Author | PJI

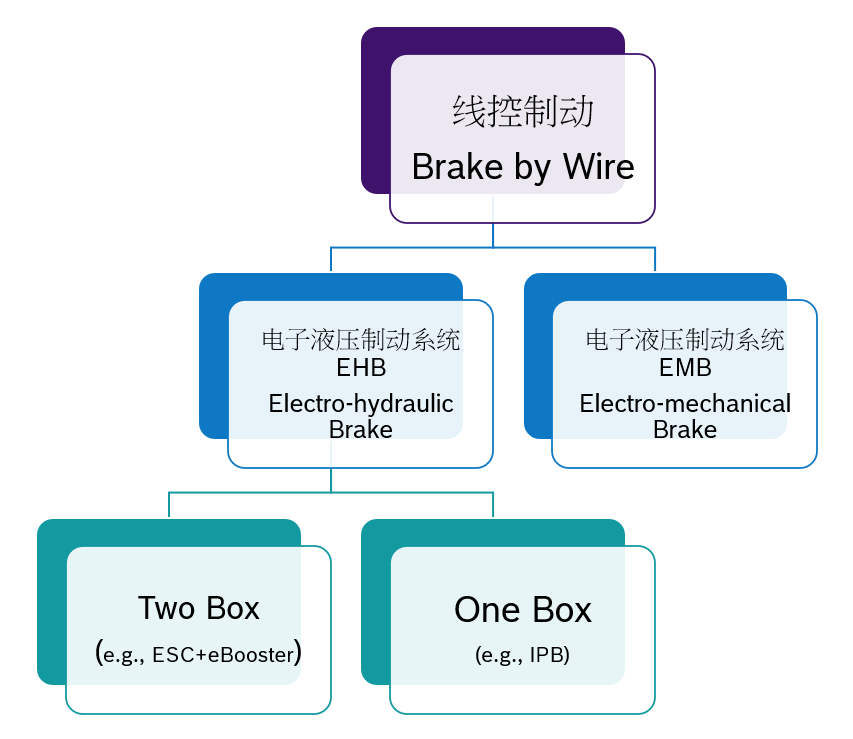

Based on different brake actuators, the electronic control brake system can be divided into Electro-Hydraulic Brake (EHB) and Electro-Mechanical Brake (EMB). Among them, EMB is the future development direction, but there are still many challenges and has not yet been put into mass production. EHB is based on the traditional hydraulic brake system, using electronic devices to replace some mechanical components, and is currently the mainstream electronic control brake technology. Furthermore, according to the degree of integration, EHB can be divided into Two-box and One-box electronic control brake systems.

The previous articles have discussed Two-box and One-box systems in depth. In this article, we will summarize the market performance and mainstream suppliers of these two systems, offering a brief overview of the market development trend of electronic control brakes.

Development prospects of electronic control brakes: extensive growth space in line with the trend of electrification and intelligentization

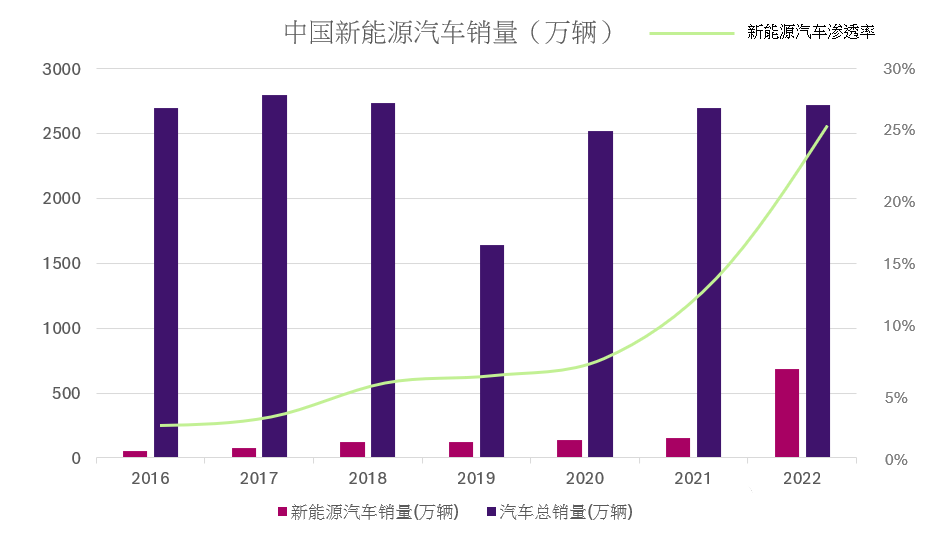

On the one hand, electronic control brake products solve the pain point that new energy vehicles lack a vacuum source, and recover braking energy through the motor to improve driving range. Therefore, the penetration rate of electronic control brakes in new energy vehicle models is higher than that in traditional fuel vehicles, and the electronic control brake industry will benefit from the growth of new energy vehicle sales and penetration rate for a long time. Currently, the global new energy vehicle market is becoming larger and larger, and the domestic new energy vehicle penetration rate continues to increase. There is extensive growth space in the future. New energy vehicle sales have risen from 507,000 in 2016 to 6.887 million in 2022. The penetration rate of new energy vehicles has risen from 1.81% in 2016 to 25.60% in 2022, an astonishing increase.

On the other hand, since the electronic control brake system does not rely on mechanical connection between the brake pedal and the power assist unit, it can achieve decoupling between the chassis and the body and better adapt to the technical solutions for autonomous driving above L3. As the core module for “perception-decision-execution” in the above-mentioned process, the market size of electronic control brake system will have greater development opportunities with the continuous improvement of the penetration rate of L3 and higher level autonomous driving.

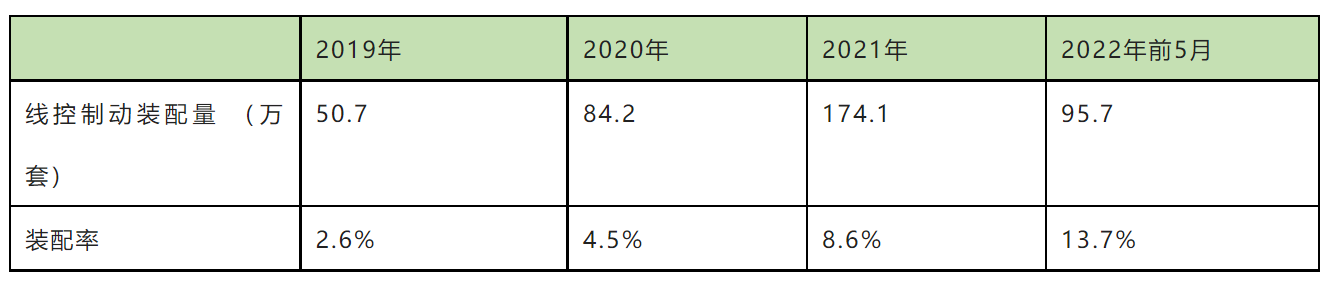

Currently, the electronic control brake system is still in the early stage of development, and the overall penetration rate is relatively low, but it is showing an upward trend overall. According to the statistics of Zosi Data Center, the installed rate of the electronic control brake system in domestic passenger vehicles was 2.6% in 2019, and it has increased to 8.6% in 2021. Due to the rapid growth in domestic sales of electric vehicles, by May 2022, the installed rate of the electronic control brake system had climbed to 13.7%. With the development of the trend towards electric and intelligent vehicles, electronic control brake system has gradually gained widespread recognition and will accelerate its penetration into the market.

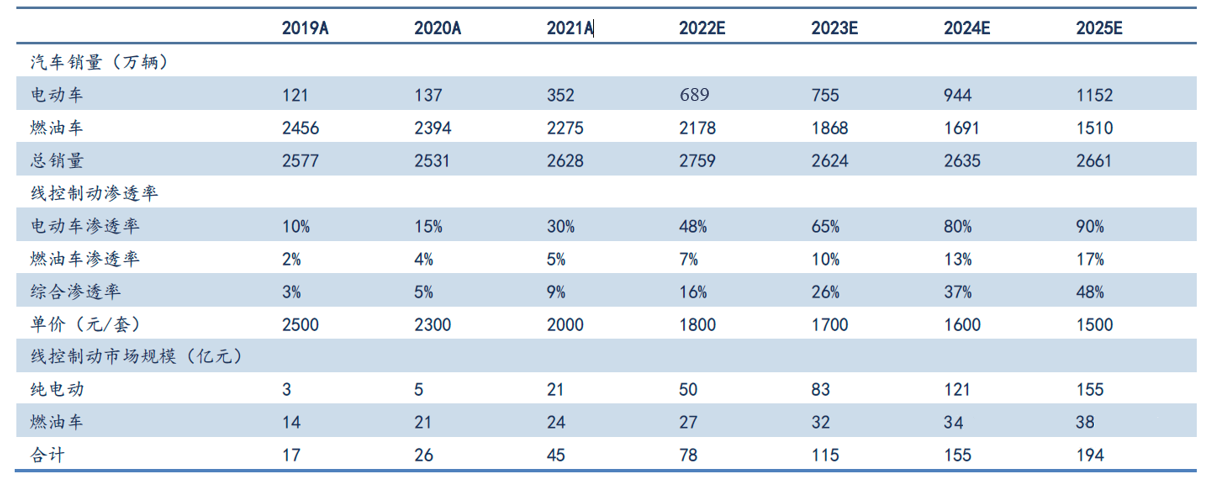

Based on the following assumptions, Cinda Securities has made a prediction for the domestic market of electronic control brake system that it is expected to reach nearly CNY 20 billion by 2025.

-

It is estimated that the sales of electric vehicles will reach 11.52 million units in 2025, with a compound annual growth rate of 34%. The sales of fuel vehicles will decline as the penetration rate of new energy vehicles increases, falling to 15.1 million units in 2025.

-

The penetration rates of the electronic control brake system products for electric and fuel vehicles were 30% and 5%, respectively, in 2021, and are expected to reach 90% and 17% by 2025. The comprehensive penetration rate will increase from 8.6% in 2021 to 48% in 2025.### Prediction of the Market Size of China’s Electronic Line Braking Systems from 2019 to 2025

It is estimated that the single-set price of electronic line braking systems will be 2000 yuan in 2021 and gradually decrease with the cost reduction to 1500 yuan in 2025. The data comes from China Securities.

The Market Structure of Electronic Line Braking Systems: EMB is a Trend, but EHB is currently Dominant

The development of vehicle braking has gone through four stages: pure mechanical braking, hydraulic braking, electronic control braking, and electronic line braking. Compared with the traditional hydraulic braking system, electronic line braking systems are free from reliance on vacuum boosters and have the advantages of short response time, small size, lightweight, and strong scalability. According to the different braking actuators, electronic line braking systems have two technical routes:

- Electro-Hydraulic Brake (EHB)

- Electro-Mechanical Brake (EMB)

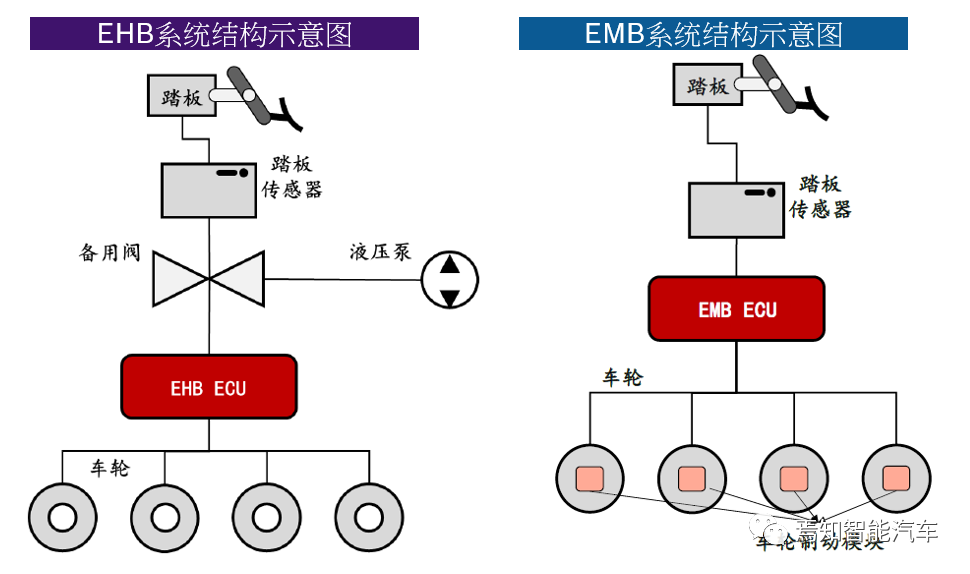

EMB replaces the hydraulic master cylinder system with four electric-motor-driven wheel-end calipers, realizing “fully electronic control”. Due to the significant differences in braking actuators, the industry refers to EHB as “wet” electronic line control braking and EMB as “dry” electronic line control braking.

While retaining the advantages of the EHB system, the EMB system further releases the freedom of layout of braking system components. At the same time, four electric motors and calipers replace the relatively complex hydraulic system, simplifying the process and cost of vehicle assembly and later maintenance. Meanwhile, the EMB system achieves complete electronic control, which can be better integrated with other electronic control systems in the automotive industry and is more in line with the trend of electrification and intelligence of the automotive industry.However, although EMB technology has many advantages compared to EHB hydraulic line control technology, the high degree of line control also places higher requirements on the reliability of EMB, and there are still many technical difficulties that need to be overcome, such as:

- For purely data signal transmission, how to achieve redundant backup to meet regulatory requirements in the event of vehicle network failures.

- The motor/control unit is on the wheel side, producing high temperatures during braking, requiring high temperature resistance and heat dissipation for key parts.

- The wheel-side brake motor requires a large amount of power, therefore requiring 48V or higher voltage for driving.

- Large and medium-sized passenger cars have higher requirements for braking ability, which puts higher demands on motor volume and installation feasibility.

- Requires support from control chips and a large number of sensors, and cost-effectiveness needs to be effectively reduced for popularization.

Until these difficulties are overcome, EMB will not be put into mass production. Currently, various corporations are still in the research and development stage. Therefore, standing at the point of time in 2023, the author draws the following conclusions:

EMB is the future direction of driving line control, but EHB will remain the mainstream line control scheme for the next 5-10 years.

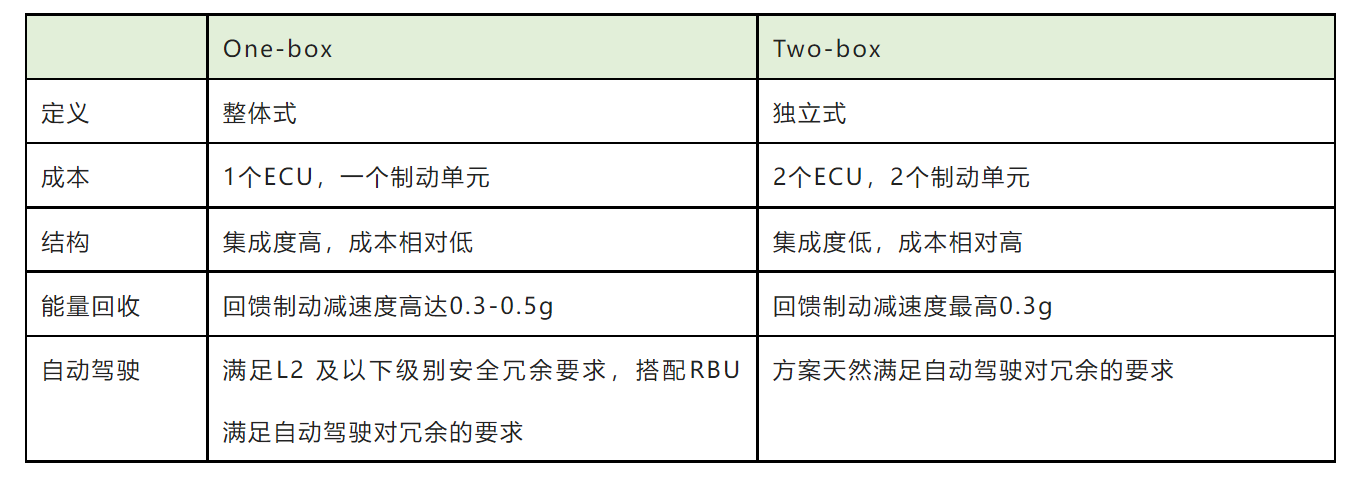

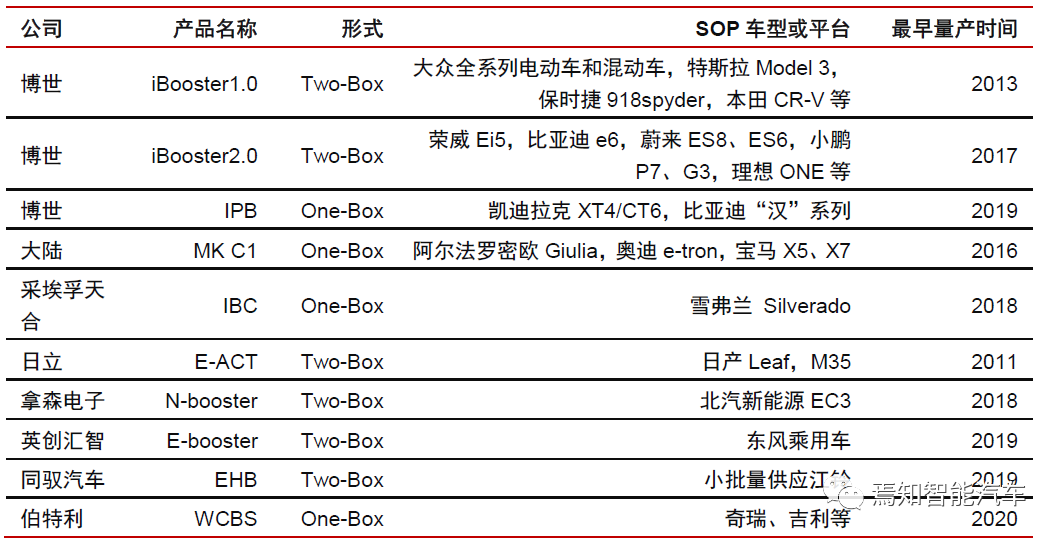

The EHB system is divided into One-box and Two-box based on whether it is integrated with the stability control function ABS/VDC. The currently popular Two-box scheme is the “eBooster+ESC” combination, where eBooster and ESC respectively achieve basic braking functions and stability functions. The ESC and eBooster share a hydraulic system on the vehicle, which coordinates their work to support the driver or intelligent driving system’s braking requests accurately and efficiently compared to traditional vacuum power-assisted systems. In the One-box scheme, the driver pedal force does not act on the master cylinder, and the pedal feel is achieved through the simulator, while the braking force is achieved by a servomotor, providing greater flexibility in adjusting the pedal feel. Moreover, during the process of intelligent driving system control, One-box provides braking force without causing the braking pedal to move, achieving true decoupling.

Comparison between One-box and Two-box:

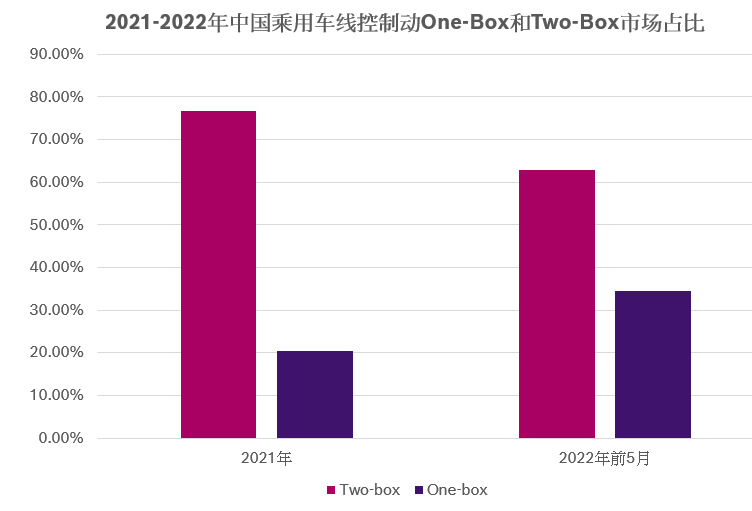

According to the current market performance, the mainstream of wire-controlled braking market application is the Two-box technology solution. However, due to the slow progress of the landing of automatic driving and limited installation of automatic driving systems in vehicles, the advantages of Two-box are not obvious, and One-box is expected to become the mainstream technology of EHB in the next stage. According to research and statistics from Zosi Automotive, the market share of One-Box and Two-Box solutions in 2021 were 20.5% and 76.6%, respectively. According to data from the first five months of 2022, their market share was 34.6% and 62.8%, respectively, indicating a continuous increase in the penetration rate of One-Box solution, and this trend is expected to continue over the next several years.

According to the current market performance, the mainstream of wire-controlled braking market application is the Two-box technology solution. However, due to the slow progress of the landing of automatic driving and limited installation of automatic driving systems in vehicles, the advantages of Two-box are not obvious, and One-box is expected to become the mainstream technology of EHB in the next stage. According to research and statistics from Zosi Automotive, the market share of One-Box and Two-Box solutions in 2021 were 20.5% and 76.6%, respectively. According to data from the first five months of 2022, their market share was 34.6% and 62.8%, respectively, indicating a continuous increase in the penetration rate of One-Box solution, and this trend is expected to continue over the next several years.

Trend of wire-controlled braking players: foreign enterprises dominate, domestic brands have a chance to break through

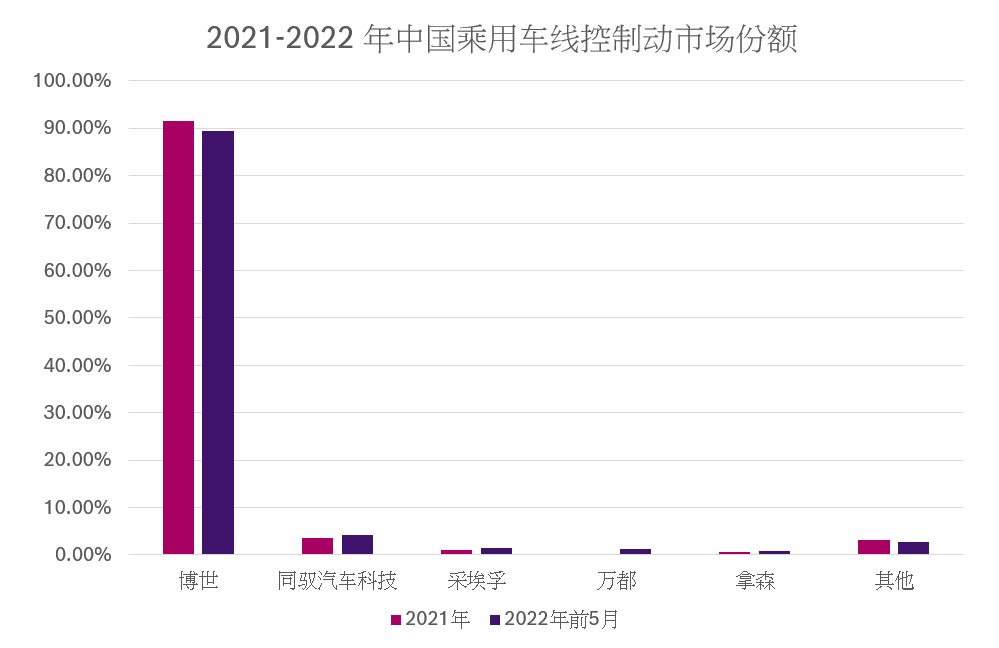

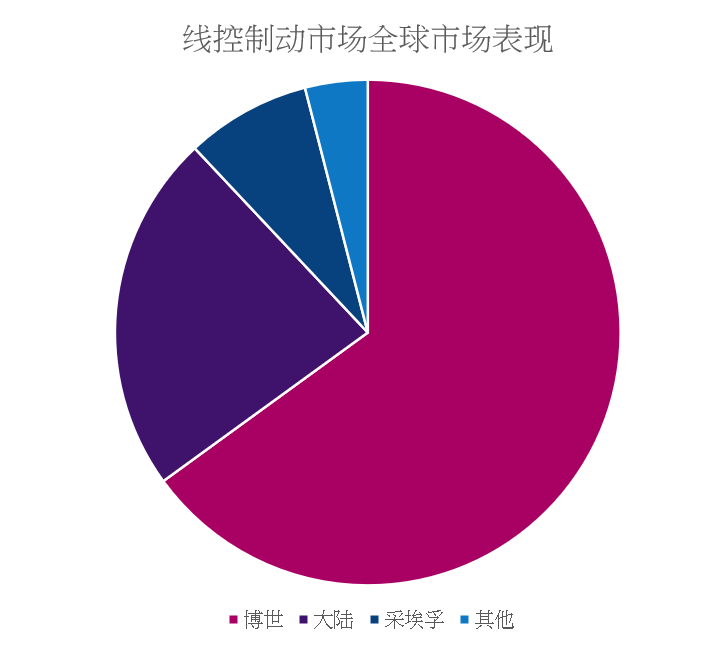

Wire-controlled braking is still in the early stage of development, and overseas head Tier 1 giants such as Bosch, Continental, and ZF, rely on their technical accumulation and first-mover advantages in the traditional braking field, they occupy the vast majority of the global market share. Currently, Bosch, Continental and ZF have realized the mass production of EHB solutions. Among them, Bosch’s performance is the most prominent.

Bosch takes the lead in self-developing the layout of wire-controlled braking, occupies a leading market position, and its main products are the iBooster+ESP of the Two-box technology route and the IPB of the One-Box technology route. Among them, iBooster+ESP products were launched earliest and are currently the most widely used. They have been widely matched with models such as Porsche, SAIC Volkswagen’s new energy products, Tesla’s entire series, Ideal ONE, Lynk & Co 01/03, Xpeng P7/G3 etc. IPB products started to enter the Chinese market since 2021, and have now received a large number of orders starting with its matching with BYD Han.

According to statistics, in 2022, more than half of the global Wire-controlled braking system market share is occupied by Bosch. In the domestic market, relying on reliable quality and good reputation, Bosch’s wire-controlled braking system occupies a monopoly position.“`

Other giants, such as the MK C1 line control braking product of Continental’s One-box scheme, are mainly for the European market at present. Starting from the end of 2020, their market share has gradually increased as they start to target the Chinese market. ZF acquired the vehicle and commercial vehicle line control braking technology through the acquisitions of TRW Automotive and WABCO. Their line control braking product IBC for passenger cars began mass production at the end of 2018, initially targeting the European and American markets. From 2022 onwards, ZF’s efforts in the Chinese market are becoming more apparent and should not be underestimated.

On the other hand, we can also see that domestic brands are gaining strength. Companies like Bethel, Foryou Technology (BYD), Unity Automotive, INVOIC Intelligent, and Nason Electronics are gradually achieving mass production of line control braking products.

Under the current special circumstances, the market share of domestic line control braking suppliers is also gradually increasing. The driving factors for the increase in market share of domestic suppliers can be summarized as follows:

-

The “chip shortage” caused by the epidemic has prompted domestic automakers to choose domestic suppliers with stronger supply capabilities.

-

As the market share of domestic automakers gradually increases, they are choosing more domestic suppliers from the perspective of supply chain autonomy, driving the market share of domestic suppliers up.

“““markdown -

Chinese suppliers have the advantage of joint development and faster response speed.

As a chassis engineer, I am deeply impressed by the achievements made by domestic brands in the field of online controlled dynamic market. I sincerely express my blessings to the engineers and entrepreneurs who silently contribute to this success. Brake is closely related to safety. I hope domestic brands can seize the rare market opportunities, continue to launch safe and reliable online controlled brake products, and achieve a breakthrough against foreign enterprises as soon as possible.

“`

This article is a translation by ChatGPT of a Chinese report from 42HOW. If you have any questions about it, please email bd@42how.com.