Author | Wang Lingfang

Editor | Qiu Kaijun

Ningde Times’ “lithium mine rebate” plan has stirred up the auto and battery industries.

It is reported that Ningde Times has launched the “lithium mine rebate” plan for mainframe factories with a demand of over 10 GWh. The price of carbonate lithium for a part of power battery is settled at 200,000 yuan/ton, and the remaining part is calculated based on the market price difference. The condition is to pay a 10% advance payment and be bound for more than three years. The supply volume in the 4th-5th year shall not be lower than the previous year. The terms are divided into three categories, with the rebate ratio decreasing in sequence according to the commitment of exclusive supply, 80% and less than 80%.

So, should the second-line battery companies follow suit? If they have their own lithium mines, there is no problem. However, if they do not control the upstream lithium mines, the second-line battery companies will face a double blow in terms of customers and profit margins, and may even be at risk of survival.

A new round of shuffling in the battery industry has arrived.

Most importantly, Ningde Times may have opened up a channel for rapid decline of carbonate lithium, and the cost of new energy vehicle batteries is expected to further decrease.

Only for Core Customers

First, let’s look at the scope of mainframe factories involved in the Ningde Times “lithium mine rebate” plan.

Industry insiders stated that the Ningde Times rebate plan only targets core strategic customers such as Li Auto, NIO, Huawei, CRO, Changan, BAIC, SAIC, etc., and other customers do not have this preferential condition.

According to insiders close to Ningde Times, not all companies currently accept the plan. Some companies are still observing and hoping to start using this method next year. After all, many companies cannot come up with the deposit all at once.

In addition, some industry insiders have concerns about this. Ningde Times’ rebate does not involve the basic price, generally speaking, the battery pricing is a basic price+carbonate and lithium linkage. This rebate actually equals to a 4% price cut. Before that, Ningde quoted a price 10% higher than that of second-line enterprises, and now it is still 6% higher after the rebate.

Car companies need to weigh this price, which is still much higher than that of second-line battery companies, and at the same time cuts off the possibility of car companies expanding their two- and three-supply sources.

NIO may be quite entangled. On the one hand, as the second largest customer of Ningde Times, it relies heavily on Ningde Times. On the other hand, it has invested in Xinwanda, hoping to increase the two-supply source to ensure safety. In addition, the SEMISOLID battery produced by Beijing Weilan New Energy will also be used in its ET7 model. Last year, NIO also announced the production of its own battery.

## Domestic lithium carbonate cost below 200,000 yuan/ton

## Domestic lithium carbonate cost below 200,000 yuan/ton

Participating in this rebate program will likely affect NIO’s series of layouts, but some companies have performed very positively. It is reported that Avita will probably sign the agreement, after all, CATL is Avita’s second largest shareholder. With such a close binding relationship, Avita has almost no other choice. However, Tesla, GAC, and XPeng Motors are not included in CATL’s “plan”.

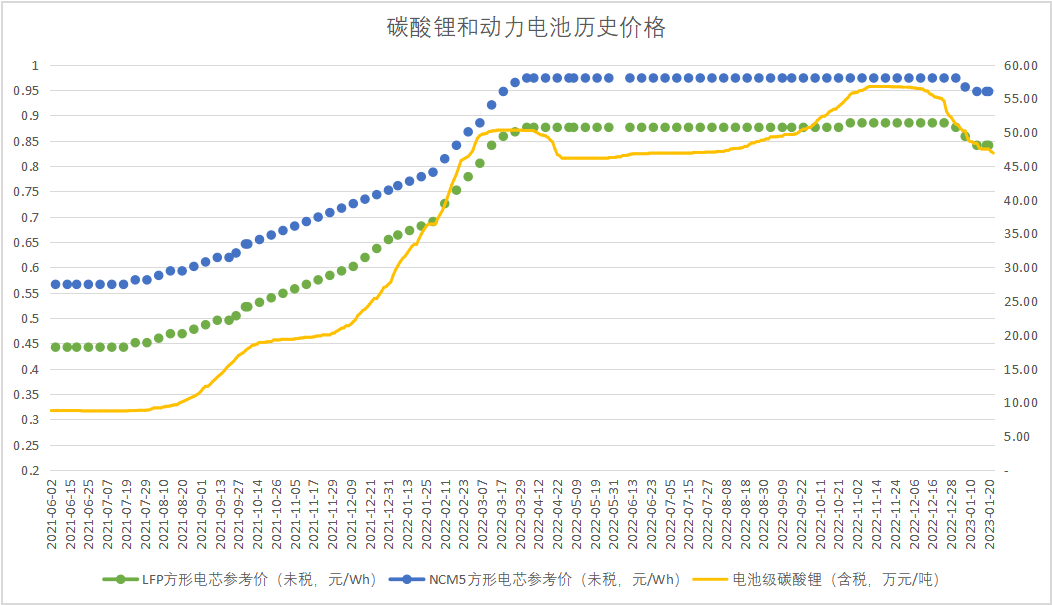

The quantity of low-priced lithium carbonate in China restricts the scope of CATL’s rebates. According to industry insiders’ predictions, CATL’s Jiangxi mine produces about 30,000 tons of lithium carbonate, plus the total amount of carbonate reclaimed by Aoyin Pu, probably enough to meet the needs of core customers. In terms of cost, the lithium carbonate cost of Jiangxi mine is about 150,000 yuan/ton, and Aoyin Pu’s recovery cost is about 170,000-180,000 yuan/ton. The two costs below RMB 200,000 provide CATL with a bottom line.

In addition, while CATL is doing the above rebate operations, it also negotiated with upstream lithium salt factories for a lithium carbonate purchase price of less than RMB 300,000/ton this year.

In addition to CATL, BYD, EVE Energy, and Guoxuan High-tech and other battery companies are all laying out domestic lithium mines.

Domestic battery companies’ self-supply of lithium carbonate

On February 20th, EVE Energy revealed in a conference call that its lithium carbonate production in Qaidam Salt Lake in Qinghai Province will be around 10,000 tons this year. If the lithium resource supply controlled by EVE Energy is roughly based on the 100GWh battery sales volume, it is expected that it can reach 40-50%. There may be some differences in the prices of lithium from different sources, but the cost is generally controllable.

In other words, in addition to CATL, the above-mentioned enterprises also have the capital to offer rebates to downstream car companies. According to Cinda Securities’ prediction, the equity shipment volume of these companies this year is about 59,000 tons, but their total output is about 102,000 tons. The price of this part of lithium carbonate will be significantly lower than that in the overseas market.

If calculated by 700 tons of lithium carbonate required for 1GWh battery production, and calculated based on the total amount of lithium carbonate held by the aforementioned battery companies’ holding companies, they can supply approximately 146GWh of batteries by 2023.According to data from the China Innovation Alliance of the Vehicle Power Battery Industry, the average electric capacity per car in December 2022 is 50.4 KWh. Based on this calculation, the low-cost lithium carbonate held by Chinese battery companies can supply around 2.9 million new energy vehicles in 2023.

If other domestic battery companies with lithium mines follow the trend set by Ningde Times, then the price of lithium carbonate may indeed plummet rapidly.

Second-tier companies are more cautious, but the trend of battery price reduction is clear

In fact, power battery companies had started to reduce prices before Ningde Times’ “Lithium Mine Rebate” was exposed. The usual price transmission period is about 2-3 months, but the rapid decline in lithium carbonate prices exceeded expectations, and the price reduction has continued to expand this year.

Ningde Times clearly aims to accelerate the downward trend of lithium carbonate.

According to statistics from the China Association of Automobile Manufacturers (CAAM), in January 2023, the production and sales of new energy vehicles were 425,000 units and 408,000 units respectively, down 46.6% and 49.9% month-on-month, and down 6.9% and 6.3% year-on-year.

This is the monthly data of several car companies lowering prices combined with the influence of the Spring Festival holiday.

The price cuts of car companies have already begun. Since late October last year, many brands such as Tesla, AITO Wenzhen, and Lynk & Co have lowered prices or introduced car purchase subsidies. New energy car models of brands such as Geely and XPeng have also joined the “price protection and sales promotion” campaign, but the situation is still not optimistic.

If car companies have to reduce prices further to boost sales, the pressure will inevitably be passed upstream, and the prices of batteries and raw materials must decline.

However, second-tier companies do not have the scale and resource advantages of Ningde Times, and must participate in competition by sacrificing cash flow and profits, and face survival difficulties. Therefore, they are relatively cautious.

When communicating with insiders of companies such as Amperex Technology, Eve Energy, Lishen Battery, and J-Well Power on whether to follow suit in price reduction, most people said their company is currently observing.

Companies with mines and sufficient funds are more likely to follow suit. For example, an insider from CATL said, “We still have some differences with Ningde Times’ customers, so it won’t affect us much. We have considered following Ningde Times’ policy, but we will follow our own rhythm.”Representatives from Lishen Power Battery have stated that they are also evaluating the situation and have the ability to keep up with demand, but they will not do so through strong binding agreements.

As previously revealed by Lishen, they will also announce progress in overseas lithium mining in the second half of this year, with the main focus being in South America and Africa.

CATL plans to benefit downstream companies by providing support in terms of strategy and partially giving profits to them, considering that most of their downstream customers are not yet profitable. Meanwhile, their production capacity is expanding and they hope to increase their market share among customers.

It is not yet known how CATL will provide these benefits.

Fujian-based battery makers Funeng Technology, Zhongchuangxin Aviation, and J-Walker are still cautious and will continue to monitor the situation, choosing not to follow suit for now.

The purpose of Contemporary Amperex Technology (CATL) is clear: first, they want to lower the expected price of lithium carbonate by lowering their prices. Secondly, they want to further suppress second-tier battery companies, including Lishen, SVOLT Energy Technology, Zhongchuangxin Aviation, and Xingwangda, who have lost many customers to CATL in recent years while still operating at a loss. CATL wants to increase the losses of these companies to the point where they can no longer compete in the industry.

Even if the rebate policy of CATL does not work when lithium carbonate price reaches CNY 200,000 per ton, at least they will not lose money. As stated by a representative from Chinese battery maker Guoxuan High-Tech: “We do not want to make money from lithium carbonate. Our goal is to further replace fuel vehicles with new energy vehicles and enlarge the new energy car market so everyone can truly benefit.”

If lithium carbonate does reach CNY 200,000 per ton, then the cost of each electric car will be reduced by CNY 20,000 to CNY 30,000, resulting in more benefits for consumers.

However, it is certain that the threshold for remaining in the industry will continue to rise. Battery companies that don’t control upstream resources will have even less room to survive. The price of new energy vehicles is expected to continue to decline.

This article is a translation by ChatGPT of a Chinese report from 42HOW. If you have any questions about it, please email bd@42how.com.