Author: Xiong Ruifeng

It’s the end of the year, and everyone is feeling down except for BYD.

This year’s consumer market has been full of surprises with ups and downs, leaving some happy and others sorrowful.

During the middle of the year, we often talked about a term “low season not so low”. Due to the economic winter caused by the pandemic in the first half of the year, the traditionally slow season for passenger cars from June to September saw an unusual phenomenon with tens of thousands of consumers making “revenge” purchases.

Now, at the end of the year, this “cold wave” has returned with a vengeance, the aggressive attack has dampened the enthusiasm of the market, and as a result, it has led to the “busy season not so busy” in November.

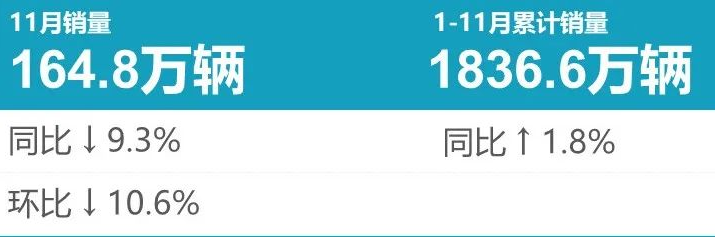

According to the latest data released by the China Passenger Car Association, the retail sales of passenger cars in November 2022 reached 1.649 million units, a year-on-year decrease of 9.2\% and a month-on-month decrease of 10.5\%. This is the first time since 2008 that the “Gold September, Silver October, Bronze November” has shown a month-on-month decline.

From a macro perspective, retail sales from January to November totaled 18.367 million units, an increase of 1.8\% year-on-year with a net increase of 317,000 units. However, the main contribution was still due to the implementation of the car purchase tax preferential policy from June to September which led to a surge in sales. Due to the outbreak of the pandemic in October and November and the significant impact of some dealerships closing down on normal automotive consumer rhythms, the retail sales in October and November dropped significantly.

In terms of specific data, the most eye-catching performance in November was the increase of new energy vehicles, which rose by 7.8\% month-on-month and 58.3\% year-on-year, with a penetration rate reaching 36.3\%, a 15 percentage point increase from 20.8\% in November 2021. In contrast, gasoline cars (SUV/MPV/sedan) generally saw a significant decline, with a month-on-month decrease of 18\% and a year-on-year decrease of 27\%, completely reversing the positive growth trend year-on-year growth of 6\% from June-September this year.

The performance of the manufacturer rankings showed that the total retail sales of the top 15 auto companies this month was 1.239 million vehicles, and the market concentration rate was 75.2%. However, compared with last month, the number of companies with retail sales exceeding 100,000 vehicles decreased slightly. Currently, there are four companies including BYD, Geely, FAW-Volkswagen and Changan, among which BYD has been ranked first for five consecutive months this year.

The performance of the manufacturer rankings showed that the total retail sales of the top 15 auto companies this month was 1.239 million vehicles, and the market concentration rate was 75.2%. However, compared with last month, the number of companies with retail sales exceeding 100,000 vehicles decreased slightly. Currently, there are four companies including BYD, Geely, FAW-Volkswagen and Changan, among which BYD has been ranked first for five consecutive months this year.

It is worth mentioning that although with a cumulative sales volume of 1.58 million vehicles from January to November, BYD only ranked second, it is only 10,000 vehicles behind the first place, FAW-Volkswagen (1.59 million vehicles). According to the current “cheating” growth rate, BYD will undoubtedly surpass FAW-Volkswagen in December to become the sales champion of the whole year of 2022.

In addition, the sales performance of domestic brands hit a new high in November, with a retail volume of 870,000 vehicles, a year-on-year increase of 5%, accounting for 53.4% of the domestic retail market share. That means one out of every two new cars sold is domestically produced.

As a comparison, mainstream joint venture brands had a retail volume of 540,000 vehicles in November, a year-on-year decrease of 31% and a month-on-month decrease of 23%. Among them, German brands had a market share of 18.9%, a year-on-year increase of 0.1 percentage point, Japanese brands accounted for 15.3% of the market, a year-on-year decrease of 6.9 percentage points, and American brands had a slight increase in market retail, with a share of 9.6%, an increase of 0.6 percentage points year-on-year.

Sedan market, BYD dominates the list

In terms of segmented sedan sales, the domestic sedan market sold 804,000 vehicles in November, a year-on-year decrease of 9.9% and a month-on-month decrease of 12.6%; Cumulative sales from January to November reached 9.143 million vehicles, a year-on-year increase of 3.9%. Overall, in November, domestic cars have overtaken joint venture cars, becoming the new ruler of the sedan market. Among the top ten, domestic cars occupied five seats and monopolized the top four.

At the same time, there were only two car models with sales exceeding 30,000 units on the sedan list in November, namely, Wuling Hongguang MINI EV and BYD Han. Among the top 15, only four car models had a positive year-on-year increase in sales.

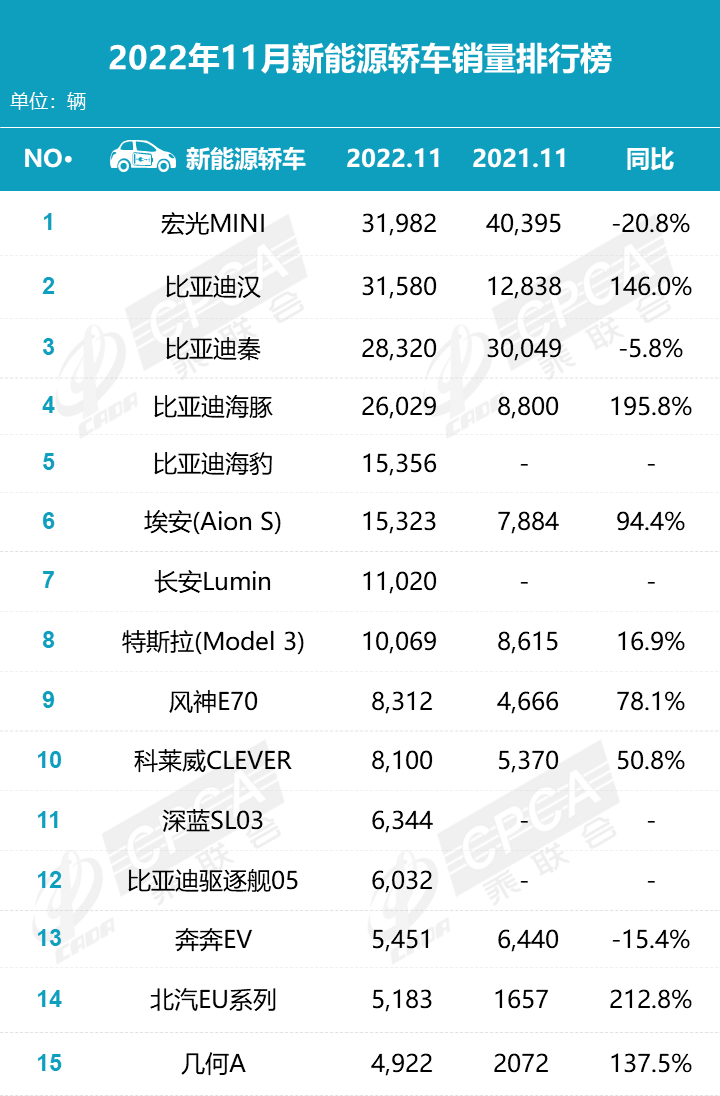

In terms of specific rankings, although the Wuling Hongguang MINI EV has occupied the top spot for three consecutive months (monthly sales of 31,982 units), its year-on-year data has decreased by 20.8%.

“Second, third, fourth places all belong to BYD. The monthly sales volumes of Han, Qin and Dolphin all surpassed the threshold of 26,000 units. Han has even exceeded 30,000 units and it is only a few hundred units away from the top spot of Hongguang MINI.”

Among the domestically-made models on the list, there is also Geely Emgrand, which ranked eighth this month, and its sales reached 19,367 units. Meanwhile, BYD’s first sports coupe, the Dolphin, broke through 15,000 units in monthly sales, ranking 12th.

The previous year’s sales champions, the Dongfeng Nissan Sylphy and the SAIC Volkswagen Lavida, both experienced a significant decline, ranking fifth and sixth respectively, with monthly sales barely reaching 20,000 units. Meanwhile, the joint venture midsize sedan players still could not see FAW-Volkswagen Magotan. Only GAC Toyota Camry, SAIC Volkswagen Passat, and GAC Honda Accord made it on the list.

“It is worth mentioning that the missing person from last month, the Tesla Model 3, has continued to be missing this month.”

Looking at the overall sales from January to November, four models on the list had cumulative sales of over 300,000 units, including Dongfeng Nissan Sylphy, Hongguang MINI EV, BYD Qin, and the new SAIC Volkswagen Lavida. However, Sylphy’s lead advantage in data is gradually diminishing. It is currently impossible to determine who the sales champion of the car market will be this year.In addition, the growth rate of BYD models is very rapid this year, and perhaps by 2023 we will see the feat of three BYD models occupying the top three spots on the list.

SUV is also dominated by domestic production

In terms of SUV sales, the sales volume in November reached 964,000 vehicles, a year-on-year increase of 9.3% and a month-on-month increase of 2.8%; while the cumulative sales volume of SUVs from January to November was 7.868 million, a year-on-year decrease of 3.7%.

Regarding the overall data of the SUV market in November, the overall performance was bleak, and only 18 models had sales exceeding 10,000, among which Chinese-made SUVs performed outstandingly, occupying eight seats in the top ten, while joint venture SUVs performed poorly.

In terms of model ranking, BYD is undoubtedly fully fired, with three models on the top ten list, among which the BYD Song family, with its excellent product strength and competitive price, has become the most popular SUV model (monthly sales of 63,600 vehicles), with a comprehensive layout of pure electric and hybrid models such as the Song Pro series and the Song PLUS series; and the younger brother BYD Yuan PLUS also achieved a sales volume of 20,200 vehicles, ranking fourth, which is admirable for a pure electric vehicle.

The elder brother BYD Tang family also achieved a single-month sales volume of 19,600 vehicles for the first time, a year-on-year increase of 145%. It is not easy to achieve such a result as a SUV model priced at 200,000 yuan.

Tesla Model Y, with a monthly sales volume of 52,424 units in November, a year-on-year increase of 126.8%, became the second-place winner with considerable strength. Its performance was also quite impressive, especially considering that some of Tesla’s vehicles in China are exported overseas. The performance of Model Y is even more commendable.

Tesla Model Y, with a monthly sales volume of 52,424 units in November, a year-on-year increase of 126.8%, became the second-place winner with considerable strength. Its performance was also quite impressive, especially considering that some of Tesla’s vehicles in China are exported overseas. The performance of Model Y is even more commendable.

Haval H6, an old player, ranks third. Although it had held the monthly sales champion title for several months before, the pressure on its sales growth has increased significantly due to the rapid penetration of new energy vehicles. However, Haval timely transformed and introduced plug-in hybrid and hybrid models (with the plug-in hybrid version selling over 4,000 units per month), achieving a small breakthrough in sales in November, with 20,836 units sold.

In addition, domestically produced models, including Changan CS75, Yidong E, NIO ES8, and Geely Boyue L, have achieved breakthroughs, ranking sixth, ninth, tenth, and eleventh, respectively.

As for the overall performance of joint venture SUVs, only Volkswagen Touareg L made it to the top ten. Former star players such as GAC Toyota Highlander, Dongfeng Honda CR-V, GAC Honda UR-V, and FAW Toyota RAV4 also had relatively mediocre performances.

In terms of total sales volume from January to November, the BYD Song family maintained its position as the leader, selling 408,542 units, an increase of 127.8% compared to the same period last year. Tesla Model Y and Haval H6 remain in the second and third place, with sales of 285,927 and 234,157 units, respectively. Honda CR-V and Changan CS75 maintained their rankings in the fourth and fifth place, and there were no significant changes in the top five rankings compared to the cumulative sales from January to October.

The luxury market is no longer strong

Despite policies such as the purchase tax, luxury brands (cars priced over 300,000 RMB) in November also fell victim to the “storm,” with significant decreases in sales compared to the same period last year, particularly notable in sedans and SUVs represented by BBA.

As for high-end sedans, the Mercedes-Benz C-Class, with 13,718 units sold, took the top spot for the first time since its upgrade. The BMW 3 and 5 Series, Mercedes-Benz E-Class, and Audi A4L remained popular with domestic consumers, with monthly sales exceeding 10,000 units.

From January to November accumulated sales, the BMW 5 and 3 Series brothers firmly occupy the top two spots, followed by the Mercedes-Benz E-Class and the Audi A4. Of course, apart from BBA, other brands’ models exhibit significant disparities in sales, and challenging their position is not easy.

Turning to the high-end SUV market, whether in terms of monthly sales or cumulative sales from January to November, the Tesla Model Y has a significant advantage in the list. The BMW X3 ranked second with 12,632 units sold in November, followed closely by the Audi Q5L and the Mercedes-Benz GLC, in the third and fourth positions, respectively.

In addition, the Li Auto Li One sold 9,087 vehicles in November, although not breaking the 10,000-unit mark in a single month, it still ranked high (fifth).** In terms of cumulative sales from January to November, the combination of Tesla, BBA, and Li Auto remains stable.**## Breakthrough in New Energy Vehicles Again

On the new energy vehicle market, the improvement of supply and the high oil price have resulted in a hot market. As the historical high oil price locks the electric price, it has driven the continuous strong performance of electric vehicle orders, although the November trends of new energy vehicles and traditional fuel vehicles were affected by individual regional epidemic prevention measures, most new energy manufacturers have accumulated good orders, coupled with flexible price promotion, which has significantly increased the number of leading manufacturers.

In terms of data, the retail sales of new energy passenger cars reached 598,000 in November, a year-on-year increase of 58.2%, a month-on-month increase of 7.8%, and an upward trend in trend for the period from January to November. The cumulative retail sales reached 5.03 million, a year-on-year increase of 100.1%.

Looking at the sales ranking of new energy manufacturers in November, BYD is in a leading position in both pure electric and plug-in hybrid sectors, while Tesla China and SAIC-GM-Wuling ranked second and third with 62,493 and 34,510 respectively; the first place in cumulative sales from January to November is still BYD, while SAIC-GM-Wuling and Tesla ranked second and third with a change of positions.

The market share of new forces in November slightly decreased (data was 12.7%), a year-on-year decrease of 7.3 percentage points. Among them, the sales of new forces such as NIO, LI, IM, and Leap Motor maintained strong year-on-year and month-on-month performance, especially the second-tier which had strong performance. This is also the advantage of the sub-market track.

Among the mainstream joint venture brands, North-South Volkswagen is strongly leading, holding 55% of the mainstream joint venture pure electric market share, which shows that Volkswagen’s firm electrification transformation strategy has yielded initial results, while other joint venture brands still need to work hard.

In terms of new energy vehicles, Hongguang MINIEV still tops the new energy vehicle list with 31,982 vehicles sold. The following four are all models under BYD, including Han, Qin, Dolphin, and Dolphin II, but the ranking of BYD Tang dropped two places compared to October, indicating fierce competition in the new energy vehicle market.

Due to the rapid product iteration and intensified competition in the industry, the impact of new models on delivery volume has weakened, and brands within the industry are also clearly competing with each other. As a result, the sales performance of each brand tends to diverge. Therefore, new faces like Changan Lumin, Dongfeng Fengshen E70, Kewei CLEVER, and Shenzhen Blue SL03 have emerged in November.

In terms of cumulative sales from January to November, Hongguang MINIEV, Han, Qin, Dolphin, and Model 3 firmly hold the top five positions, while other models are catching up in the following ranks, with no significant difference in sales between them.

Regarding new energy SUV models, three of the top five are taken by BYD, with the first place being the Song series that sold 63,636 units, a year-on-year increase of 223.1%; third place is the Yuan PLUS, which sold 20,204 units per month; and the fourth place is the Tang series, which sold 19,688 units in November, a year-on-year increase of 145.7%. The second place is Tesla’s Model Y, but there is a significant gap in sales compared with BYD Song series, with 52,424 units sold in November, a year-on-year increase of 126.8%.

Moreover, in the rankings, in addition to BYD and Tesla’s singing show, emerging brands such as WM Motor’s M5, Xpeng’s P7, Jinkou 001, NIO’s ES7, and NIO’s U have also entered the top ten.

Conclusion

Reviewing the first eleven months, due to the gradual penetration of new energy and the rapid development of export business, the spring of Chinese brands is accelerating. A “revolutionary” movement has completely transformed us from “who buys domestic cars” to “who doesn’t buy domestic cars,” and to some extent, it has accelerated the final “carnival” moment of some brands that rely on price cuts to increase sales, which cannot be sustainable. And as for “who will be the sales champion in 2022?”, the answer is actually very obvious.

“At this time, many netizens might think that there will be a shocking reversal in the end.”

Indeed, because the Spring Festival in 2023 is earlier than in previous years, the sales peak before the Spring Festival will start in December, plus the gradual easing of the epidemic situation, so this December will usher in the double BUFF of pre-holiday consumption and policies. But you should know that you work hard, and others also work hard.

For those who want to achieve a big reversal, I can boldly say here: “almost impossible.”

This article is a translation by ChatGPT of a Chinese report from 42HOW. If you have any questions about it, please email bd@42how.com.