After seven and a half years of being listed, NIO has achieved quarterly profitability for the first time, with a net profit of 283 million yuan.

This evening, Beijing time, NIO released its financial results for the full year and fourth quarter of 2025. Key financial data for the fourth quarter are as follows:

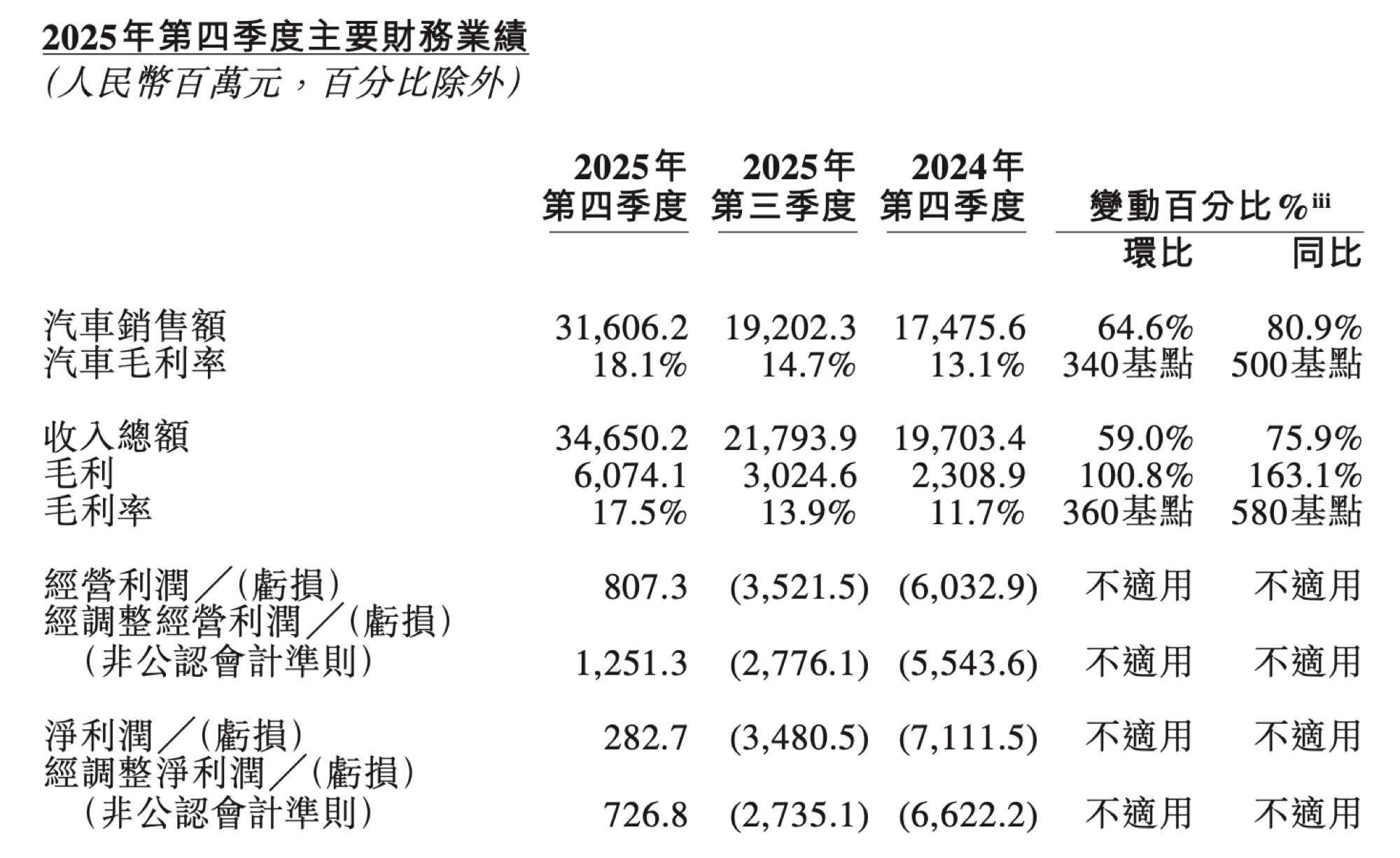

- Quarterly revenue reached 34.65 billion yuan, a historical high, with a 59% quarter-on-quarter increase and a 75.9% year-on-year increase.

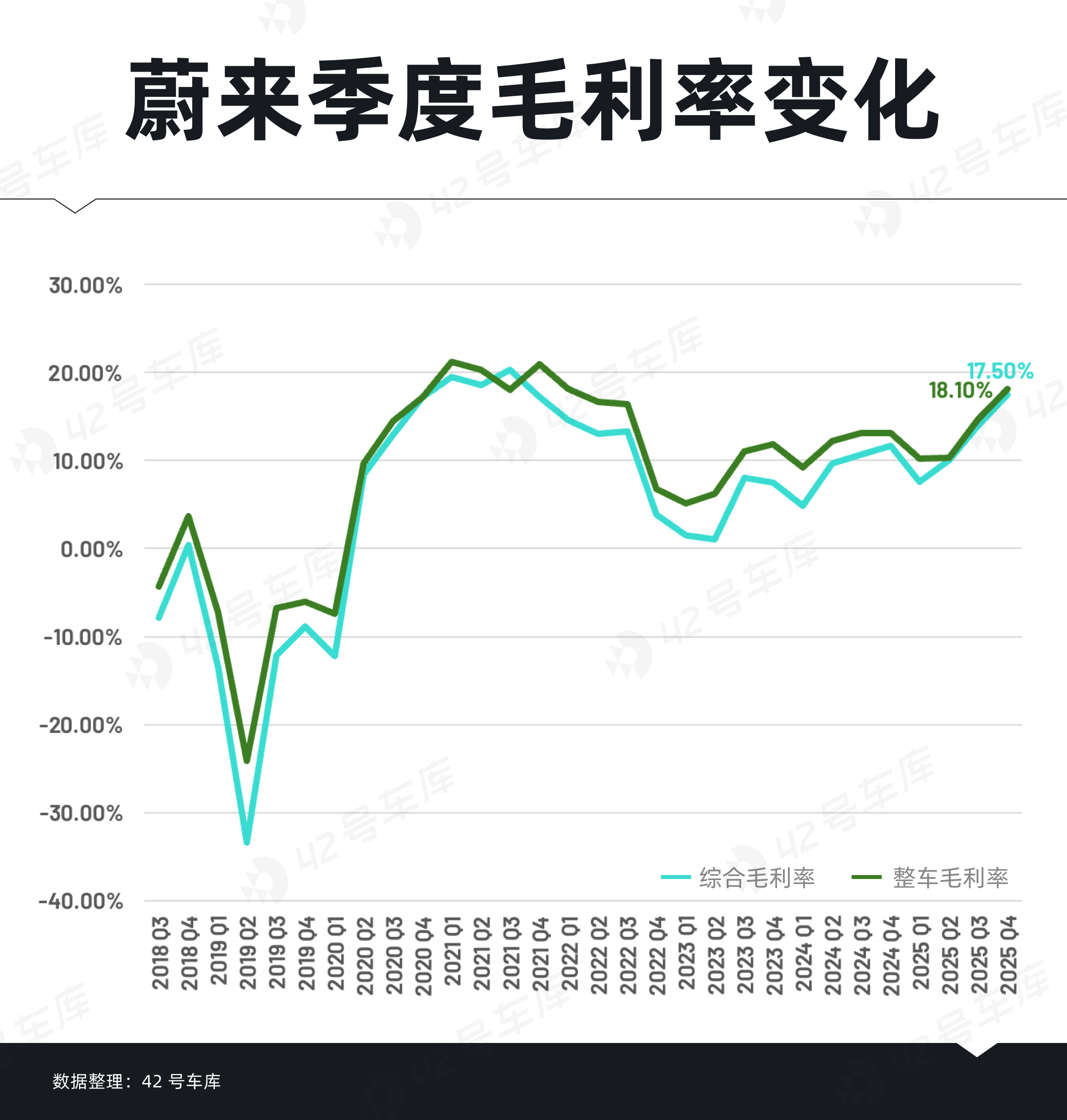

- Vehicle gross margin stood at 18.1%, while the overall gross margin was 17.5%, both being the highest since 2022.

- Net profit was 283 million yuan, marking NIO’s first profitability. This contrasts with a net loss of 7.112 billion yuan in the same period last year and a net loss of 3.481 billion yuan in the previous quarter.

- Operating profit was 807 million yuan, compared to an operating loss of 6.033 billion yuan in the same quarter last year and an operating loss of 3.522 billion yuan in the previous quarter.

- Quarterly deliveries reached 124,800 vehicles, including 67,400 NIO brand vehicles, 38,300 ONVO brand vehicles, and 19,100 Firefly vehicles. Deliveries grew by 71.7% year-on-year and 43.3% quarter-on-quarter.

Key data for the year 2025 includes:

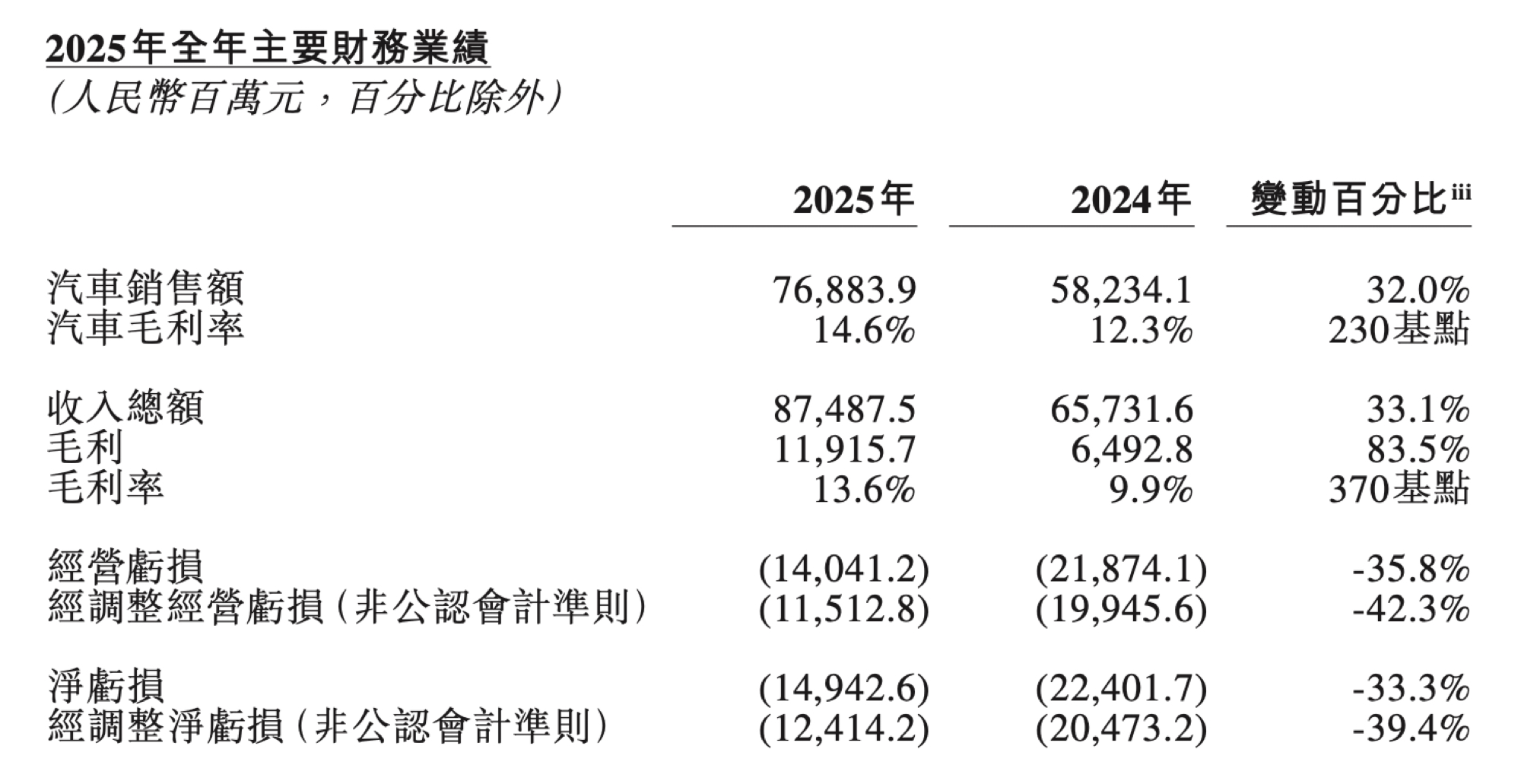

- Annual revenue of 87.488 billion yuan, up 33.1%.

- Annual net loss of 14.943 billion yuan, down 33.3%; annual operating loss of 14.041 billion yuan, down 35.8%, demonstrating a significant narrowing of losses.

- Delivery of 326,000 vehicles, approximately 38% more than in 2024.

So, how did NIO achieve quarterly profitability?

In fact, last July, Li Bin provided a formula for NIO’s profitability: achieving total monthly sales of over 50,000 vehicles across three brands, maintaining a gross margin between 17% – 18%, sales and management expenses at around 10%, and research and development expenses at 6% – 7%.

In the fourth quarter of 2025, NIO achieved an overall gross margin of 17.5%, with sales, general, and administrative expenses of 3.537 billion yuan (10.2% of revenue) and R&D expenses of 2.026 billion yuan (5.8% of revenue). However, there is still a gap of approximately 25,000 vehicles to reach the 150,000 quarterly vehicle sales target.

At 8 p.m. tonight, NIO will hold a conference call on its fourth-quarter and full-year 2025 results. NIO’s founder, Chairman, and CEO Li Bin, along with CFO Steven Wei Feng, will address questions related to new models, the new Shenzhi chips, and the impact of ultra-fast charging on battery swapping.

As of press time, NIO’s pre-market price on the NYSE is $5.46, up 10.33%, with a market cap of $13.73 billion.## First Quarterly Profit

NIO achieved its first quarterly profit, marking 30 quarters since its NYSE debut.

Earnings report shows that in Q4 2025, NIO net income reached 283 million yuan, with operating profit at 807 million yuan. Adjusted net income (Non-GAAP) was 727 million yuan, and adjusted operating profit (Non-GAAP) was 1.251 billion yuan.

Despite turning a quarterly profit, NIO’s profitability remains fragile.

We have compiled NIO’s profit and loss data over the past 30 quarters since 2018. NIO experienced a cumulative net loss of 99.72 billion yuan over the first 29 quarters. The curve shows that NIO was close to profitability around 2021 but missed it, leading to an expanding loss from 2023 to 2025, peaking at a quarterly loss of 7.112 billion yuan in Q4 2024.

A turning point occurred in 2025, as NIO’s losses narrowed over the first three quarters, culminating in profitability in Q4. Overall, in 2025, NIO reported a net loss of 14.943 billion yuan, a decrease of 33.30% compared to the previous year.

Therefore, achieving full-year profitability in 2026 naturally became NIO’s new goal. NIO CFO Steven Feng stated that in 2026, NIO aims to achieve Non-GAAP annual profitability.

According to the financial report, NIO’s revenue in Q4 2025 reached an all-time high of 34.65 billion yuan, up 75.9% year-over-year and 59% quarter-over-quarter. Notably, automobile sales amounted to 31.606 billion yuan, increasing 80.9% year-over-year and 64.6% quarter-over-quarter, showing significantly faster growth.

Looking at the full-year 2025 data, NIO’s total revenue was 87.488 billion yuan, reflecting a growth of 33.1% compared to 2024, maintaining a rapid growth trajectory.

Next, we examine gross margin data, which is crucial for a company’s profitability. In Q4 2025, NIO’s overall gross margin was 17.5%, with a vehicle gross margin of 18.1%.

For the full year 2025, NIO’s gross margin was 13.6%, improving by 370 basis points from 2024; meanwhile, the vehicle gross margin was 14.6%, compared to 12.3% in 2024.

In terms of operating expenses, NIO has become noticeably more prudent in its spending.In the fourth quarter of 2025, NIO’s R&D expenses amounted to RMB 2.026 billion, a year-on-year decrease of 44.3% and a quarter-on-quarter decline of 15.3%. For the full year 2025, R&D expenses totaled RMB 10.605 billion, a decrease of 18.7% compared to 2024.

The financial report provided different explanations for the year-on-year and quarter-on-quarter decrease in R&D expenses, identifying organizational optimization and employee cost reductions as common factors. Compared to the same period in 2024, the reduction in fourth-quarter R&D expenses in 2025 was primarily due to the reduction in R&D personnel costs from organizational optimization, as well as decreases in design and development expenses resulting from the different development stages of new products and technologies. Compared to the third quarter of 2025, the decline was mainly due to the reduction in R&D personnel costs from organizational optimization.

In the fourth quarter of 2025, NIO’s selling, general, and administrative expenses were RMB 3.537 billion, a year-on-year decrease of 27.5% and a quarter-on-quarter decline of 15.5%. For the full year 2025, these expenses were RMB 16.088 billion, an increase of 2.2% compared to 2024.

NIO attributes the fourth-quarter decline in selling, general, and administrative expenses both year-on-year and quarter-on-quarter to reductions in marketing and other support staff and associated costs resulting from organizational optimization, as well as a decrease in sales and marketing activities.

According to the latest financial data from NIO, as of December 31, 2025, NIO’s cash and cash equivalents, restricted cash, short-term investments, and long-term deposits totaled RMB 45.9 billion, with current liabilities exceeding current assets.

For the first quarter of 2026, NIO expects vehicle deliveries to be between 80,000 and 83,000 units, representing a year-on-year increase of 90.1% to 97.2%. Total revenue is expected to be between RMB 24.482 billion and RMB 25.176 billion, representing a year-on-year growth of 103.4% to 109.2%.

New Cars, New Chips, Battery Swap VS Ultra-Fast Charging

At 8 PM tonight, NIO held its fourth-quarter and full-year 2025 earnings conference call. During the call, NIO CEO William Li and CFO Steven Feng addressed various topics such as the new cars and the second chip from NIO, first-quarter sales and gross margin outlooks, and the impact of ultra-fast charging on battery swapping.

According to the plan, the NIO ES9 will be launched in the second quarter of this year. Concurrently, the ET5, ET5T, ES6, and EC6 will undergo annual updates, and a large five-seater SUV based on the ES8 platform will be launched in the third quarter. Within the ONVO brand, the L80 will be launched in the second quarter, and the L60 and L90 will also receive product upgrades and refreshments.

Given this product lineup, NIO will have five large SUVs available for sale this year, boosting Steven Feng’s confidence in the company’s gross margin performance.

Feng expects NIO’s vehicle gross margin to remain at the fourth-quarter level of last year during this year’s first quarter. This is due to the backlog of orders for the NIO ES8 and the superior gross margin performance of large SUVs (the ES8 achieved a gross margin of over 20%, nearing 25% in Q4 2025).However, at the supply chain end, components such as copper, lithium carbonate, and memory chips are experiencing price increases. Qu Yu believes that the price hike has just started, and the negative impact will be controlled within a reasonable range.

While discussing the Shenzhi chip, Li Bin stated that the second Shenzhi chip has completed tape-out and is in the mass production phase.

The second Shenzhi chip targets the mid-range market, using a 5 nm process. Its positioning is slightly below the NX9031, yet it offers performance equivalent to approximately three Orin-X chips. Li Bin noted that this chip is significantly more cost-effective compared to the NX9031. Moreover, early testing and engagement are already underway with industry clients, though Li Bin did not disclose the names of external clients.

Recently, ultra-fast charging vs. battery swapping has become a hot topic within the industry. With the emergence of ultra-fast charging, does battery swapping still hold an advantage?

Li Bin believes, “Charging and battery swapping are not mutually exclusive. We have recently observed advancements in charging speed by some companies within the industry, which are undoubtedly great technological developments. However, in the foreseeable future, we believe that the speed and experience of fast charging cannot surpass battery swapping, which is a consensus recognized within the industry.”

Li Bin emphasized that battery swapping is a systemic solution, not merely a question of “faster or slower.” He outlined the advantages of the battery swapping model from three perspectives.

Firstly, battery swapping can systematically address the disparity between car and battery lifespan. Currently, the industry’s common standard is an 8-year/160,000 km warranty with a battery health rate of 70%, but if a car is to be used for 15 years, safety becomes a significant concern post-warranty. In the battery swapping model, with the incorporation of long-life battery design, charge-discharge strategies, and health monitoring measures, Li Bin believes it can significantly enhance battery safety and maximize battery longevity.

Secondly, Li Bin considers battery swapping stations as distributed energy storage facilities that can participate in electricity storage and consumption, as well as grid interaction, offering substantial commercial opportunities and value. Compared to standard energy storage and charging, NIO can reduce power loss by 6%, providing better economic efficiency.

Thirdly, the continuous deployment of the battery swapping network not only improves user experience but also grants significant competitive advantages for NIO’s long-term commercial success.

Discussing the progress of NIO’s assisted driving systems, Li Bin remarked that there are two key indicators to evaluate their effectiveness: the duration of assisted driving usage and the reduction in accidents.

Data shows that after updating to NMW in February, NIO users’ assisted driving usage time increased by 80% compared to January. However, NIO has not yet deployed all cloud computing resources. As planned, NIO will release two major updates for its assisted driving system in the second and fourth quarters of this year.From a numerical standpoint, NIO’s recent profit does not signify that the company has completely emerged from its loss cycle. An accumulated loss approaching ten billion yuan over the past 30 quarters remains a heavy burden on the financial statements.

More importantly, NIO’s profitability is still predicated on maintaining the variables of sales volume, gross margin, and expense ratio within an optimal range. Any fluctuation in these factors could potentially disrupt profitability. Therefore, this quarterly profit is not the end, as the true test awaits in 2026.

This article is a translation by AI of a Chinese report from 42HOW. If you have any questions about it, please email bd@42how.com.