Author: Tao Yanyan

Editor’s Note: Zhi Neng Monthly Report is officially launched, mainly divided into five sections: whole vehicle (domestic Part1, domestic Part2, Europe, America), battery (domestic, overseas, energy storage), charging, electric drive and intelligentization.

Introduction to the Electric Drive Report: Some analysts believe that electric drive technology is the next big thing, and we are also curious to know whether great companies will emerge in this field. Next, this report will mainly discuss the new energy passenger car electric drive system in January 2023. There are different sources of data about electric drive technology:

According to the data from NE Research Institute:

-

In January, the shipments of three-in-one and multi-in-one systems (electric drive systems) for pure electric passenger cars were 188,000 sets, a year-on-year decrease of 9.7%.

-

In January, the shipments of motors were 337,000 sets, a year-on-year decrease of 3.5%.

-

In January, the shipments of electronic control units (ECUs) were 336,000 sets, a year-on-year decrease of 3.3%.

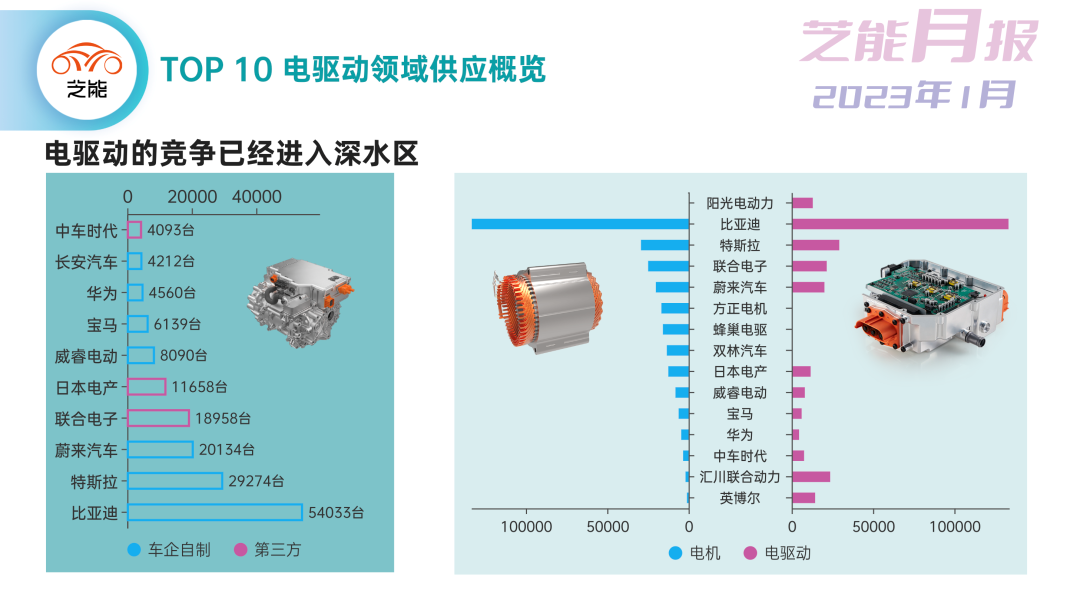

While according to the data from Corder Insight, the top 10 electric motor and electric drive companies shipped 251,000 and 259,000 units respectively. The main differences between the two calculation methods are whether to consider the four-wheel drive system and whether to include the dual-motor system in PHEVs.

Note: We understand that the dual-motor system in PHEVs is not included here. If we calculate the dual-motor system in PHEVs, the whole quantity comparison will be more complicated.

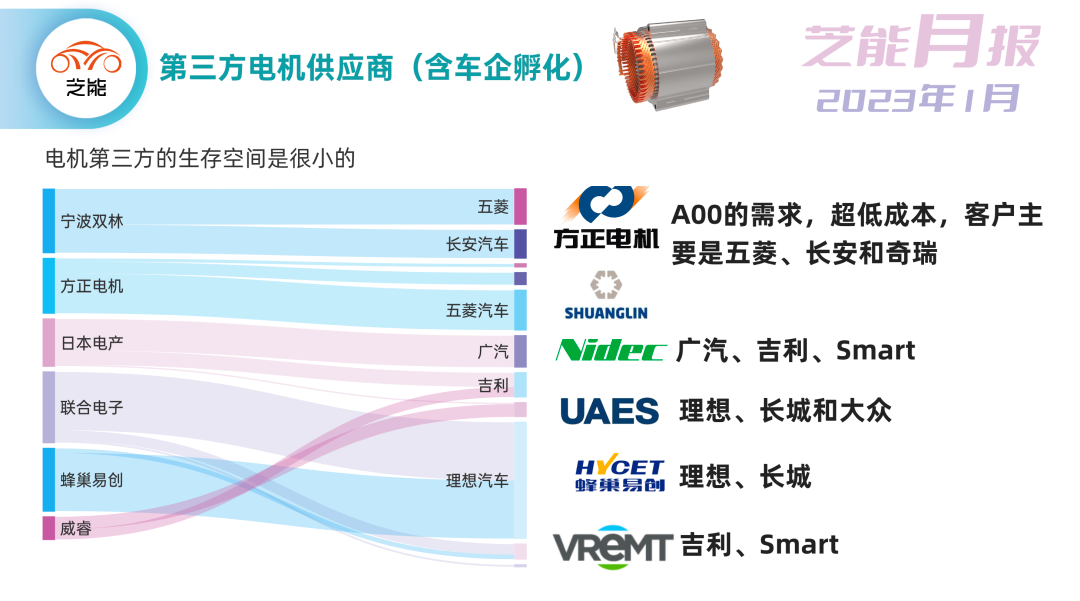

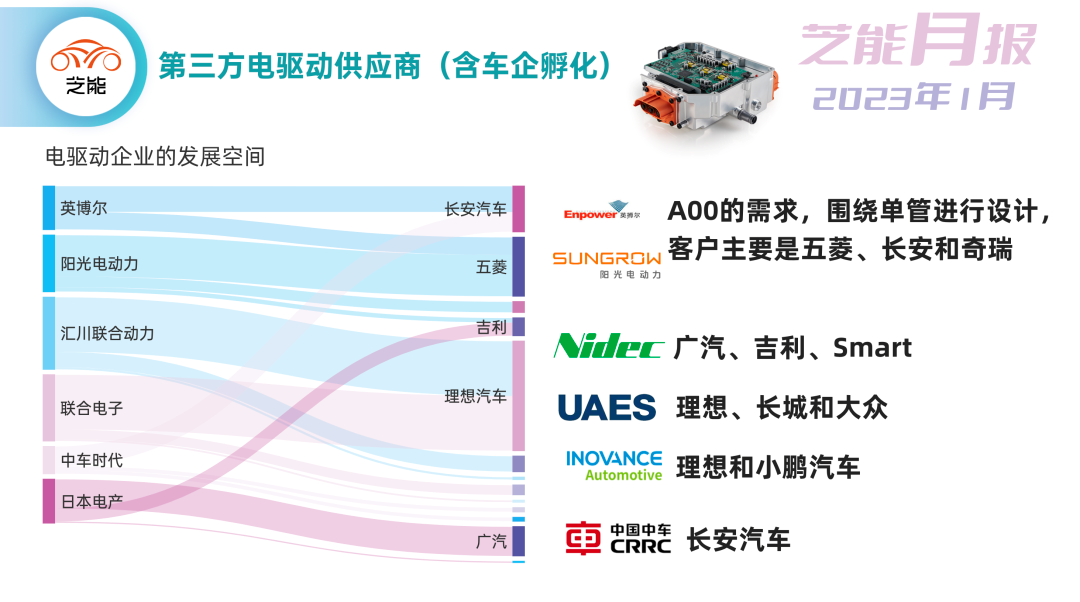

We can see that currently in the electric-drive field, automakers and companies incubated by automakers dominate the leading position; third-party electric-drive companies only have a small survival space in the market of A00 low-power motor vehicles and limited standard products.

Discussion on the Breakdown of Motor and Electric Drive Demands

1) Breakdown of Data in the Motor Field

We have made some breakdowns here to see the differences from several dimensions.

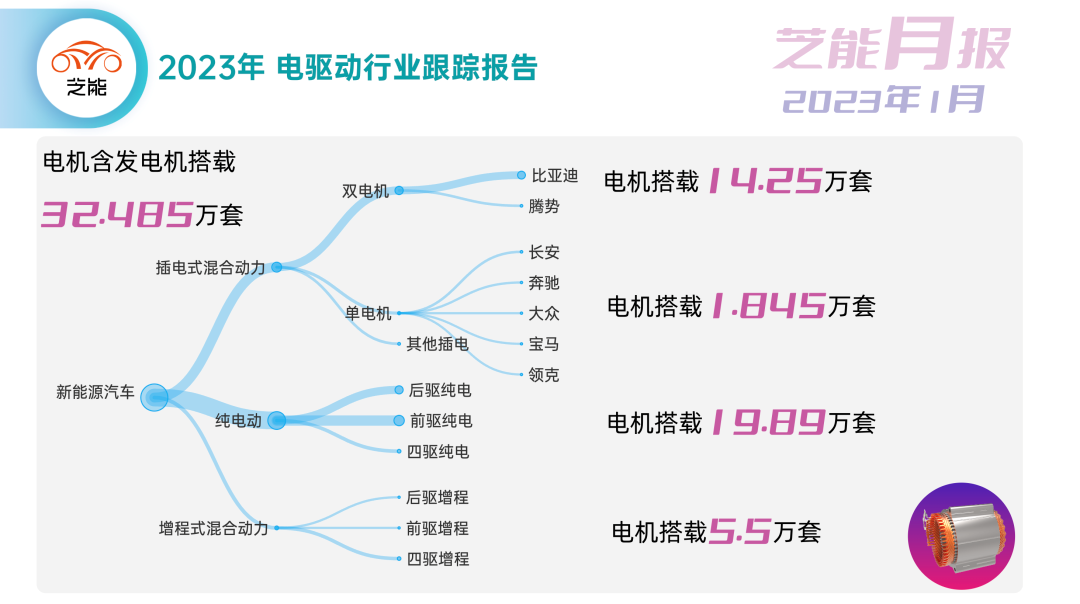

The data in Figure 3 is based on the original data in the introduction, and then adjusted and estimated according to the driving modes of PHEV’s dual motors, extended range (four-wheel drive), and pure electric drive – unified according to the actual number of motors rather than the number of vehicles. Here, we can see that the proportion of four-wheel drive in China is increasing.

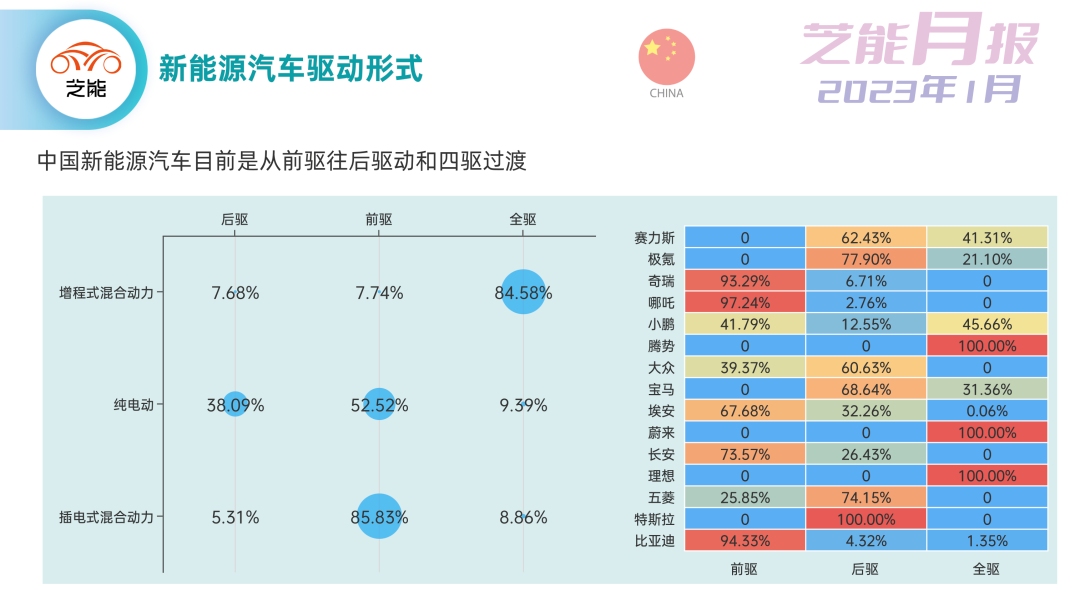

Figure 4 has made a proportional distribution chart of vehicle models according to two dimensions: the level of electrification (pure electric, extended range, plug-in) and the driving form. It can be seen clearly that different levels of electrification of vehicles have clear tendencies in selecting driving systems. Different brands have completely different preferences for driving forms and power characteristics (Figure 4 right).

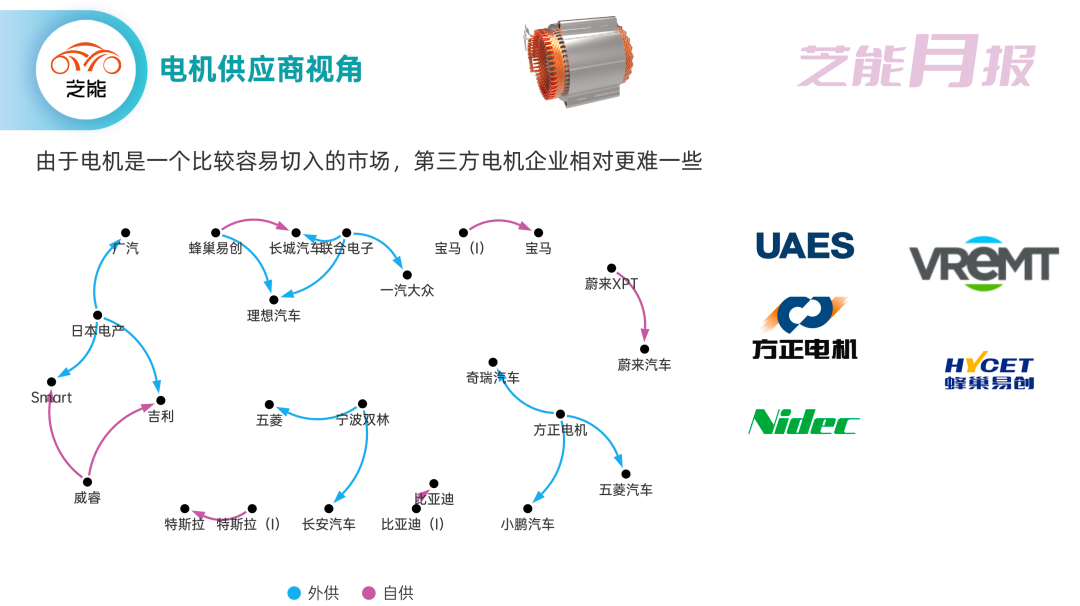

From the market performance point of view, several listed electric motor companies (Jing-Jin Electric, Casic Motor, etc.) are not as good as some traditional parts companies (BorgWarner, Honeycomb Energy). We understand that on the one hand, the technical difficulty of electric motors itself is not high; on the other hand, only the part of car companies pursuing high-performance experiences attaches importance to making performance differentiation in (electric) motors, and most of these automotive brands choose to design, develop, and manufacture motors themselves, only a few of them have the willingness to open up the demand for high-performance motors to third-party suppliers.

Therefore, it’s difficult for motor companies to find valuable customers, and they can only produce low-priced and low-performance standard products, turning the business of motors into a bargain.

Currently, there are no particularly good customers in the motor field except for new forces. With the entry of new forces into the high-performance motor design field, the overall market has become smaller.

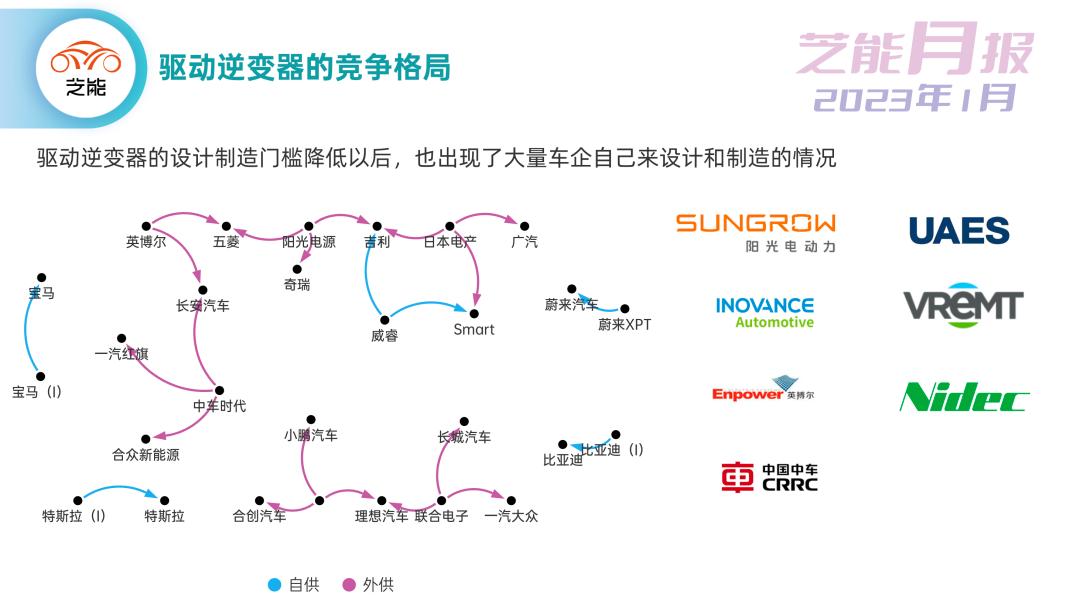

2) Data breakdown in the field of electric drive inverters

After the design and manufacturing threshold of electric drive inverters was reduced, many car companies began designing and manufacturing their own inverters. However, high-performance driving systems still need to choose appropriate suppliers in the field of power modules – making compromises between cost and performance. This has caused the development of several leading inverter companies to be unsatisfactory.

Like motors, except for the A00 level market, strong suppliers of drive inverters currently include Huichuan Joint Drive, United Electronics, and Japan Electric.

Monthly Review of Electric Drive Industry

Currently, it seems that vehicle manufacturers’ in-house manufacturing or suppliers with a background in vehicles have better order situations than third-party companies during a downturn cycle. There are indeed some basic reasons behind this.- The difference in motor efficiency is not so obvious, and it is relatively easy for car companies to obtain production line technology through investment. Suppliers, on the other hand, cannot command significant premiums without unique technologies.

-

Power modules are the main bottleneck in inverter production. Car companies are now controlling the production of high-value and long-cycle chips, and will undoubtedly procure some power modules themselves, which objectively leads to a decrease in demand for inverter design and outsourcing.

-

In the electric drive industry, from three-in-one to multi-in-one, car companies still need to configure their production capacity according to the needs of industry development.

Therefore, the electric drive industry has prematurely entered the red ocean, resulting in low profits for all companies in this field, with the lion’s share of the value chain going to power module companies.

Conclusion: In the electric drive industry, valuable contents require more time to decompose and contemplate. We will try to dig up this information to improve this monthly report. There will also be related content tracking of power modules in the future.

This article is a translation by ChatGPT of a Chinese report from 42HOW. If you have any questions about it, please email bd@42how.com.