From Old Li in Financial Street

How cool Tesla used to be, how bearish it is today, but there are always beneficiaries in the capital market whether you go short or long.

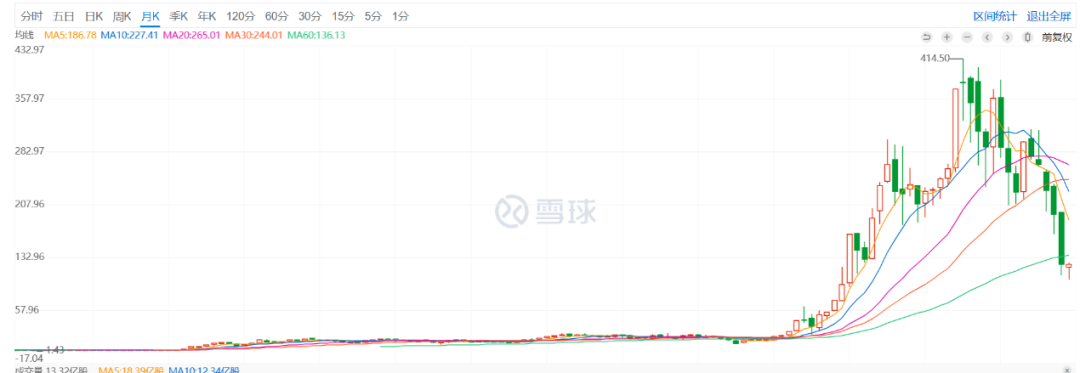

Since the end of 2021, Tesla has been constantly falling in the secondary market, while its sales and stock prices have diverged. In 2022, Tesla’s global sales exceeded one million vehicles for the first time, with a total of 1.314 million vehicles sold. Although it is a growth achievement, it is still lower than the market expectation.

Many friends are concerned about the future trend of Tesla. Today, Old Li will talk with you about what caused Tesla’s falling stock prices in the past year, why there are short selling institutions in the US market, and when Tesla’s stock price will rebound.

The Cause of the Falling Stock Price

In 2022, Tesla’s market value declined by nearly 70%, which was a Waterloo for the company that had been the most shining star in the global capital market in the past three years.

Although there are many discussions about Tesla in the industry, most people look for the reasons for the falling stock prices from the company’s fundamentals. In Old Li’s opinion, from a capital perspective, the company’s fundamentals are not the main cause of the falling stock prices, but rather external capital environment, major shareholder reduction, and reduced market confidence.

Let’s first talk about the external environment. Old Li has always said that industry and capital market are interconnected. Only when both the industry performance and the capital environment are good, can market value continue to grow. If the target company’s industry performance is good, but the external capital environment is poor, market value will fall accordingly. Obviously, Tesla and a number of US technology stocks belong to the latter case.

In 2022, US technology stocks all fell sharply. In the past year, Apple’s market value has shrunk by nearly 30%, NVIDIA’s market value has shrunk by 51%, and even traditional companies like Toyota’s market value has shrunk by 26%. Of course, Tesla, which has the most severe “overheating” and “controversy,” fell the most.

In the past year, the US market has suffered from severe inflation, and the profit performance of many technology companies has been poor. However, these companies have a price-to-earnings ratio of over 30 times, and in the case of continuous interest rate hikes by the Federal Reserve and rising interest rates, these “high-quality assets” of the past have become “bad assets” in a flash, forcing people to sell and transfer their assets to safer places. In the past three years, Tesla’s stock price has risen the fastest, and people have made quick money, so it is reasonable to sell.As the CEO and largest shareholder, Musk’s cashing out has intensified the selling of Tesla’s stock. In 2022, Musk has reduced his holdings of Tesla’s stocks by large amounts several times, cashing out $8.5 billion, $6.9 billion, $3.95 billion, and $3.58 billion in April, August, November, and December respectively. Within a year, Musk cashed out a total of $22.93 billion.

Compared with Tesla’s market capitalization of nearly $400 billion, Musk’s absolute selling was not high, but the continuous large-scale selling has brought distrust to the market. There are various rumors about the reasons for Musk’s selling, all of which are harmful to Tesla’s market management. These rumors include Musk cashing out Tesla’s stock to support Twitter, Musk giving up Tesla and no longer serving as the company’s CEO, and Musk intentionally lowering Tesla’s market value to reduce exposure.

Musk’s selling, the slowdown in performance growth, and the overvaluation of technology stocks have all contributed to the lack of confidence in Tesla. Before 2020, people bought Tesla’s stocks with the expectation of how much they would rise, but in 2022, people’s first thought about buying Tesla’s stocks is how much further they will fall.

As early as the end of 2021, many U.S. stock analysts in China suggested that Tesla and American technology stocks were likely to undergo another pricing in 2022. But what they did not expect is that Tesla would become a target, and many media outlets analyzed Tesla’s decline in market value as a fundamental problem, which is not the case. Even if Tesla’s sales increase to 2 million vehicles in 2022, in such a turbulent capital environment, American investors will still sell Tesla’s stock.

Short Selling is Still Profitable

Tesla’s market value has been continuously falling, causing long position investors to lose money, while short position investors earned a large sum in the past year.

In the context of China’s secondary market, everyone is adopting long positions, and China’s market investors cannot short sell. Therefore, when the market enters a bearish phase, everyone’s return on investment will not be good.

In comparison, the U.S. capital market is relatively mature, and although the short-selling mechanism in the United States also has many problems, it is a mature mechanism. In Old Li’s view, the deteriorating external environment, Musk’s selling, and the weakened market confidence of Tesla are not enough to cause a 70% decline in its market value. After all, Tesla was still a trillion-dollar market value company at the end of 2021.

Tesla has always been a stock that attracted short-sellers in the US market. From 2018 to the present, short-sellers have been trying to short Tesla. In the confrontation between the bulls and the bears of Tesla in 2019, the bears were defeated and Tesla’s market value further increased. To the bears, the increase means that “bubble” exacerbates. Once the external market environment deteriorates and Tesla’s performance cannot be realized, the bears will usher in new opportunities.

Generally, when the market value begins to decline, the market will have a net short position, and when the short-sellers cover their positions, the market will form a buying buffer, and the market value will temporarily stabilize, and then the market will further decline.

If we look at the changes in Tesla’s market value in 2022, it basically follows this rule. In the first and second quarters of 2022, although Tesla’s delivery volume was still good, the market value continued to decline. In the third quarter, Tesla’s market value stabilized, and in the fourth quarter, the market value collapsed again.

Some friends of Lao Li who invest in US dollar funds said that in the past year, there have been significant differences between the bulls and bears of Tesla. Although the number of institutional investors who are bullish is much higher than that of short-sellers, the external environment is so poor that the investors who are bullish have not been able to stabilize the market value. In this process, the short-sellers have actually benefited the most.

Whether in the domestic or foreign markets, another important factor that determines a company’s performance in the capital market is the CEO. Whether it is Apple or Nvidia, or traditional companies such as Toyota, their top executives all emphasize “stability.”

Iron Man Musk has a radical style, which also brings a radical approach. In terms of business operations, Tesla is just one of its business layouts. In addition, Musk has gradually shifted from the “technological aspect” to the “social aspect.” Since investing in Twitter, Musk has gained a greater voice in the social field, and has also revived Trump’s account. Some investors have started to have new opinions about Musk.

Regardless of the domestic or foreign market, the relationship between the capital, enterprise, and CEO is not a case of “one gains, another loses,” but rather a relationship of strength begetting strength or weakness begetting weakness. When companies and CEOs are in a position of strength, the capital will give them greater support; whereas, when companies and CEOs are weak or face great risks, capital tends to be the first to withdraw, and the performance of capital will be reflected in the market capitalization of the enterprise.

Clearly, Tesla cannot escape from the capital environment that has developed in the US market for several decades. I believe this is the most direct reason for the decline of Tesla.

Does Tesla Still Have a Chance?

Recently, many friends have been asking when they can buy Tesla at a bargain. Frankly, it is difficult to determine at the moment, and it still depends on the overall situation. When the US capital environment and Tesla’s business performance are improving, its market capitalization may rebound; otherwise, Tesla’s market capitalization will not perform well.

Currently, there is still a lot of controversy over Tesla in the US market, and the staunchest supporter of Tesla, the investment goddess, Cathy Wood, recently stated that Tesla’s market capitalization will nearly quadruple by 2026, approaching that of Apple. On the other hand, fund managers on Wall Street are preparing for a “cold winter” in 2023, as the Federal Reserve may try to eliminate inflation and kill the high valuations of tech stocks, and Tesla will definitely be the first to fall.

In addition to the external environment, the biggest controversy surrounding Tesla in the US market is pricing. Prior to 2021, the US market had always positioned Tesla as a tech stock, and people had been giving it a high price-to-earnings ratio using the valuation method for tech stocks. However, Tesla’s financial performance in recent years has proved that it is not a true tech stock—a high investment, high output, and low return enterprise, but rather a manufacturing enterprise.

However, Tesla is different from traditional automobile manufacturers such as Volkswagen and Toyota. Its profit margin is much higher than that of traditional manufacturing companies and it also has a good performance in free cash flow. Therefore, it is also unreasonable to use the traditional valuation method for manufacturing enterprises, and Li called it a “tech-type manufacturing company.”According to Lao Li’s opinion, both Tesla, Chinese new forces, and traditional electric vehicle companies can be classified as technology-based manufacturing enterprises. Due to the significant changes in products and services, the profit margin and free cash flow of the electric vehicle industry are higher than that of traditional manufacturing companies but lower than that of high-tech enterprises. Therefore, the market should give electric vehicle companies a reasonable price-to-earnings ratio between traditional manufacturing companies and high-tech enterprises. This means that Tesla’s reasonable pricing range should be higher than traditional companies but lower than high-tech companies. Based on actual performance, corresponding P/E ratio can be assigned, and the reasonable market value of the enterprise can be obtained.

Under this logic, Tesla’s performance is particularly important. Currently, the Chinese market has the greatest impact on Tesla’s sales volume, and since last year, the domestic electric vehicle market has gradually entered the “boom era.” New products from various companies are emerging, but Tesla’s main models, Model 3 and Model Y, were launched in 2017 and 2020 respectively, with a slow iteration speed. In addition, Tesla’s full self-driving capabilities have not been fully implemented in China, which has a significant impact on Tesla’s business model.

Currently, Tesla’s Shanghai factory has sufficient production capacity, but with the emergence of more public opinion events and continuous price reductions, Tesla’s brand effect and influence have greatly weakened, and market demand has also decreased. Although some funds predict that Tesla’s delivery volume will experience a significant outbreak in the first quarter of 2023, Lao Li still has reserved views on its market value.

For such a technology stock with ups and downs like Tesla, it is difficult for individual investors to grasp the exact bottoming-out time. When the external environment is not yet stable, it is ideal to focus on the domestic market and wait.

This article is a translation by ChatGPT of a Chinese report from 42HOW. If you have any questions about it, please email bd@42how.com.