Special Contributor | Happy and Comfortable

Editor | Qiu Kaijun

Unlike the high-profile price increase in 2022, Tesla took the lead in significantly reducing the prices of Model 3 and Y in January 6, 2023. Since then, the entire Chinese passenger car market has been dragged into a muddy price war.

In January, the overall retail sales volume of the market was 1.293 million units, and both year-on-year and month-on-month declines exceeded 35\%, creating the worst January performance since 2020.

On February 10th, BYD, the global champion in new energy vehicle sales, also introduced the Qin Champion Edition for 99,800 yuan, opening the curtain of “equal price for gasoline and electricity” and bringing further impact to the entire market.

Within just a week, GAC Toyota’s bZ4x decreased 30,000 yuan, and FAW Toyota’s similar models decreased 60,000 yuan. The highest discount of the Geely Emperor PHEV was up to 30,000 yuan, and the starting price dropped to 109,800 yuan. In addition, Nissan’s Ariya had the highest discount of 60,000 yuan, lowering the starting price from 284,800 yuan to 224,800 yuan…

From new energy vehicles to fuel-powered cars, a new round of “price cuts” for passenger cars is about to come.

What is the logic behind this, and who will be the next to cut prices?

Today, let’s take a look at the background of the “price cut” wave.

The overall market was sluggish at the beginning of the year and consumer willingness was low**

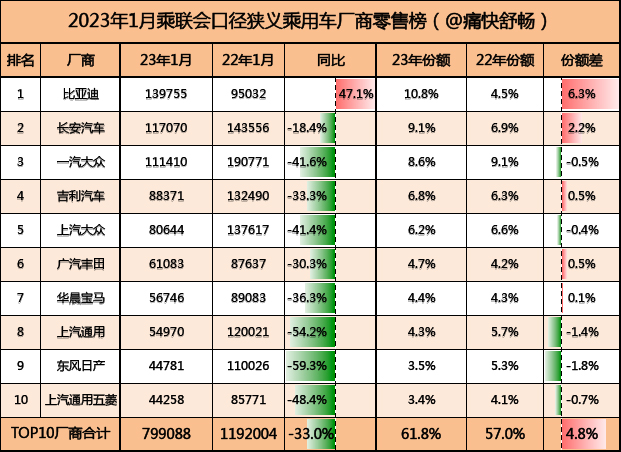

On February 12th, it was the day when China Passenger Car Association released its monthly sales rankings. However, attentive friends may have noticed that this time, the association only released the rankings of car models, but not those of car manufacturers.

The reason is: the data for car manufacturers in January was really “disastrous”. Here, the author compiled a list of car sales volume in January based on the market analysis released by the association a day earlier and the data disclosed by car companies.

It can be said that it is shocking to look at. Among the TOP10 list, except for BYD’s positive year-on-year growth, the year-on-year growth of the remaining nine automakers is negative. Even most of the joint venture automakers showed a negative growth of more than 40\% year-on-year in January compared with the same period last year.

No wonder the association chose not to disclose the rankings of car manufacturers in January.If we take a closer look at the TOP 10 list of model sales decline, compiled based on the China Passenger Car Association retail data, it becomes even clearer.

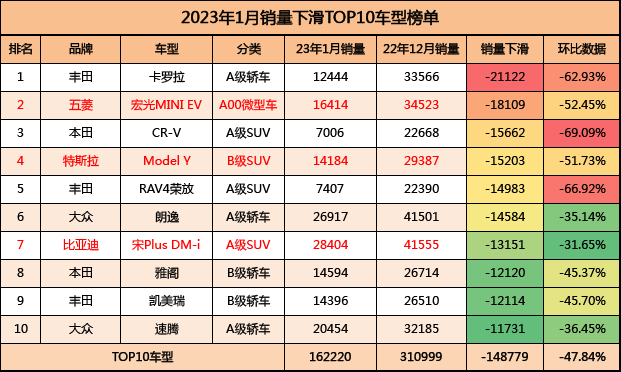

In January, the sales of Toyota Corolla, RAV4 and Honda CR-V dropped more than 60% compared to the previous month. The sales of Accord and Camry dropped over 45% compared to the previous month. These two B-class cars are also perennial TOP 3 candidates. The sales of Volkswagen Sagitar and Lavida also dropped more than 35% compared to the previous month. These several models are the major models with high sales in Toyota and Volkswagen.

Even the TOP 3 models in the 2022 new energy vehicle sales ranking, Wuling Hongguang Mini EV, Tesla Model Y, and SUV sales champion Song Plus DM-i also saw sales decline by more than 50% compared to the previous month, with the latter declining by 31% compared to the previous month.

The expiration of the 2022 new energy vehicle subsidy cut and the fuel vehicle purchase tax reduction policy has severely overdrafted the demand for January and even the first quarter of 2023. Coupled with the Spring Festival factors, the January data looks so unattractive.

However, since February, the sluggish market performance has not been further alleviated. According to the latest data from the China Passenger Car Association, from February 1st to 12th, 464,000 passenger cars were sold, a year-on-year increase of 46% (February 1st to 6th in 2022 was the Spring Festival holiday). The total cumulative sales of passenger cars this year were 1.757 million units, a year-on-year decrease of 27%.

The advanced overdraft of the market, coupled with insufficient consumer willingness, has led to the start of this wave of price cuts.

Therefore, many auto companies have reached a consensus after the Chinese Spring Festival: “In 2023, market demand is the priority, rather than profits.”

Why choose to prioritize market demand over profit? This involves the two characteristics of the auto industry and the characteristics of the new energy era.

Two Characteristics of the Auto Industry

The automotive industry is a typical capital-intensive and fixed asset-intensive industry with economies of scale. This industry characteristic determines that if you want to increase scale, you need to invest a large amount of fixed assets.

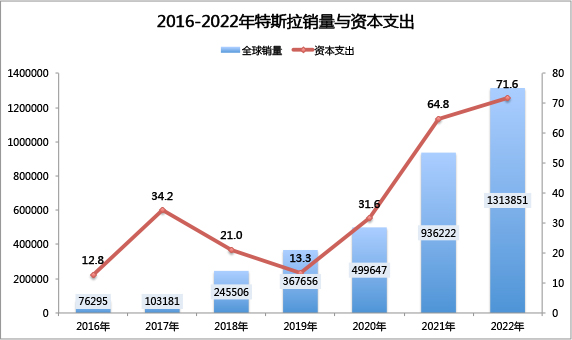

Taking Tesla as an example, the capital expenditure data from 2016 to 2022 shows that in the seven-year period, Tesla’s fixed asset investment was $24.93 billion (equivalent to RMB 174.5 billion). The synchronous increase in production capacity and sales has led to Tesla’s global production capacity reaching 2 million vehicles at the end of 2022. The increase in production capacity of almost 1 million vehicles requires an investment of $10 billion in fixed assets (after simply deducting the relevant battery input).

Next, such a massive investment in fixed assets needs to be amortized over every car produced each year. Therefore, for the factories that have already been put into production, capacity utilization rate has become a core indicator for amortizing fixed asset investment, and it is also one of the most important indicators that various automakers pay attention to.

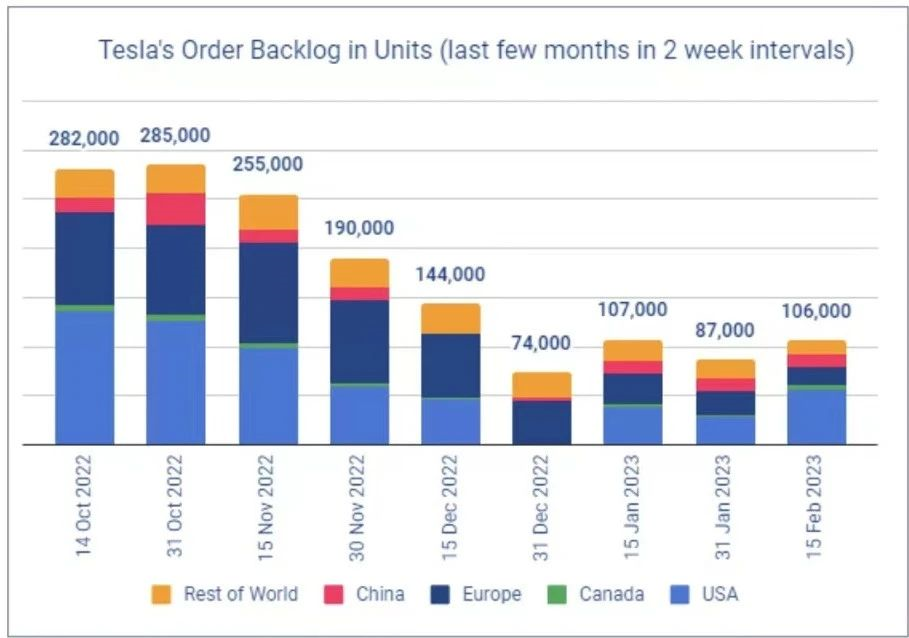

Taking Tesla as an example again, its full-year capacity utilization rate in 2022 is 83% (annual global production capacity of 1.65 million vehicles and production output of 1.37 million vehicles). After entering 2023, Tesla’s global annual production capacity will approach 2 million vehicles, equivalent to a monthly production capacity of 160,000 vehicles. However, according to Troy’s tracking of global orders, as of December 31, 2022, Tesla only has 74,000 orders worldwide, which is also the fundamental reason why Tesla chose to launch a large-scale global price reduction on January 6.

As of February 15, the latest data shows that Tesla’s global orders have reached 106,000 vehicles. Even if all orders were fulfilled, capacity utilization would quickly drop to only 70% based on a monthly production capacity of 150,000 vehicles. This is also the most important reason for the recent news about Shanghai factory’s shutdown and renovation.

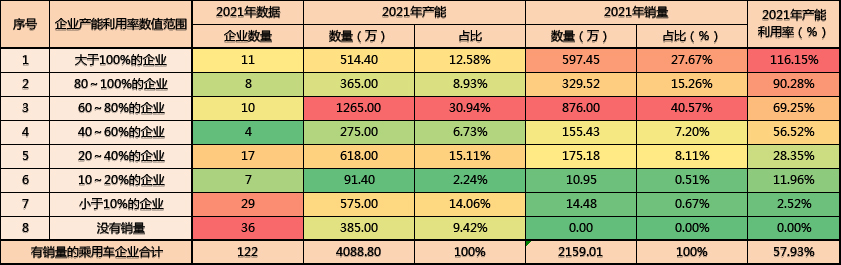

After seeing Tesla’s data, let’s take a look at the utilization of production capacity of Chinese passenger car companies in 2021.

In China, there are 122 enterprises with qualifications for passenger car production, of which 36 have no sales, accounting for 29.5%. The remaining 86 enterprises have an average utilization rate of 58.29%. There are 19 enterprises with a utilization rate of more than 80%, 10 enterprises with a utilization rate between 60-80%, 4 enterprises with a utilization rate between 40-60%, and 24 enterprises with a utilization rate below 40%.This is also why relevant departments consider overcapacity as the most important reason for the overall surplus production of passenger cars.

For the automotive industry, high fixed asset investment can only be effectively amortized through high capacity utilization rates. If effective production capacity utilization cannot be achieved, or if the scale is not sufficient, effective amortization cannot be achieved, and naturally, there will be no increase in profitability.

This is why everyone has reached a consensus: “scale is important, profit is not.”

However, in 2023, there is another very important factor: the substitution of new energy for fuel vehicles.

The relationship between new energy and fuel vehicles

At the China Electric Vehicle 100-People Forum held on February 17th, former MIIT Minister Miao Wei stated that “new energy vehicles are a complete substitution for fuel vehicles, and what really needs to be controlled is the overcapacity of fuel vehicles.”

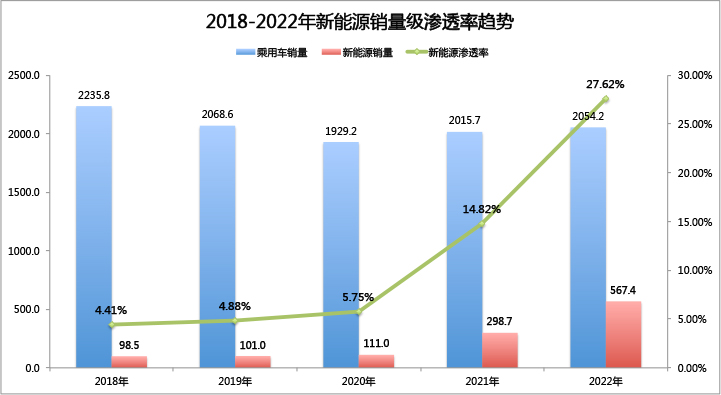

Before 2022, the penetration rate of new energy vehicles in the Chinese market was less than 20%. On the market side, the reaction was more of a supplement to fuel vehicles, but starting in 2022, the penetration rate of new energy will rapidly increase to 25%, and in the future, new energy will replace fuel vehicles more.

At this time, the “oil and electricity at the same price” competition strategy led by global new energy leaders BYD and Tesla will greatly occupy the market share of traditional fuel vehicles.

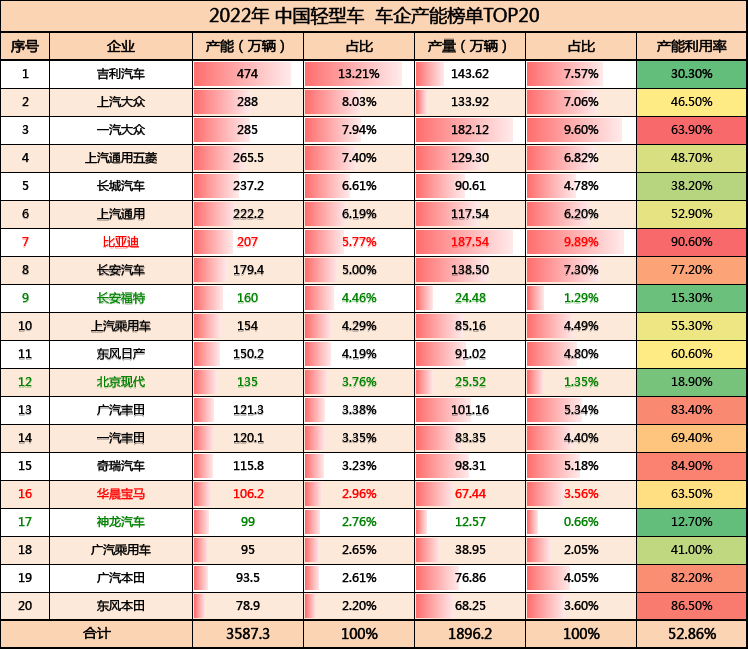

If we combine the production capacity utilization of China’s light vehicle companies in 2022 (from Gaishi Automobile Statistics) and take another look, we will have a better understanding of which car companies will follow up on this “price war” sparked by Tesla.

Compared with 2021, the overall capacity utilization rate in 2022 has slightly decreased. Only five major automakers have a capacity utilization rate of more than 80%: BYD, Dongfeng Honda, Chery Automobile, GAC Toyota, and GAC Honda.- The major automakers with a capacity utilization rate of 60-80% are: FAW-Volkswagen, Dongfeng Nissan, FAW Toyota, and Brilliance BMW;

- The major automakers with a capacity utilization rate of 40-60% are: SAIC Motor, SAIC-GM, SAIC-GM-Wuling, SAIC Volkswagen, and GAC Motor.

From the perspective of the capacity utilization rate, the major automakers that have seen a significant decline in their utilization rates while their output has not increased are: Great Wall Motors, SAIC-GM-Wuling, and Dongfeng Nissan, with the utilization rate declining by more than 10 pcts. FAW Toyota and SAIC-GM have seen a utilization rate decline of more than 6 pcts.

There are two types of major automakers that will participate in the “price reduction wave” in the future. The first type are those who will maintain high capacity utilization in 2022 but will face impacts on their major models in 2023, typical of which are Toyota, Honda, and Volkswagen. The second type are those major automakers that urgently need to improve their capacity utilization rate, typical of which are Geely, Great Wall, and Nissan. As for car companies like Ford, Hyundai, and Kia whose sales scale in 2022 is below 200,000, their price reduction or not will not have a significant impact on the market.

According to first-hand feedback, the newly launched BYD Qin champion edition priced at 9.98 has doubled the number of customers in many BYD stores and the newly added daily order data has significantly exceeded the store’s expectations. Meanwhile, many joint venture A-level sedans have begun to struggle to maintain their market competitiveness. Even Toyota and Volkswagen will soon participate in this wave of “price reduction wave”, otherwise, if the sales volume of popular models cannot be guaranteed, the annual sales target of car companies will be worrying.

The Coming Price Reduction Wave

-

From the operational perspective, the automotive industry has two essential characteristics: First, high fixed asset investment; Secondly, the capacity utilization rate is a key indicator for measuring the operational efficiency of car companies.

-

For the automotive industry, once there is a surplus capacity, every major automaker will face difficult choices: at this time, they can choose “price reduction to maintain quantity” to maintain the basic capacity utilization rate, or “reducing the quantity to maintain price” to maintain stable financial indicators.

In 2022, Honda and Great Wall chose the “reducing the quantity to maintain price” strategy, and it was found that both their production volume and sales volume were rapidly declining;

In 2023, Tesla and BYD chose the “price reduction to maintain quantity” strategy. Specific market performance will be reviewed at the end of the year.

3. Under the background of the accelerating substitution of new energy for fuel vehicles, major automakers who are pragmatic ultimately choose “to achieve sales, not profits” – the price reduction wave will come in the first half of 2023.# 这是一个Markdown文本

着重强调的文字

这是一个 强调的文字 ,这是一个 斜体的文字 ,这是一个 加粗斜体的文字 。

列表

无序列表

- 项目 1

- 项目 2

- 项目 3

有序列表

- 项目 1

- 项目 2

- 项目 3

链接

这里是一个链接, Markdown 教程,请点击进去学习。

图片

这里是一张图片:

代码块

这是一段代码块:

print("Hello world!")

表格

| 表头1 | 表头2 | 表头3 |

|---|---|---|

| 单元格1 | 单元格2 | 单元格3 |

| 单元格4 | 单元格5 | 单元格6 |

HTML 标签

这是一个超链接的 HTML 标签。

This article is a translation by ChatGPT of a Chinese report from 42HOW. If you have any questions about it, please email bd@42how.com.