This year, Li Bin has repeatedly emphasized one goal: achieving profitability by Q4 2025. However, from the just-released Q2 financial report, the path to profitability still appears somewhat convoluted.

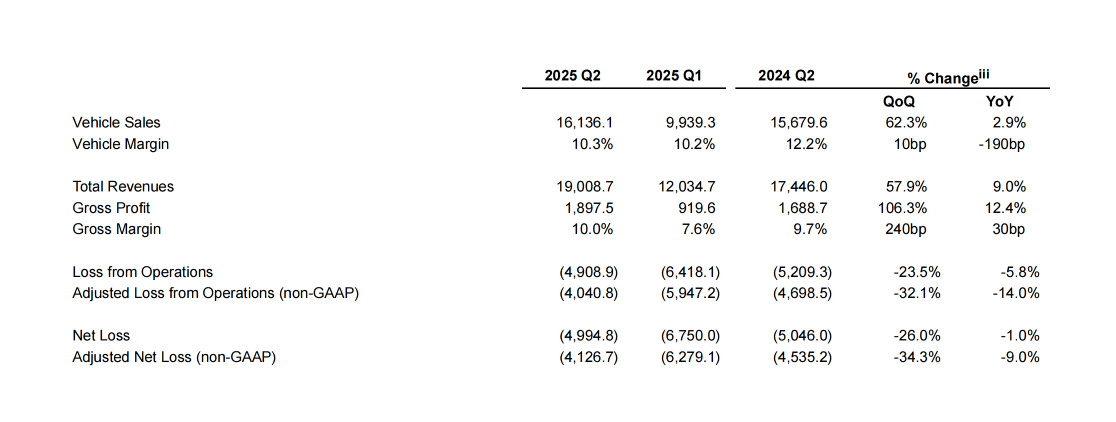

According to NIO’s 2025 Q2 financial report released today, the company achieved a total revenue of 19.01 billion yuan, an increase of 9% year-on-year and 57.9% quarter-on-quarter. The gross profit margin recovered from 7.6% in Q1 to 10%. The net loss was 4.995 billion yuan, a noticeable reduction from the 6.75 billion yuan in the first quarter, yet there’s still a considerable gap from achieving true breakeven.

On paper, NIO’s financial indicators seem to signal a turnaround, but a closer inspection reveals unresolved concerns—though revenue rose quarter-on-quarter, the year-on-year growth rate slowed, the gross profit margin is yet to stabilize, and cash flow remains under pressure. NIO is still quite a distance away from truly emerging from its loss predicament.

Beyond the single quarter’s loss, the more pressing question for the external world might be: Does NIO possess the fundamentals to turn losses into profits within the year?

After all, in this race against time, NIO is accelerating at full speed, but the capital market is not a cheerleader but an adjudicator, focused solely on results.

Hanging in Mid-air: The Profit Promise

In Q2 2025, NIO presented a financial report that seemed to both incur losses and show growth, with revenue rapidly recovering, the gross profit margin stopping its decline and rebounding, effective cost reductions, and a notable narrowing of losses. Yet, from a long-term perspective, NIO has yet to cross the profitability threshold.

Firstly, there’s a recovery on the income side. Driven by the “5566” model upgrade launch, ET9 deliveries, and a rebound in demand for the ONVO L60, NIO delivered 72,056 vehicles in Q2, a quarter-on-quarter growth of 71.2%, successfully meeting the delivery guidance of 72,000 to 75,000 units set during the Q1 financial report release. This includes 47,132 NIO brand vehicles, 17,081 ONVO brand vehicles, and 7,843 Firefly brand vehicles.

The increase in sales directly propelled automotive sales revenue to 16.14 billion yuan, a quarter-on-quarter rise of 62.3%, the highest value in the past five quarters, also boosting total revenue to 19.01 billion yuan. The concurrent rise in deliveries and revenue is currently NIO’s most positive signal.

NIO’s gross profit performance in the second quarter also showed recovery. The vehicle gross profit margin returned to 10.3%, approximately the same level as the previous year; the overall gross profit margin rebounded to 10.0%, marking a new high over the past three quarters. Gross profit reached 1.898 billion yuan, growing over 100% quarter-on-quarter. This partly reflects the initial effectiveness of model mix optimization, and another part benefits from vehicle cost reduction and stabilizing pricing strategies.

However, another aspect of the financial report is still glaring. Despite revenue and gross profit increases, net losses remain at 4.995 billion RMB. Although it’s a noticeable reduction compared to the Q1 loss of 6.75 billion, it still remains high.

A somewhat pessimistic figure is that NIO’s total liabilities currently stand at 93.4 billion RMB, with total assets at 100 billion RMB, leading to an asset-liability ratio exceeding 93%. While slightly reduced from Q1’s 100.28%, it remains significantly higher than Xpeng’s 67% and LI’s 54%.

Cost control has become crucial for NIO’s attempt to stop the bleeding. Adjusted operating losses for Q2 decreased to 4.041 billion RMB, a 32.1% sequential drop. Sales and management expenses have decreased compared to Q1, while R&D expenses stayed roughly constant, reflecting an intention to gradually tighten internal operations and shift gears in growth. Yet, the gross profit of less than 1.9 billion is insufficient to cover R&D expenses of 3 billion and around 4 billion in selling, general, and administrative expenses.

As for cash reserves, by the end of June, NIO held a total of 27.2 billion RMB in cash, short-term investments, and long-term deposits, experiencing a slight sequential increase. This provides a certain buffer for brand expenditures on new product deliveries, further establishment of sub-brands, and infrastructure development.

Overall, the improvement in some Q2 financial data stems more from the sequential recovery brought about by scale effects rather than a fundamental improvement in profitability structure. As there are still two quarters left before reaching Li Bin’s stated goal of Q4 profitability, currently, NIO remains on the edge of a cliff, not yet stepping into the safe zone.

Is the Acceleration Fast Enough?

Looking back at the second quarter, NIO’s business pace was nearly maximized across the board. The new “5566” model completed its replacement, effectively supporting NIO’s mid-to-high-end brand foundation. Although ET9’s delivery scale is not large, it has a relatively positive impact on NIO’s brand strength. The sales of ONVO L60 continuously climbed, while the Firefly brand, targeting the entry-level market, achieved its first large-scale deliveries in the second quarter.

The three brand lines truly formed a delivery synergy in the second quarter, and this pace accelerated upon entering the third quarter.

In July, NIO’s three brands together delivered 21,017 vehicles, which swiftly soared to 31,305 in August, totaling over 830,000 deliveries. By the end of July, ONVO’s second model, the L90, was officially launched and commenced delivery.

This vehicle became one of the key models determining NIO’s profitability in the fourth quarter. Li Bin revealed that within three days of L90’s launch, it ranked among the top three in weekly sales of large SUVs, only trailing AITO M8. He also mentioned in today’s financial report conference call that L90’s order numbers exceeded expectations, reaching a record 10,575 deliveries in its first month of launch. The robust sales of L90 have enhanced the momentum of the ONVO brand and spurred demand for the L60, with L60 orders reaching a new high for the year in August.

On August 21st, the pre-sale of the new ES8 was announced, with official market release and delivery to commence in late September. This model is receiving positive market feedback. During the earnings call, William Li shared the delivery data for the Firefly: over 10,000 units delivered within three months, securing the top position in the high-end pure electric small car market.

According to William Li, to ensure the production capacity of current models, NIO will not deliver new models across its three brands this year; however, at least three models will be released next year: ONVO L80, NIO ES9, and ES7.

In the past few months, NIO has been actively building its infrastructure. By the end of August, the company had constructed a total of 3,539 battery swap stations and 4,755 charging stations globally. On August 16th, NIO’s G318 Sichuan-Tibet battery swap route was officially completed.

Overall, NIO is striving to establish a high-growth, highly-executive brand image in the third quarter with a dense new product lineup, more cost-effective product offerings, and faster infrastructure deployment. However, whether the current growth rate can translate into real profitability, preserve profit margins amidst price wars, and stabilize cash flow amid high investments are the upcoming challenges NIO must confront.

Q4 Monthly Delivery Target of 50,000 Units

Following the release of NIO’s second-quarter financial report today, NIO CEO William Li and CTO Qu Yu provided responses regarding this year’s production planning, sales expectations, gross margin improvements, and next year’s new product plans. We have edited them without altering the original intent:

Q: What is the production capacity status for the NIO ES8 and ONVO L90? What are the delivery targets for the remainder of the year?

A: The demand for the NIO ES8 and ONVO L90 is indeed stronger than initially expected, so we are working closely with our supply chain partners to comprehensively increase production capacity. The ONVO L90 will reach a production capacity of 15,000 units in October. The new NIO ES8 will reach a production capacity of 10,000 units in October and 15,000 units in December. Based on the current demand and supply situation, the goal is to achieve a delivery volume of 50,000 units per month on average across all three brands in the fourth quarter.

Q: How will the gross margin change in the second half of the year?

A: The auto gross margin in the second quarter was 10.3%, primarily due to being in a product transition phase. The 5566 model for the 2025 version was transitioned gradually by mid-to-late May. In terms of the total sales volume of 72,000 units for the second quarter, the 5566 accounted for only 20% of deliveries; therefore, the improvement in gross margin compared to the first quarter was not significant.

The gross margin target for the third quarter will further improve. The fourth quarter will see full quarter deliveries of both the L90 and the ES8, with the target for the vehicle gross margin in the fourth quarter to reach a break-even point between 16-17%, aspiring to achieve 20%.

In other business segments, a positive gross margin of 8.2% was achieved in the second quarter, benefiting from the profit improvement in after-sales and financial services brought by existing users, and a reduction in losses in energy. Notably, there was also a significant profit in basic external services in the second quarter.

Q: What is the production capacity plan for ONVO L90 and NIO ES8 in the coming period?

A: In terms of production capacity, priority will certainly be given to ensuring the delivery of ONVO L90 and the all-new ES8, even if L60 needs to give way to L90. As a result, L60 users are also waiting for their vehicles. It is expected that the capacity constraint for ONVO will ease starting in October, with the hope that the full supply chain capacity for both ONVO and NIO brands can increase to 25,000 vehicles per month in the fourth quarter.

The capacity for the Firefly brand is steadily increasing, with hopes of achieving a peak capacity of 6,000 units per month in the fourth quarter. Combined, the total capacity for all brands will be approximately 56,000 units.

Originally, the plan was to release L80 this year, but considering that production capacity mainly needs to satisfy current delivery models, there will be no new product deliveries this year. However, whether it will be released this year depends on market conditions.

Apart from ONVO L80, next year the NIO brand will launch two large SUVs, the ES9 and ES7. The main focus of this year’s NIO DAY will be the launch of the new ES8.

Q: What are NIO’s upcoming gross margin targets?

A: For NIO, the target is to achieve a 20% gross margin. The NIO brand aims to strive for 25% on that basis, ONVO aims to achieve higher margins while maintaining 15%, and the Firefly brand aims for around 10%. Compared to the previous generation of products, our current generation has significant cost competitiveness through technological advances in in-house research and cost control measures to achieve cost reduction.

Q: What new vehicle models will be available in 2026?

A: There are mainly three large vehicles: ONVO L80, NIO ES9, and ES7. The recently refreshed 5566 has no new model plans for next year. A few days ago, we announced the standard configuration of a 100 kWh battery, which will further enhance their competitive edge in range. We believe their competitiveness will remain strong for the foreseeable future. There may be minor variant updates, such as a Champion Commemorative Edition. The Firefly brand will not have a second car next year.Q: What level is expected for quarterly R&D expenses by 2026?

This year, we have undertaken significant efforts in R&D. From next year, we will maintain R&D spending of about 2-2.5 billion per quarter, as we believe this will ensure our long-term competitiveness.

The exact scale of investment is not yet fully anticipated. We hope to rely more on social resources for the construction of charging stations next year. As for the launch and development costs of new models next year, we aim to maintain them at similar levels to this year.

Q: What is the financial impact of the standard 100 kWh battery? How much will it increase costs?

A: In our previous policy announcement on the 5566, we mentioned that for the 2025 model, we had already offered considerable promotions to customers. The recent price adjustment effectively turns these promotions into standard pricing, so the final transaction price for customers remains largely unchanged. There is no significant impact on the gross margin and transaction price for the 5566. The long-term impact on sales requires observation, but currently, it shows a positive change in sales.

Q: How much cost can be saved by using fully self-developed chips?

A: There isn’t a significant relationship between delivery volume and the price per chip. The cost of similar processing power compared to second-generation chips has decreased considerably, and cost has also dropped substantially when compared to chips of similar performance sourced externally. However, the specific savings details are not disclosed.

Q: What potential impact does the current product lineup have on next year’s new products?

A: The L90 has a positive impact on the sales of the L60. Orders for the L60 reached a new high in August compared to any month this year, significantly surpassing the order numbers of July. With the recent standardization of the 100 kWh battery in the 5566 model, we believe this combination will clarify the entire pricing system.

Following the strong sales of L90 and ES8, there has been a withdrawal of many large pure electric SUVs from the market, indicating a significant influence on consumer perception. The competitiveness of large pure electric SUVs is becoming evident, heralding the advent of this segment’s era, thus having a very positive impact on NIO’s existing products concerning user perception.

Q: How do we view the stable sales of L90 and ES8 in the long term?

A: The competition in the Chinese market is indeed fierce. In terms of smart electric vehicle sales trends, the initial impact from new car launches is quite strong and then transitions into a stable sales period. It is challenging to envision a single vehicle consistently selling in large volumes, making it a considerably challenging target. From this year, we have been constructing a new marketing paradigm to extend the effect of new cars as much as possible, aiming to maintain a relatively high level of stable sales.

This article is a translation by AI of a Chinese report from 42HOW. If you have any questions about it, please email bd@42how.com.