Sales Report of Chinese EV Brands in 2021

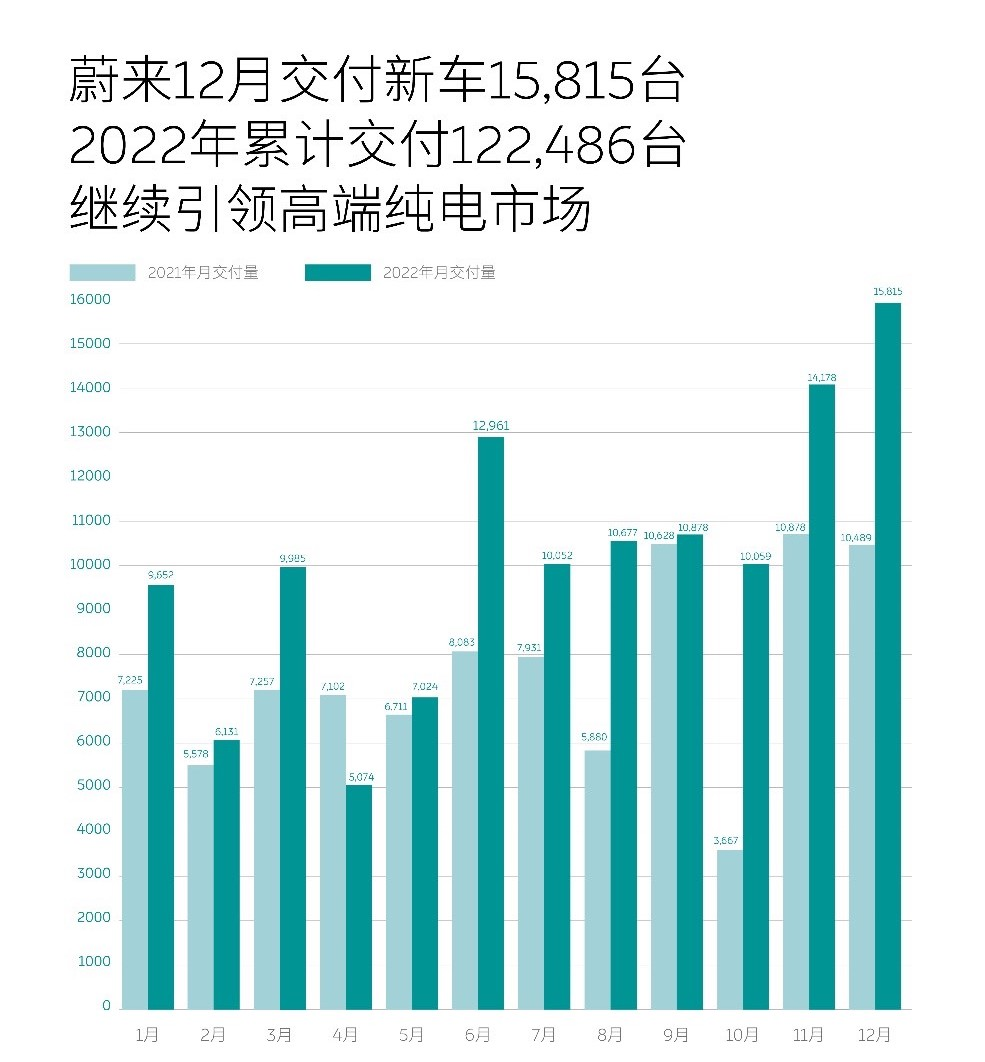

Last year, NIO delivered a total of 122,486 vehicles, representing a 34% YoY growth, and finally exceeded the 100,000 sales milestone.

Among the Chinese new energy vehicle (NEV) brands, breaking through the 100,000 threshold was previously seen as a challenging task. However, it seems that it is no longer as difficult or rare as before.

Xpeng and Li Auto respectively completed 120,800 and 133,200 sales in 2021, while WM Motor made it to 152,100. Furthermore, BYD sold 1.85 million NEVs, and Tesla China estimated 454,000 sales. At least five other NEV brands reached sales over 200,000 units. Meanwhile, WM Motor’s new brand WENJIE sold 76,000 EVs despite being a latecomer.

In terms of absolute figures, NIO has been leading the pack for ages, yet still lags behind new contenders in 2021.

At the same time, NIO’s founder, William Li, has set another goal to surpass Lexus sales by 2023.

Half of his followers think this is just a routine speech to boost stock prices, while the other half believe again that this underdog leader will make an incredible breakthrough.

The essence of the disagreement comes not from whether one supports or rejects NIO, but from a lack of common understanding: What does 100,000 NIO unit sales represent? Are comparing NIO to Lexus appropriate, and if so, what does it entail? In its five years of existence, how deep and far can NIO go on the high-end road?

The First Leading Chinese High-end Automaker

China’s luxury car market proved to be very accommodating to new entrants, and the market consensus is that breaking the 100,000 sales mark is the new “mainstream”. So far, the only challengers are BBA (BMW, Benz, Audi) and Cadillac.

As a second-tier NEV manufacturer, Lexus has been hovering around 200,000 sales for years. NIO’s target of exceeding 200,000 vehicle sales in 2021 accounts for a 63% YoY growth.

It is admirable for a star company to achieve such high growth. Although NIO only had a 34% YoY growth last year, in a rigid sub-segment, every unit sold means a new challenge against established EV players, and therefore every unit is hard-won.

NIO aims to achieve what other mature brands cannot convince Chinese consumers to switch to. For years, only Lexus and Cadillac have been able to achieve sales over 200,000 units.

From an internal perspective, NIO’s 2021 performance does not fully reflect demand, but rather production capacity. Disruptions caused by the pandemic resulted in lower-than-expected sales of the ET5 model. Meanwhile, a generational shift from the first to the second generation requires some debugging, leading to a decrease in sales. These issues will be resolved this year, facilitating better sales performance.By last month, NIO had accelerated through the curve, with a delivery of 15,800 vehicles, an increase of 50.8% YoY, setting a new monthly record. Second-generation products accounted for 83%, almost 78% of the entire fourth quarter, which implies that first- and second-generation products have successfully achieved market deliveries, and more robust releases can be expected.

William Li indicated that by this year’s fourth quarter, NIO’s second-generation products should be fully competitive in the market.

Under the scale, three features are worth noting.

First, the transaction price remains firm, and quantity is not obtained through price reductions. By October last year, the average transaction price of NIO’s entire terminal reached RMB 466,000.

NIO is in the upper range of RMB 400,000, slightly higher than Mercedes-Benz, and far ahead of BMW, Lexus, and Audi. The starting price for the cheapest model, ET5, is RMB 328,000, and the actual average transaction price is close to RMB 350,000. Moreover, the ES6 has an average transaction price of over RMB 400,000. In other words, except for ET5, NIO does not have any models below RMB 400,000. In the pure electric vehicle market above RMB 400,000, NIO’s market share has reached 74%.

Second, high-end sedans have become the new growth point and are gradually gaining ground.

China’s automobile industry has been long suffering from a sedan shortage. The price ceiling for Chinese brand sedans has long been stuck at RMB 200,000.

However, electric vehicles have changed the competitive advantage and consumer trends, with Chinese brand sedans such as NIO ET5, Jinkang 001, BYD Han, and XPeng P7 priced above RMB 300,000 receiving warm welcome. NIO is at the forefront, achieving a high-end surge of over RMB 400,000. Last year, the two sedans, ET7 and ET5, delivered a total of 34,888 units in their first year of deliveries, with a brand share of more than 28%. Among them, 23,075 units of ET7 were delivered at an average transaction price of nearly RMB 500,000.With the opening up of production of ET5, it is expected to boost the sedan sector and form a healthier and more stable growth structure.

Thirdly, fearless competition against the leading market and BBA.

NIO’s leading market is proportional to the level of economic development, per capita purchasing power, and the progress of consumption concepts. The more influential it is, the more it will be taken first, concentrating on the developed cities in East and South China. In Shanghai, for example, ET5 and BMW 3 can be in direct competition.

In fact, BMW is NIO’s first major customer base. A clear benchmark target is progress, which shows that the brand positioning has successfully achieved self-realization.

Although the gap is still evident across the country. This is rooted in the number of stores. NIO only has half of BBA’s store presence. Especially below the third and fourth tier cities, their presence is weak, while this part contributes to more than 40% of BBA’s revenue. In the long run, the experience of running in the first and second tier cities can be replicated down, and the opportunity is at hand.

Four years ago, NIO began delivering its first batch of ES8, delivering 10,000 units aggressively.

At the end of that year, Li Bin, NIO’s Founder, at a capital forum, vigorously defended the question of the carmaker’s quality, stating that NIO should shoulder the mission of promoting Chinese automobile brands because the ES8 is the highest valued individual car in Chinese industrial consumer products.

Although there have been many aggressively priced products released since then, in terms of volume, price, structure, and brand competitiveness, only NIO has formed a consensus among consumers for high-end Chinese brands.

Last year, NIO expanded overseas again, entering four European countries. This is an important piece of the puzzle. According to Li Bin’s prediction, NIO needs to achieve global annual sales of one million in the high-end track to cross the next threshold.

From 100,000 to 1 million, how to get started? Qin Lihong said the starting point is to grasp the trend. Without a trend, NIO cannot become a climate.

Standing at the key point of the track

Grasping the trend is an action plan that is severely underestimated. Most people can only see the rough facts that have already happened.

The next one to three years is a crucial window period for understanding the market pattern.

What is a trend? Qin Lihong pointed out that it is something that cannot be fully seen today, but will definitely happen. Therefore, grasping the trend requires a vision that pierces through time, the courage to bet ahead of time, precise management strategies, and above all, long-term psychological endurance even under skepticism.Just like NIO today, it noticed the coupling trend of high-end demand and electrification back in 2014, and has been building its high-end system competitiveness. Despite many “confusing moves” in the past year, NIO has seen the trend of self-development, vertical integration, and user experience in the industry, in order to build competitiveness in the system three to five years from now.

One of them is self-development. From Day 1, NIO has been persistently self-developing, from the traditional self-developed motor, self-developed ICC, self-developed Design for AD, to the self-developed seat revealed at the end of last year, making it the first domestic automaker to completely independently develop a seat.

Many long-term investments that are currently viewed as burn-and-repeat research will be redeemed as benchmark quality in one to two years.

The recent example is the design of the native lookout tower for autonomous driving, with the lidar leading the way on the roof. It was heavily mocked when it was released at the beginning of 2021, but now many companies are following suit, recognizing the functional aesthetics of standing high and far.

As the leader, not only design confidence in independent aesthetic judgments is required, but also long-term consistent technical solutions. For example, variables that control exterior styling and layout plans are necessary to maintain the same set of data accumulation and meet the shared requirements of different models. Branches will cause operational pressure.

Today, the industry is enthusiastic about the preparation of adding lidar to cars, but NIO has only one. The reasoning behind it is that, in order to demonstrate strength, it adopts five, and will the accumulated data from other options still be useful when future sensor intergenerational evolution occurs, requiring only one or three solutions?

Technical direction should reflect final thinking, strategic determination, and business warmth. NIO’s internal planning requires managing a vehicle for 15 years, until the day it is scrapped. This requires at least 22 years of platform and systematic outlook from the early stages.

This is too difficult to coordinate with suppliers, so we have to rely on ourselves.

For example, the power replenishment system. NIO has currently seven models, whether sedans or SUVs, the physical size of the battery pack and the connection structure were set to use unified specifications in 2016. This posed a great challenge for the body and allowed for cross-model battery swapping, becoming a brand-wide service.

The second is vertical integration. NIO has decided to independently research and develop batteries and chips, and has formed a full-stack self-research team of more than 400 people for batteries and 500 people for chips.

If we exclude the money earned from the battery industry from the money earned from the electric vehicle industry last year, the latter would have negative growth. NIO’s gross profit in the third quarter of the year fell to 13%, which was also a pressure warning.

There are two exceptions in the industry, BYD and Tesla. The inspiration they bring is that core components must be (to a certain extent) vertically integrated in order to provide opportunities for cost optimization and profit improvement.

This is a serious deviation from NIO’s earliest assumptions. For example, with regard to batteries, the original expectation was that costs would decline linearly, but now raw material prices are soaring in an unexpected manner. If the price of lithium carbonate drops to around ten thousand, NIO’s gross margin can still reach 24% to 25%. However, one cannot rely on irrational external conditions to determine one’s fate.

NIO quickly adjusted its strategy and improved its vertical integration. Li Bin has done the math: batteries currently account for nearly 40% of the total vehicle cost. If a battery manufacturer has a gross margin of 20%, self-produced batteries can generate an additional 8% gross margin, and self-developed chips can generate an additional 10% gross margin. Assuming a normal gross margin of 10 points, with self-developed technology, the gross margin can reach 20%. Otherwise, there will be no chance of achieving full-year profitability in 2024.

This is not just accounting fiction. As a result of the first round, a chip specifically developed for LIDAR has already been shipped and will be installed in cars this year, replacing the previous FPGA and saving seventy to eighty U.S. dollars in costs per chip. Despite the high investment, NIO has spent tens of millions and dozens of people on-site, and can still expect efficiency improvements after depreciation.

Third, it’s the digital experience of the mobile internet era. This is the most fragmented part of the NIO system’s competitiveness, running through energy, automobiles, services, and APPs, with the biggest variable being the self-developed phone, which will be launched this year. The interconnection function has been teased on the all-new ES8, and the biggest feature currently is car control.# Li Bin said that NIO doesn’t intend to enter the smartphone race, just like how NIO also does clothing, which doesn’t make NIO a clothing company. So, as a smartphone within the NIO automotive ecosystem, how much value can it generate, or how can it serve the main business?

We can take a look at another “seemingly useless” layout – the NIO App. It has accumulated over 5 million registered users, with over 380,000 daily active users, generating over 20 million high-quality UGC in the past year, serving as a popular community and a platform for media. In the eyes of many, it may just be a way to increase popularity, with no real conversion to sales.

However, based on this private domain traffic, NIO has recently launched the Car Owner Benefit Partnership program. This program opens up the private domain traffic to service enterprise owners who are also NIO car owners, and who operate businesses such as catering, homestays, bookstores, and tourism, providing discounts or exclusive benefits to other NIO car owners in exchange.

NIO won’t charge for the traffic, but just by harnessing the lively energy of small private enterprises and aggregating them, it adds value to the community itself, making it more charming as a brand. Just like how early adopters of NIO viewed it as a school of thought, and not just as a product. As of November last year, the number of online stores reached 3145, with nearly 3000 car owner partners spanning across 137 cities.

This is a result of the system. Without the previous cultivation of stickiness, such as points, APP, NIO Houses, communities, and lifestyles, this cannot be achieved.

Not everyone agrees with these trends, and you can always argue that self-development is a duplication of resources, vertical integration is a sign of poor industrial chain coordination, and digitization is losing money while making noise. They do not provide the ultimate answer, but rather raise a deeper question: where is the industry high ground for intelligent electric vehicles?

In comparison to the traditional era of fuel-powered cars, mature car companies will not give up self-developing the three major parts, as they are the high ground for competition, and independent brands have almost fallen to their knees in this regard.

The high ground of the intelligent electric vehicle industry, whether it be the three-electrics, autonomous driving, or digitization, has yet to be determined. What can be certain is that this will be the strategic value key to the industry chain in the next decade, deciding the judgment of billions of yuan in the five to ten years ahead.

“Since there is no consensus yet,” said Qin Lihong, “let’s turn it into a moat first.”

Blind digging of the river is the treasure of NIO’s founding story. “Eight years ago, we were nobody. There were so many state-owned enterprises, central enterprises, and large foreign enterprises, all of whom were strong and powerful,” explained Qin Lihong. “If everyone had done it, we would not have had the opportunity. Many things in the industry will eventually reach a consensus, but the lack of consensus in the process is the opportunity for new companies.”

In order to seize the next window of opportunity, NIO’s R&D investment is particularly over the current fundamentals, such as investing one hundred million yuan in seat self-production. Starting from the third quarter, they plan to maintain R&D expenses of 3 billion yuan per quarter, which also includes a large portion of losses.

In NIO’s view, R&D is for gaining tomorrow’s possibilities. Thanks to the R&D in 2021, they launched the NOP+ for 2022, and thanks to the R&D 18 months ago, they launched the ET5. Judging from the timing of current investments, NIO’s research and development that caused losses will build a significant leading advantage in three to five years.

Perhaps some friends may say, “Don’t focus on the useless things. They can’t even sell a few cars.” But the more critical issue is that without these useless things, there would be no NIO at all.

Li Bin proposed two formulas for successful high-end marketing.

“First is the spirit and temperament, an independent pursuit, creative leadership ability, and comprehensive systematic thinking. Second is to provide a full-cycle experience that exceeds expectations from the car, services, community, to lifestyles.”

At first glance, all of these seem like emotional elements, but breaking them down reveals that it is a technical activity that runs through design, R&D, operation, service, mode, and even strategy.

For success or failure, whether modest or uncertain, one thing is certain: a story like that of NIO’s is almost impossible to replicate. If a brand is unique, then it is destined to be lonely.

This article is a translation by ChatGPT of a Chinese report from 42HOW. If you have any questions about it, please email bd@42how.com.