Author | Wang Lingfang

Editor | Qiu Kaijun

“Considering the current situation, we expect the price of lithium carbonate to plummet rapidly, having already dropped to 250,000 RMB/ton. We estimate it will decline further, possibly even below 100,000 RMB.”

Wang Yu, chairman of Forteq Technologies (Ganzhou) Co., Ltd., said this in an interview on April 2nd at the “China Electric Vehicle 100 People Forum (2023)”.

Wang Yu believes that the rapid growth of market demand in the past led automakers to allocate substantial funds for subsidizing sales in order to achieve their performance targets. It is unlikely that automakers will allocate as much money for subsidies this year. The most significant possibility is that production might be reduced if prices don’t meet expectations. In addition, the mass production of sodium-ion batteries has already impacted the lithium carbonate and lithium hydroxide industries.

In Wang Yu’s opinion, the supply and demand of lithium carbonate and lithium hydroxide in 2022 are actually balanced, with many speculative factors involved.

Electric vehicles haven’t achieved “excellence” yet

In 2022, the production and sales volume of new energy vehicles reached 6.88 million units, bringing the total ownership to 13.1 million units, accounting for 4.1% of the market share.

Thus, electric vehicles have resolved the issue of shifting from “non-existent” to “existent.” Wang Yu suggests that the industry has now entered the next phase – achieving “excellence.” However, there are still several shortcomings in electric vehicles.

First, low range and slow charging. Currently, most vehicles have an energy consumption ranging between 10 kWh/100km and 20 kWh/100km. Compact sedans consume about 15 kWh/100km to 18 kWh/100km, while SUVs use roughly 16 kWh/100km to 20 kWh/100km. Based on this energy consumption, an average battery capacity of 60 kWh is needed for a 500 km driving range, which in reality would only cover about 350-400 km – even lower in winter.

Why not install more batteries? The issue lies in energy density – battery capacity and vehicle battery pack volumes are limited. Especially during the last two years, many models have switched from ternary batteries to lithium iron phosphate ones due to cost reduction efforts. Achieving a longer driving range with current technologies proves to be difficult.

Furthermore, charging time remains an issue for both ternary and lithium iron phosphate batteries.

Furthermore, charging time remains an issue for both ternary and lithium iron phosphate batteries.

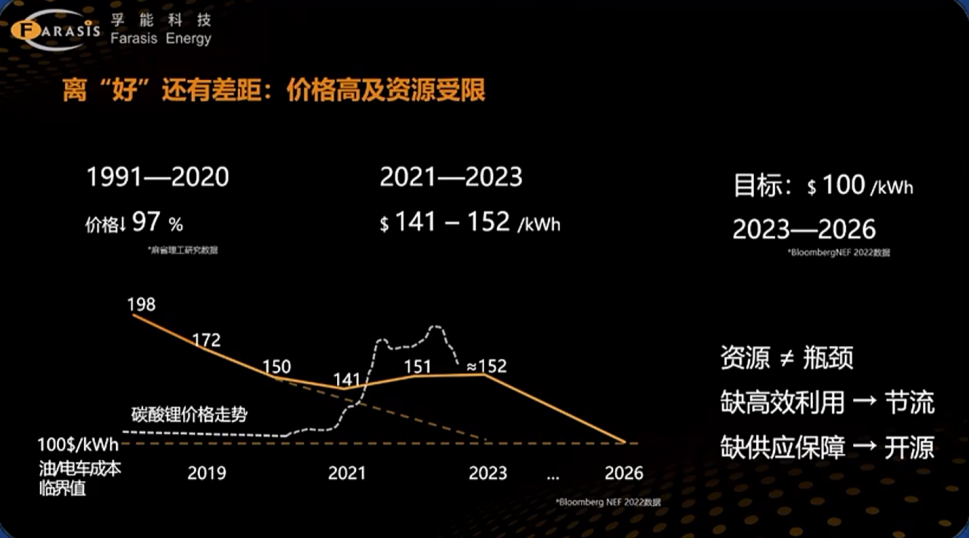

Secondly, price and resource constraints. Overall, lithium-ion battery prices have dropped by 97% from 1991 to 2020. However, starting in 2021, power battery prices began to rise, from $141/KWh to $152/KWh.

Previously, cobalt prices drove up battery costs. Cobalt prices increased tenfold in 2018, prompting the industry to develop “cobalt-free” batteries. Today, the cobalt content in lithium-ion batteries has been lowered to 5% or even less, and can even be entirely removed if needed. Subsequently, lithium carbonate prices surged.

In Wang Yu’s opinion, lithium carbonate prices are not determined by current predictions but are determined by market demand and supply, as well as vehicle manufacturers’ sensitivity to price.

Wang Yu believes that the supply and demand of lithium carbonate and lithium hydroxide in 2022 are actually balanced, with many speculative factors involved.

“Given this year’s situation, we expect lithium carbonate prices to decline rapidly, having already dropped to 250,000 yuan/ton. We estimate that it may further decrease, potentially reaching below 100,000 yuan.” Wang Yu states.

Wang Yu estimates that last year, the vehicle and battery industries contributed at least 100 billion yuan in profits to the lithium industry, which is unfavorable for the industry.

The significant drop in lithium carbonate prices, along with the recent decrease in traditional car prices, has significantly impacted the market and increased uncertainty.

Wang Yu notes that, to his knowledge, every vehicle manufacturer will still strive to achieve their operational performance targets this year with some postponing production time, but so far, he has not observed any impacts altering their operational plans. It is slightly better for ZEFI, as most of its products are exported.

In Wang Yu’s view, lithium carbonate resources are not scarce, and current production difficulties are not significant; it should quickly return to normal operation. “As the actual cost of lithium carbonate should be around 30,000 yuan, there is no reason for prices to surge to 500,000 or 600,000 yuan; such increases would be detrimental to global carbon reduction, environmental protection, and sustainable energy development.”In the interview, Wang Yu mentioned that sodium batteries are an excellent choice because sodium carbonate is only 2,000 yuan/ton, making sodium battery development more suitable for China’s current situation. Domestic lithium resources have not been fully explored yet, and are greatly affected by the restrictions of lithium and cobalt. Once these resource constraints are resolved, the development of China’s new energy vehicles will be more stable with fewer fluctuations, and the future direction will have better controllability and predictability.

From “Having” to “Good”: Four Aspects of Improvement

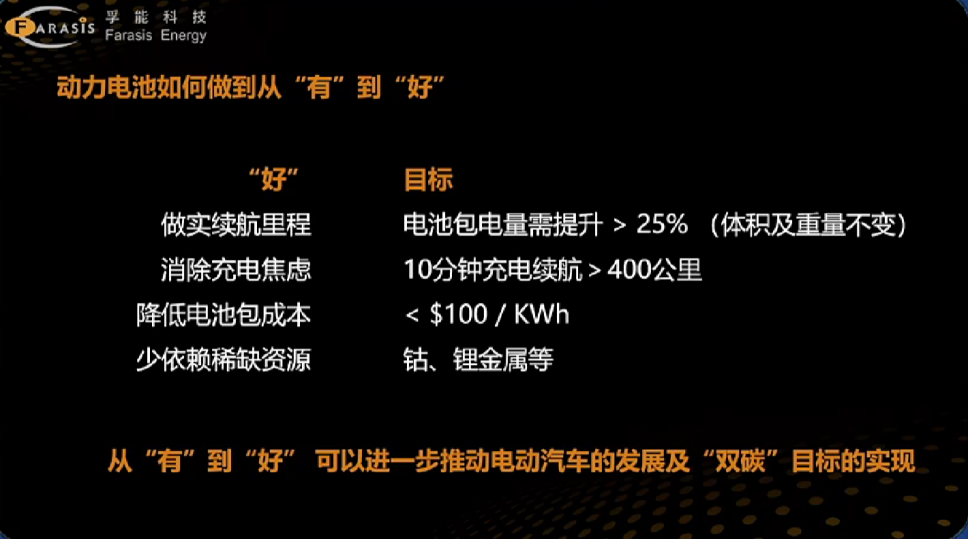

Wang Yu believes that to progress from “having” to “good”, four aspects need improvement.

First, increase driving range by enhancing battery pack capacity by 25%, providing an excellent user experience for customers.

Second, eliminate charging anxiety with a goal of charging 400 kilometers in 10 minutes, fulfilling requirements within the time it takes to enjoy a cup of coffee.

Third, maintain battery pack pricing at 100 USD/KWh.

Fourth, reduce reliance on cobalt and lithium resources, further advancing the development of electric vehicles and the realization of dual-carbon targets.

In Wang Yu’s view, achieving a solid driving range is related to material and product design. Regarding design, FONERGY Technology has made significant efforts, but this alone cannot resolve the core issue of driving range. Properly addressing this issue requires research and innovation in materials.

To eliminate charging anxiety, the key is to tackle ion conduction and electron conduction issues, lowering impedance. As for pricing, cost has now become the most pressing issue, which must be comprehensively resolved from the aspects of materials, design, manufacturing, and recycling. This is because costs depend not only on materials but also on battery design. In the past, integrating batteries into PACKs was an innovative design approach, in addition to manufacturing innovations; further research is needed to develop lithium- and cobalt-free batteries.

FONERGY Technology’s Solutions for Safety and Cost Issues

However, Wang Yu believes that future development trends call for high-energy-density batteries. Therefore, high-energy-density batteries and solid-state batteries remain essential technologies that must be continuously developed in this industry in the short to medium term.

Mentioning solid-state batteries, Wang Yu frankly stated that even though research progress in various aspects of solid-state batteries is currently satisfactory, commercialization is still a relatively distant goal. To further address safety issues of these batteries during this stage, various automakers, including FONERGY Technology, are developing semi-solid-state batteries, aimed mainly at reducing electrolyte quantities to improve safety.Translate the following Markdown Chinese text into English Markdown text in a professional manner, retaining the HTML tags in Markdown, and output only the results.

Even without organic electrolyte, a fully charged battery would not pose a safety hazard, mainly because the battery may cause combustion, vaporization of the electrolyte, and subsequent participation of positive electrode materials in extreme situations or under short-circuit conditions, resulting in explosive gas generation and safety risks. Removing the organic electrolyte and turning it into a solid-state electrolyte is the future direction of this industry.

However, transitioning from liquid to solid-state electrolyte does not solve the battery’s energy density and energy issues, which primarily depend on its positive and negative electrode materials. During development, Fernel Technology will gradually adjust its technical route according to the development situation to meet market customer demands as much as possible.

Fernel’s semi-solid-state battery started mass production in September 2022 and is primarily produced in a factory jointly owned by Fernel and Geely in Ganzhou. This is the first generation of our semi-solid-state battery.

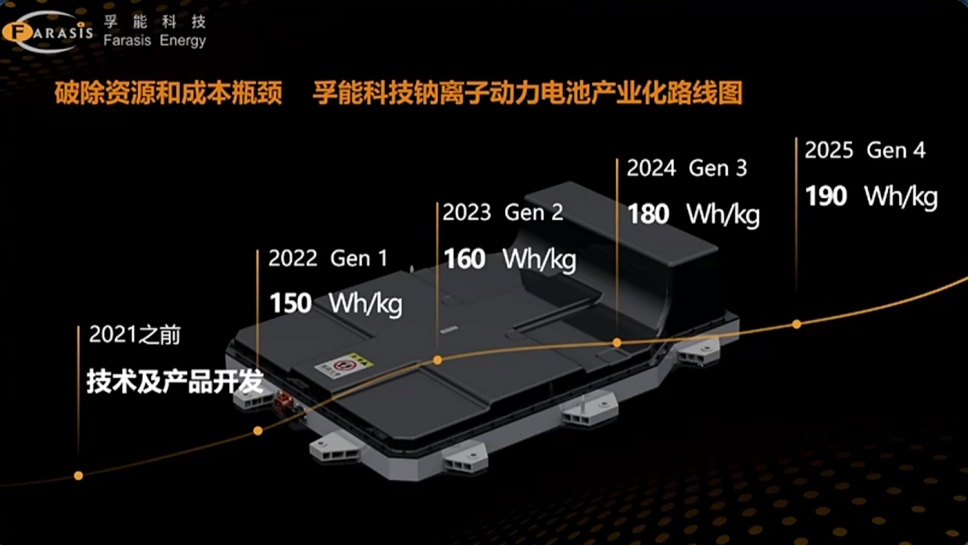

Last year, Fernel Technology actively presented alternative plans for the implementation of sodium-ion battery industrialization, aiming to address the constraints of lithium metal on the industry. This year, Fernel’s sodium-ion batteries have entered mass production, with the short-term plan being to replace vehicles with a range of up to 300 km with sodium-ion batteries, and eventually those with a range of up to 500 km in the medium term. Fernel’s future offering to automakers will consist of sodium-ion and ternary cell combinations.

At the system solution level, the SPS is based on large flexible pouch batteries directly integrated into vehicles. This system is not only compatible with ternary materials but also with lithium iron phosphate, and it accommodates both liquid and solid-state batteries, significantly improving power performance, energy density, and range. Adopting this technology has reduced the overall PACK cost by 33%. An 80 kWh battery can now cover a distance of approximately 600 to 700 kilometers.

Additionally, Wang Yu proposed four appeals. First, he called on the government to support increased resource surveys of lithium, nickel, and cobalt, and to develop and utilize these resources in a reasonable and orderly manner. The carbon neutrality goal requires worldwide concerted efforts for humanity and sustainable energy development, which is a global issue. The industry’s progress should not be hampered by the resource challenges or price issues of individual metals.

Second, Wang called on the government and academia to accelerate the construction of the sodium-ion battery industry chain and support the research and development of next-generation sodium-ion battery materials.Thirdly, it is recommended that battery companies serve as the main body for recycling and reusing retired power batteries, as the cost of ternary batteries will be even more affordable than that of lithium iron phosphate batteries. This can give birth to various business models, with longer driving ranges and better life spans for the ternary batteries.

Lastly, a fixed-term retirement system should be applied to electric vehicles, for example, stipulating that all electric vehicles must exit the market after 10 or 15 years. This can help prevent future risks caused by uncontrolled power batteries, such as fires or other hazards.

This article is a translation by ChatGPT of a Chinese report from 42HOW. If you have any questions about it, please email bd@42how.com.