Author: Tao Yanyan

Editor’s note: Zhi Energy Monthly Report is officially launched, which is mainly divided into five sections: vehicle, battery (domestic, foreign, energy storage), charging, electric drive and intelligentization.

The whole vehicle report is divided into two parts. Part 1 is to sort out the overall industry, including tracking key enterprises, and Part 2 is to make judgments on the situation of various models. First, let’s look at the data:

-

In terms of total sales, the total sales volume is 1.247 million, of which 951,400 are fuel vehicles (including 44,600 HEVs), 109,000 are plug-in hybrids, and 181,800 are pure electric vehicles.

-

In terms of penetration rate, in January, new energy vehicles accounted for 23.3%, of which BEVs accounted for 14.6% and plug-in hybrids accounted for 8.7%. Interestingly, the ratio of PHEV to BEV is 1:1.67, and I estimate that it may exceed 1:1.4 by mid-year.

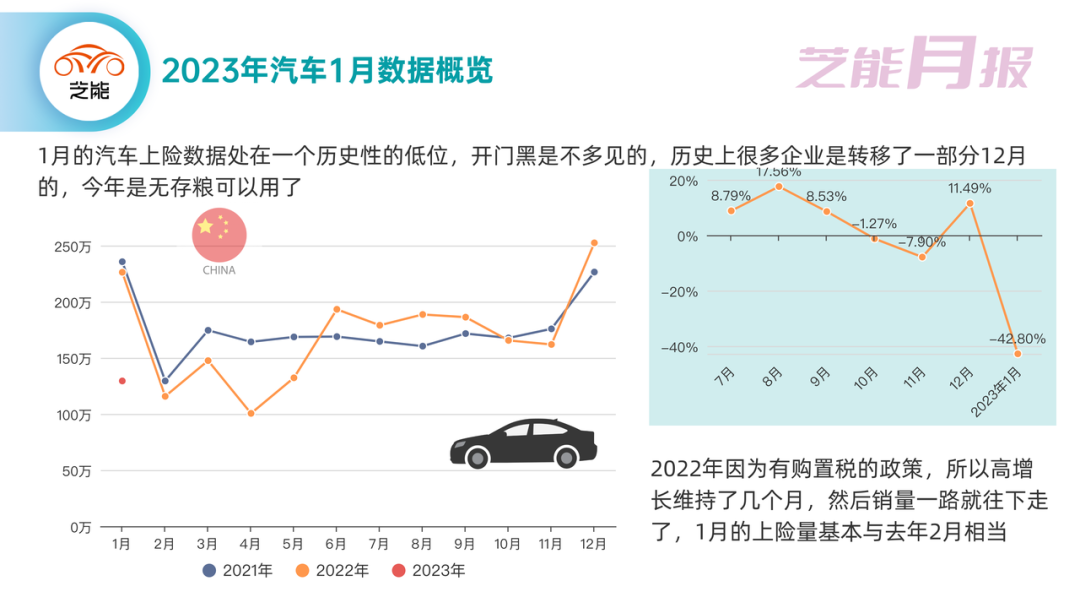

In January, automobile insurance data was at a historically low level, and even compared to the data of February last year during the Chinese New Year, it did not increase much. In the history of Chinese automobile sales, it is rare to have such low sales at the beginning of the year. Many companies in history have transferred some of their December sales to the next year. This year there is no such surplus.

Industry Analysis

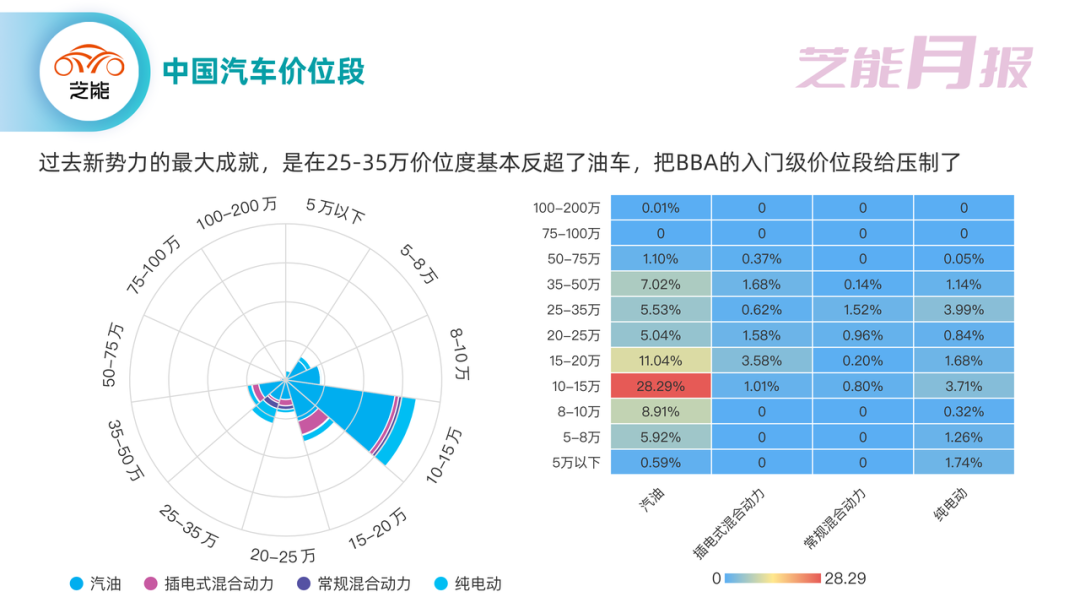

From a hierarchical perspective, China’s car demand follows the United States, moving forward all the way. The similar underlying logic between China and the United States is that they both like larger cars. The United States has lowered fuel prices due to resource endowment, while in China, the promotion of plug-in hybrids and range extenders has led to larger and larger cars. Relatively speaking, the biggest problem in the development of pure electric vehicles in the next step is that the larger the car, the larger the battery required, and the corresponding cost is higher.

The biggest achievement of new energy vehicles in the past was that they surpassed traditional fuel vehicles in the price range of 250,000-350,000 yuan, suppressing joint venture brands. The current development of new energy vehicles is to continuously gain market share in various price ranges of traditional fuel vehicles.

The rise in battery prices in 2022 actually blocked the way of high-end pure electric vehicles. Large batteries mean higher costs, and the pricing of high-end pure electric vehicles is getting more and more expensive, which makes companies less profitable. With Tesla launching a price reduction strategy in 2023, range-extended and plug-in hybrid vehicles with limited power costs will have the opportunity to increase their configurations. Currently, with the price reduction, the main sales range of pure electric vehicles is shifting downwards, and the sales range of PHEV will also shift to a certain extent. However, in the price range of 350,000 yuan, PHEVs are beginning to surpass BEVs.

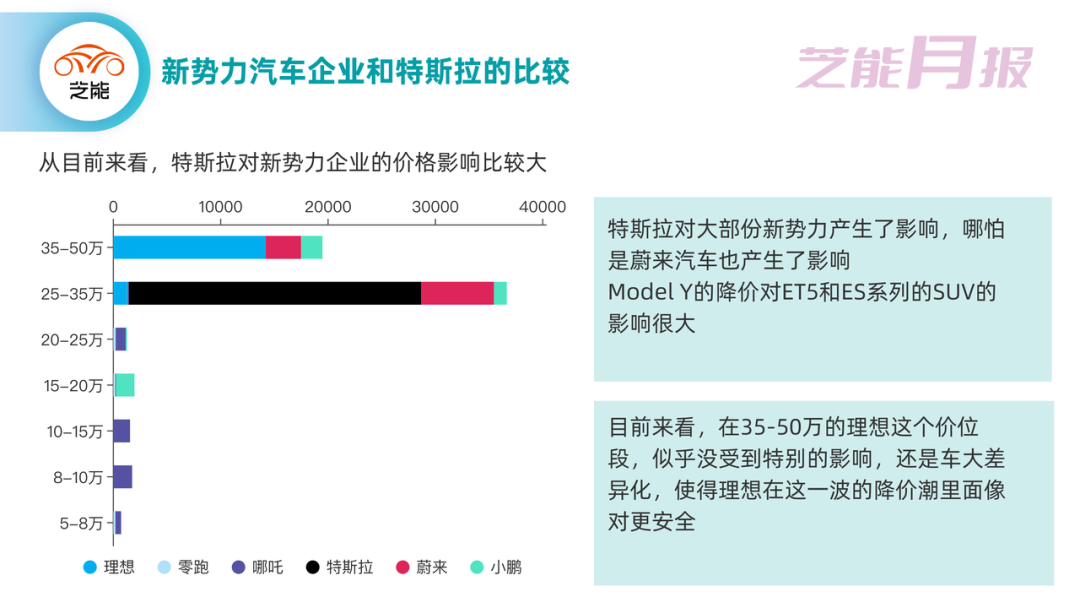

Tesla has had an impact on most of the new energy vehicle companies, even NIO. The price reduction of Tesla Model Y has had a great impact on NIO’s ET5 and ES series SUVs. In the price range of 350,000-500,000 yuan, it seems that there has not been a particularly significant impact, and differentiating the product is still important, making IDEAL safer in this price reduction wave.

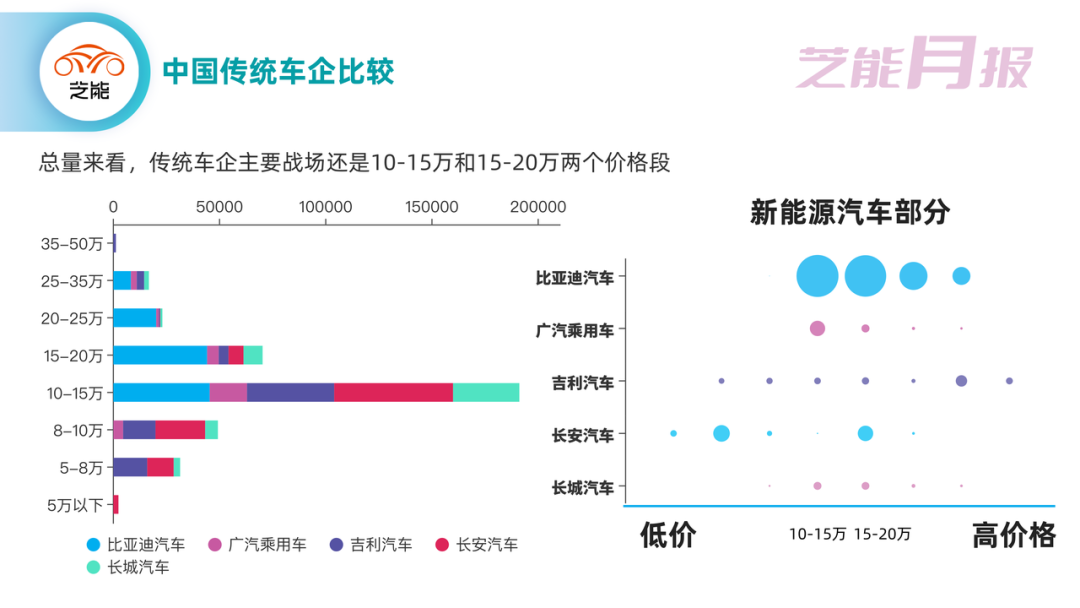

We will continue to observe the annual five companies that we follow in their transformation. The 100,000-200,000 yuan price range is a core competitive interval, especially for 100,000-150,000 yuan models.

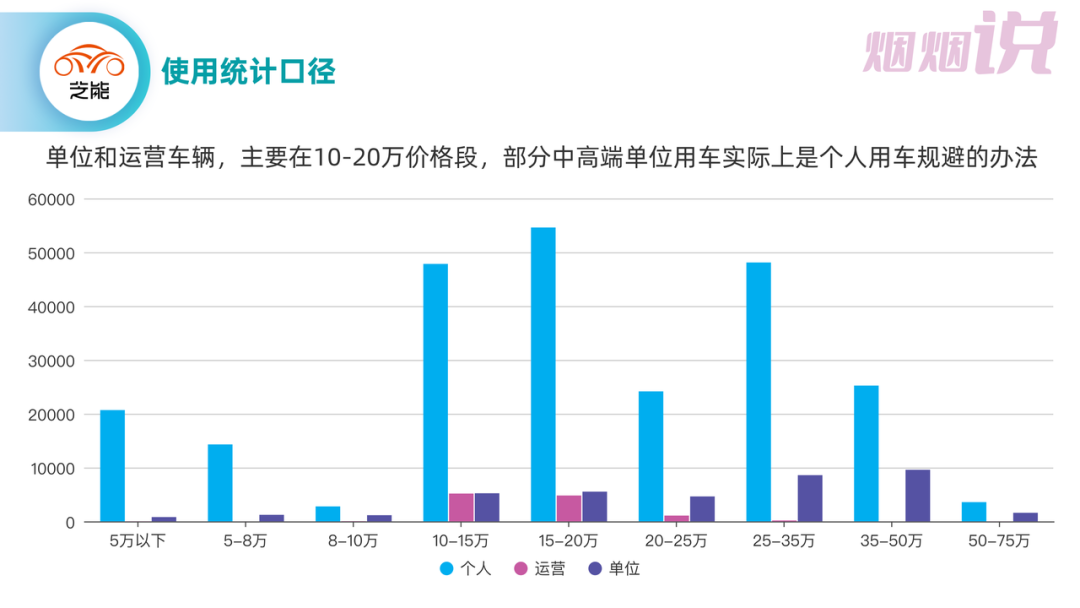

The main units and operating vehicles are mainly in the 100,000-200,000 yuan price range, and some high-end units use cars that are actually transferred from personal cars of business owners.

The main units and operating vehicles are mainly in the 100,000-200,000 yuan price range, and some high-end units use cars that are actually transferred from personal cars of business owners.

Specific Situations of Car Companies

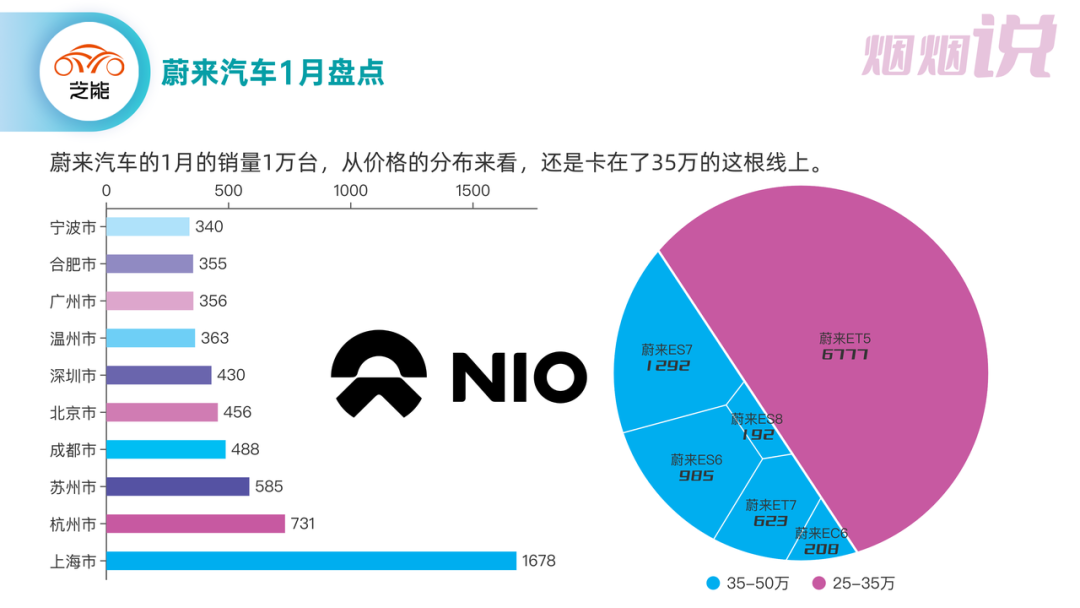

NIO

ET5 is the mainstay – sales in Shanghai have been very hot recently, and it is now relying on the cities of Suzhou, Shanghai and Hangzhou for support.

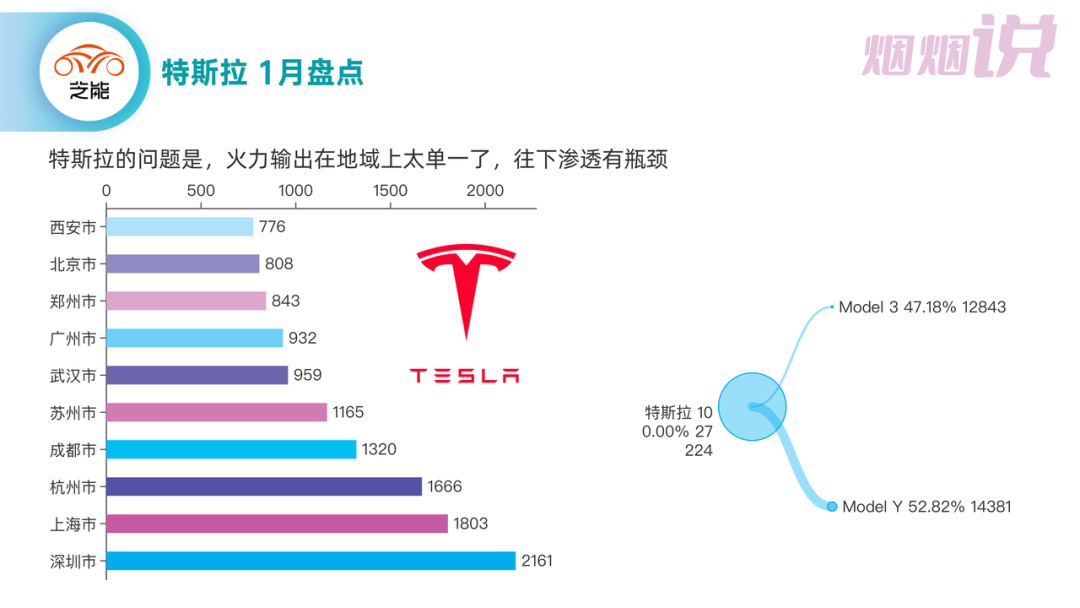

Tesla

Tesla’s current sales range still revolves around big cities, and this round of price cuts has not changed the situation.

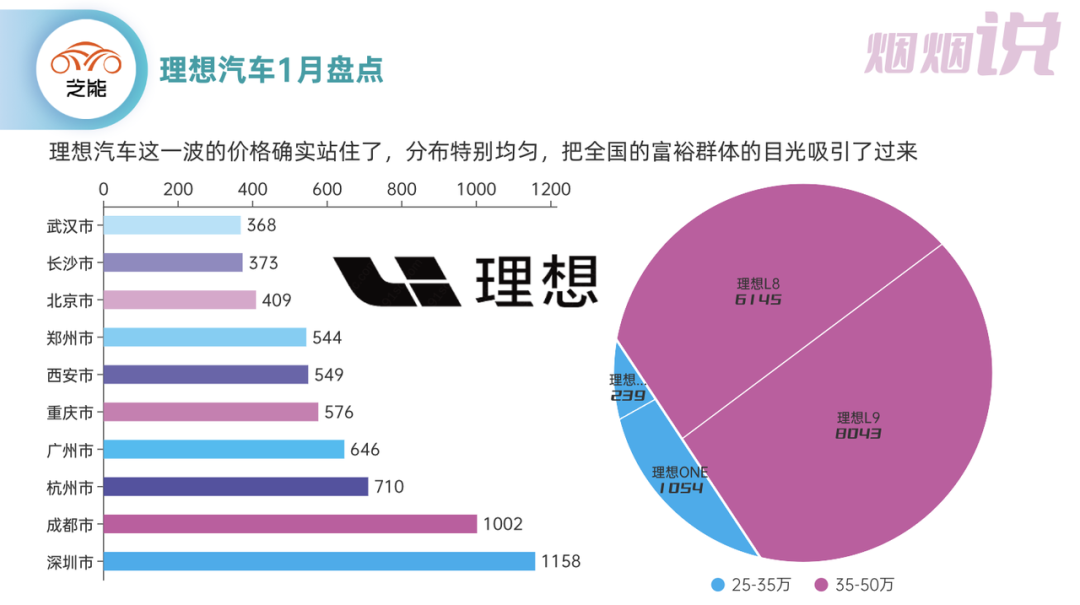

ideal

It has successfully popularized the selling points of car models to the whole country. This round of prices have indeed stood firm, and the distribution is particularly uniform, attracting the attention of the wealthy population across the country.

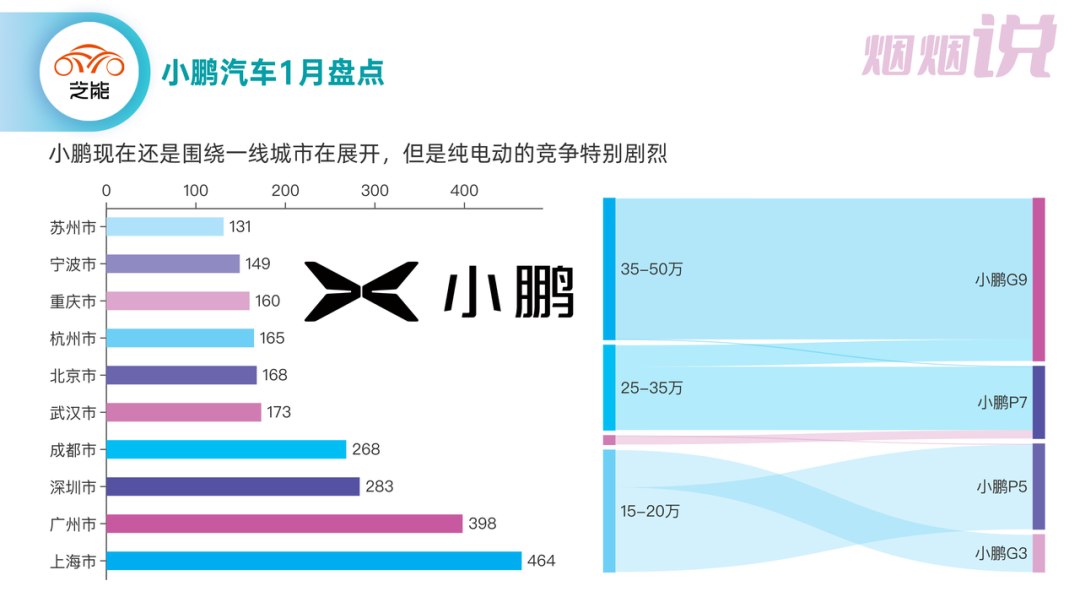

XPeng Motors

XPeng’s price range is indeed too scattered, with a high proportion of G9 in the high price range, and low demand in the low price range. Therefore, it does cover such a wide price range of 150,000-500,000 yuan, and the brand features are completely unclear.

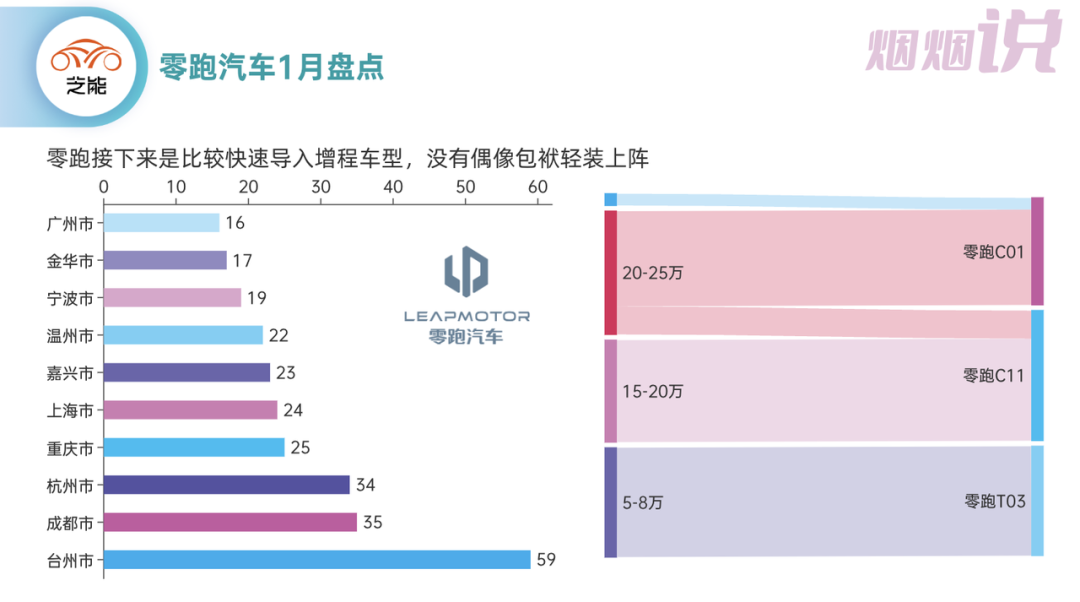

LI Automotive

The actual price of the pure electric C01 is higher than that of the C11, and it is indeed affected by Tesla. LI will quickly introduce extended-range models without idol baggage, which also fits the sales area of LI Automotive.

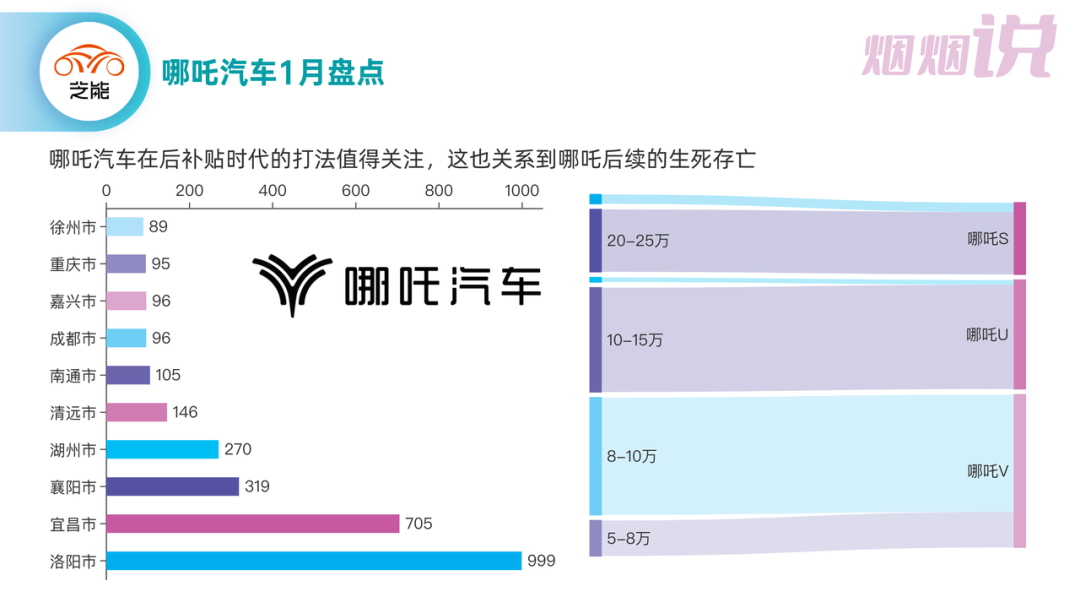

NIO

The challenge for NIO is significant, with both price and consumer recognition being major hurdles. Being too fixated on the inventory sales of the U and V models is not sustainable for their 2023 strategy.

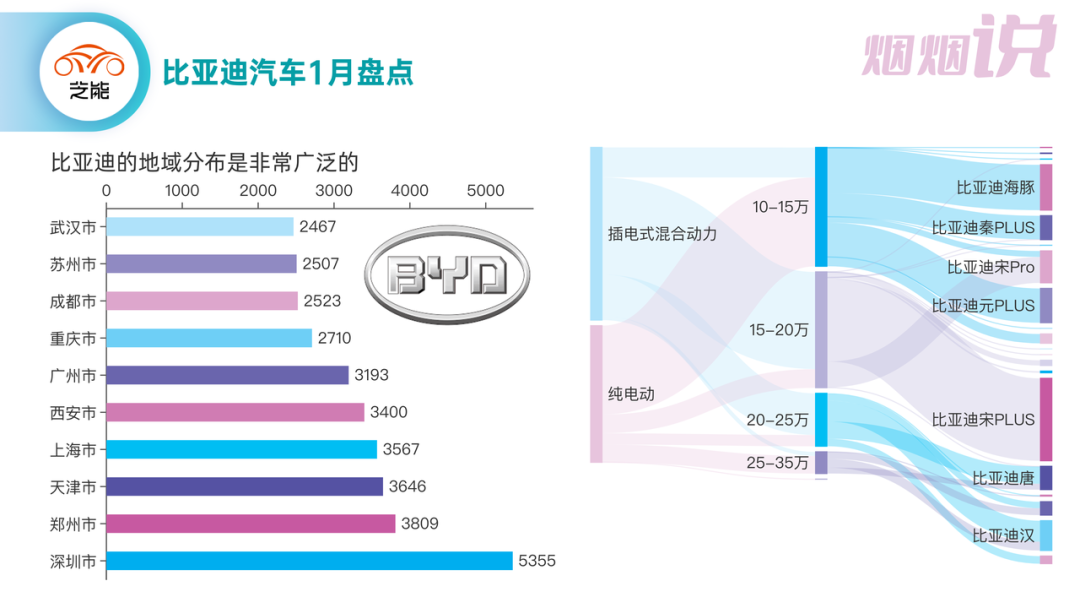

BYD

Objectively speaking, plug-in hybrids have more price advantage than pure electric vehicles. The biggest competitor for BYD is not Tesla, but other traditional Chinese automobile enterprises. The price range of 100,000 to 200,000 yuan is the main theme for our domestic brands, taking the initiative in this main battlefield is time-consuming for joint ventures; it is impossible to let the original dominant traditional self-owned automobile enterprises wait to die in this market.

Conclusion: The first part of the monthly report on the entire vehicle is still focused on some macro content, while the second part will shift the focus to the models to see what interesting discoveries can be made.

This article is a translation by ChatGPT of a Chinese report from 42HOW. If you have any questions about it, please email bd@42how.com.