Author | Wang Lingfang

Editor | Qiu Kaijun

There is no worst, only worse.

China’s auto sales peaked and then fell in 2017, and bad news has been coming since then. In 2021, it finally regained momentum thanks to the contribution of new energy, but to everyone’s surprise, the supply chain crisis struck, and since then, the pandemic has repeatedly hit, presenting an unprecedented challenge to China’s auto industry.

What to do?

On May 31st, the China Automotive Technology and Research Center held an online strategic trend-sharing seminar – “Crises and Opportunities for the Automotive Industry Under the COVID-19 Pandemic.” The seminar invited senior chief experts of the center and Deputy Director of the Chief Engineer’s Office Huang Yonghe, Tan Huilong, Head of the Strategy and Prospective Demonstration Department of Changan Automobile, Ye Hai, Director of the Huayu Automotive Systems (Shanghai) Co., Ltd., Li Xinbo, an expert in the China Automotive Engineering Research Institute, and Li Xudong, Senior Manager of the Strategic Research and Intellectual Property Department of China Automotive Engineering Research Institute to conduct in-depth analysis of industry development.

They mainly analyzed and discussed the following issues and drew the following conclusions:

Where is the sales ceiling for China’s auto production and sales? – 30 million units.

How to deal with consumer shrinkage under the COVID-19 Pandemic with slowing income growth? – Huang Yonghe suggests “Stabilizing production and improving quality” and reducing vehicle purchase taxes to further stimulate new energy vehicle consumption.

What are the crises and challenges facing the automotive supply chain, and how to deal with them? – The automotive industry has entered the “era of high costs,” and chips should promote domestic substitution.

As market demand declines and the wave of intelligent electric vehicles approaches, how can companies survive? – “Cost reduction” has become the theme, and the reconstruction of the value chain shifts from a chained ecology to a networked ecology.

Sales Ceiling: 30 million units

Faced with the decline in auto sales in the past few years, the most concerning issue in the industry is whether China is approaching the sales ceiling.

From the perspectives of the experts at the seminar, the answer is affirmative. Huang Yonghe, Tan Huilong, and Ye Hai gave predictions of a sales peak of 30 million units.

As early as 2011, Huang Yonghe predicted that the sales ceiling for China’s auto production and sales in the next ten years would be 28 million units. Today, he still believes that the peak year sales volume of China’s auto market will not exceed 30 million units.

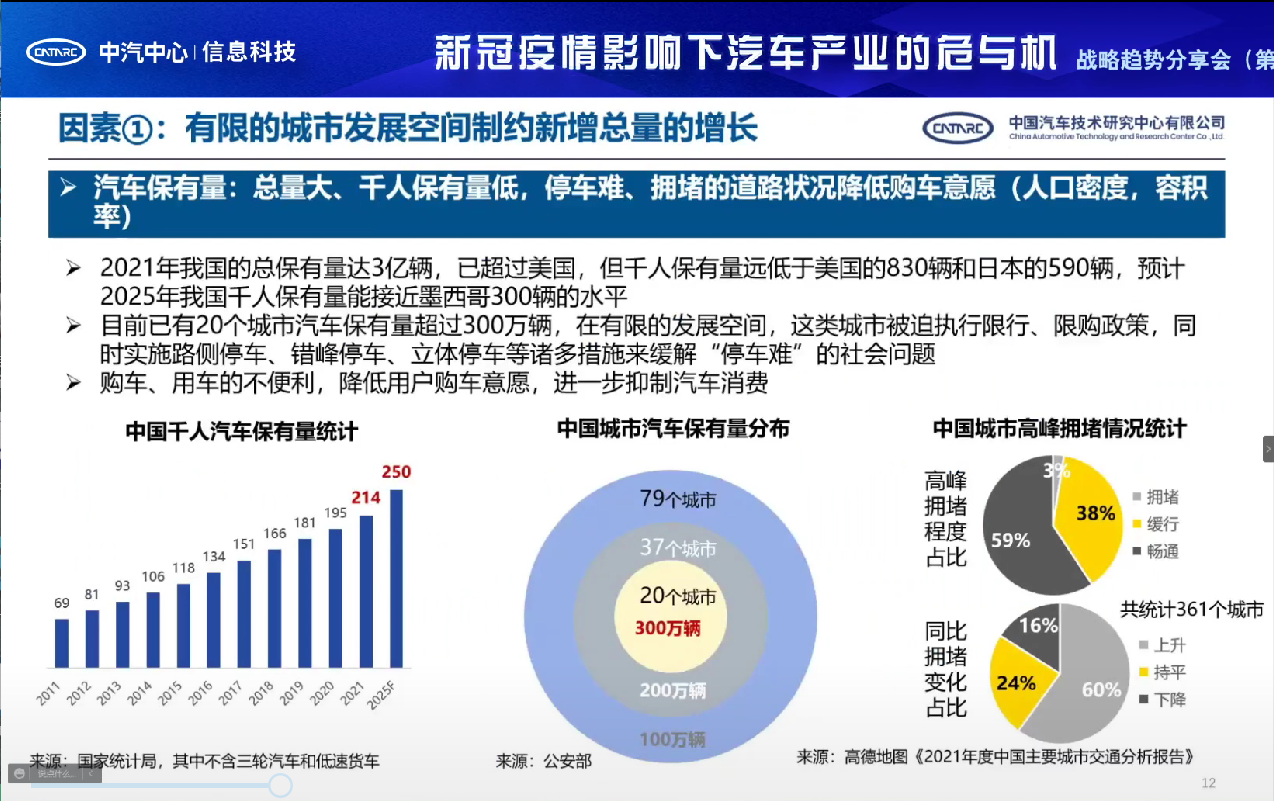

Huang Yonghe made this judgment based on factors such as the road carrying capacity of cities, the size of the consumer base, and fuel supply, stating that “these factors that drive market growth are undergoing fundamental changes.”

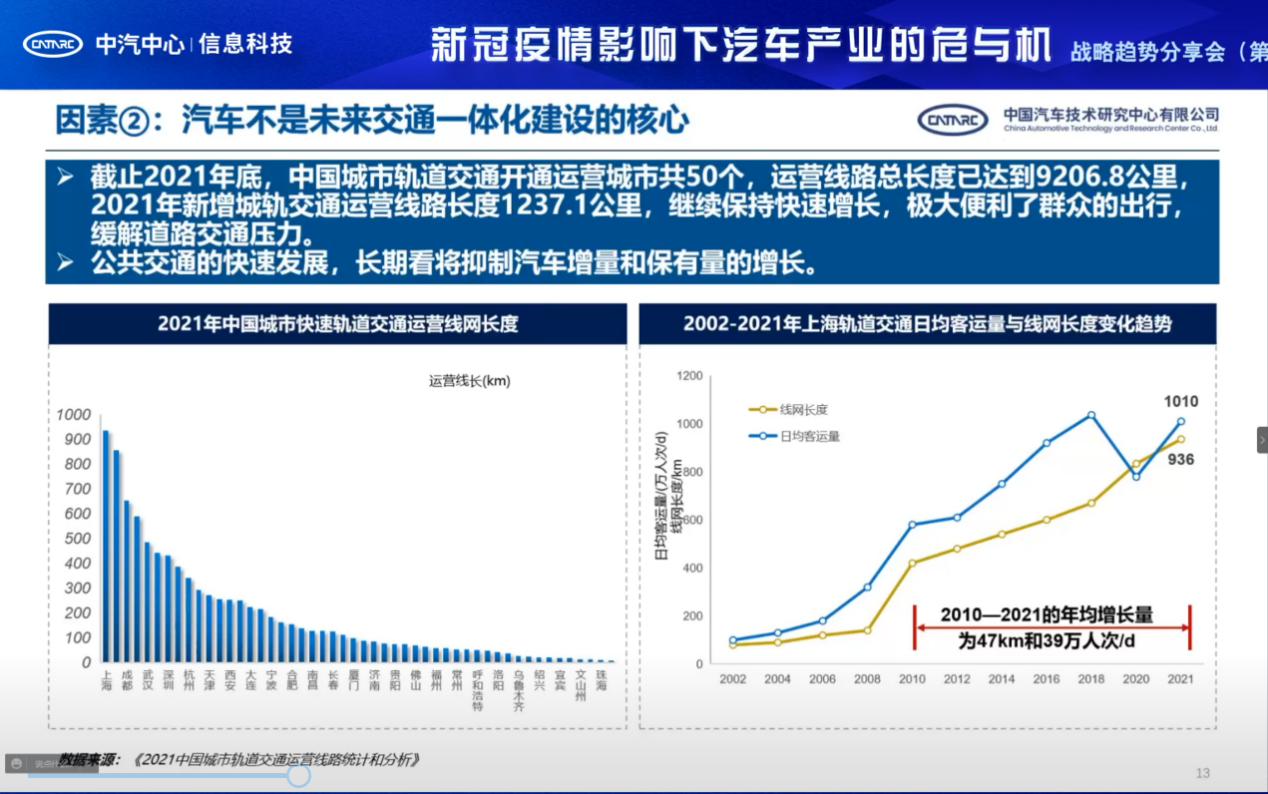

Huang Yonghe believes that in the long run, the rapid development of public transportation will certainly restrain the growth of the entire auto market.According to the data provided by Huang Yonghe, as of the end of last year, there were 50 cities in China with operational urban rail transit, and the total length of operational lines had reached 9,206 kilometers. The newly added operational rail transit line length last year was 1,237 kilometers.

In addition, the popularity of autonomous driving and sharing, as well as the decline in birth rate, will also reduce the demand for car consumption.

Tan Huilong also stated that their prediction of the peak possession of cars in China is approximately 450 to 500 million. Based on the peak possession amount, the peak sales volume is estimated to be about 30 million vehicles.

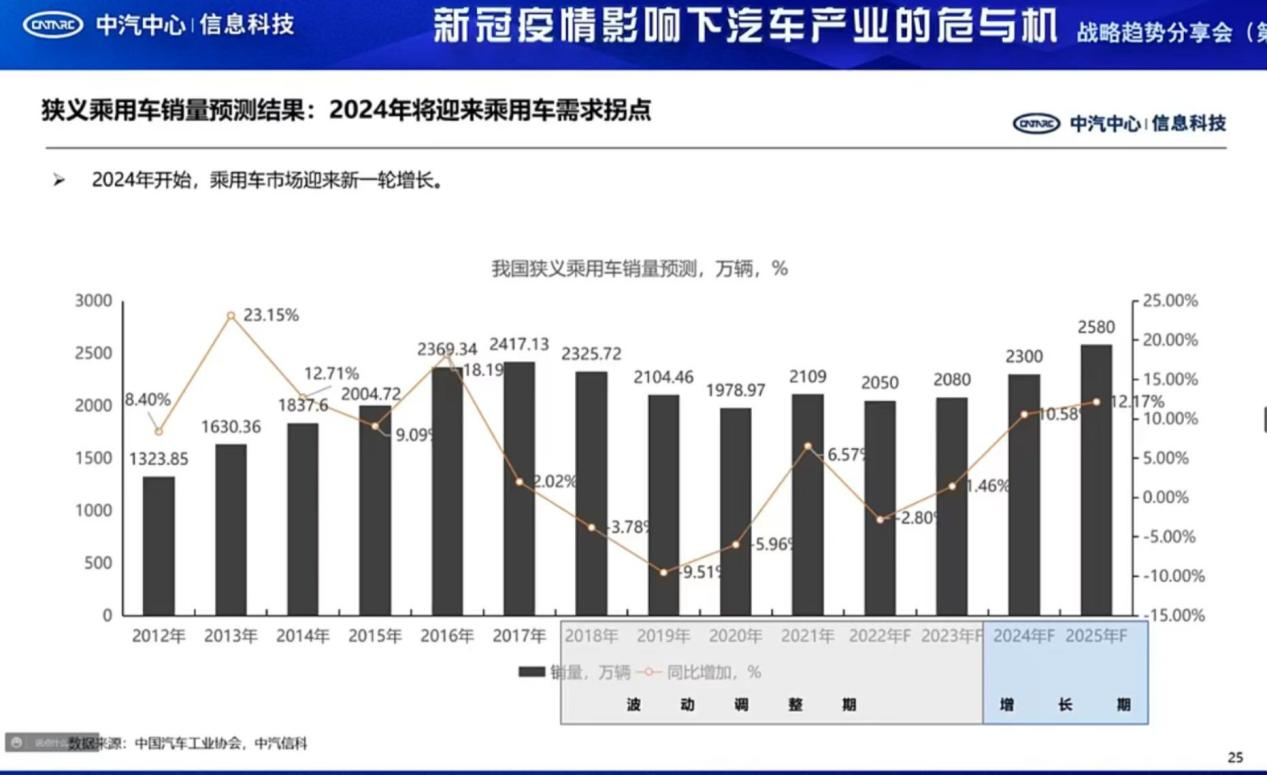

Li Xinbo believes that from 2018 to 2023, the Chinese automobile market will be in a period of fluctuation and adjustment, and there will be no obvious growth because the scrap replacement amount of automobiles in these years is relatively small. However, he believes that a large scale of scrap replacement will occur between 2024 and 2025. “That is to say, in 2024, China’s automobile market will usher in a new round of growth.”

Because returning 15 years to 2009 from 2024 is exactly the year when China’s first large-scale stimulus for automobile consumption, that is, the “auto-for-countryside” policy was implemented.

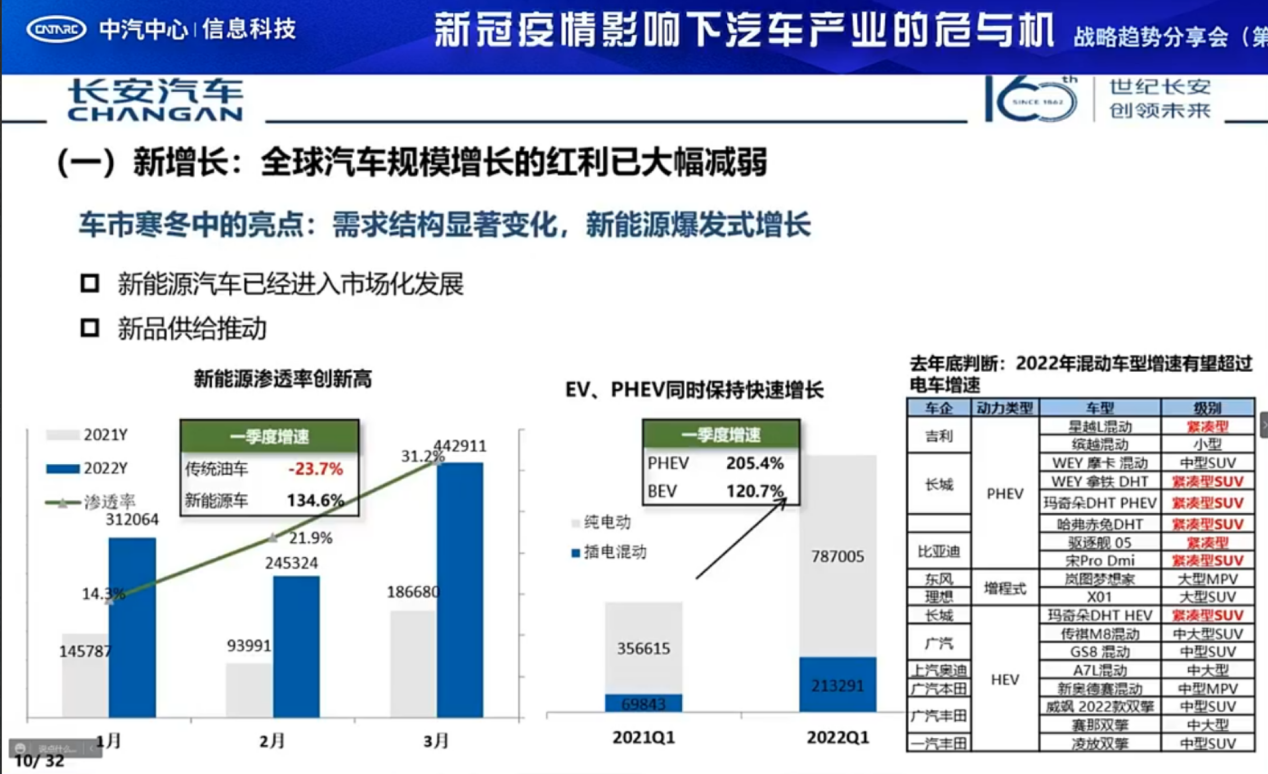

However, the experts at the meeting were optimistic about the penetration rate of new energy vehicles.

Tan Huilong believes that the slow development of the total amount of automobiles does not mean that all models are competing for stock. New energy vehicles have maintained explosive growth for many years.

New energy vehicles have entered a stage of market-oriented development from policy promotion, so consumers’ preference for new energy vehicles has clearly increased, and the advantages on the usage side, such as convenient charging, have greatly improved; new energy vehicles enjoy road rights; the driving experience of new energy vehicles is far better than that of traditional fuel vehicles.

According to Tan Huilong, from the market research, younger generations are more fond of new energy vehicles. In the age range of 18 to 40 years old, most people prefer new energy vehicles, whether they are new or replacement customers, which indicates that the explosive growth of new energy vehicles has the foundation of the market.

Ye Hai also provided a set of data. They predict that the penetration rate of energy vehicles will reach 44% by 2025, which is much higher than the official planned target. “Especially, we believe that small cars like A0 cars will have a high-speed growth, and the market share of domestic brands is expected to surpass 50% in the future.”

In Huang Yonghe’s view, the recurring pandemic in the short term, the increasing pressure of economic downturn, the declining growth rate of disposable income, and the lack of consumer confidence have also had an impact on the new energy vehicle market.

Li Xinbo agrees with Huang Yonghe’s view. He believes that according to Maslow’s hierarchy of needs theory, consumers will prioritize reducing growth-oriented needs during economic downturn, and automotive products fall into the category of growth-oriented needs. The consumption habits of residents have undergone fundamental changes under the disturbance of the pandemic.

Once automobile consumption decreases, it will have a greatly negative impact on the entire economy and even the entire automobile industry chain. Therefore, stabilizing automobile consumption and ensuring the security of the supply chain are currently the immediate priorities.

Stabilizing Consumption: Reducing Vehicle Purchase Tax and Breaking Local Protectionism

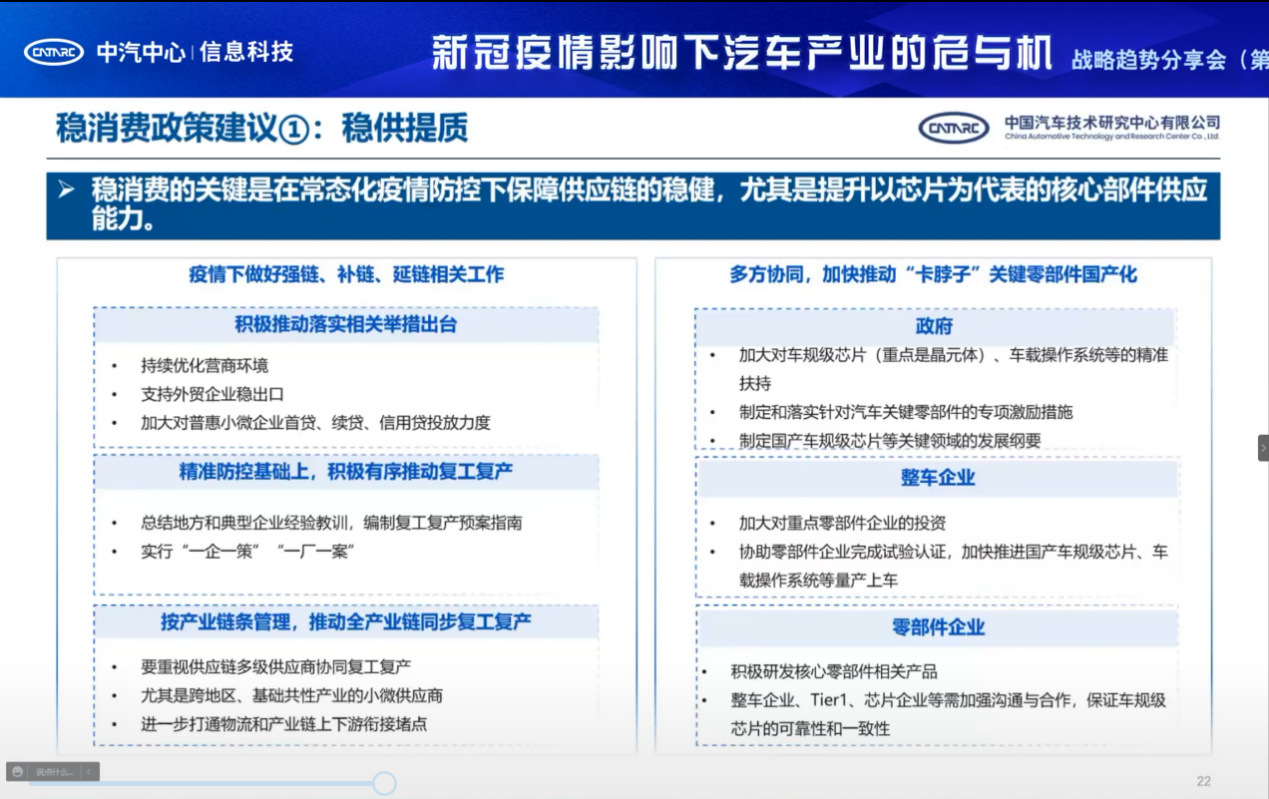

Regarding stabilizing consumption, Huang Yonghe has proposed several suggestions, the first of which is “Stable Supply and Quality Improvement”. The key to stabilizing consumption is to ensure the stability of the supply chain under normalized pandemic prevention and control, especially to improve the supply capacity of core components such as chips.

For example, in pandemic prevention and control, it is necessary to implement “one policy for one enterprise” and “one case for one factory” to implement precise measures.

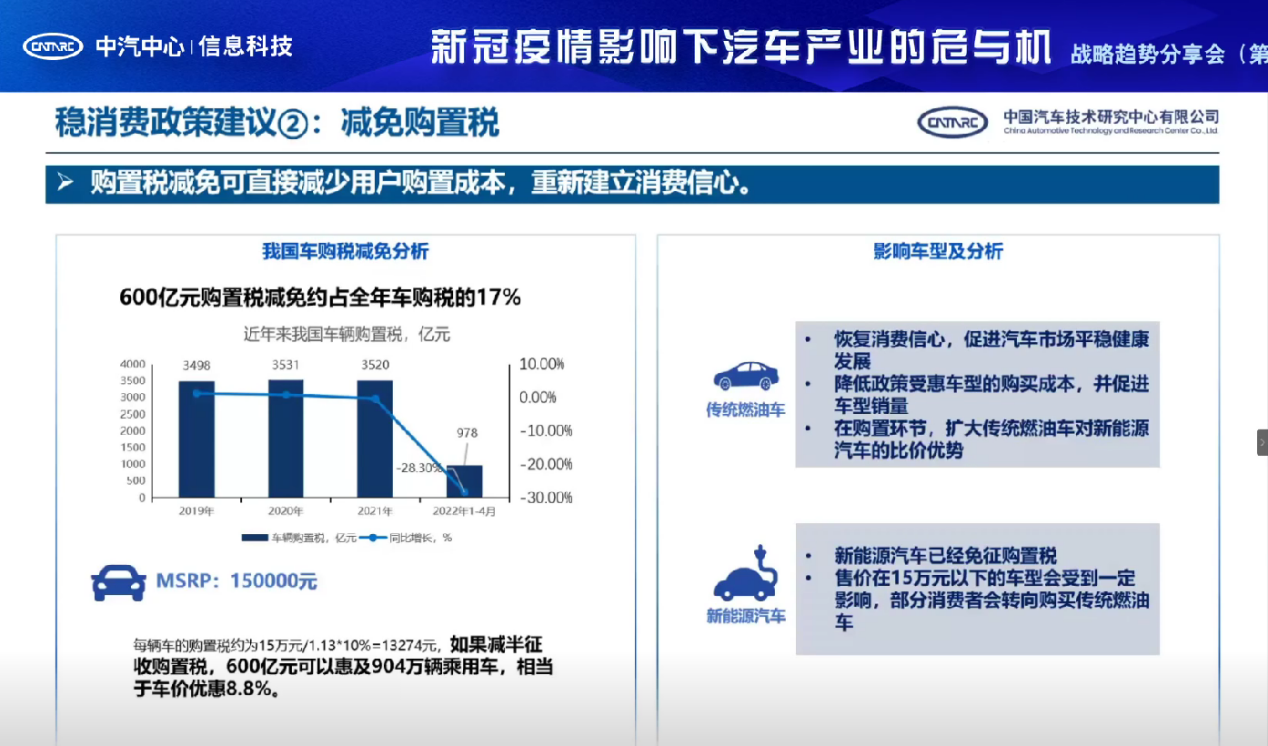

The second is to “reduce vehicle purchase tax”. Recently, the State Council’s executive meeting proposed “phased reduction of 60 billion yuan in vehicle purchase tax” to boost consumer confidence by implementing tax reduction policies.

Regarding new energy vehicles, Huang Yonghe also proposed a personal idea, hoping to formally announce the extension of the purchase tax exemption policy for new energy vehicles until the end of 2025.

Because new energy vehicles themselves are not subject to purchase tax, the exemption of purchase tax is beneficial to fuel vehicles and negative to new energy vehicles.Regarding the current policy of “halving the vehicle purchase tax for passenger cars with a displacement of 2.0 liters and below, with a bicycle price (excluding VAT) not exceeding 300,000 yuan,” Huang Yonghe pointed out that the stimulus is too strong and has a significant negative impact on new energy vehicles.

BYD has sold over 100,000 new energy vehicles for two consecutive months, and in March announced that it will no longer produce or sell traditional fuel vehicles. “If this policy only benefits traditional vehicles, in my personal opinion, it will have a greater detrimental effect on the confidence of enterprises like BYD that only produce and sell new energy vehicles, and serious negative consequences,” said Huang Yonghe.

Huang Yonghe also mentioned the issue of “local protection.” Various locations have their own “small standards” and “narrow catalogs” for new energy vehicles, and the national government has issued various documents requiring the abolition of local protection. However, the issue has not been fundamentally resolved. Huang Yonghe proposes that the State Council should supervise and implement this issue to solve it thoroughly.

Huang Yonghe also suggested that the overall reform plan for the automobile green tax system should be launched as soon as possible. “In other words, on the premise of ensuring the overall balance of automobile taxation, based on the current automobile taxation system, we should launch the overall reform plan of the automobile taxation system as soon as possible, especially increasing the regulatory effect of energy conservation, environmental protection, and low-carbon products. We should also study the automobile green taxation system based on energy efficiency indicators as soon as possible.”

This series of measures aims to reduce consumers’ purchasing costs and enhance their confidence.

Supply Chain Crisis and Strategies

In addition to stabilizing consumption, the automotive industry chain also faces major challenges in the long run.

The crisis in the automotive supply chain is divided into two aspects: common problems at the international level and problems within the Chinese industrial chain itself.

Regarding the common problems, Tan Huilong believes that the main issue is high costs. “The global economy has entered an era of high costs, which puts great pressure on the operation of the automobile manufacturing industry.”

Tan Huilong stated that high costs mainly manifest in four aspects.

“The first is the increase in the cost of human resources.” After the outbreak of the epidemic in 2020, the unemployment rate skyrocketed, but the decrease in labor participation also caused varying degrees of labor shortages in various industries, accompanied by the constant increase in wages. Taking the United States as an example, compared to the average wage in 2019, the average wage accumulated by January 2022 had increased by 10.7%.China also has similar issues. The proportion of labor force under 59 years old is shrinking rapidly, and the average wage growth in China in the past 10 years has exceeded 10%, exceeding the average GDP growth rate. Due to the relatively long automobile industry chain, the impact is also very obvious.

Secondly, after the outbreak of the epidemic and geopolitical conflicts such as the Russia-Ukraine conflict, every country is trying to build their own internal circulation and formulate backup plans for key and core technologies, resulting in a decrease in global resource allocation efficiency and cost increase. Deglobalization may lead to a decrease in global resource allocation efficiency.

Thirdly, frequent geopolitical events have made commodity prices and supply chains more fragile, and transportation costs have also increased significantly. For example, after the Russia-Ukraine conflict, many commodities that go out or come in through the Russia-Ukraine line have been greatly affected, and transportation costs have increased significantly.

Fourthly, the global green transition will also push up the price of new energy and increase the cost of green energy investment. In the short to medium term, it will still face upward pressure on energy prices.

The most difficult problem in China’s auto industry chain at present is the chip bottleneck.

Regarding the chip problem, Huang Yonghe bluntly said that it is difficult to solve within 2-3 years, mainly because the wafer manufacturing capacity is insufficient. Currently, only some IGBT and wiper control chips can be produced domestically, and other products cannot meet the requirements of automakers.

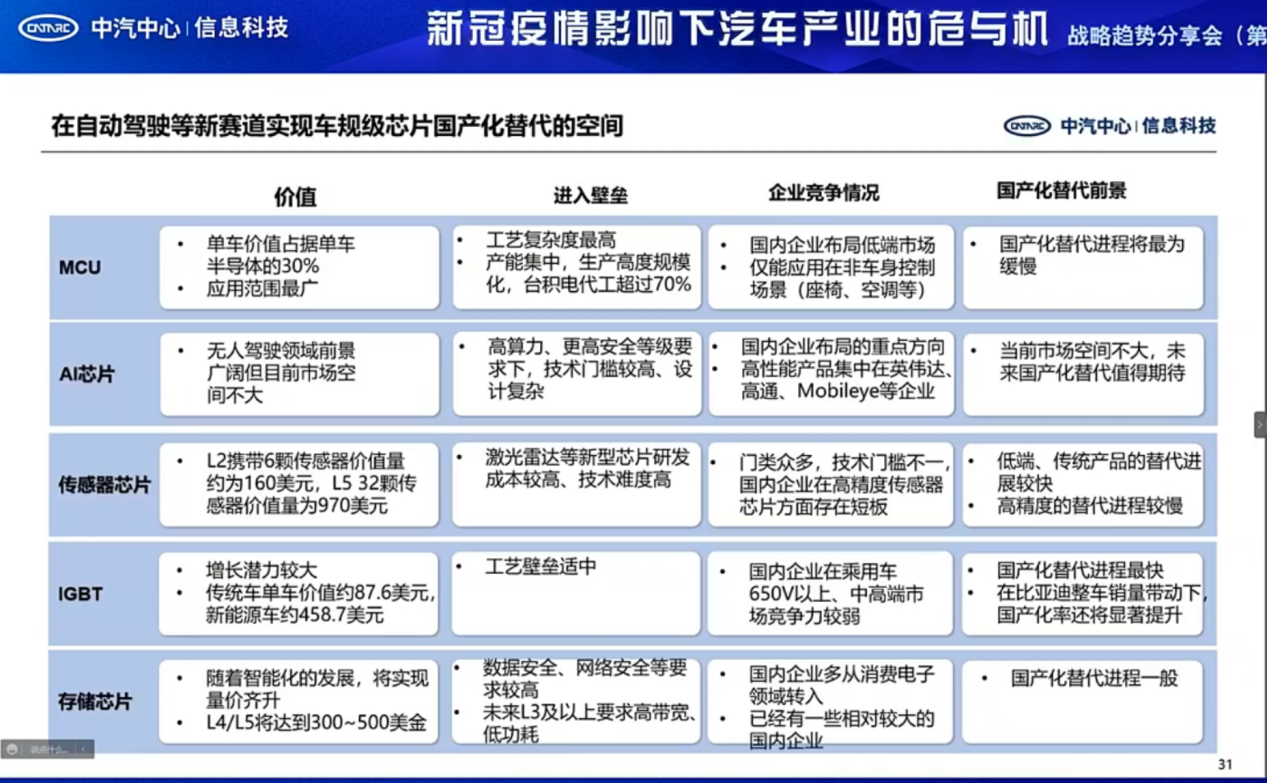

Of course, China is also actively promoting domestic substitution plans. Li Xudong said that from the overall technological strength, China only has certain advantages in chip design and packaging and testing, and relies more on foreign technology in other links of the industrial chain, especially MCU chips with high computing power and high process technologies.

In Li Xudong’s view, there are few Chinese wafer manufacturers, and currently only 9 wafer manufacturers are mainly distributed in the Yangtze River Delta region. Among them, TSMC is the most noteworthy. TSMC is currently the world’s largest wafer foundry, and its customers mainly include tech companies such as Apple, Qualcomm, and Nvidia.

Of course, there is already a trend of domestic substitution for automotive-grade chips.

Li Xudong introduced that currently, the domestic substitution process for IGBT is the fastest. IGBT has a relatively high proportion in the power control system of new energy vehicles, and the process barriers are moderate, making it relatively easy for Chinese companies to enter the market.For the AI chips used in autonomous driving, due to the relatively small market demand, Chinese companies’ investment and funding for AI chips are smaller compared to those of IGBT. However, with the increasing demand for autonomous driving, the prospect of domestically produced AI chips replacing imported ones is still promising.

The domestic replacement process of other important MCU and memory chips is still relatively slow. In Li Xudong’s view, the difficulty of MCU chips lies in their wide range of applications, making it challenging for domestic companies to cover all aspects. The solution is to gradually break through on specific components.

Another challenge is in wafer production; 70% of MCU chips are produced by TSMC, so it will take some time to achieve true independent supply.

To promote the localization and substitution of automotive chips, Li Xudong suggests working on four aspects:

Firstly, it is recommended to establish a special support fund to support domestic chip companies in their technical research and development and testing work.

Secondly, it is suggested to promote domestic chip companies to break through the critical technology of reliable design and conduct research on standards such as ISO26262 in the verification of automotive chips, helping chip enterprises design chips that meet the requirements of vehicle regulations from the source.

Thirdly, it is recommended to promote testing and packaging companies to implement the TS16949 quality system. Only after reaching TS169 quality system can automakers safely use domestically produced chips.

Finally, speed up the formulation of relevant domestic reliability basic standards research, and coordinate cooperation among all parties to complete the domestic standard system.

Competition among Automakers: Cost Reduction and Value Chain Restructuring

In the view of Li Xinbo and Tan Huilong, enterprise competition has also entered a new stage.

Survival key: reducing costs

Facing the high cost of the automotive industry, Li Xinbo believes that reducing costs is still the top priority for automakers to survive and develop.

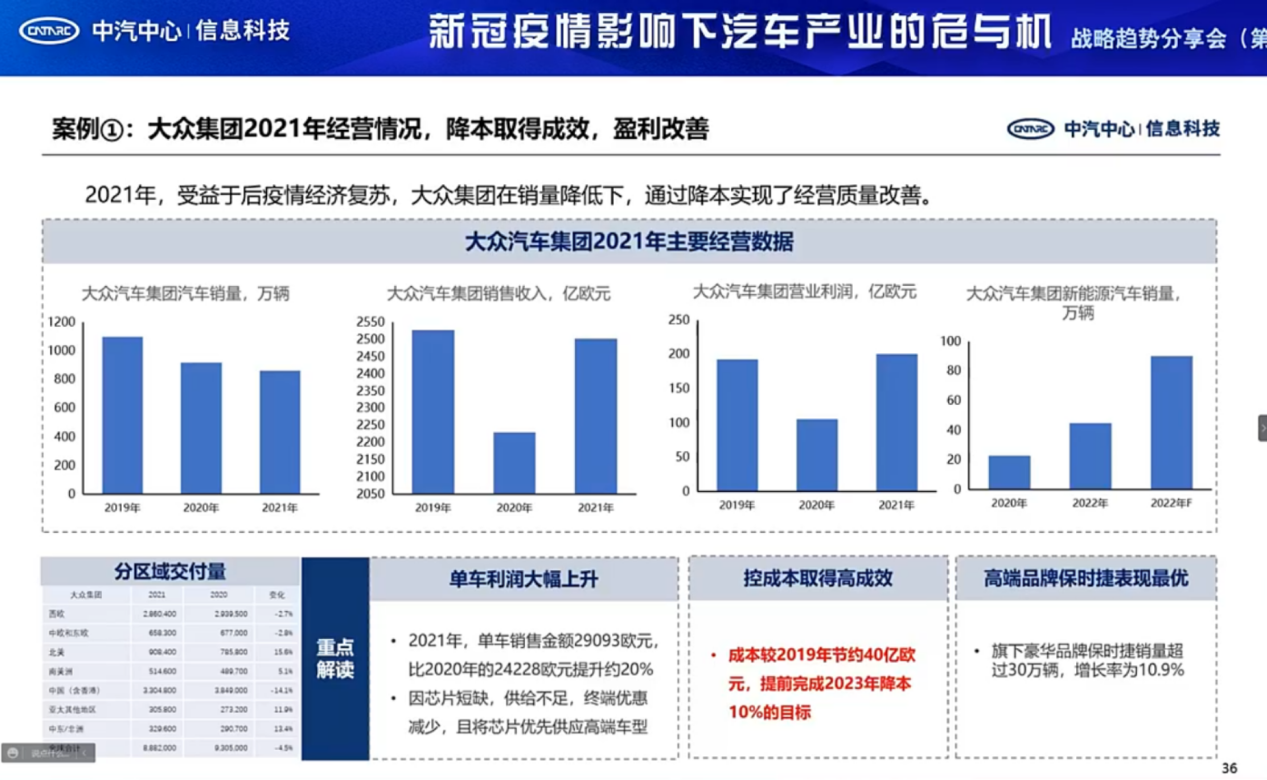

Li Xinbo analyzed the Volkswagen Group as an example: From the perspective of sales, the Volkswagen Group is experiencing a period of sales decline. On the contrary, the profit per vehicle has increased significantly.

Li Xinbo believes that this is the result of Volkswagen Group’s cost focus strategy. Four out of the five parts of Volkswagen Group’s 2030 New Auto Strategy focus on reducing costs.In terms of economic indicators, Volkswagen proposes to reduce fixed costs by 5% and material costs by 7% by 2023. In terms of platform development, Volkswagen will adopt the SSP platform, which is the next generation of electromechanical integration platform, and the core of platform strategy is to reduce costs. In terms of batteries and charging, Volkswagen proposes to introduce standard cells, and reduce costs by 50% by 2030 by increasing the universality of cells. In terms of mobile travel solutions, the focus is on developing high-level autonomous driving, which in addition to solving traffic safety issues, can also improve travel efficiency and continue to reduce costs.

Through the case of Volkswagen Group, it can be seen that the profit model of new energy vehicles has undergone fundamental changes, and future profits may depend on ecological profitability. Li Xinbo uses new forces enterprises as an example, where enterprise A sold 550,000 vehicles in 2021 and its operating income increased by 38% compared to the same period last year, but its net profit decreased by 28% compared to 2020, which is caused by the insufficient ability to control costs.

Further analysis reveals that the government subsidies included in A’s current report in 2021 reached as high as 2.263 billion yuan, if the amount is excluded, the profit for this period was only 782 million yuan.

Regarding point accumulation, in 2021, Enterprise A can earn at least 943 million yuan in points revenue. The problem is that in recent years, there has been a significant improvement in the supply-demand balance of points. Mainstream negative points enterprises can offset their points by affiliated enterprises, including SAIC-GM, FAW-Volkswagen, etc. In the future, point trading prices may further decrease, resulting in lower point income for new energy vehicle enterprises.According to this, Li Xinbo drew several conclusions. Firstly, new energy vehicle enterprises that have not achieved economies of scale are currently unable to achieve profitability. Secondly, after the subsidy exits, only new energy vehicle enterprises with continuing financing capability can survive. If profitability cannot be improved, many new energy vehicle enterprises will be eliminated because capital pursues profits. If it continues to be unprofitable, the financing situation of the enterprise will deteriorate. Thirdly, all current traditional automobile enterprises have not missed the strategic window for developing new energy vehicles, that is, it is not too late for these traditional automobile enterprises to vigorously develop new energy vehicles now.

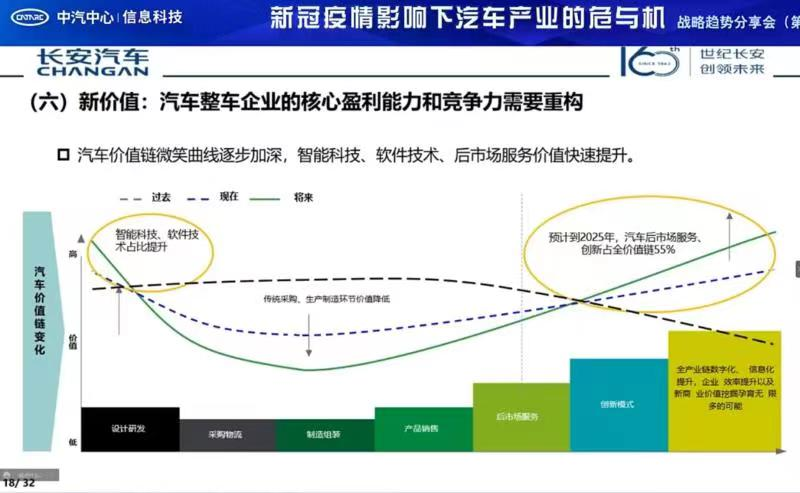

Value chain reconstruction and supply chain reshaping

The value chain of the new energy vehicle industry is already different from that of traditional car companies. Tan Huilong explained that the characteristics of the value chain of the traditional automobile manufacturing industry follow the smile curve of the manufacturing industry, that is, the value-added by the manufacturing enterprise is relatively high at the R&D and marketing ends.

Tan Huilong believes that there is still a relatively high profit contribution on the production side. However, in the era of intelligent and connected vehicles, products based on software will greatly increase the added value of front-end and back-end.

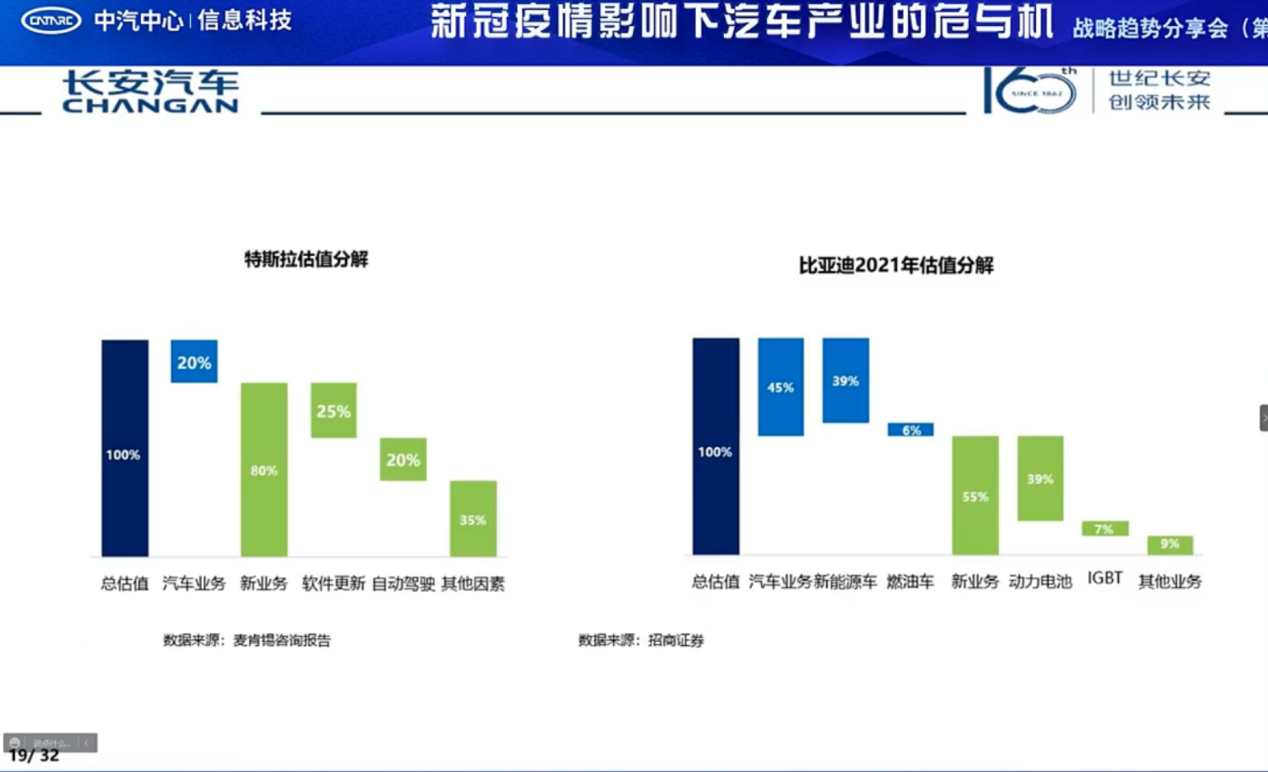

Tan Huilong analyzed Tesla and BYD as examples. In 2020, only 20% of Tesla’s valuation was from the automotive business, and the value of new business accounted for 80%, of which software updates accounted for 20% of Tesla’s total value. Similarly, among Chinese brands, BYD’s new business accounted for 55% of its valuation in 2021.

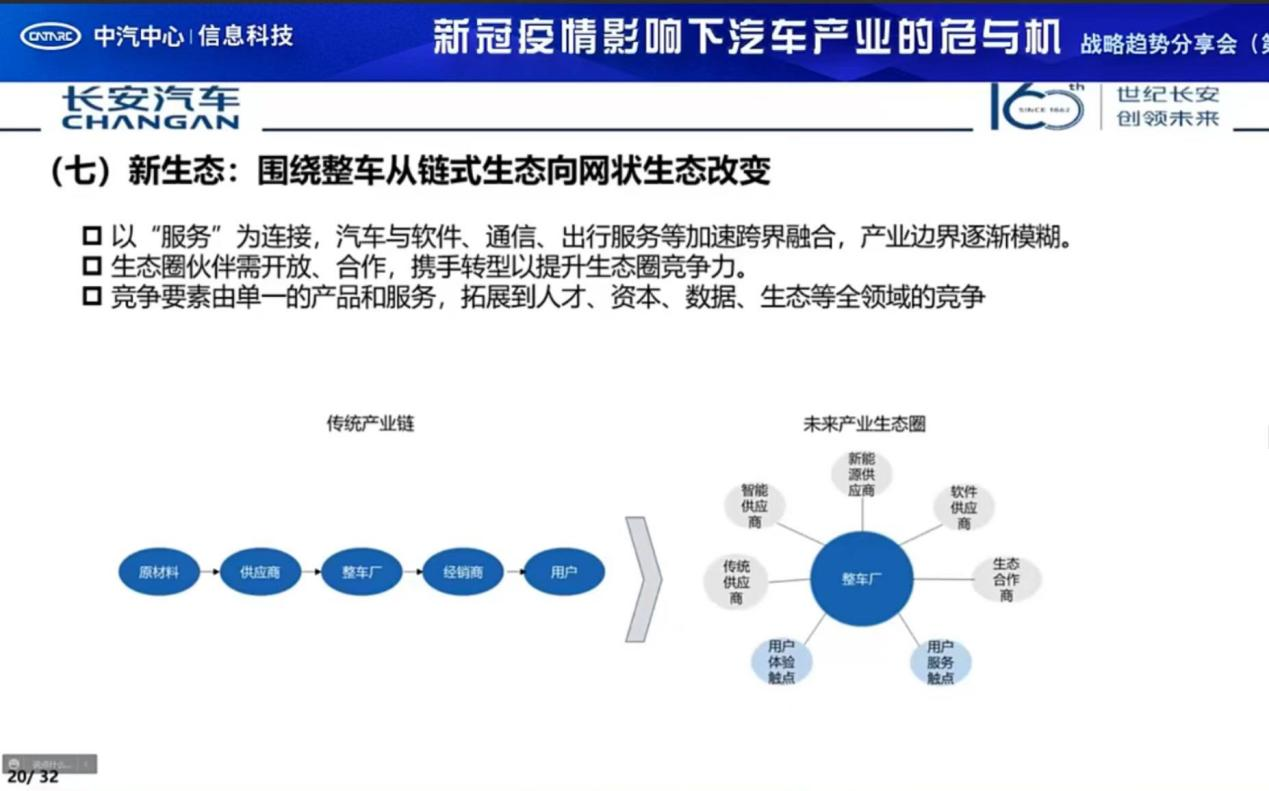

Value chain reconstruction will also bring about changes in the automotive ecosystem. Tan Huilong believes that this linear relationship of the traditional chain is transforming into a meshed ecosystem, forming a highly coupled relationship. On the traditional industrial chain, the main relationship between a car company and its upstream and downstream is mainly the supply relationship.

Currently, this relationship is transforming into a strategic partnership. All participants in the ecosystem are deeply involved in the entire value chain of user research, product definition, technology development, and customer management.

Internet technology companies such as Huawei and Tencent have already been deeply involved in the creation of the intelligent and connected value ecosystem, participating in the entire process from customer demand research to product development with vehicle enterprises, not only to make it easier and more efficient for partners to develop, but also to bring ultimate travel experience to consumers.In this process, there will also be a power struggle among these dominant enterprises regarding the core technological capabilities for intelligentization, as well as customer resources. In addition, tech companies like Baidu, Xiaomi, Huawei, etc. are still ambitious about making cars, which will trigger a battle between new and old forces in the Chinese car market.

Tan Huilong believes that this is good news for China’s automobile industry as it promotes market prosperity and revitalizes the industry.

The development of intelligent connected vehicles, coupled with the ongoing global spread of the epidemic and economic recession, puts pressure on cost control and efficiency in competition among enterprises. Only by surviving the hard winter can we usher in the next round of growth.

This article is a translation by ChatGPT of a Chinese report from 42HOW. If you have any questions about it, please email bd@42how.com.