作者: Tao Yanyan

Editor’s note: We have selected ten power battery companies based on 2022 data to look ahead to their future development. Among them, foreign companies include LG, SK on, Samsung SDI, and Panasonic; domestic companies include CATL and EVE Energy. Today, we’ll take a look at the second-tier battery companies in China.

In addition to CATL and EVE Energy, when reviewing other power battery companies in China, we can look at the overall supply relationship of domestic power batteries. From 2015 to 2020, CATL seized the opportunity of expanding production and provided battery supply for vehicle manufacturers. However, stabilizing battery supply from 2021 to 2022 relied on vehicle manufacturers monitoring CATL closely – and even talking about pricing and payment conditions for the first time, as the tide has turned. As a result, starting in 2021, we can see the relationship between domestic independent vehicle manufacturers and some global vehicle manufacturers gradually shifting from a single supply to a diversified one of primary, secondary, and even tertiary supplies.

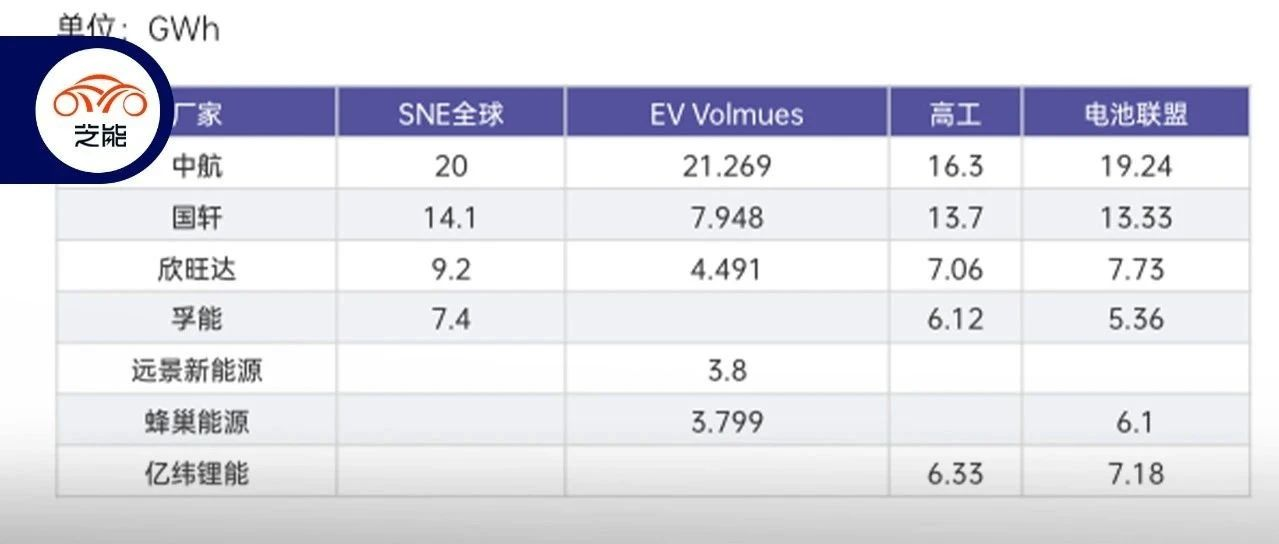

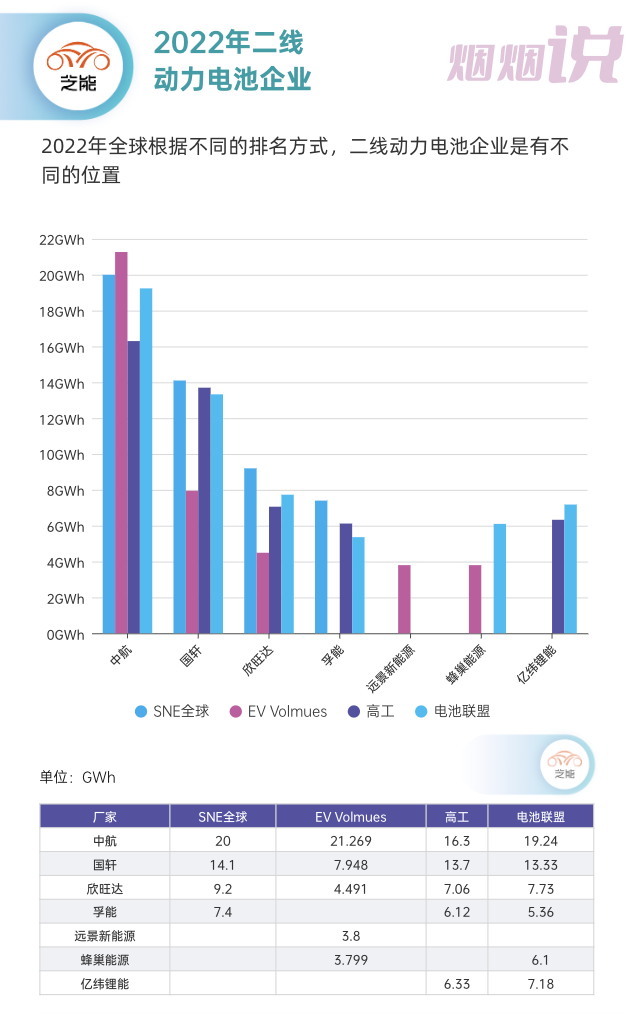

Secondary power battery factories in China can be divided into several categories:

◎ Those that come from the consumer lithium battery sector, such as EVE Energy and XW Power;

◎ Those born out of car companies’ battery business, such as Honeycomb Energy, and later, Yinpai Electric and Juwong Technology;

◎ Those that have been on the road with CATL, such as Farasis Energy, Funeng Technology, and Guoxuan High-tech (backed by Volkswagen);

◎ Those acquired from car companies, such as Anhua Taisen and Hengli New Energy.

Supply relationship of vehicle manufacturers

From the history of automobile companies’ development, in order to achieve stable supply chain and bargaining power, all vehicle manufacturers hope to have backups, that is, to develop qualified suppliers. This is reflected in the supply of first-tier (Point A) and second-tier (Point B) supplies, especially in the balancing and substitution of critical components. This is actually something that is considered during the development stage. If one supplier encounters difficulties during development, the second and third suppliers can immediately take over without delaying the overall development plan of the vehicle model. In fact, in addition to particularly difficult components, the development of supply chains by automakers is also to prevent monopoly by a single supplier and the consequent huge impact on the entire vehicle factory.### Collaboration relationships of China’s second-tier power battery companies

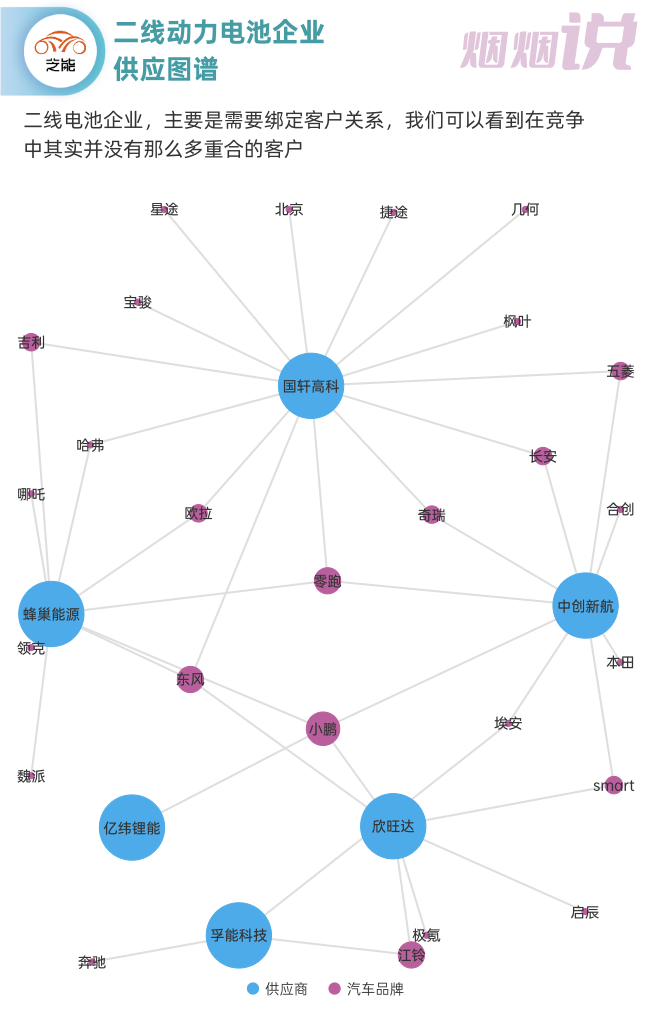

The main supply relationships among China’s second-tier power battery companies include:

◎ Aerospace Creative: GAC and Changan (which entered into capital cooperation agreements with Aerospace Creative), as well as Smart, Wuling, Chery, and SERES.

◎ CATL: Changan, Chery, Wuling, SERES, Great Wall Motors (Haval and Ora), and Geely (Geometry and Maple).

◎ XW Power: Dongfeng, Xpeng, and Geely (Zeekr).

◎ SVOLT: Great Wall Motors (Haval and Ora), SERES, Dongfeng, and NIO.

◎ Funeng Technology: Mercedes-Benz, GAC, and Jiangling Motors.

◎ EVE Energy: Xpeng.

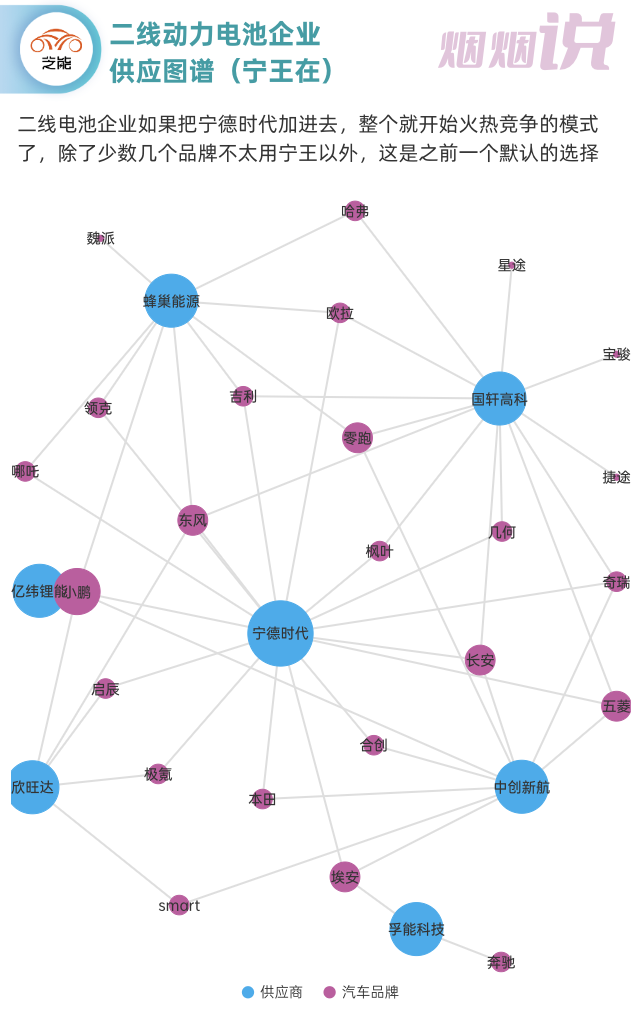

However, almost all second-tier battery companies are still living in the shadow of Ningde Times. If we add Ningde Times, it will open the mode of fierce competition among all of them – except for a few brands, almost everyone has defaulted to choosing Ningde Times. Of course, we should also see that, in the process of bundling second-tier power battery companies with customers in this round, Ningde Times also diverted some customers and seized core clients.

But in 2023, the overall situation is quite special. As we can see, with a large amount of output, battery companies need customers. In the allocation orders of core customers such as NIO and Ideal, there is a certain game.

In fact, we have also seen car companies such as NIO beginning to plan to produce batteries, with two technical routes: “stacked semi-solid soft pack” and “large cylindrical battery.” The whole battery manufacturing process is even more complex than we imagined.

Why does NIO want to produce batteries:

◎ The exploration of the lower end of the first, second, and third brands requires cost-controllable and suitable batteries to support them.

◎ The battery replacement mode can accommodate more products with different technologies, which can be replaced with lower trial-and-error cost.

◎ After the battery asset business is operated, having its own closed-loop battery manufacturing can solve many problems, and the reuse of battery assets has its own battery material recycling.◎Binding with Anhui, the entire industrial park needs to introduce high-value battery business.

Progress in independent and diversified procurement:

NIO plans to build its first battery factory in Hefei, Anhui Province, to produce its self-developed large cylindrical batteries that are similar to Tesla’s previously released large cylindrical batteries. The planned capacity is 40GWh, and the main models of the large cylindrical batteries planned for production in the new factory are the 4680 and 4695 models. For this purpose, NIO has established a company in Hefei, Anhui–NIO Battery Technology (Anhui) Co. Ltd., with a registered capital of 2 billion yuan. As for the team, NIO has an electric battery-related team of more than 400 people, participating in research and development work such as battery material, battery core, and pack design, battery management systems, and manufacturing processes, which is also a part of the reserved resources.

What to Look for in 2023?

In fact, in the stage of rapid development of the industry, theoretically, new entrants have opportunities. However, from 2021 to 2022, second and third-tier battery factories are working hard to finance to create opportunities and have built a lot of capacity. By 2023, it will be a phased problem-the window period of rapid development of the industry’s power battery has passed, and second and third-tier enterprises must seize market share as the capacity expands, or it will be really difficult if there is no customer after the capacity has risen.

From a technical point of view, the technology of using power lithium batteries is already relatively mature, and it is more difficult to make major breakthroughs. The two mainstream directions currently revolve around blades or large cylindrical shapes. We will continue to track valuable enterprises to provide analysis.

Summary: The competition of power battery companies will be a matter of life and death in 2023. In fact, there are many companies that do semi-solid-state and solid-state batteries that will join in. The trend of the battery industry has already been seen this year.

This article is a translation by ChatGPT of a Chinese report from 42HOW. If you have any questions about it, please email bd@42how.com.