Ranking of Global EV Battery Installation in 2022 Released by SNE Research

Author | Lingfang Wang

Editor | Kaijun Qiu

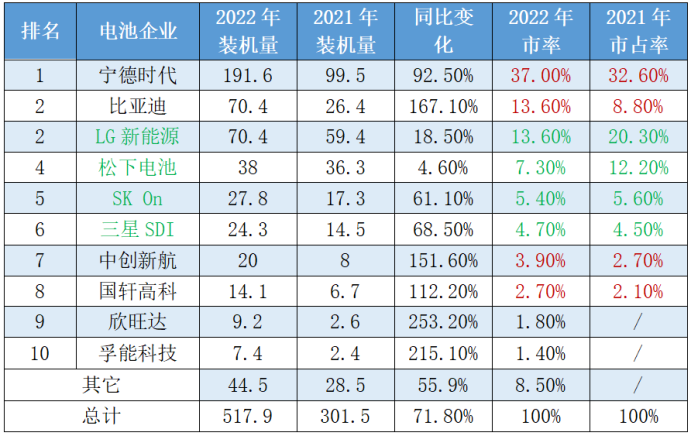

On February 7th, SNE Research, a South Korean market research institution, released the ranking of global EV battery installation for 2022, and CATL (Contemporary Amperex Technology Co., Limited) once again topped the list without surprise.

As the leading enterprises, CATL, BYD (Build Your Dreams), and Japanese and Korean giants have maintained relatively stable rankings.

Specifically, the market share of the two major battery giants in China is still slightly increasing, while the market share of Japanese and Korean enterprises has decreased significantly, although their installation volume has increased.

According to tracking data provided by SNE, the estimated usage of EV batteries worldwide is expected to reach about 749 GWh in 2023.

Fierce Competition among Chinese Enterprises

Overall, the growth of CATL comes from the sales growth of Tesla’s Model 3 / Y, GAC Aion Y, and Geely’s ZEEKR 001.

BYD’s batteries are still mainly used for self-supply, and the overall sales volume is driven by the hot sales of series models such as Han, Yuan, and Qin. In 2022, BYD also made initial progress in supplying power batteries to Chinese auto manufacturers such as FAW (First Automotive Works) and Changan Ford.

Foresight Science & Technology entered the top 10 with a three-digit growth rate, thanks to the strong growth of the Mercedes-Benz EQ series in Europe.

At present, in the passenger car sector, the models supported by Foresight Science & Technology mainly include Mercedes-Benz EQS/EQA/EQB/EQE, GAC Aion S/Aion V, Voyah Dream Edition, JMC Yi/EZEV3, and Kawei Chuanwei EV6, etc.

Since last year, the development of Xinwangda’s power battery sector has been rapid, with revenue growth of more than 500% in the first half of the year. Currently, more than 80% of domestic host manufacturers have relevant cooperation with the company, and their main customers include Dongfeng Motor, Geely Auto, Dongfeng Liuzhou, and XPeng Motors.

Xinwangda also holds a considerable share in HEVs. In 2020, the company was recognized by overseas customers and won the designated order for Nissan-Renault power batteries. Last year, it also announced its entry into the Volkswagen supplier system in Germany.According to the data from the production, engineering, and research of the automotive industry, among the domestic customers of Xinwanda, Dongfeng and Geely are relatively supply chain-intensive customers. It is expected that the future new energy enterprises will gradually increase.

Currently, Chinese second-tier battery enterprises represented by Xinwanda have gradually increased their competitiveness, which has constituted certain pressure on both domestic and foreign battery enterprises, including Chinese first-tier enterprises.

Japanese and Korean enterprises decline

Contrary to the rapid growth of Chinese enterprises, the growth of South Korea’s three giants-LG New Energy, Samsung SDI, and SK On-is slow. The market share of the three giants has decreased from 30.2\% in the same period last year to 23.7\%, a decrease of 6.5\%.

In terms of specific installed capacity, in 2022, LG New Energy’s installed capacity was 70.4GWh, a year-on-year increase of 18.5\%, regaining the second place. SK On’s installed capacity was 27.8GWh, an increase of 61.1\%; Samsung SDI installed capacity was 24.3 GWh, an increase of 68.5\%. All three companies achieved double-digit growth, but compared with China’s three-digit growth, the decline in market share is not surprising.

Compared with South Korean manufacturers, Japanese manufacturer Panasonic’s growth is slower, and its market share has also declined compared to last year. Panasonic ranks fourth in installed capacity with a capacity of 38GWh, a year-on-year increase of 4.6\%, but its market share has decreased by 4.7\%. As one of Tesla’s main battery suppliers, Panasonic’s year-on-year growth was made possible by the growth in Tesla’s North American vehicle sales and Toyota BZ4X sales.

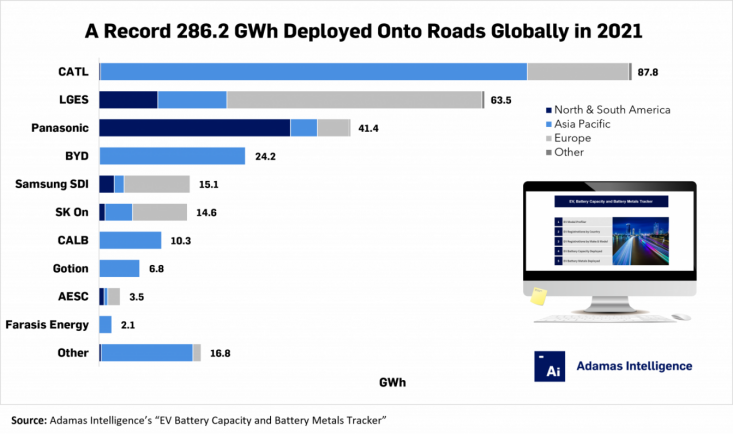

In addition, it should be noted that the development of overseas new energy vehicles is much slower than that of Chinese automakers. Panasonic is one of the earliest companies to supply power batteries to automakers and is also one of the earliest battery companies to supply Tesla. However, Panasonic’s dependence on Tesla is extremely high. According to data from Adamas Intelligence, in 2021, 87\% of Panasonic’s batteries were used in Tesla cars, which was close to 90\% in 2020.

There is no data available for 2022, but it is unlikely to see a significant reduction since Panasonic is actively building production lines for Tesla’s 4680 batteries.Of course, Panasonic is also actively expanding its customer base. At present, it has expanded to companies such as Volkswagen, Ford, and Lucid, and has become the largest supplier of power batteries for Volkswagen and Ford.

From the 2021 data published by Adamas Intelligence, it can also be seen that the three Korean giants’ share of the Chinese market is very small, and they have basically withdrawn from the competition with Chinese battery companies.

Companies with many overseas customers are slower to ramp up production

Compared with last year’s rankings, this year Xinwanda and Funeng Technology have replaced last year’s winners, Contemporary Amperex Technology Limited (CATL) and SVOLT.

As a new force in the battery industry, CATL officially debuted in 2019. New companies must go through a series of challenges such as capacity building and capacity ramping.

AESC, as an old power battery enterprise, also faces similar problems. In 2019, SVOLT began to invest in capacity building in China, and growth of the shipment volume was relatively limited due to limited overseas capacity.

What Honeycomb Energy and SVOLT have in common is that they have a certain number of overseas customers, such as Honeycomb Energy receiving orders from PSA Groupe (Stellantis Groupe) and electric bus orders from Turkey’s OTOKAR company in 2021.

Especially, SVOLT has a very high proportion of overseas customers, including German BMW, Mercedes, Japanese Honda, Nissan, and French Renault. It had previously signed a cooperation agreement with FAW, with progress mostly in the field of heavy truck replacement batteries.

These overseas customers cannot convert orders into actual installed capacity in the short term. Generally, it takes about 3 years from designated supply to actual supply for overseas automakers, and about 1 year for domestic automakers.

Therefore, the growth rate of these two companies’ installed capacity is relatively slow, and they are easily left behind by manufacturers mainly targeting domestic automakers.

It can be seen that the competition for the ninth and tenth rankings is very fierce. With Honeycomb Energy’s collaboration with Stellantis Groupe’s 16 billion project, Renault providing 5-year 40GWh to 120GWh power battery orders to SVOLT, and Yiwei Lithium Energy’s increasing volume on overseas orders such as the BMW project, the rankings of battery companies may change.

However, the continual decline in the market share of Japanese and Korean companies seems to be irreversible. The power battery market has become a stage dominated by Chinese companies, and future competition will increasingly be between local companies.# 标题一

这是一段加粗的文字,其中包含一个链接和一个图片:

以下是一个列表:

- 项目一

- 项目二

标题二

这是一个段落,其中包含一个 code 字符串。

print("Hello, World!")

该段落还包含一个表格:

| 列1 | 列2 |

|---|---|

| 1 | 2 |

| 3 | 4 |

标题三

这是一个有序列表:

- 项目一

- 项目二

该列表也可以嵌套:

- 项目一

- 项目 1a

- 项目 1b

- 项目二

标题四

这是一个引用:

这是引用的内容。

This article is a translation by ChatGPT of a Chinese report from 42HOW. If you have any questions about it, please email bd@42how.com.