Author: Wang Yi

On March 10th, China Automotive Power Battery Industry Innovation Alliance released the monthly data of domestic power batteries in February 2023.

The data shows that in February, the total output of power batteries in China was 41.5GWh, a year-on-year increase of 30.5% and a month-on-month increase of 47.1%. From January to February, the cumulative output of power batteries in China reached 69.6GWh, a cumulative year-on-year increase of 13.3%.

In terms of installed capacity, the total installed capacity of power batteries in China in February was 21.9GWh, a year-on-year increase of 60.4% and a month-on-month increase of 36.0%. From January to February, the cumulative installed capacity of power batteries in China reached 38.1GWh, a cumulative year-on-year increase of 27.5%.

Overall data shows that the increase in sales of new energy vehicles in February has driven the recovery of power battery installed capacity.

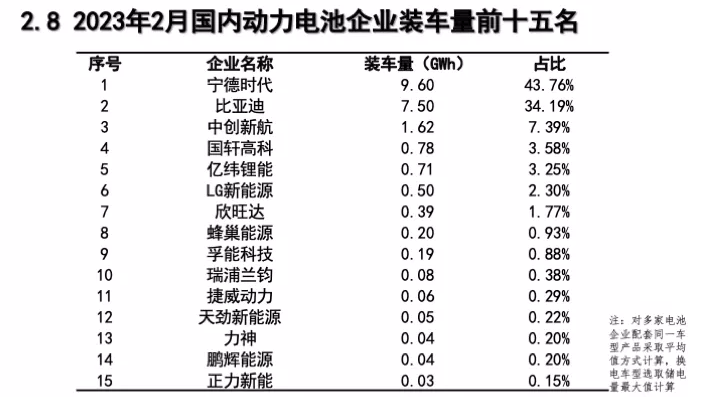

In February, a total of 39 power battery companies in China achieved vehicle matching, ranking the top 3, top 5, and top 10 power battery companies’ installed capacity were 18.7GWh, 20.2GWh, and 21.6GWh respectively, accounting for 85.3%, 92.2%, and 98.4% of the total installed capacity.

In February, the top 15 power battery companies in China in terms of installed capacity were, in descending order: CATL, BYD, ATL, Gotion, EVE Energy, LG Energy Solution, XWDT, SVOLT, Funeng Tech, Lishen, JWELL, TIANJIN LISHEN, Lishen Battery, Penghui Energy, CALB.

The top two companies, CATL and BYD, had a total installed capacity of 17.1GWh, accounting for 77.95% of the power battery market share.

However, although CATL, as the leading enterprise, still ranks first, its market share is continuously declining.

CATL’s Response

Among all power battery companies, CATL had an installed capacity of 9.6GWh, ranking first. However, its market share decreased by 4.26 percentage points year-on-year and 0.7 percentage points month-on-month.In February, the market share of CATL’s installed power batteries was 43.76%. This is the fourth consecutive month of decline since November last year.

Earlier, CATL released its 2022 financial report. In 2022, its total operating revenue was CNY 328.594 billion, a year-on-year increase of 152.1%; its net profit was CNY 30.729 billion, a year-on-year increase of 92.9%. In 2022, CATL’s global market share for power batteries reached 37%, ranking first in the world for six consecutive years.

In recent years, rising prices of some core materials for power batteries, such as lithium carbonate, have had a significant impact on the entire new energy industry. The increase in raw material prices has squeezed CATL’s profit margins. In the first quarter of last year, CATL’s gross profit margin was as low as 14.5%, but by the fourth quarter, the figure had climbed back up to 22.6%.

To cope with the rising price of lithium, CATL has shifted the pressure of the price increase to downstream automakers. In the fourth quarter of last year, the average price of CATL’s power batteries rose to CNY 1.21/Wh, a 32% increase from the first quarter’s price of CNY 0.92/Wh. As a result, downstream automakers that were squeezed have gradually begun to find ways to get out of the predicament, and some power battery companies have also started to embark on the road of independent R&D and production.

However, although CATL has obtained high profits by transferring the pressure of rising raw material prices, it has indirectly led to a decline in its market share. CATL is clearly aware of this. The recently launched “Lithium Mine Rebate” plan by CATL is an attempt to seize market share. The plan requires automakers who sign this cooperation to commit to purchasing no less than 80% of their batteries from CATL, and the price of some lithium carbonate for power batteries will be settled at CNY 20,000 per ton within the next three years.

Another reason for the “Lithium Mine Rebate” plan is that in February, BYD’s installed power battery capacity reached 7.5 GWh, accounting for 34.19% of the market share, while its market share in the same period last year was only 21.24%. Now, the gap between BYD’s market share and the first-place CATL has narrowed to within 10 percentage points. In terms of installing phosphate iron batteries, BYD has surpassed CATL with a market share of nearly 50%.In fact, since last year, BYD has gradually posed a threat to CATL’s market share. Although CATL occupies about half of the market share, this number has been declining in recent years. At the same time, the gap between BYD and CATL is becoming smaller.

Data shows that the cumulative installed capacity of domestic lithium iron phosphate batteries in January and February was 25.9 GWh, accounting for 68% of the total installed capacity, with a cumulative year-on-year growth of 55.4%. BYD’s installed capacity reached 13 GWh, with a market share of over 50%, which is about 16 percentage points higher than the second-placed CATL. In terms of lithium iron phosphate battery alone, BYD’s status can be reflected by data.

Different from CATL, which is a leader in the entire new energy battery industry, BYD’s production of batteries has always been mainly for self-supply. In the field of power batteries, the two are not “dead enemies” targeting each other. BYD, which is self-reliant, cannot compete with CATL, which is called the “king of CATL” in the industry.

However, the sales performance of BYD’s new energy vehicles is too eye-catching. In 2022, BYD’s total sales reached 1.86 million vehicles, accounting for 27% of the entire new energy vehicle market. This directly took away the cake from other new energy vehicle companies.

Many customers were hit, directly affecting the installation of CATL power batteries.

It is reported that BYD will continue to increase its sales target to 3.5-4 million vehicles this year. This target is undoubtedly a naked “threat” to other car companies.

For CATL, the alarm has already sounded, and necessary measures must be taken. “Lithium mine rebates” give its customers more attractive benefits, which can not only help CATL stabilize its market share in power batteries, but also enhance its ability to cope with the crisis of profit being squeezed in a way that benefits customers.

CATL previously emphasized that lithium mine sharing is not for the purpose of reducing prices, but because the company has some mineral resources and hopes to share them with long-term strategic customers without seeking excessive profits.

Although there are not many car companies that have signed this agreement with CATL, it is undeniable that the “lithium mine rebate” plan can provide a backup for CATL’s installed capacity in the next few years.Ningde Times’ idea is great, but the continuously declining prices of lithium carbonate add more uncertainty to the “lithium mine rebate” plan.

Relying solely on the “lithium mine rebate” plan may be able to help Ningde Times continue to expand its market share while stabilizing its market share, but such driving force is clearly insufficient for the company’s long-term and sustained development.

The market is always changing rapidly. It is still unknown what kind of pattern China’s power battery market will present in the future. Whether it is dominated by “Ning Wang”, followed closely by BYD, or emerges as a dark horse, all require time to precipitate and market testing.

This article is a translation by ChatGPT of a Chinese report from 42HOW. If you have any questions about it, please email bd@42how.com.