Author | Zhu Shiyun

Editor | Qiu Kaijun

“Achieving global success is not just a superficial display or a battle of attrition, but rather a process of deep-rooted cultivation and exploration. It is the historical mission of Chinese auto companies to make Chinese brands deeply rooted in the hearts of people in other countries and cultures,” said a frontline executive in charge of Chinese auto companies’ global expansion.

Compared with China’s booming new energy vehicle market, Europe is like a “paradise”: high subsidies for new energy vehicles, “old players” with weak motivation for electric and intelligent vehicles, China’s significant cost advantage, and the possibility of a ban on internal combustion engines in Europe by 2035.

In November 2020, PwC estimated that Chinese electric vehicles could capture 5% of the European electric vehicle market by 2030. If based on the total European sales in 2022, it would be a market of 565,000 vehicles; if an actual ban on internal combustion engines is implemented, it would be a market on the scale of tens of millions, which is very attractive.

But can Chinese new energy vehicle companies going to Europe without competitors and with a ban on internal combustion engines simply win easily? Recently, Zhang Lin (pseudonym), a frontline fighter in the European market, told us about the realities and trends, and specifically mentioned four misconceptions that Chinese auto companies should avoid.

Not a cheap market

“China is the global haven for electric vehicles’ prices, even considering tariffs and freight costs, the price difference is still significant,” Zhang Lin said when talking about pricing. “So we are also not willing to set the price too low. There is no need to do so.”

For example, BYD Yuan Plus with a 60 kWh battery in China is priced between RMB 149,800 and 167,800, while in Germany it costs between 42,000 and 47,000 euros, equivalent to RMB 309,000 to 344,000. After a 10% import tariff and about RMB 40,000 per vehicle for freight costs are deducted, the price is RMB 244,500 to 276,300, which is about 64% more expensive than in China.

In late September 2022, BYD announced that it would be the first Chinese automaker to launch three models, Han, Tang, and Yuan Plus, in the European market. According to Clean Technica data, 1,905 Yuan Plus were sold in six European countries, including Germany and the UK, in 2022.“`

“In the past three years, as Zhang Lin said, China has been blessed by favorable timing, geography, and people in its push towards Europe.

Favorable timing means that when there is a chip shortage, European, American, and Japanese car companies tilt chip resources towards combustion engine cars based on profit considerations. Chinese car companies prioritize supplying products for overseas markets, which enables them to sell cars and helps Chinese businesses gain a foothold.

Geography refers to European subsidies policies, such as Germany’s maximum subsidy of 9,000 euros for cars priced below 40,000 euros, which was reduced to 4,500 euros this year.

People refer to the hard work of Chinese car companies’ deployed employees.

“The past three years have been the time window for European consumers to get to know and accept Chinese cars. Meanwhile, the pandemic has led to other brands adjusting their policies in Europe, providing opportunities for Chinese brands to establish a dealership network in Europe, as Zhang Lin said. But Europe may be about to “roll up” soon.

First, as more and more Chinese brands enter the European market, price wars are intensifying.

“China has a strong cost advantage. It will take some time for European consumers to accept new Chinese brands. New players often seek quick victory, and price wars are the fastest way.“

Secondly, the ban on combustion engines will accelerate the transformation of existing players and exacerbate market competition.

Thirdly, China’s current development model of using profit to exchange scale for new energy is not suitable for European regulation.

“European regulations focus on companies that have not made a profit for three consecutive years. Once a large-scale company is still losing money, it will be considered tax evasion. When punishing, the parent company will be implicated.”

Finally, the ban on combustion engines may be followed by more stringent carbon footprint requirements which use taxation and fees to eliminate China’s cost advantage and create an even playing field for Chinese and foreign car companies.

Direct Sales? Not practical

There are many barriers for Chinese car companies to enter Europe.

“Customers have said to dealers, ‘My father bought a car from your father and it has been working well, so I’m buying a car from you.’ This was the first ‘cultural shock’ Zhang Lin experienced in Europe, where customers’ trust in dealers is more important than car manufacturers. There are often ‘family-run’ dealers that have been in business for three generations or more.”

! MG Europe dealership, note how similar the two dealers look“

{kind=link}

**In practical operations, the European dealership model is challenging the "more advanced" direct sales model in China.**

Currently, Chinese new energy vehicle companies mainly use three types of dealership models to enter the European market.

The general agency model is the lightest, with high commissions but no need to bear operating costs, which can quickly achieve sales; the dealership model is relatively heavy, but it is conducive to opening up the market in unfamiliar territories while also taking into account brand building; the direct sales model has the highest cost and the brand goes directly to consumers.

Currently in Europe, BYD uses the general agency model, while mainstream brands such as SAIC, Great Wall, Geely, and Chery mainly adopt the dealership model. Tesla and Chinese new car makers are direct sales.

"We also consider adding new sales models for disruptive products." Zhang Lin said, "But in Europe, only Tesla's direct sales model has succeeded after a continuous ten-year investment. Whether Chinese companies can adopt the direct sales model in Europe depends on whether they have the same commitment and resource platform to support it."

**Unlike Chinese dealerships that mainly depend on manufacturers, European dealerships have strong constraints on both customers and OEMs.**

On the one hand, dealerships have transparent pricing and good service, with strong customer loyalty in the local market. Moreover, 70% of first-time car buyers in Europe are over 40 years old and more accepting of the dealership model.

On the other hand, dealership alliances are powerful. Volkswagen's new energy agency system in Europe is currently only implemented in Germany and has not yet been extended to other countries. "If Volkswagen can't make it in Germany, it's easy to imagine the resistance Chinese companies will face."## Pure Electric Intelligent SUV? Can't Sell

Another product strategy that is not suitable for the European market is China's.

"China's intelligent configuration exceeds expectations for European users and there is redundancy." Zhang Lin believes that, due to regulatory and user habits constraints, if the domestic intelligent interconnection is copied, it will become a burden on the road forward, not just a selling point.

The European General Data Protection Regulation (GDPR) is the strictest in the world **and has strict regulations from the user authorization of the vehicle end to the cloud operator data transmission for personal information required for functions such as fatigue monitoring, intelligent voice assistants, and in-car navigation**, and many popular functions in China cannot meet GDPR requirements.

**On the other hand, the age of first-time car buyers in Europe is mostly over 40, and they do not have a strong preference for intelligence.** Although monthly consumption habits are common in Europe, they are directly related to income, and young consumers are more inclined to buy used cars. "Therefore, knowing who the customer is is a prerequisite." Zhang Lin said.

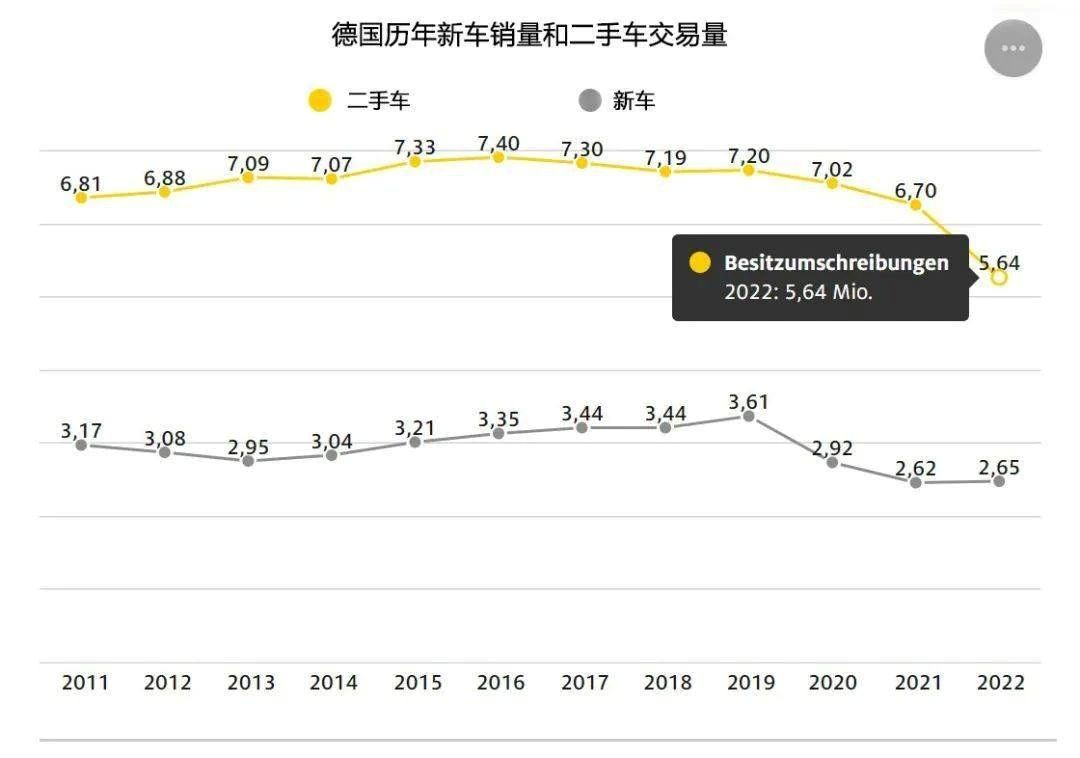

**In addition, the mature second-hand car market in Europe is also one of the reasons why young people do not buy new cars.** For example, the number of new car transactions in Germany has been maintained at around 3 million vehicles annually, and the scale of second-hand car transactions is more than twice that of new cars.

**What China cars are good at, "large", is not suitable for Europe.**

At the end of 2022, SAIC launched a pure electric product MG4 (named MG Mulan in China) designed for Europe with a simple interior without a sunroof. A0-class cars are "against the market" in China. "But in Europe, the roads are narrow, and users like 'small steel cannons' like Golf, and they have no interest in large screens or leather seats, and do not pursue sunroofs excessively." Zhang Lin analyzed.

```

From the results, it can be seen that the delivery of more than 7,000 MG4s in Europe has been completed in 2022. According to official SAIC data, nearly 5,000 MG4s were delivered in Europe in January 2023, and the "oversea monthly sales of a single model breaking through ten thousand" is about to be achieved.

"Using Chinese models to go abroad, hoping to do incremental business essentially is short-termism. Europeans tend to be more rational when using cars, and Volkswagen has always emphasized 'doing well in China for China' and emphasized localization. In other words, the long-term strategy of Chinese automobile companies going abroad also needs to tailor the development of products to the needs of the European market. In this regard, SAIC is the most solid and forward-looking," said Zhang Lin.

## Relying on Complete Vehicle Export? Local Manufacturing is Better.

"Now the change in overseas and European sales volume proves our manufacturing capabilities. In the future, local manufacturing is a must-have path for Chinese car companies to transform into global companies," said Zhang Lin.

Currently, Chinese car companies use complete vehicle exports to trade with Europe, and in order to ensure transportation capacity and reduce costs, many major car companies even build their own fleets. Currently, SAIC's Anji-owned fleet has more than 30 automobile transport ships, and many other ships are being built and bidding; BYD ordered eight automobile transport ships last year, and at the beginning of this year, it ordered two more.

Institutions predict that BYD will achieve sales of 200,000 vehicles overseas this year, and SAIC will strive for a target of 1.2 million vehicles in overseas sales.

Therefore, complete vehicle exports are clearly not a "long-term plan." Zhang Lin said that many Chinese car companies have already planned and prepared to build production bases overseas. "The cost of transportation and supply chain of complete vehicle exports is too high, and building factories can better reflect the determination of long-term development in local areas."

Can building factories in Europe be possible? Zhang Lin believes that in Europe, where the automobile industry has matured, subcontracting, assembling of scattered parts, and acquiring local production capacity are all optional solutions for Chinese automobile companies to localize manufacturing in Europe.

The transition from an export-oriented model to a manufacturing-oriented model is not only the localization of production places and products, but also means the localization of organization and culture.

“Establishing factories in Europe presents huge challenges for Chinese enterprises in terms of cultural communication, employment systems, and union organizations. It not only requires hard work to learn, but also involves paying the tuition to do so,” Zhang Lin said. “This is an inevitable issue that will be encountered as Chinese enterprises move towards manufacturing in Europe. However, if other enterprises can survive, Chinese enterprises can certainly do so as well.”

Currently, many Chinese battery companies have taken the first step in building factories in Europe, while Tesla is further expanding its manufacturing capacity in the European and Latin American markets. Behind the lively overseas sales lies the longer-term overseas development path for Chinese automobile enterprises, which is slowly unfolding.

This article is a translation by ChatGPT of a Chinese report from 42HOW. If you have any questions about it, please email bd@42how.com.