Sales Changes: Joint Ventures are No Longer Popular

1. Volkswagen – The Brand Most Affected by the New Energy Era

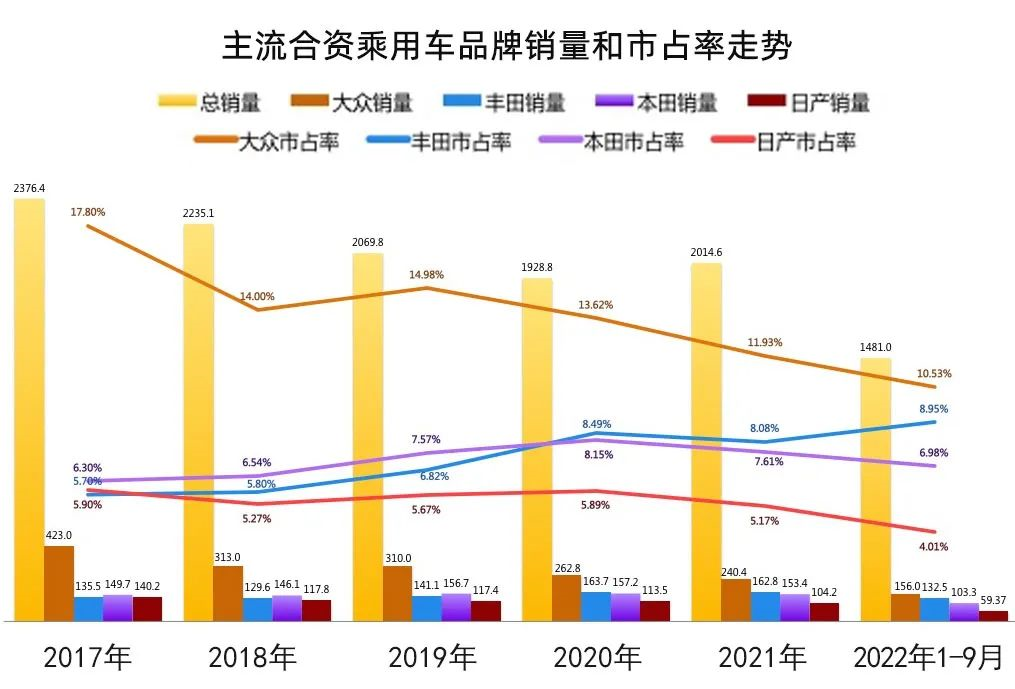

Volkswagen has always been a perennial in China’s passenger car market. At the pinnacle of 2017-2019, Volkswagen created a sales peak of 4.23 million vehicles for a single brand in the Chinese market, with a market share of 18.4%. This was unprecedented in the Chinese passenger car market.

However, after entering 2020, with the rise of new energy, Volkswagen’s brand sales have shown a stair-step decline: from 4.23 million in 2017, 3.1 million in 2019, 2.4 million in 2021, to only 1.56 million in the first nine months of 2022 (estimated to be below 2.4 million for the whole year).

The market share has also dropped from 19.3% in 2019 to 11.2% in the first nine months of 2022, a decline of 8.1 percentage points in three years.

Monthly sales have dropped from about 350,000 vehicles to around 200,000 vehicles, a decline of 42.85% in three years.

The popular models, whether A-class such as Lavida, Bora, Sagitar or Tiguan, or B-class Passat and Magotan have all experienced a year-on-year sales decline of more than 10%.

In the first nine months of 2022, Volkswagen sold 1.56 million vehicles, a year-on-year decline of 13.52%.

It can be said that the Volkswagen brand has gradually lost its charm in the Chinese market.### 2. Toyota – The Rising Star of New Energy Era

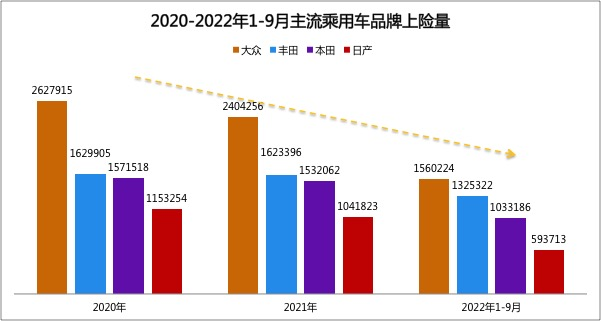

Toyota is the only top joint venture brand that has achieved a sales growth against the decline in sales. From 1.355 million units in 2017 to 1.628 million units in 2021, the total sales volume has increased by 20% in five years. This is almost unheard-of among traditional joint venture brands.

Toyota can be considered as an indirect beneficiary of the new energy era due to its hybrid electric vehicle (HEV) products. In the past 5 years, the sales volume of the overall HEV market has grown rapidly from 152,000 units in 2018 to 530,000 units from January to September 2022, with Toyota HEV’s sales accounting for more than two-thirds of the market share. The sales volume of Toyota HEV was 392,000 units from January to September 2022, an increase of 46% year-on-year.

Therefore, from January to September 2022, Toyota’s sales volume reached 1.3253 million units, an increase of 12.57% year-on-year, and the market share reached a new high of 8.95%. This is not only due to the growth of HEV, but also to a significant price reduction in the terminal market. Especially this year, Toyota, which has maintained stable prices for a long time, has finally launched its “killer strategy” of price reduction, with terminal discounts exceeding 30,000 yuan, and buying a Corolla for 80,000 to 100,000 yuan has become the norm in the market.

The growth of HEV and promotional price reductions have directly driven Toyota’s sales volume to exceed Honda, becoming the second-ranked brand in terminal sales.

3. Honda – Out of the Top Three Joint Venture Brands in Terminal Sales for the First Time in Nearly 5 Years

In 2017, Honda was undoubtedly the second-ranked passenger car brand in the Chinese market, and in 2019 and 2020, its terminal sales volume exceeded 1.5 million units, and its market share reached 8.15%.

However, in the past two years, as new energy products have been selling like hotcakes, Honda’s sales volume has continued to decline, with a year-on-year decline of 2.4% in 2021 and 6.12% year-on-year from January to September 2022.

There are three main reasons: first, the continued absence of new energy products has led to a significant weakening of Honda’s base of fuel vehicles, such as the monthly sales of the A0-class car, the Fit, which used to be the sales champion, now can only be maintained at around five to six thousand units, while the B-class car, the Accord, has also been strongly impacted by domestic new energy products. Second, HEV products have never been able to break through and their sales have lagged far behind Toyota. Third, in terms of pricing, Honda has not adopted a similar aggressive strategy as Toyota.

This is also the fundamental reason why Honda has lost the second-ranked passenger car brand in China’s market and further lost the third place for two consecutive years.### 4. Nissan — Falling Meteor in Top Joint Venture Brands

In 2017, Nissan ranked among the top 5 brands in sales with 1.4 million units sold, however, by 2021, Nissan’s terminal sales had plummeted to only 1.04 million units, a decrease of 25.7% over 5 years!

From January to September of this year, Nissan’s sales were 593,700 units, a 23.9% decrease compared with the same period last year. It is very likely that its sales will drop below 900,000 units this year.

Currently, Nissan primarily relies on three models – Sentra, Teana, and Qijun – to support sales. Qijun’s sales have already collapsed, with only 12,977 units sold from January to September, a year-on-year decrease of 86.05%; Sentra sales were 301,756 units, a year-on-year decrease of 19.71%; and Teana’s sales were 114,362 units, a year-on-year increase of 4.24%.

Qijun failed due to its 3-cylinder engine, and Sentra lost its A-level sedan championship in September, leaving only Teana to support Nissan. However, the cost of maintaining sales is that the individual price of Teana can only be maintained at just over 160,000 yuan, and the average price of the brand can only be maintained at about 120,000 yuan, which is nearly 30% lower than the average price level of Volkswagen and Toyota above 150,000 yuan.

It can be said that Nissan will be one of the first to drop out among the top joint venture brands (the other one being GM).

Changes in Sales Structure: Brand Diving Strategy Has “Failed”

If the decline in brand sales is already tense, what is most frightening is not just the decline in sales. It is the loss of driving force that supports brand sales, especially for joint venture brands, a significant blow when high-volume city sales decline.

From the changes in the sales areas and structures of the four top joint venture brands, we can see some trends.

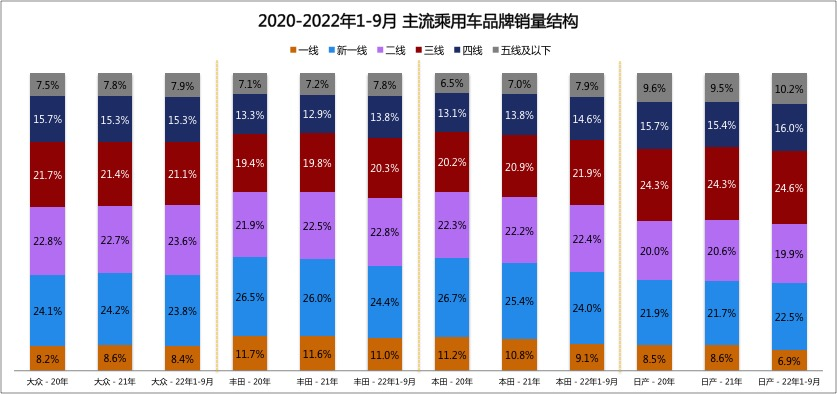

1. Volkswagen

As the joint venture brand with the strongest brand power and the largest scale, Volkswagen’s regional distribution is generally balanced. Whether it is the distribution of sales or the change in sales, it is basically in a very stable state.The sales of Volkswagen in first-tier cities remained stable at around 8.2-8.6%, slightly decreasing in new second-tier cities and maintaining at around 24%, and slightly increasing in second-tier cities. The sales in other third-fourth-fifth-tier cities remained relatively stable.

2. Toyota

Toyota’s brand strength ranks only second to Volkswagen and its dealer scale is also comparable to that of Volkswagen. However, there is a downward trend in regional sales. The proportion of first-tier cities accounts for more than 11%, decreasing by 0.7 percentage points compared to 2020. But it is also the brand with the highest sales proportion in first-tier cities among the top four brands. Toyota’s sales proportion in new second-tier cities decreased by 2 percentage points compared to 2020. The proportion of other level markets has all increased.

3. Honda

Honda has shown a trend of market sinking. The sales proportion in first-tier cities is 9.1% (already decreasing to below 10%), down by 2.1 percentage points compared to 2020. The sales proportion in new second-tier cities is 24%, down by 2.7 percentage points compared to 2020. The sales proportion in second-tier cities remained relatively stable at around 22.4%; The proportion of third-tier and lower markets has increased.

4. Nissan

Nissan’s sales decline is more obvious. The sales proportion in first-tier cities is only 6.1% (the smallest among all top joint venture brands), down by 1.6 percentage points compared to 2020. The proportion in new second-tier cities slightly increased to 22.5%, with an increase of 0.6 percentage points compared to 2020. The total sales proportion in first-tier and new second-tier cities is 28.6%, down by 1 percentage point compared to 2020. However, the sales proportion in third-tier and lower cities is 26.2%, up by 0.9 percentage points compared to 2019.

After the passenger car market in China has entered the era of new energy, the “car buying trend” of high-level city consumers has been shifting towards new forces brands and independent new energy. However, the overly conservative product definition logic and long product upgrade rhythm of the top joint venture brands are the fundamental factors that gradually downgraded their brand strength.

Especially when they are unable to achieve ideal sales in high-level cities and have to turn to middle and low-level cities for sales, joint venture brands will inevitably slide into deeper quagmires. If it is combined with the slow transition of new energy products, no matter who it is, how strong it used to be, if they want to climb out of the quagmire again, it will become more and more difficult.

Changes in average sales price: Brand value begins to gradually “fade”

The overall market sinking of these top joint venture brands will not only affect sales but also further affect the overall average sales price.Let’s take a look at the overall average price and sales structure by price range for the top four brands in the first nine months of 2022.

1. Overall Average Price Structure

We divided the prices into five segments: under 100,000 yuan, 100,000-200,000 yuan, 200,000-250,000 yuan, 250,000-350,000 yuan, and above 350,000 yuan. From these five segments, we can see the sales structure of the top four brands.

Nissan had the highest proportion of sales below 200,000 yuan, reaching 85.1%, followed by Volkswagen with 63% and Toyota and Honda both below 50%.

For sales above 250,000 yuan, Toyota had the highest proportion (due to some imported models) at 14.8%, followed by Honda at 11.1%. Volkswagen and Nissan were both below 10%.

2. Overall Average Price Level

Volkswagen’s overall average price in the first nine months of this year was 151,200 yuan, an increase of 1,300 yuan from the same period last year. Toyota’s overall average price from January to September this year was 158,100 yuan (excluding imported models), the highest among the four joint venture brands and a decrease of 1,100 yuan from the same period last year. Honda’s overall average price in the first nine months of this year was 155,700 yuan, the second highest among the four joint venture brands, an increase of 300 yuan from the same period last year. Nissan had the lowest average price among the four joint venture brands, at only 131,000 yuan, a decrease of 1,000 yuan from the same period last year.

By looking at the overall distribution of price segments and the average price level, it can be seen that Nissan has been affected the most in terms of sales and price levels, followed by Volkswagen, while Toyota and Honda have been relatively less affected overall.

If the top four joint venture brands continue to rely on price leverage to achieve their sales targets, they may be able to maintain their sales this year, but in the long run, the comprehensive collapse from brand to channel will be inevitable.

Summary

The overall sales, sales structure, and selling price of a brand will have a profound impact on the brand’s revenue, profits, image, and customer perception, among other key decision factors.

The transformation of new energy technology, the rise of domestic brands, and the impact of new forces, coupled with the cognitive shift of younger generation consumers, have made it difficult for once-strong but now conservative joint venture brands to recreate their past glory.The joint venture brands can no longer rely on a single model such as Corolla or Sunny to achieve sales exceeding 400,000 units. Even Toyota and Volkswagen, the world’s top two automakers, must understand that in the future of the Chinese market, it will be dominated by domestic brands. Of course, the decline of joint venture brands does not mean the disappearance of joint ventures, but it does mean the reshuffling of the industry’s status.

This article is a translation by ChatGPT of a Chinese report from 42HOW. If you have any questions about it, please email bd@42how.com.