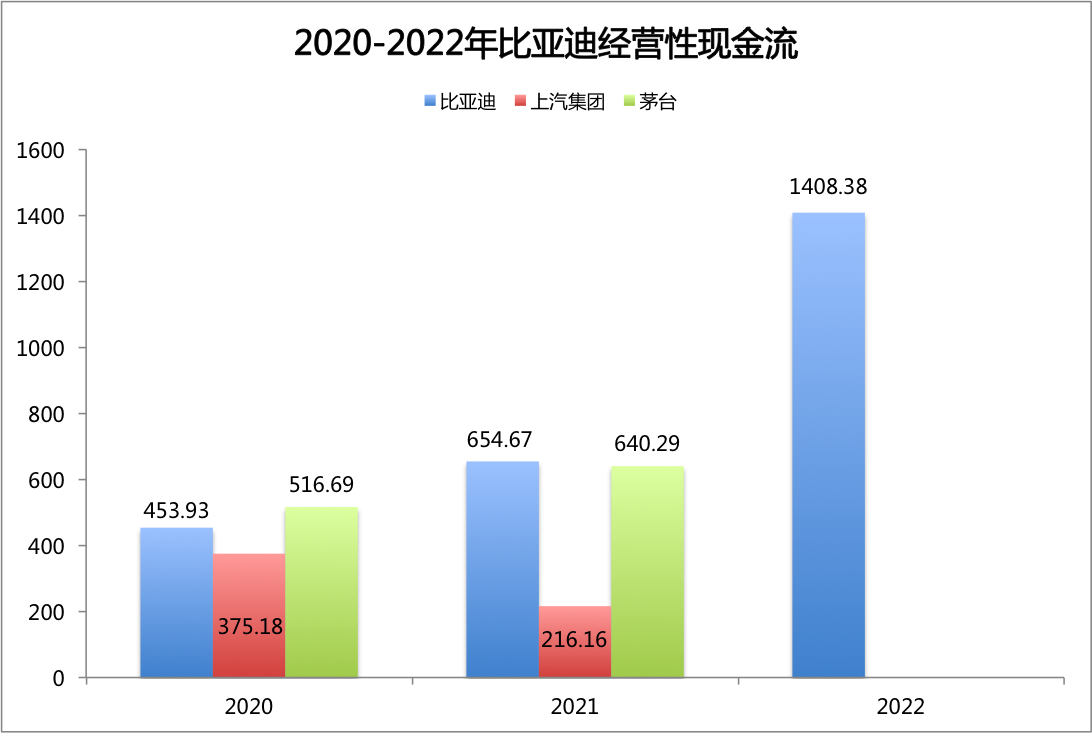

2. Operating Cash Flow “Soaring”

In 2022, BYD’s operating cash flow reached 140.838 billion yuan, which is 2.7 times that of 2020.

SAIC’s peak annual operating cash flow was only over 50 billion yuan, and Moutai’s operating cash flow in 2021 was only 62.029 billion yuan.

In 2021, BYD’s operating cash flow surpassed Moutai’s, and in 2022, BYD’s operating cash flow reached twice the peak of SAIC.

Such operating cash flow data is also among the top in the A-share market.

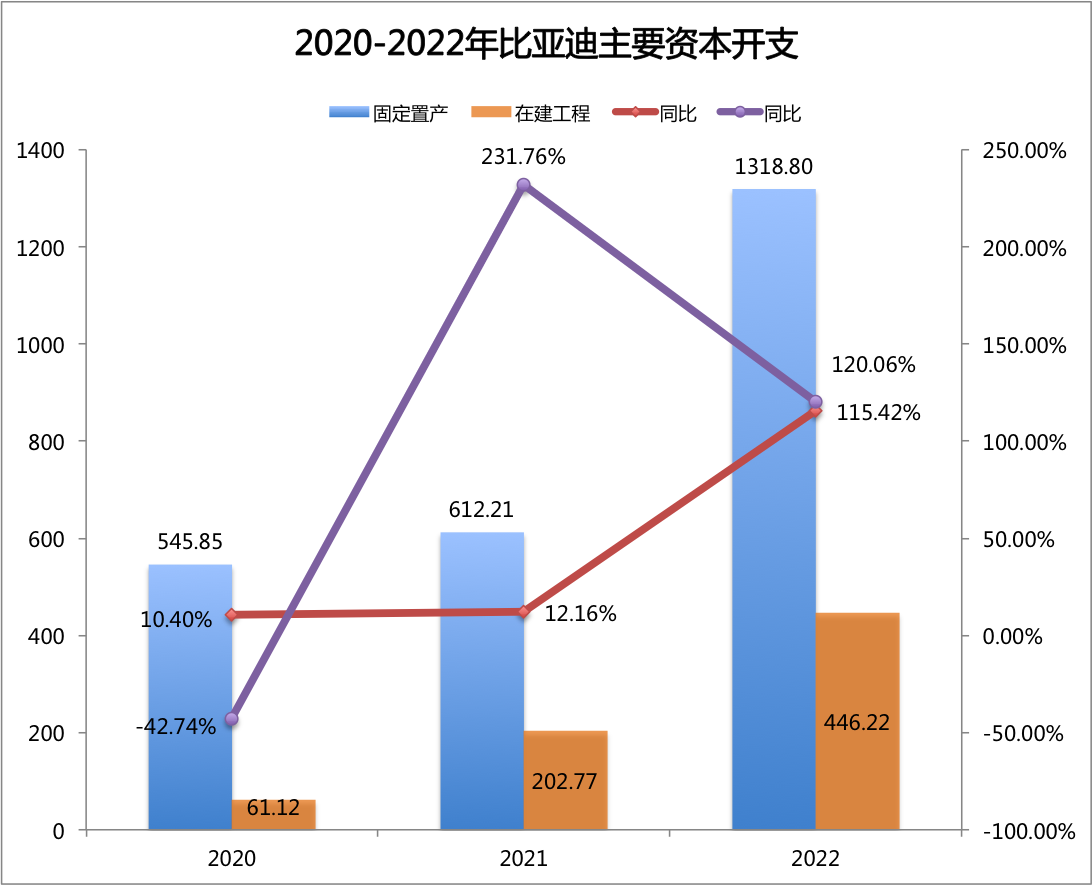

3. Investment “Soaring”

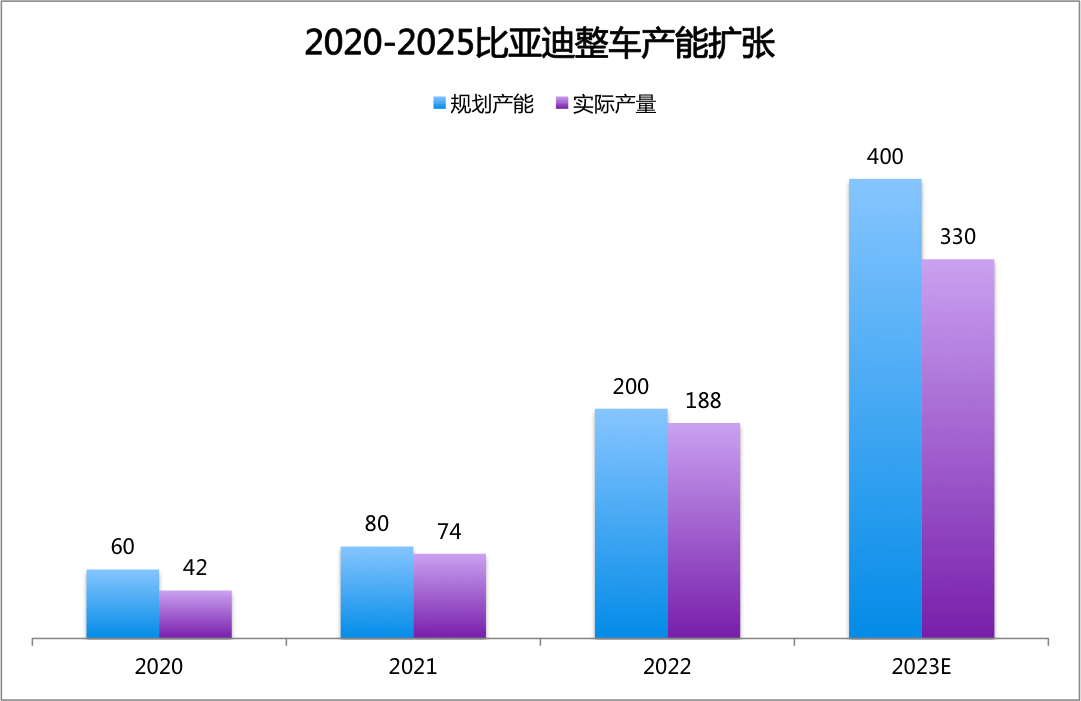

In 2022, BYD’s fixed assets were RMB 131.88 billion, an increase of RMB 70.659 billion from the beginning of the year, a year-on-year increase of 115.42%; the construction in progress was RMB 44.622 billion, an increase of RMB 24.345 billion from the beginning of the year, a year-on-year increase of 120.06%.

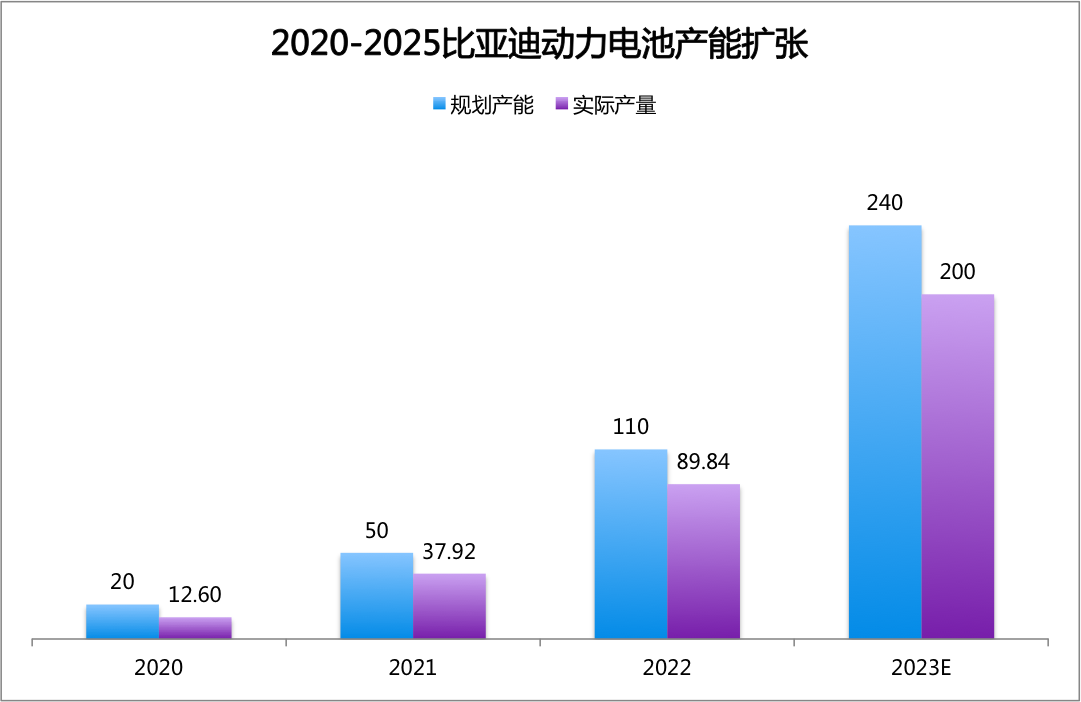

This means that in just one year, BYD invested more than 95 billion yuan in production line and capacity construction. With two consecutive years of high-intensity production line investment, BYD quickly increased its vehicle production capacity from 800,000 to more than 2 million, and it is expected to approach 4 million in 2023; the battery factory’s production capacity was increased from 20GWh (excluding consumer types) in 2020 to nearly 110GWh in 2022, and it is planned to exceed 240GWh in 2023.### 4. Profit “Soaring”

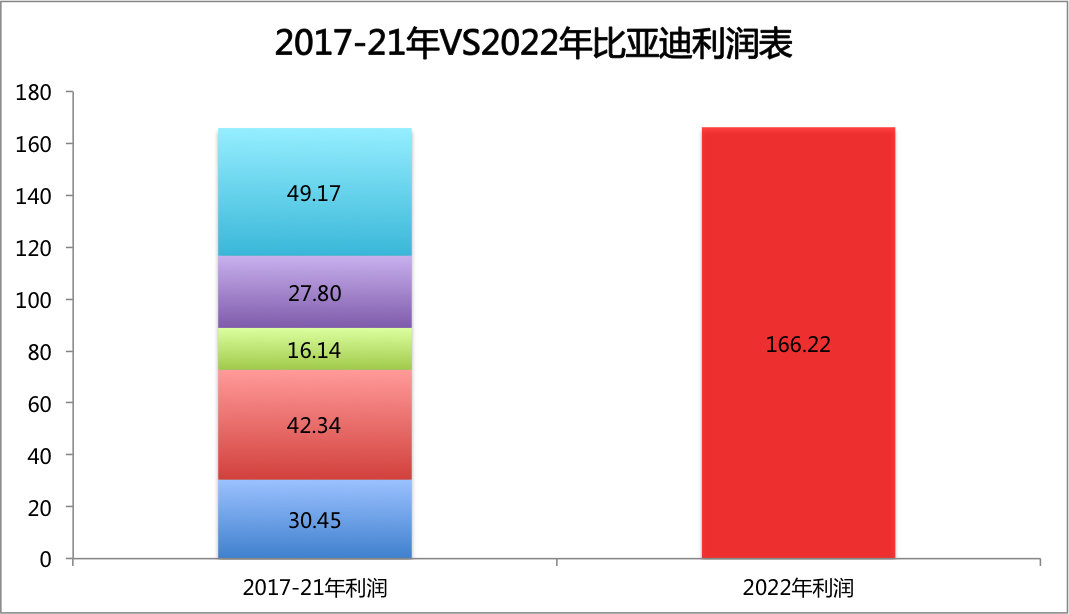

In 2022, it was the first year that BYD’s net profit growth rate was greater than the revenue growth rate and the sales growth rate. Its net profit of 16.622 billion yuan is almost equivalent to the sum of its net profit for the past five years combined.

There is logic behind the economies of scale in the automotive industry, but there are deeper reasons which we will analyze further.

How did BYD achieve this?

1. Products cater to the market, comprehensive mid-to-high-end transition

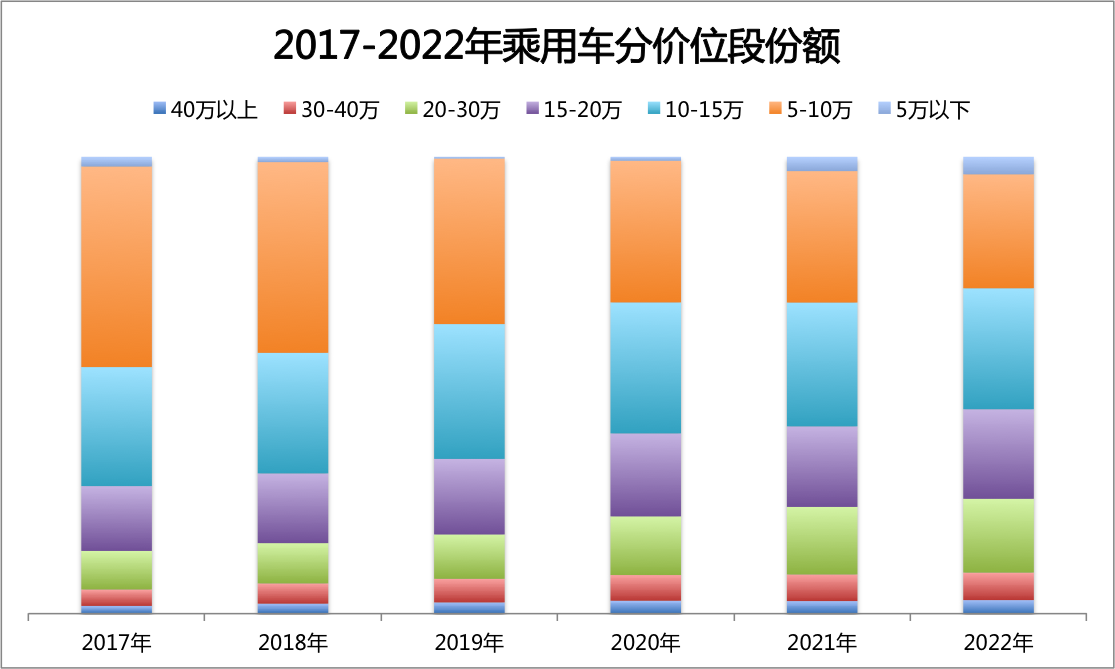

According to the data from the Yiche Research Institute, since 2020, the proportion of first-time car buyers in the Chinese passenger car market has been declining rapidly, while the proportion of customers who buy cars for the second time or more has been growing rapidly. In 2020, first-time car buyers accounted for about 40%, while customers who purchased cars for the second time, or changed cars, accounted for 40% and increasing customers accounted for 20%. By 2022, the proportion of first-time car buyers has approached 30%, while customers who purchased cars for the second time or changed cars accounted for 45%, and the increasing customers accounted for 25%.

Looking at the sales structure of the overall market, the proportion of passenger cars priced below 150,000 yuan is rapidly decreasing, while that of passenger cars priced above 200,000 yuan is rapidly increasing.

After the launch of the Tang in 2020, BYD’s product structure has excellently matched the changes in the market—comprehensive mid-to-high-end transition, which is the basic guarantee for the best-selling products of BYD.

From the sales structure, in 2020, the proportion of BYD’s car models priced under 100,000 yuan accounted for as high as 24.07%, while the sales of car models priced over 200,000 yuan accounted for only 15.54%. By 2022, the proportion of car models priced under 100,000 yuan is only 1.48%, while the sales of car models priced over 200,000 yuan have reached 26.18%.From the perspective of average unit price, BYD’s average unit price, including commercial vehicles, is RMB 14.36 million (excluding mask revenue). In 2022, the average unit price, including commercial vehicles, reached RMB 18.16 million. In two years, the average unit price of a single vehicle has increased by 26.46%.

The synchronous increase in sales structure and average unit price is the primary factor and starting point for BYD to achieve a surge in profits.

2. Large-scale fixed asset investment is the guarantee for BYD’s sales

The automobile industry is a typical industry with heavy capital investment. Taking Tesla as an example, Tesla’s capital expenditures have exceeded 100 billion yuan since its establishment, and its production capacity has been increased from 0 to 2 million vehicles.

However, BYD’s successive investment of over 100 billion yuan in fixed assets in 2021-2022 is the core guarantee for BYD’s doubling of production and sales.

In 2020, BYD’s vehicle production capacity was 600,000 vehicles, with actual production of 420,000 vehicles and a capacity utilization rate of 69.51%. In 2022, BYD disclosed that its production capacity is 1.25 million vehicles, with actual production of around 2 million vehicles and actual sales of 1.88 million vehicles, with a capacity utilization rate as high as 93.78%. At the just-concluded annual report briefing, BYD for the first time revealed its sales target for 2023, which is to achieve a minimum of 3 million vehicles sold and a maximum of 3.6 million vehicles sold.

Similarly, for new energy vehicles, it is not enough to expand the production capacity of complete vehicles alone. The production capacity of power batteries is also indispensable. In 2020, BYD’s planned production capacity for power batteries was 20 GWh, with actual production of 12.6 GWh and a capacity utilization rate of 62.99%. In 2022, BYD’s planned production capacity for power batteries is 110 GWh, with actual production of 89.84 GWh and a capacity utilization rate of 81.67%. It is expected that with the increase of energy storage battery capacity in 2023, the production capacity of power batteries will expand to 240 GWh, and production volume is expected to reach 200 GWh.You can see that the 2-year capital of 115.8 billion yuan has enabled BYD to significantly increase its production capacity, whether in complete vehicles or power batteries.

And these production capacities, especially the power battery production capacity, are the core guarantees for BYD to achieve a leap in scale.

3. Research and Development, R&D and More R&D

In 2022, BYD made significant progress in both R&D expenses and R&D personnel.

In terms of R&D spending: In 2022, BYD’s R&D spending was 20.223 billion yuan, of which the spending on automotive projects was 16.28 billion yuan. This figure is 2.14 times the 7.323 billion yuan spent on automotive R&D in 2021, and 3.92 times that of 2020. It is precisely these sustained high-intensity R&D investments that have enabled BYD to continuously launch products such as the DM-i super hybrid, the DM-p king hybrid, the pure electric e-platform 3.0, the CTB battery body integration, the four-wheel distributed drive “Easy Four”, and the upcoming “Cloud Carriage” technology platform.

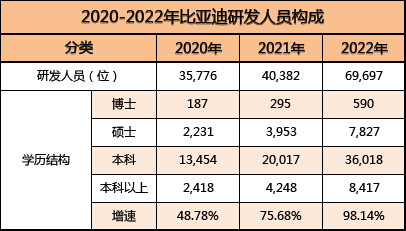

In terms of R&D personnel: In 2022, when many companies were reducing recruitment, BYD was expanding by recruiting 20,000 R&D engineers. This has also enabled BYD’s engineer headcount to reach 69,697 by the end of 2022, including 590 with a Ph.D. degree and 7,827 with a master’s degree. The proportion of R&D engineers with a master’s degree or above has increased from 7% in 2020 to 12% in 2022. In the latest earnings conference, BYD plans to continue recruiting 30,000 new graduates this year, 60% of whom will have a master’s or Ph.D. degree, and plans to hire 700-800 graduates from Tsinghua University and Peking University.

High-end talents and sustained R&D investment are the foundation of BYD’s technology pool, as well as its strength in continuously introducing new technologies to the industry.

This kind of technological innovation capability and intensive technological investment have kept most competitors in a “benchmark + catch-up” rhythm. For example, since its launch in Q1 2021, the DM-i super hybrid has been popular in the market, continuously selling well in 2022, with the Song Plus winning last year’s compact SUV sales championship. However, it wasn’t until Q1 2023 that mainstream domestic brands offered products and technical solutions comparable to the DM-i super hybrid. Nevertheless, with the launch of the BYD 998 Qin champion edition, competitors are once again faced with a difficult choice: if they introduce new cars, BYD has cost advantages in scale (can offer “quantity over price”); if they don’t introduce new cars, their market share will be diluted.# BYD’s Annual Report Reveals a Crucial Detail: R&D Capitalization Rate Is “Pitifully Low” Compared to Other Domestic Auto Brands

BYD’s 2022 R&D capitalization rate was less than 8%, a “pitifully low” figure compared to mainstream Chinese domestic auto brands. For example, Great Wall’s R&D capitalization rate in 2020 was 55.82%, and in 2021 it was 63.96%. Meanwhile, BYD’s R&D capitalization rates for its automotive sector in those same years were only 18.87% and 34.72%, and it dropped to 7.66% in 2022. BYD has essentially chosen to fully expense almost all of their R&D costs, leaving ample room for continued profit growth in the coming years.

A Benchmark for Chinese Domestic Auto Brands

BYD is undoubtedly the most successful brand in the 2022 Chinese passenger car market. That year, BYD became the first brand in the world to announce the cessation of production of fuel vehicles, and replaced Tesla as the world’s best-selling new energy vehicle brand, achieving historic sales volume as the first domestic self-owned car brand.

Looking back on BYD’s history, it is clear that they had a long-term strategy from the beginning to move towards new energy vehicles, and they stimulated and met the demand for these vehicles through methodical development, production, and sales. BYD’s success is based on their long-term strategy and execution.

Furthermore, BYD’s success also rests on their industry preparation in the short term. In the midst of the new energy vehicle market explosion, BYD capitalized on market demand for its product structure and injected substantial amounts of capital into R&D, production capacity, and expansion, thereby achieving amazing incremental revenue and profit growth.

This exemplifies BYD’s success as a benchmark for domestic Chinese passenger car brands.

This article is a translation by ChatGPT of a Chinese report from 42HOW. If you have any questions about it, please email bd@42how.com.