Special Contributor | Thrilling Comfort

Editor | Qiu Kaijun

On December 9, Li Auto released its Q3 financial report. The financial reports for the top three new automakers have now been disclosed.

At the performance briefing, Li Auto expressed very positive expectations for Q4 delivery, average selling price per vehicle and profitability. Li Auto’s chairman Li Xiang also stated in an internal memo that the company had completed the “from zero to one” phase and needed a comprehensive organizational transformation to embrace the “from one to ten” phase of achieving a revenue of 10 billion yuan.

The performance of the top three new automakers has been mixed this year, but overall, they are recognized by the industry as the leading players with relatively good products and operations. Similar to the “from zero to one” statement, some people believe that these three companies have already “survived”.

Today, we will combine the Q3 financial reports of these three companies and the competition pattern in the new energy vehicle industry to see how the new players can survive in this market.

Comparison of Core Financial Data

-

NIO: Its quarterly sales volume and overall revenue were the highest in Q3, and it was the first one of the three new automakers to achieve two consecutive quarters of revenue exceeding 10 billion yuan.

-

XPeng: Recently, XPeng’s sales performance has been the worst among the three companies. The competitiveness of its previous generation products has declined, and more importantly, the sales performance of G9 has been poor. Thus, XPeng has the lowest revenue, lowest monthly revenue per store, lowest gross profit margin per vehicle, and the highest cost ratio among the three companies.

-

Li Auto: Li Auto has the highest operating efficiency with the best performance in terms of monthly sales per store, overall cost ratio, and operating losses.

-

Operating Losses: The operating losses of the three companies in Q3 were quite astonishing: -3.87 billion yuan for NIO, -2.202 billion yuan for XPeng and -2.129 billion yuan for Li Auto. This means that the operating losses per vehicle sold were respectively -115,500 yuan, -94,100 yuan, and -91,400 yuan for the “NIO+XPeng+Li” trio. Compared with the first half of the year, these operating losses not only did not shrink but expanded. At present, the situation of “the more we sell, the more we lose” cannot be completely changed in the short term for the “NIO+XPeng+Li” trio.

“NIO+XPeng+Li” Underperformed in the Market

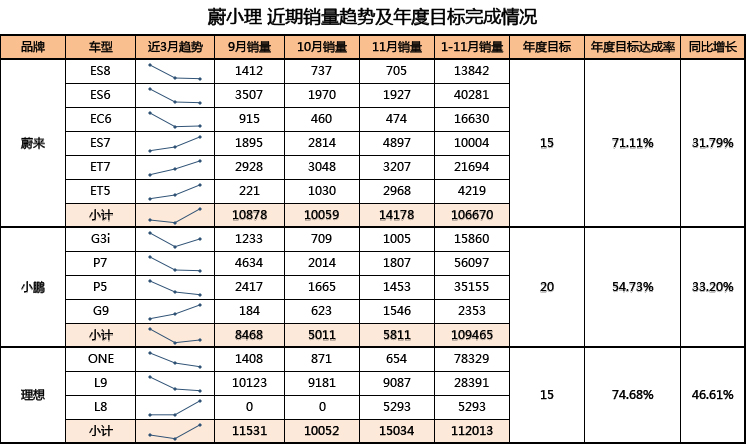

- The ambitious goals set at the beginning of the year were not achieved.Three new forces in the automobile industry set relatively aggressive sales targets at the beginning of 2022, “riding the wave of hot sales in December 2021”: NIO and Xpeng hope to achieve 150,000 units sold, while Li Auto aims to sell 200,000 units or even challenge the goal of 250,000 units!

Dreams are wonderful, but reality can be very harsh: As of November, not only have they failed to achieve their respective annual targets, but they have also “lost the market” in terms of growth rate.

NIO: Sales of 106,670 units were accumulated from January to November, a year-on-year increase of 31.79\%, only achieving 71.11\% of the target of 150,000 units, with only one month left. Even if the sales increase by more than 20,000 units, the annual target cannot be achieved.

Xpeng: Sales of 109,465 units were accumulated from January to November, a year-on-year increase of 33.20\%, only achieving 54.73\% of the target of 200,000 units. Not only did the sales of the new G9 model not increase, but the sales of old models were also weak, resulting in annual sales being overtaken by Li Auto.

Li Auto: Sales of 112,013 units were accumulated from January to November, a year-on-year increase of 46.61\%, only completing 74.68\% of the target. Even if monthly sales increase by more than 25,000 units, the annual goal cannot be reached.

According to the latest data from the China Passenger Car Association, the sales of new energy passenger vehicles in China in January-November 2022 reached 5.03 million units, a year-on-year increase of 100.1\%. The top three new forces not only failed to reach their brand’s annual sales targets, but also grew at a slower pace than 50\%, far behind the market.

Of course, they would say that in the second half of 2022, the top new forces have all started iterating into their second-generation products, and fluctuations in sales during the product transition period are normal.

Let’s continue to look at the different strategies and performances of each company after iterating into the second-generation products.

2. The second-generation products of each company have different performances

NIO: Leading the NT2.0 era, gradually using 775 to fully replace the previous generation 866 products. However, as the next-generation product, ES7 is considered by users to be a “re-skinned car” of ES6, with more changes in the hardware configuration of intelligent driving. After the delivery of ET7, various defects and problems have continued to emerge, and there has even been a state of “heavy rain outside, light rain inside the car.” ET5 has also been criticized for its limited interior space, which is not suitable for consumers over 180cm tall…XPeng: The release of G9 can be called a “farce” in the automotive industry this year. It was a grand gesture of “increased configuration and price reduction” within 48 hours after the press conference, and the press conference also triggered a series of internal organizational and personnel “earthquakes” within XPeng. The latest news is that He XPeng has returned his focus to car manufacturing, co-founder Xia Yan resigned as executive director, and Li Pengcheng, head of the brand’s public relations department, resigned on December 9.

Li Auto: Compared to NIO and XPeng, Li Auto’s performance is currently the most stable. Although it announced the discontinuation of ONE shortly after the L9 launch, which brought serious customer reputation and public opinion crisis, it relied on strong marketing methods and the explosive effect of centralized delivery to dilute the various problems caused by the ONE discontinuation. At the same time, Li Auto quickly released the upgraded version of ONE called L8, and achieved the delivery of L8 in November at a fast pace to cope with market changes.

Looking at the sales trends of the second-generation products of various companies in the past three months, NIO’s ES8 is relatively stable, with a slight and steady increase each month as production capacity increases and the company climbs up the learning curve. It is expected to achieve its first delivery target of 20,000 vehicles in December.

Li Auto’s L9 achieved sales of over 10,000 in the first month through “centralized delivery”, but sales declined for two consecutive months after that. With the start of centralized delivery of L8 in November, the data for December is expected to be better. The company’s expectations are very high for the Q3 earnings conference call, with a Q4 delivery expectation of 45,000-48,000 units, which means that December’s delivery is expected to be 20,000-23,000 units. At the same time, it is expected that the steady-state monthly sales of L9 will be 8,000-11,000 units, and L8 will be 11,000-14,000 units, which means that the monthly sales of just two models priced above 350,000 RMB can reach 19,000-25,000 units.

XPeng performed the worst among the three companies. Due to the climbing of production capacity, G9 has not yet achieved volume production, and the sales of P7 and P5 have continued to decline. In particular, the main model P7 has rapidly declined from 9,000 units in March to less than 2,000 units, which shows the aging of the product’s competitiveness and the fierce competition in the market.

At present, the total sales of China’s passenger car market will fluctuate around 20 million units with a fluctuation range of positive or negative 5% for a period of time. When the overall market no longer continues to rise, and companies begin to face the ceiling of capacity and internal competition, their strategic choices will determine their trends for the next 3-5 years.

Choices and Adherence

NIO: With limited pure electric vehicle market space priced above 400,000 RMB, is having multiple brands a necessity or a helplessness?On December 12, at the NIO media event, the company announced the production of its 300,000th passenger car and plans to complete the migration of its entire vehicle lineup to the second generation platform in the next six months.

Within the new NT2.0 product system, NIO continues to refine its product offerings, including the replacement model for the 775, the 866, and three new models planned to launch next year: the ES4 (compact SUV), ES5 (medium-sized SUV, same platform as ET5), and EC7 (sedan version of ES7). The upcoming large vehicle with the codename “Aries” will be named the “9 series”. Additionally, a new model, the EE, is planned to be released next year for launch the year after.

NIO is planning to complete the full transition to NT2.0 in six months and achieve comprehensive coverage of sedans and SUVs with over 300,000 units sold, from entry-level to large vehicles, in 18 months, completing a full layout of a “luxury brand”.

From a financial perspective, NIO has the highest unit sales price and unit gross margin. However, it is also the only new energy company with a negative service gross margin, and its Q3 service loss even reached nearly CNY 7,000. Such a loss rate has surpassed the profit level of most independent car brands.

NIO’s “loss-making services” have always been a hot topic, such as this year’s “Driving Enjoyment Service,” which includes driving and pickup services, elderly care services, school bus services, and even homework assistance. According to official NIO data, there were 1.2 million road service orders from January to November this year, with an average of over 100,000 orders per month. To a certain extent, this is the advantage of NIO’s full life cycle service. However, the amount of losses incurred by these services far exceeds the tolerance of ordinary OEMs.

NIO is attempting to build its own brand and castle with its unique “battery swap + service” offering, realizing the vision of the first independent luxury brand, and its performance so far has been good. With an average price of over CNY 400,000, NIO has achieved over 100,000 annual sales, and there are no models priced below CNY 400,000, which is second only to Porsche, Land Rover, and Mercedes-Benz in terms of average price, and a price range that many brands aspire to achieve.However, for NIO, “luxury brand” label is not enough. In November, NIO accounted for 77% in the market share of 400,000+ pure electric new energy vehicles, and also over 35% in the market share of 300,000-400,000 pure electric new energy vehicles.

However, according to the data released by the China Association of Automobile Manufacturers, the mainstream price range in the Chinese market is 100,000-250,000 RMB, accounting for 57.8% of the overall market share. The market space for vehicles priced at over 400,000 RMB is relatively limited, accounting for only 5.5% of the overall market share. This means that the market capacity ceiling is at 1.1 million to 1.2 million vehicles.

For NIO, the upper limit of the high-end market is too low, and the only option is to build multiple brands through exploration.

With the operation of NIO’s second advanced manufacturing base and the construction of its self-developed battery base, the first model of the Alpine brand, the B-level SUV product with the codename “DOM”, will also return to the market with a price range of 200,000-300,000 RMB, which is most likely the “battery-swapping version of Model Y” mentioned by executives.

For NIO, it is not only necessary to solve the problem of excessively high R&D and market cost rates (as high as 43.11%, meaning that 43% of the money is spent on R&D, management, and marketing costs for each car sold), but also to resolve the service content and differentiation for different brands and customers. For sub-brands, if there is no service provided, why not buy another brand in the same category? If the same service is provided, it will have a real impact on the clients of the mother brand. If a trimmed version of the service is provided, adding a new brand will inevitably divert the service resources. How can two different service standards be used to achieve this?

These are all real problems and challenges facing NIO and its sub-brands. However, no matter what, we hope that NIO can find a unique way for its own “luxury brand”!

2. XPeng: Ignoring market changes is the greatest risk

In XPeng’s Q3 earnings conference, the core message conveyed by the management was the organizational restructuring and continued focus on “intelligent driving”.

Regarding the first point, there has already been much discussion on the internet. Today, we will focus on the second point: can XPeng’s focus on “intelligent driving” bring about a turnabout for the company?

Let’s start by looking at the supply and demand sides:

First, on the supply side, XPeng’s product planning has always been the most irregular among the three new forces.

The first model is G3, primarily an A-class SUV, followed by the launch of the B-class P7. In the face of the competition at the time, Model 3 dominated the market, with only Han EV and P7 competing. P7 relied on its appearance and intelligent cockpit to thrive in the market. Soon after, the P5, which was based on the same platform as G3, was released. Although it had a laser radar, it had poor space performance and appearance, and its BOM cost was high. Therefore, it could only try to seize the market of A-class intelligent cars priced around 200,000 RMB. G9’s failure is needless to say, appearing at the Guangzhou Auto Show at the end of 2021, but it was delayed until October 2022 to achieve limited deliveries. It is weird that without large-scale organizational restructuring, such organizational and supply chain capabilities could continue.

At the third quarter briefing, XPeng stated that there will be three heavyweight models next year:

E Platform: A redesigned P7 with unchanged space, without a 800V high-voltage system, still focused on intelligent driving, and an improved charging power. The expected price will be comparable to the current model.

SUV based on F Platform: Codenamed F30, smaller in size than G9, priced between 200,000 and 300,000 RMB, it is planned to be launched in mid-2023.

Third vehicle based on H Platform: Codenamed H93, it is a C-class MPV that will be launched around Q4 2023.

These vehicles on these platforms will have a high degree of commonality in terms of power systems, intelligent driving systems, chassis and electronic architecture, as well as corresponding supply chains and production capabilities.

Unfortunately, XPeng’s F30 and H93 will once again fall into the Red Sea of competition (this is the third time XPeng has entered a fierce competition). Especially the H93, it is very likely to be involved in the most fiercely competitive MPV market in 2023- from the Buick Century, Zeekr 009, DENZA D9, Hongqi HQ9, Voyah Dream Family, Toyota’s Serena and Gray Voyager, to SAIC’s Master Edition, not to mention the Ideal W01 and GWM MPV that are planned to be launched in 2023- XPeng’s product planning department must be very nervous.

Regarding the consumer end, as the new energy market changed rapidly in 2022, the retail penetration rate, as of November, has reached 27.37%. It can be said that this year, at least one of every four vehicles sold in China is a new energy vehicle. New energy is no longer the choice of early adopters from 1-2 years ago, but the mainstream choice of mainstream consumer groups.## Translation

So despite a gap in the level of intelligence between BYD, the leader of new energy vehicle sales, and the top new players, BYD is still expected to surpass FAW-Volkswagen’s annual sales of 1.8 million+ with new energy vehicles.

The core reason for this is that the current “smart driving” technology is only binary, meaning that for most ordinary consumers, there are only two states: “1” means that they can safely hand over the steering wheel to the chip and algorithm, and if the car manufacturer cannot do so at present, then for most customers, it is the same as “0”.

Even the current “best global ADAS system-FSD” is not of much practical significance for Chinese consumers, and consumers still flock to the entry-level standard range version. The optional rate for domestic “FSD” is also less than 5%.

In such a market environment, XPeng seems to have not even noticed the changing needs of customers, and is still fully focused on betting on its “smart driving” system. Admittedly, XPeng’s intelligent cockpit was once the best in China, but how to get consumers to pay for the “smart driving” system that still gives poor experience? XPeng has tried many methods, even reducing the charging service rights and bundling with XPolit to achieve higher purchase and usage rates. According to the third-quarter report, XPeng had the highest proportion of service revenue among the three top new players.

However, in the current stage of the market, the market has repeatedly verified that “smart driving” is not the primary factor driving customer purchases, and it cannot even be considered an important factor for mainstream consumers.

XPeng’s latest all-out bet seems to have hit the right direction, but it has once again overlooked the changes in the market! With increasingly fierce competition, the market will not give a new player so much time. The company has already failed with two models. If another 1 or 2 models have research and development failures, the entire company may be destroyed. Even with 30-40 billion yuan in cash, it may not be enough, especially if the restricted funds, short-term liabilities, and payables are deducted, leaving only 23.6 billion yuan in cash available.

- Ideal: Is it possible to realize the dream of relying solely on the family user market and achieving a revenue scale of over 100 billion yuan?

In terms of market awareness and understanding of segmented customers, IDEAL not only ranks among the top new players but also leads most of the main automakers.

According to the third-quarter report, “Due to unexpected market demand for IDEAL L9 and the accelerated launch of IDEAL L8, as well as the reduction in forecast orders for IDEAL ONE, the inventory provision and purchase commitment losses related to IDEAL ONE amounted to RMB 802.8 million (USD 112.9 million).”The information confirms the market sensitivity of ideals: simply put, the launch of L9 performed better than expected, which seriously affected ONE’s orders. At the same time, in order to cope with the ceiling of the mid-to-high-end market, it was decided to quickly launch L8 to take over from the ideal ONE and compete in the price range of 350,000 to 400,000 yuan. However, because the previous order for the ideal ONE was too optimistic, the lowest number of parts purchases was promised to partners, resulting in a loss of up to 803 million yuan this time.

Why did Ideals stop producing ONE? On the one hand, L9 products sold well, and on the other hand, three products, L6/L7/L8, were launched in one go, covering the family-oriented SUV market with a price range of 25,000 to 50,000 yuan. Expanding the product matrix to cover more price ranges is to cope with possible market changes and fluctuations.

If according to the ideal third-quarter report: after deducting the additional loss of 800 million yuan for the ideal ONE, the gross profit margin of the automobile sales business in the third quarter was 20.8%. If this data is further broken down, excluding the revenue and cost of the on-sale ideal ONE in Q3, the gross profit of L9 should be at the level of 25-26%. If models including L8 in Q4 can achieve a gross profit margin of more than 24%, Ideal will be the one closest to Tesla in financial data!

From the recent product planning point of view, in addition to L7 and L6, Ideal will also launch W01, a pure electric version of the C-class MPV in 2023, which is expected to be available in the first half of next year, and its derivative B-class MPV – W02; W03 and The full-size SUV-S01 will also be launched in 2024. According to this plan, by 2024, Ideal will have 9 cars to cover family users.

At the same time as realizing the above-mentioned product matrix, Ideal also experienced an “internal storm” in the second half of the year, which directly caused this large-scale organizational price adjustment. In the open letter to Ideal employees on December 9th, it was considered that: Ideal Motors has completed the phase from 0 to 1 and is about to enter the phase from 1 to 10,and will fully upgrade to a matrix-type organization, and start to impact on revenue of billions of yuan.# The Indicators to “Survive”

The ideal hope is to open up the road to billion-dollar revenue by organizing a change and a product positioning that captures all family customers across the network. However, the case of Great Wall has set an example—a single layout of SUVs easily reaches the sales ceiling.

In less than a year, the performances of the leading new forces are starting to differentiate. NIO and IDEAL are increasing their sales, while XPeng is falling behind. The indicators for the new forces to “survive” are relatively simple, regardless of “from 0 to 1” or billion-dollar revenue: firstly, achieving the scale and economy of 300,000 vehicles sold annually; secondly, achieving quarterly positive profits as soon as possible.

This article is a translation by ChatGPT of a Chinese report from 42HOW. If you have any questions about it, please email bd@42how.com.