Special Contributor | Enjoyable Experience

Editor | Qiuka jun

The new energy price reduction wave since the beginning of 2023 has begun to spread throughout the entire auto market.

On March 6th, “Hubei launched the strongest car purchase discount season in history”, and many models of Dongfeng joint venture and independent brands began a “crazy clearance sale mode”. Among them, Dongfeng Citroen C6 has the highest discount of 90,000 yuan. The original 200,000-level model can now be purchased for 120,000 yuan, almost half of the original price.

Today, let’s talk about the reasons behind the “fuel car price reduction”, what has caused it? Of course, if you want to know the industry logic behind the new energy price reduction wave, please refer to our previous article: “The Coming Price Reduction Wave, Who is the Most Anxious?“.

The new car consumption market in January and February is too weak

On March 8th, the China Association of Automobile Manufacturers released the latest data: in February, the production of passenger cars was 1.664 million units, a year-on-year increase of 11.6%, and a month-on-month increase of 23.6%; manufacturers’ wholesale sales were 1.618 million units, a year-on-year increase of 10.2%, and a month-on-month increase of 11.7%; passenger car retail sales reached 1.39 million units, a year-on-year increase of 10.4%, and a month-on-month increase of 7.5%; passenger car exports (including complete vehicles and CKD) were 250,000 units, a year-on-year increase of 89%, and a month-on-month increase of 8%.

At first glance, whether it is year-on-year or month-on-month, this set of data shows positive growth. However, it should be noted that the Chinese Spring Festival in 2022 was from February 1 to 6, while the Chinese Spring Festival in 2023 was in January. Therefore, both year-on-year and month-on-month data are actually distorted.

If we merge the data from January to February and view it as a whole, we can see how weak the market for new car consumption is.

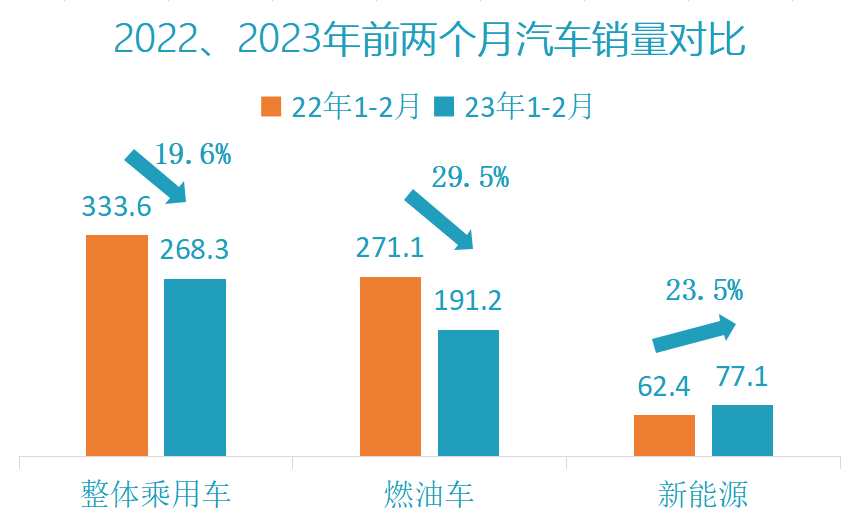

The overall retail sales volume of passenger cars in January and February 2023 was 2.683 million units, compared to 3.336 million units in the same period last year, a year-on-year decrease of 19.6%; among them, the retail sales volume of fuel cars was 1.912 million units, compared to 2.711 million units in the same period last year, a year-on-year decrease of 29.5%; the sales volume of new energy vehicles was 771,000 units, compared to 624,000 units in the same period last year, a year-on-year increase of 23.5%.The penetration rate of new energy vehicles in January-February 2023 was 28.7%, an increase of 10 percentage points compared to the same period last year, which was 18.7%.

It can be said that except for new energy vehicles, the sales data in the first two months can maintain positive growth, and the sales of fuel vehicles are accelerating their decline.

After reviewing the data from the China Association of Automobile Manufacturers (CAAM), and in conjunction with the latest insurance coverage data, it can be seen that the terminal performance of the first two months of 2023 is weaker.

We compared the latest insurance coverage data from January 1 to March 5, 2023, with the data from January 1 to March 6, 2022 (although there is a difference of one day, it has little effect on the overall data and trend).

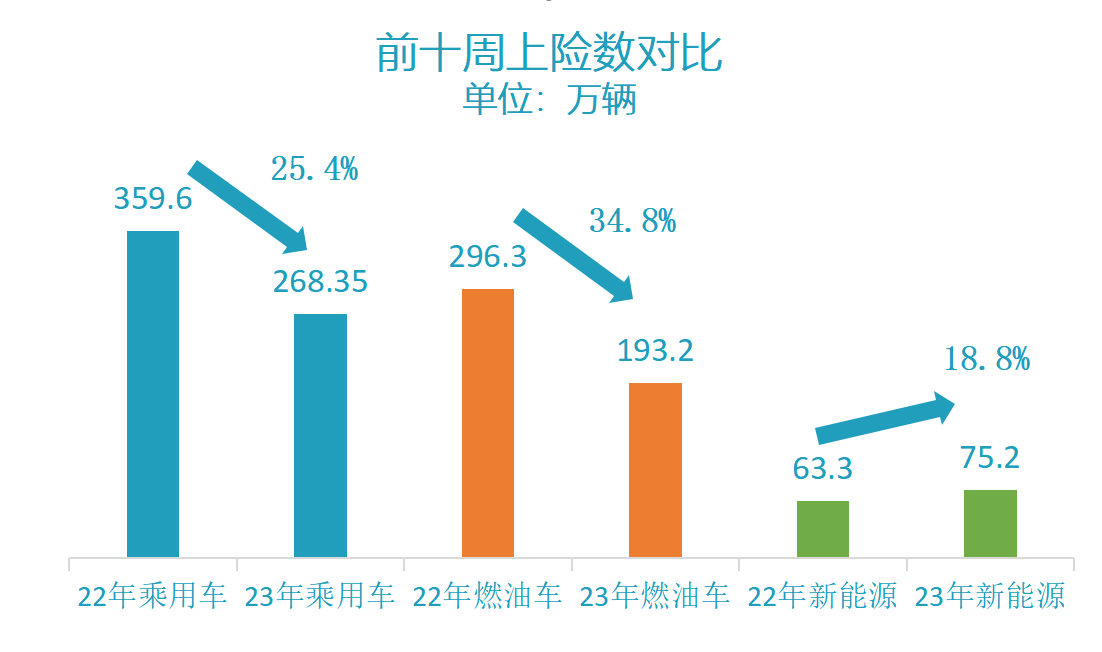

Data for the first ten weeks of 2023 shows that the overall passenger car terminal sales were 2.684 million units, compared to 3.596 million units in the same period last year, a year-on-year decrease of 25.4%; among them, the terminal sales of fuel vehicles were 1.932 million units, compared to 2.963 million units in the same period last year, a year-on-year decrease of 34.8%; and the terminal sales of new energy vehicles were 752,000 units, compared to 633,000 units in the same period last year, a year-on-year increase of 18.8%.

The new energy vehicle penetration rate in the terminal for the first ten weeks of 2023 was 28.0%, an increase of 10.4 percentage points compared to the same period last year, which was 17.6%.

Through these two sets of data, it can be seen that: firstly, the overall market has declined by more than 20% year-on-year, which is sufficient to illustrate the weakness of the new car market at the beginning of 2023; secondly, the substitution of new energy vehicles for fuel vehicles has become mainstream; thirdly, the overall foundation of the fuel vehicle market is rapidly “collapsing”.

The substitution of new energy vehicles for fuel vehicles has become mainstream

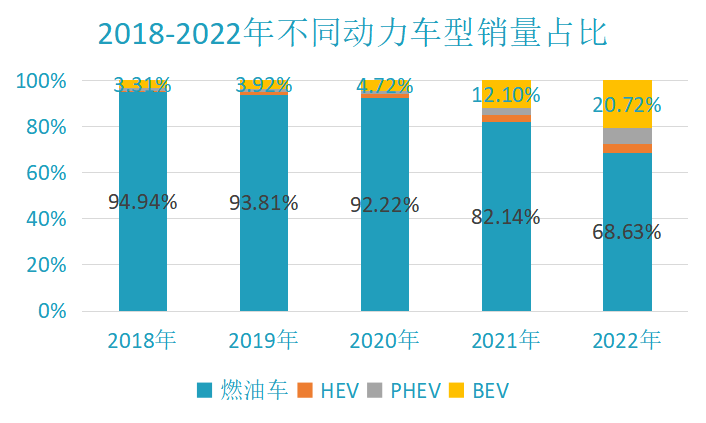

- In the last five years, the sales of fuel vehicles have continued to decline.

According to the China Passenger Car Association’s retail sales data, in 2018, the sales of fuel vehicles were 21.22 million units, accounting for 94.9%, and then they have continued to decline for four years in a row. By the year 2022, the sales of fuel vehicles were only 14.11 million units, accounting for 68.6%. In five years, the sales of fuel vehicles have declined by 33.5%, and their market share has declined by 26.3 percentage points.

Especially after entering 2022, fuel vehicles have experienced a wave of accelerated decline, and this achievement was still made after the policy of halving the purchase tax for fuel vehicles was added.

Especially after entering 2022, fuel vehicles have experienced a wave of accelerated decline, and this achievement was still made after the policy of halving the purchase tax for fuel vehicles was added.

Fuel vehicles have already become the most disadvantaged one in the “unprecedented great changes of a century”. What’s more important is that this decline will be all-round from 2022.

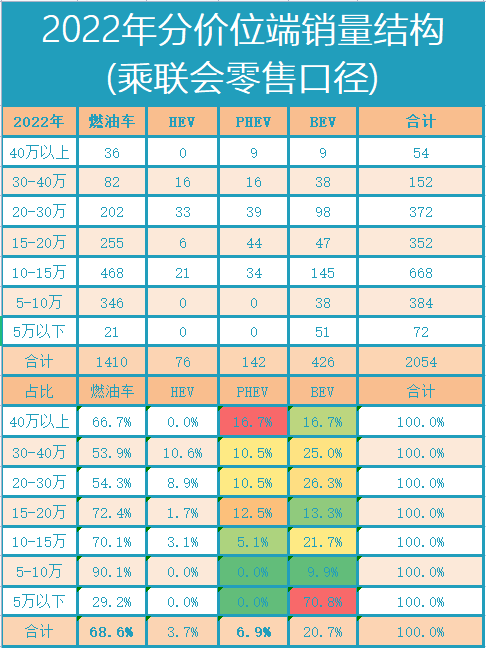

- After 2022, new energy vehicles will replace fuel vehicles in different price segments.

If before 2022, the replacement of new energy vehicles for fuel vehicles was mainly concentrated in the “dumbbell-shaped” market, on the one hand, in the micro-car market below 50,000 yuan, A00 pure electric vehicles represented by Wuling Hongguang MINI EV have rapidly exceeded one million in sales. On the other hand, in the high-end market above 300,000 yuan, the new forces represented by Tesla+Li Auto have also begun to rise rapidly.

So after entering 2022, new energy vehicles will rise in different price segments, and even the traditional fuel vehicle market segment with the highest market share of 50,000-150,000 yuan will be further diverted due to the hot sales of BYD’s A-class plug-in hybrid sedan and A0-class pure electric sedan.

Especially in the price segment of 200,000-400,000 yuan, the sales share of new energy + HEV models has begun to approach the share of fuel vehicles.

The main market space of fuel vehicles has been suppressed in the sub-segment markets of A-class and B-class fuel vehicles, which are mainly traditional fuel vehicles, with prices ranging from 50,000 to 200,000 yuan.

- New energy fully replaces fuel vehicles

Looking at the overall market situation from early 2023, we will find that the market’s recognition of fuel vehicles and new energy has undergone a complete change—from new energy being a trend to “new energy being mainstream”.

The core reasons are mainly the following two points:

First, the experience of new energy vehicles subverts that of fuel vehicles:

In terms of use cost, driving experience, and intelligent cockpit experience, new energy is a crushing level of existence for fuel vehicles. Especially the “large battery + plug-in hybrid” technology combination brings the experience of “city electricity and long-distance oil” which is a “reduced strike” for traditional A-class and B-class fuel vehicles.

On February 10th, after BYD launched the Champion Edition Qin Plus-DMi priced at 99,800 yuan, it thoroughly shattered the illusion of traditional joint venture fuel vehicle clearance sales. With the “oil-electricity same price” strategy.

Second, the restructuring of the value of new energy vehicles:

In the traditional fuel vehicle system, whether it is a luxury brand or a joint venture brand, the main consumer perception of power and value is based on the “engine + gearbox”, forming the following value perception chain (or contempt chain) – V12 > V8 > V6 > V4.

However, in new energy vehicles, power is no longer scarce. When basically any four-wheel drive vehicle with dual motors can run into the 5-second club, the “technology premium” for joint venture and luxury brand fuel vehicles is completely shattered.

When all consumers start to pay more attention to “smart cockpit” as a representative of intelligence, it has already declared the “informal death of fuel vehicles.” Luxury brands that cannot provide remote OTA, remote control, and even good in-car navigation will only be left with their interior refinement and brand logo to hold onto when their last fig leaf of “brand premium” is completely eliminated by the entirely new value system constructed by new energy vehicles.

Starting from 2023, we will see new energy vehicles replace fuel vehicles in all aspects (from A00 to C-class), all price ranges (from 50,000 to 500,000), and all forms (from SUVs to sedans and MPVs). For many luxury brands, when “technology premium” and “brand premium” no longer exist, only decline, continued decline, and accelerated decline awaits them.

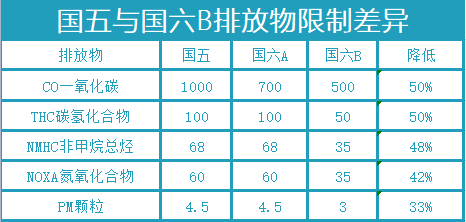

The National VI B standard becomes the last straw to crush fuel vehicles

As early as 2020, the phased implementation time of National VI standard was announced: National VI A was officially implemented on July 1st, 2020, and National VI B will be officially implemented on July 1st, 2023. The biggest difference between National VI A and National VI B is that the emission requirements have been greatly increased, especially in National VI A where many indicators are the same as National V, but National VI B has a significant improvement.

Actually, in terms of policy announcement and preparation time, sufficient time has been reserved for the industry. However, if we look at it from the perspective of inventory, it is not the case.

According to data released by the China Automobile Dealers Association and China Passenger Car Association as of February 2023, the inventory of the overall passenger car market (calculated as production minus retail sales minus exports) was 3.01 million vehicles, which was a decrease of 540,000 vehicles from the end of December 2022. However, such inventory still reached 65 days, which is more than two months of inventory (equivalent to a sales-to-inventory ratio of 2.24).

If we further break down the inventory structure, the inventory of new energy vehicles is at the level of 450,000 vehicles, which is equivalent to a sales-to-inventory ratio of less than 1.

The inventory of conventional fuel vehicles has reached around 2.5-2.6 million vehicles (excluding some HEV inventory). According to the sales data of fuel vehicles in 2023, the sales-to-inventory ratio has exceeded 2.4. Even if we look at the level of monthly sales of 1.2 million vehicles in 2022 (1411 divided by 12 months), the pressure on the inventory of 2.5 million fuel vehicles is still very high (sales-to-inventory ratio of 2).

This means that if all fuel engine factories stop producing fuel vehicles from March, the inventory of 2.5 million vehicles can still maintain fuel vehicle sales for the next two months. Not to mention, these 2.5 million inventory of National VI A models must be destocked before July 1, otherwise they will be trapped in their own hands.

On the one hand, the automobile industry is a pillar industry for many cities (combining employment and tax revenue); on the other hand, a large inventory of National VI A fuel vehicles must be sold within the specified time.

These two factors together have made National VI B, after new energy, the last straw to crush fuel vehicles.

Therefore, we can see the “fuel vehicle big sale” model in Hubei. In the future, we will also see some traditional fuel vehicle provinces follow the “fuel vehicle price reduction tide”, such as Anhui, Geelyn, and so on.

2023: Both Sorting Winners and Losers While Deciding Life and DeathIn 2023, it is a year of “division and life-or-death” for the entire Chinese passenger car market — the traditional fuel vehicles have already entered the twilight, and new energy vehicles begin to emerge as the mainstream.

When new energy vehicles establish their sufficient advantages in experience and value, it will not only be the “technical value” of internal combustion engines and transmissions that are declining alongside fuel vehicles, but also the “brand value” of many luxury brands that will suffer heavy blows.

It is not only the decline in sales and price collapse that awaits fuel vehicles, but also the “obliteration and reconstruction” of brand premium.

This article is a translation by ChatGPT of a Chinese report from 42HOW. If you have any questions about it, please email bd@42how.com.