Author: Zhu Yulong

Recently, there has been a lot of discussion about whether XPeng Motors will adopt range-extender technology or not. During the Q3 conference of LVCHI Auto, it was made clear that:

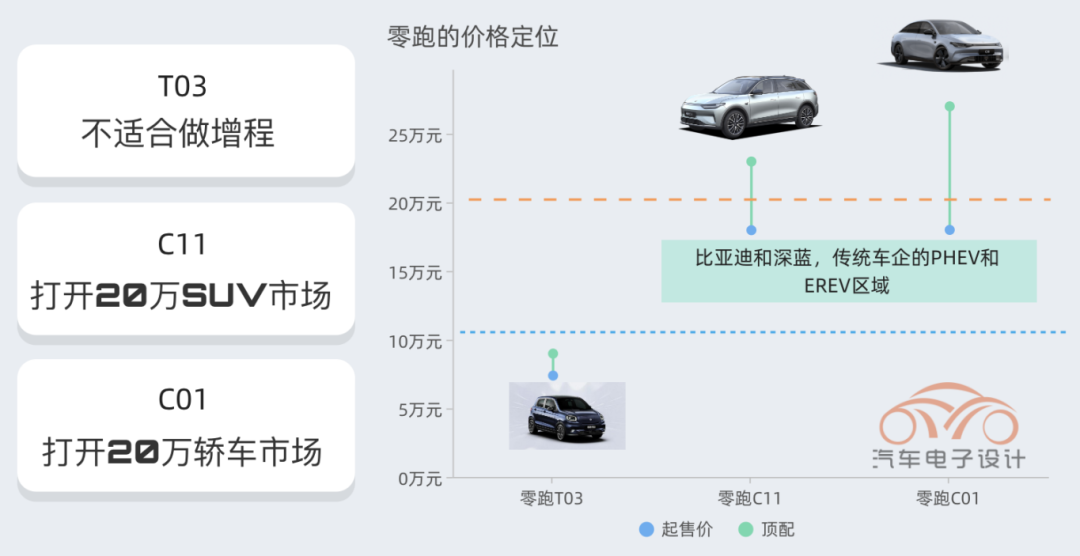

LVCHI will constantly expand their product line on the C platform, going from pure electric to range-extended; the C11 range-extended version will be released in Q4 2022 with about 3-4 models to meet different user needs. The C01 range-extended version will be released in Q3 2022 at a lower price than the pure electric version. All vehicle models on the C platform, including future new platform developments, will be released with both range-extended and pure electric versions.

Regardless of whether or not XPeng Motors adopts range-extender technology, the companies currently doing so include: Li Xiang Auto, WM Motor, Xpeng Motors, LVCHI Auto, Landjet Auto and Hybrid Kinetic. Don’t doubt the starting point, as all car companies will do their calculations when making strategic decisions.

Here, there is a common assumption that in the next 3-5 years, range-extended vehicles will have a very large growth space. Therefore, LVCHI Auto believes that the proportion of range-extenders will gradually increase to 50%, or even higher, in the Q3 meeting. After 2025, as battery costs start to decline and charging piles become more widespread, the sales of range-extended vehicles will decrease and ultimately return to pure electric vehicles. This is a realistic judgment!

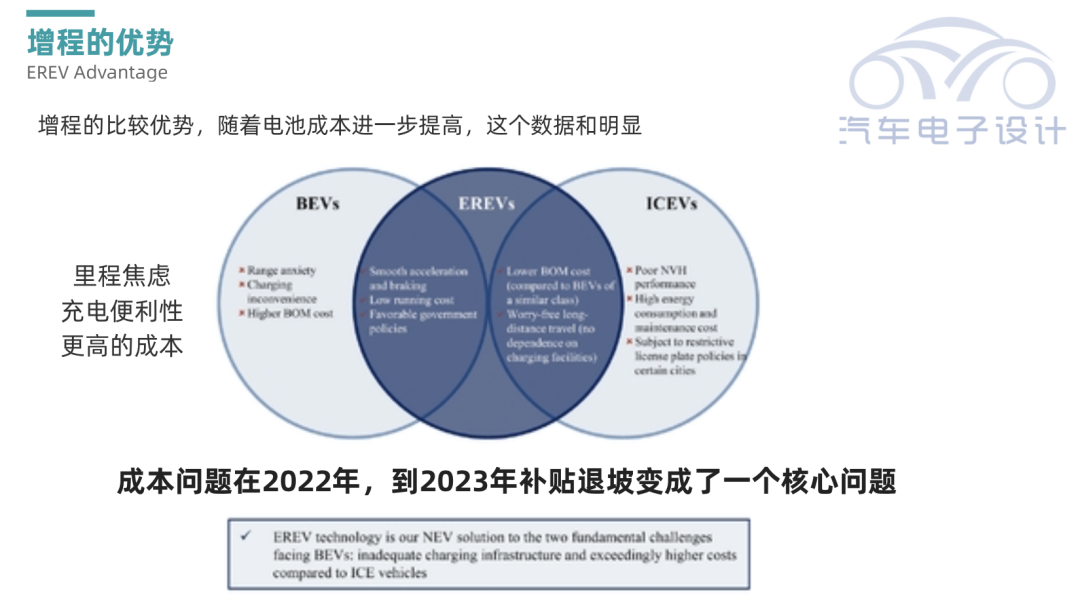

Cost difference

This issue is actually very clear when the accounts are calculated. In the composition of the power system, the battery system accounts for the largest part of the material cost.

Originally, when we looked at Li Xiang Auto’s strategy, it revolved around mid-to-large-sized battery-powered SUVs. In the L9, L8, L7 and L6 series of models, Li Xiang Auto wanted to achieve user mileage freedom. The entire battery needed to be configured for SUVs with 80-120 kWh, where electricity consumption rate is 18-20 kWh/100 km, so that 80 kWh corresponds to an effective range of 400 km; and 120 kWh corresponds to an effective range of 600 km.In the range of about 300,000 RMB, the value of 80-120kWh battery storage is currently between 88,000-132,000 RMB, and the battery system accounts for over 40% of the material cost. The electric drive system can be obtained for about 8,000 RMB, at most accounting for only 5%.

As for an extended range battery system configured with 30-40kWh, it costs about 33,000-44,000 RMB, accounting for about 20% of the material cost of plug-in hybrid cars.

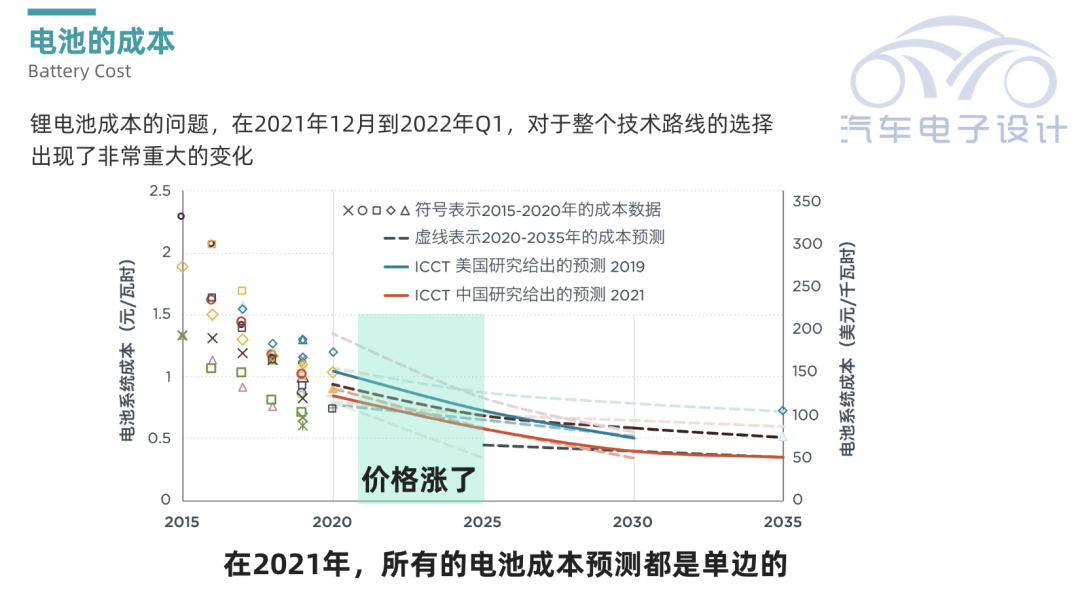

In the cost analysis of pure electric cars and extended range vehicles, the biggest challenge is that all predictions show that economy of scale will continuously lead the price of batteries downwards, but this will be proven false by 2022. The money is taken by upstream resource providers, and the next systemic price reduction will have to wait until there is a significant increase in mineral supply.

LI’s Extended Range Logic

The Changan Blue Core SL03 has officially launched, priced between 168,900 and 699,900 RMB (three power models: extended range hybrid, pure electric, and hydrogen fuel cell). This is a typical compatibility platform. The price of the extended range hybrid version is 168,900 RMB, while the two pure electric versions with different ranges are priced at 183,900 and 215,900 RMB respectively. The core issue here is that as traditional car companies continue to expand their product lines, new and old forces will clash.

In other words, not only large and medium-sized SUVs, but also sedans and compact SUVs, all follow this logic: in the next 2-3 years, various plug-in hybrids and extended range products will be launched. You might think of selling pure electric products priced around 200,000 RMB, relying on intelligence to differentiate them. However, new consumers are also completely buying plug-in (such as BYD) and extended range vehicles (such as LI and WM Motors). Therefore, the pressure is on the new forces.

“`

“`

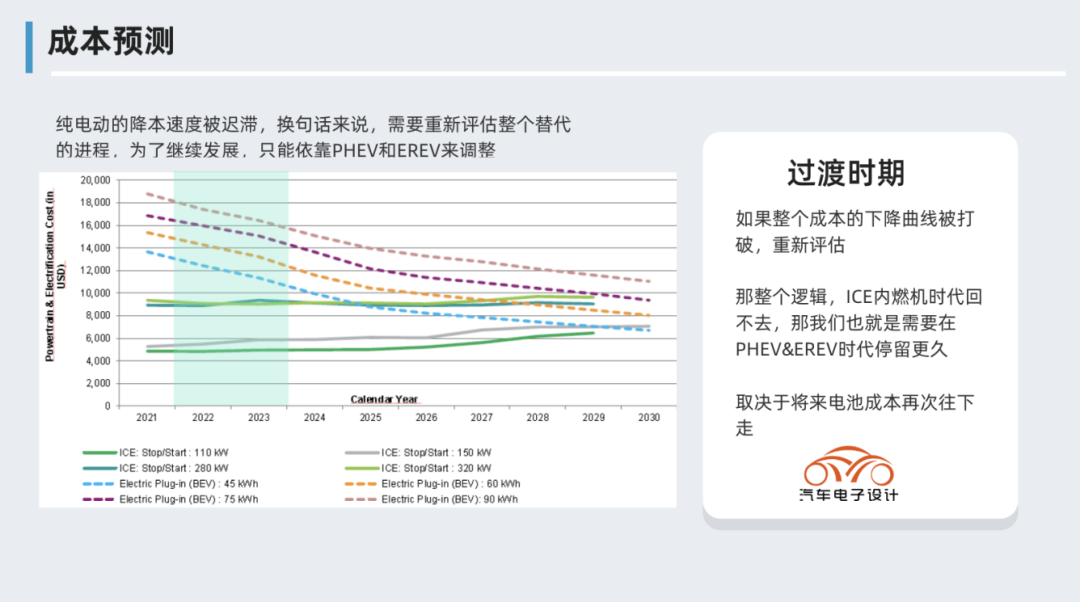

From the perspective of the development of new energy vehicles, it will take several years to directly replace the internal combustion engine with a pure electric platform. During this time, continuing to invest in internal combustion engine systems is impossible, and there are only two strategies in the transitional period:

-

Developing batteries + increasing investment in pure electric platforms: merely purchasing batteries at scale to reduce costs is not feasible, nor is it feasible to simply expand the product matrix of pure electric platforms. The only way is to produce batteries. This strategy seems to work for BYD and Tesla.

-

PHEV, EREV: For transitional products, a low-cost solution can be applied to all models.

In other words, this approach will make compatible platforms more valuable because if the scale of the pure electric platform has not reached 500,000 or more, the supply chain price cannot be negotiated, and more and more people will realize and make decisions on this matter.

Conclusion: I believe that this time, automakers have to develop fuel-efficient vehicles and plug-in hybrids mainly due to the cost of powertrains. It will take at least 2 years (2022-2023) for the supply chain to be matched from upstream to downstream, and it is expected to be smoother by 2024-2025.

“`

This article is a translation by ChatGPT of a Chinese report from 42HOW. If you have any questions about it, please email bd@42how.com.