Author | Zhu Shiyun

Editor | Qiu Kaijun

There is no sign of stopping the two-month-long price war.

On March 19th, Avita 11 single-motor version was officially released, and the price threshold will be lowered and hit the market on the 24th. Over ten days ago, Aiways launched the Younger version for 119,800 yuan. The new extended-range model of BYD’s Sea Lion will have a 60Kw power reduction and is expected to lower its price to around 240,000 yuan. It is rumored that XPeng P7i has a lithium iron phosphate version as a “backstab” to lower the entry-level price…

From official price cuts, the release of various benefits, large subsidies provided by local governments, to new models with core configuration changes on the market, this price war is different from any of the past.

This is no longer a battle for depleting inventory and seizing market share at the expense of dealer and short-term profits, but a competition and reconstruction of market structure, product value and underlying technical capabilities.

Behind the “bloody battle,” the first-mover advantage for the future is fiercely contested.

How effective is the price war?

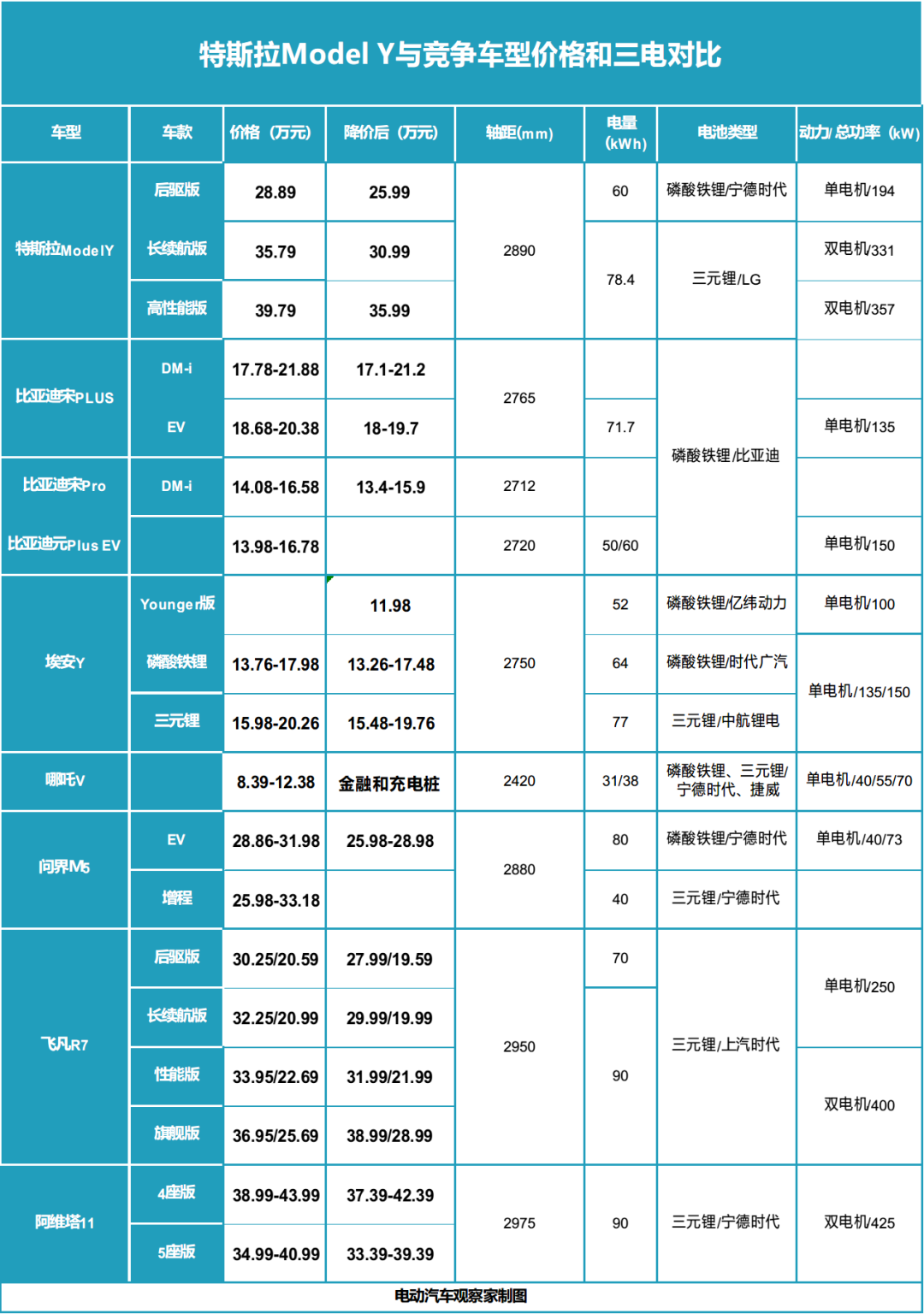

Currently, Tesla’s Model Y prices have been reduced to the appropriate level.

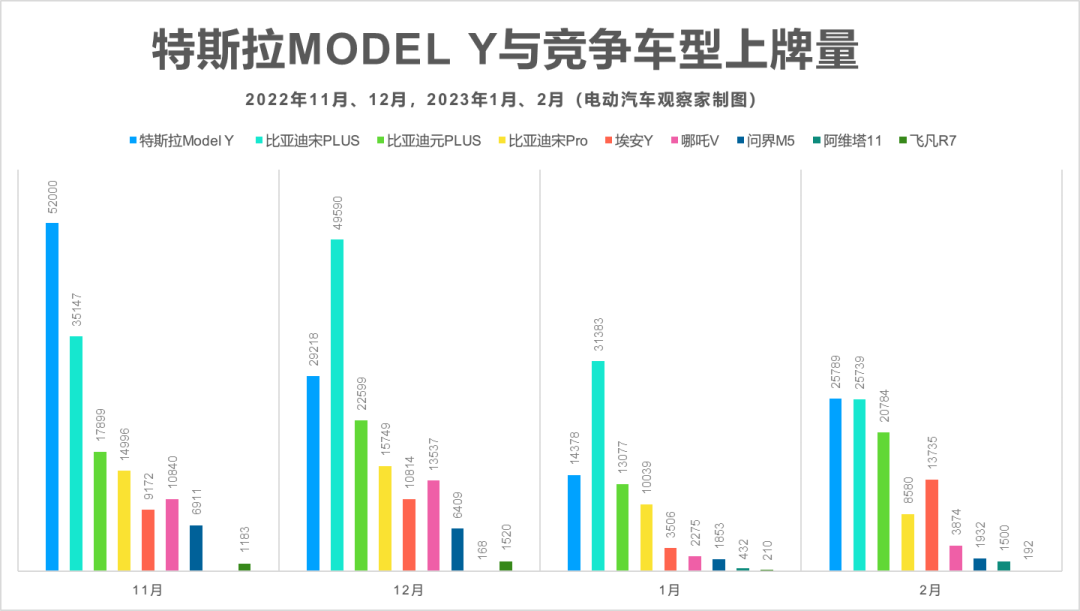

With a decrease of about 40,000 yuan in January, Model Y returned to the trend of “30,000 units per month” in February, which had a chain reaction to its competitors:

The sales gap between BYD Song Plus and Model Y was rapidly narrowed in February;

Quickly responding Aiways surpassed Song Pro in February, and its sales gap with Yuan Plus also narrowed by nearly half;

The intense competition between BYD and Aiways in the 150,000-200,000 yuan segment spread to NETA, which is priced at 80,000-120,000 yuan. The monthly sales of NETA V plummeted from over 10,000 to 3,000 units.

The compact BYD Song/Yuan new energy and Aiways Y are not direct competitors of the mid-size Model Y. However, when the pricing models of new energy SUVs produce new prices, even with a 100,000 yuan price difference, they still have to “follow suit”:“`

Before the price reduction, the price difference between the entry-level Model Y and the top-of-the-line Song PLUS was around 29\%, which later shrank to 21\%, and after BYD’s 6800 yuan discount in March, it expanded to 24\%.

The days of direct competitors of Model Y are even more “difficult”.

In January-February, Wanjie M5, Avitar 11, and Feya R7 all provided actual discounts ranging from 16,000 to 30,000 yuan, but their overall entry-level prices were still higher than Model Y’s 250,000 yuan. However, free “battery swapping” and “option funds” cannot leverage the market: the sales gap between Wanjie M5 and Model Y has widened from 356% in December last year to 1235% in February. The prospects of Avitar 11 and Feya R7 are not optimistic either.

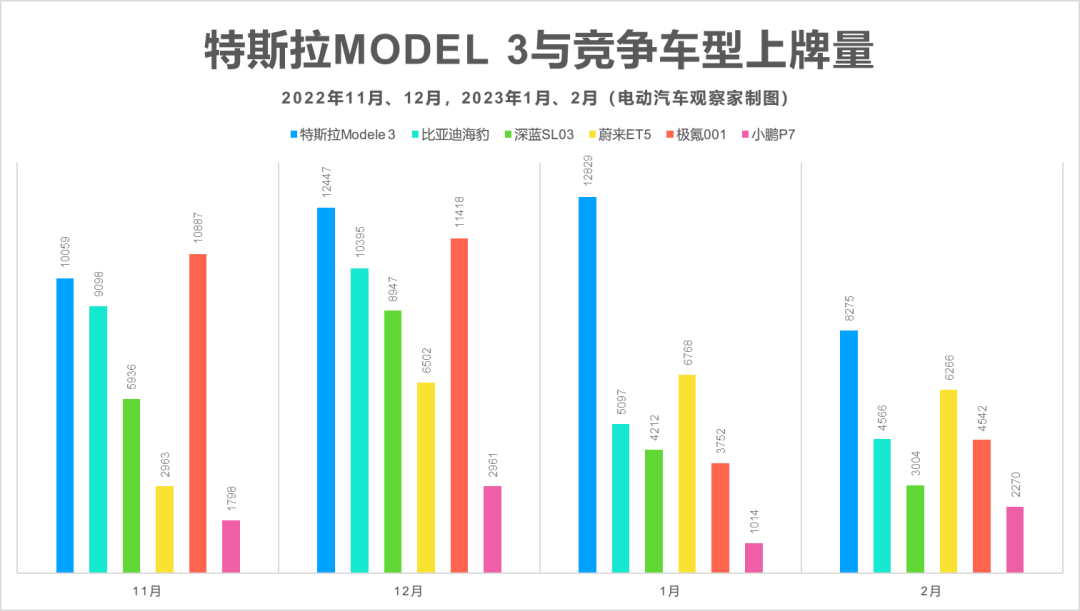

Compared with Model Y, the price reduction of Model 3 has little effect on its sales promotion.

The price reduction of about 30,000 yuan in January only brought a 3% month-on-month growth to Model 3, and the month-on-month decrease was 55% in February.

As a direct competitor, BYD Hanma’s sales were not affected continuously, and the sales gap with Model 3 was 20\%, 152\%, and 81% in the past three months, respectively. The downward trend of Hanma’s February sales of 11.6% was much smaller than that of Model 3.

It is the Deep Blue SL03, which is the “substitute” for Model 3, that was severely affected after the entry-level and top-of-the-line prices of Model 3 almost overlapped. It had stopped its monthly sales of over ten thousand units in January and experienced a larger decline in February.

However, currently, neither direct competitors nor substitutes have made strong reactions to the price reduction of Model 3. In March, Hanma offered 8,800 yuan discount, and Deep Blue offered a discount of 22,000 yuan with a limit of 10,000 units.

## Doing More with Less, Farewell to Overstocking

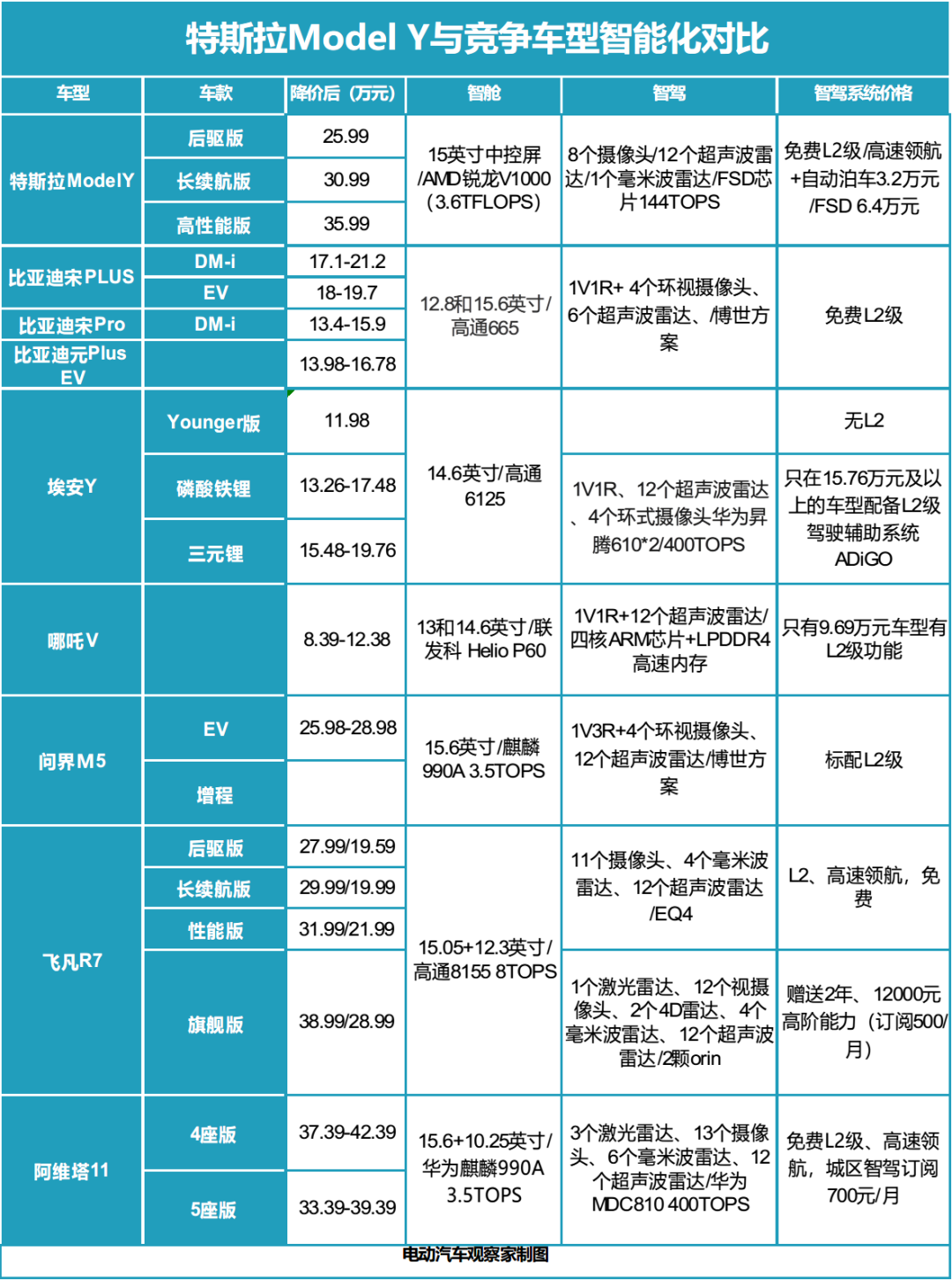

**Where to make cuts? First and foremost, intelligent driving systems that have been heavily overstocked in the past two years.**

In the February plan, the Avita 11 offers a year of city driving function for free (valued at 700 yuan/month); the RisingAuto R7 comes with two years of RISING PILOT fully integrated advanced intelligent driving system software package usage rights (valued at 500 yuan/month); and the XPeng P7i comes equipped with XPILOT and XNGP as standard features (except for the entry-level model).

**Behind the gift/standard features is a change in the business model for intelligent driving from selling software to selling hardware.**

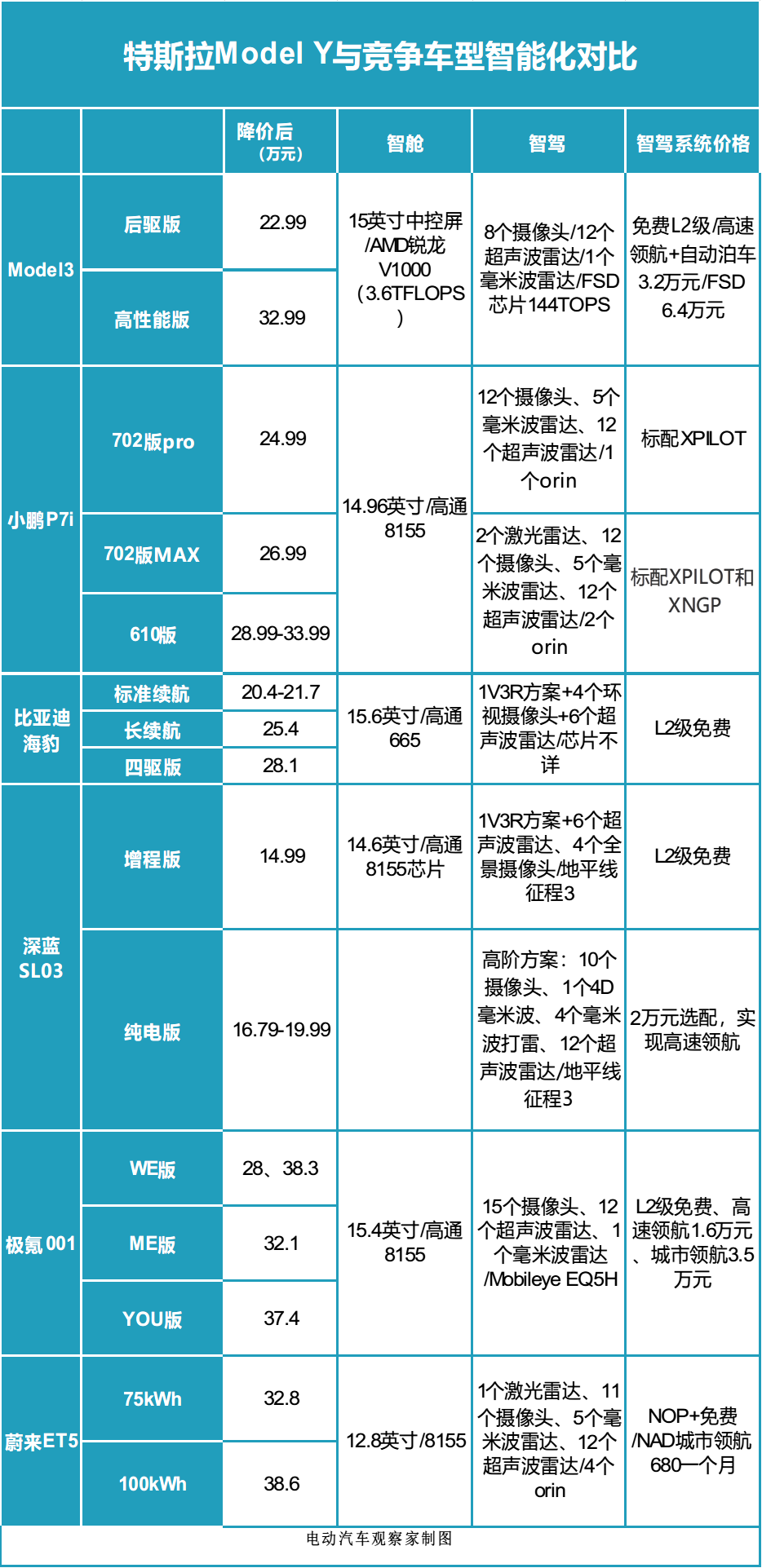

Take the XPeng P7i as an example. The Max model, which can achieve urban navigation, is 20,000 yuan more expensive than the Pro model. It is still unknown whether the possible 220,000 yuan lithium iron phosphate version will only provide basic L2 level capabilities.

**XPeng’s pricing is currently the market benchmark for intelligent driving capability:**

The L2 level basic capabilities are provided for "free", which corresponds to one to two front-facing cameras, one to three millimeter-wave radars, four surround-view cameras, a 10-TOPS chip;

Highway NOA and memory parking function can be added for an additional 20,000 yuan, with hardware upgrades from L2 basic to an 8 million pixel camera and 10-100 TOPS computing power chip;

City NOA and valet parking function can be added for another 20,000 yuan, and hardware upgrades include a lidar and computing power up to 200-500 TOPS.

Currently, the city navigation function, which has yet to be implemented, is still subscription-based, with prices ranging from 500-700 yuan/month. But the already widely available highway navigation and automatic parking functions have become "standard" with hardware.

**Furthermore, cutting high-end intelligent driving hardware directly has also become one of the options for car companies in the price war.**

The RisingAuto R7, which is marketed as the "Screen Master" cabin and the fully integrated intelligent driving "Roll King", has adjusted its prices as follows: The top-level configuration has increased by 20,000 yuan to include one more Orin chip (previously it had one), and one more lidar;

Other models have been reduced by 20,000 yuan, and fatigue monitoring, automatic lane changing, and 4D radar have become optional rather than standard features, and the Nvidia Orin chip has been downgraded to Mobileye Q4H, and 5G networks will be replaced by 4G.

"Users nowadays have a deeper understanding of their needs. We fulfill different user demands through detailed configurations," said Liu Chen, General Manager of User Development Center at RisingAuto.

"Sales volume is not directly impacted by the level of intelligent driving. From a needs standpoint,"

In 2022, Tesla officially stated that only 1-2% of Chinese car owners purchased the 64,000 yuan FSD, and only a few purchased the enhanced intelligent driving function at 32,000 yuan.

For the BYD, YeeOn, and DeepBlue models in the 150,000-200,000 yuan range, the main focus is on the 1V1R, 1V3R Bosch L2 level intelligent driving function, which costs 2,000 to 3,000 yuan.

The Zeekr001, in the 300,000-400,000 yuan range, uses the Mobileye EQ5 plan with only 48TOPS, and the high-end intelligent driving system sells for 16,000 and 35,000 yuan, but still surpassed 10,000 units sold monthly last year.

"Insiders reported to the \"Electric Vehicle Observer\" that laser radar orders from car manufacturers are being drastically reduced this year."

"Selling hardware but not software: the fundamental reason for reducing intelligent driving hardware during difficult times is that the technology is not yet perfect, and after redundancy is piled up, there is still a risk of low actual usage rates, resulting in users who \"spend 1000TOPS but get 50TOPS worth of functions\", making it difficult to form a real selling point to support the price."

"As the price war intensifies, the end of the stacking competition for intelligent driving and the beginning of a battery and electric motor competition in electrification may be the next step."

## Technology-Driven Cost Competition

"Ending the terminal stacking competition does not mean that car manufacturers will stop competing in electric and intelligent technology. In fact, the difference in this price war compared to previous ones is that the initiator is not fighting a 'war of attrition.'"

As of Q4 2022, Tesla's automotive business gross margin was 25.9%. Therefore, if Tesla is willing to erase its margins to achieve this year's 30-40% growth target, there is still about 17% reduction potential globally. In contrast, the highest discount in January was only 13.5%.```

In other words, even with such a price war butcher, Tesla is still making a profit. At the same time, Tesla FSD beta version has been pushed to 400,000 vehicles in North America with a good response. The first batch of imported Model S/X in China this year has been updated to HW4.0 hardware.

The 25% gross profit margin on automobiles and the 90% gross profit margin on FSD deferred revenue are the source of Tesla's confidence in this price war. But fundamentally, high gross margins on software and hardware are based on Tesla's innovation and transformation of underlying technology in automobile products, manufacturing, and autonomous driving.

Integrated casting of major components significantly improves Tesla's assembly efficiency; if the 4680 battery assembly runs smoothly in production, it will further enhance Tesla's efficiency and cost-effectiveness.

The electronic and electrical architecture of central computing + regional control allows the Model Y's harness to be only 1.5 kilometers, one-tenth of the distributed architecture of a fuel vehicle, saving costs and improving assembly efficiency.

Li Xiang, founder of Ideal Auto, pointed out directly in a previous communication meeting that the cost of Tesla's autonomous driving hardware system is $1,000, while Ideal, known for its cost control, is at $4,000.

Therefore, Chinese companies must face Tesla in this enduring price war, not only for short-term profits or even cash flow, but also for catching up with and innovating on underlying technology.

Currently, including Geely, XPeng, and Nio have already implemented the integrated casting production technology for major components; multiple Chinese auto companies have invested or plan to invest tens of billions of yuan to rent or build their supercomputing centers for training and iterating automated driving models. This year, Chinese auto companies based on the SOA architecture domain control electronic and electrical system architecture, vehicle operating system architecture, and urban navigation functions will begin to be implemented on a large scale.

This price war may be unprecedentedly fierce and "bloody," questioning the overall product, technology, and system capabilities of companies, and even becoming the final "elimination game" for many companies. However, "survival" is not the ultimate goal, but the upgrading and iterations of technology and industrial systems are what everyone hopes to see as a result of the battle.

我的博客

欢迎来到我的博客!这是一个用于分享我的想法和经验的地方。

最新文章

最近感兴趣的主题

- 技术

- 学习

- 旅游

如果你对我的博客感兴趣,请订阅我的 RSS feed。

照片

My Blog

Welcome to my blog! This is a place for me to share my thoughts and experiences.

Latest Posts

Recent Interests

- Technology

- Learning

- Travel

If you’re interested in my blog, please subscribe to my RSS feed.

Photo

This article is a translation by ChatGPT of a Chinese report from 42HOW. If you have any questions about it, please email bd@42how.com.