Write | Xiong Xing

Edit | Wu Xianzhi

On November 10, NIO released its Q3 2022 financial report.

The data shows that as of the end of Q3, NIO achieved a revenue of 13.0021 billion yuan, a year-on-year increase of 32.6% and a quarter-on-quarter increase of 26.3%. In addition to measures such as adjusting vehicle prices in response to the rise in raw material prices in Q2, important factors in Q3 include market recognition of new models, timely adjustment of production lines to quickly restore delivery levels, etc.

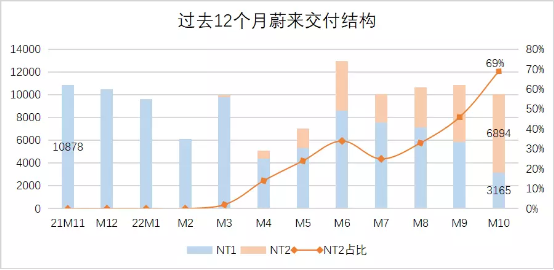

The delivery guidance for Q3 was 31,000 to 33,000 vehicles. NIO delivered 31,607 vehicles, basically achieving the guidance. The new NT2 model ES7 began delivery in August and the ET7 became the second best-selling model after the ES6 within the brand. As the ET5 began delivery, NIO’s second-generation product matrix gradually took shape, with a total of four SUVs and two sedans, continuing to maintain its advantage in the number of models among new forces in the field.

The adjustments in vehicle prices and the recovery of production and sales have not fully offset the impact of rising raw material prices. NIO’s overall vehicle gross margin was 20.9% in Q4 2021, 18.1% and 16.7% in the first two quarters of this year, and 16.4% in Q3, and has not yet returned to normal levels. NIO provided relevant explanations: mainly due to the increase in battery costs per vehicle, partially offset by the reduction in subsidies from user auto finance programs.

In Q1 of this year, NIO’s net loss narrowed to 3.8703 billion yuan, and the net loss in Q2 was 2.7575 billion yuan, affected by objective factors. In Q3, the net loss expanded to 4.1108 billion yuan, due to the increase in investment in R&D and marketing costs with the frequent launch of new models in this quarter.

After the new factory is put into production, it takes time to release production capacity, while more money is being spent on various things, such as layout in the mobile phone industry, overseas expansion, and production capacity adjustment before the large-scale production of NT2 platform.

“Short-term pain for long-term gain.” From NIO’s series of actions in Q3, it has chosen to use a long-term plan to shorten the period of pain for the company.

Taking the first step of sales growth

In September, ES7 sales reached 1,895 units in the second month of delivery, exceeding any monthly sales data of ES8 (1,412 units in September) this year. Objectively speaking, there are factors of pre-orders being released for achieving over 10,000 sales of the ideal L9, but nevertheless, the data for ES7 is not impressive compared to others.NIO still needs to face the production capacity allocation issue brought by the three new cars of ET7, ES7, and ET5. In the Q2 earnings call, Li Bin once said that the ES7 order volume is sufficient and mentioned that “delivery records will be broken every month from October to December”; in its Q3 earnings call, NIO provided a delivery guidance of 43,000 to 48,000 vehicles in the fourth quarter. This also indirectly confirmed that the delivery data during the production capacity allocation period in Q3 cannot fully reflect the actual situation of the products, and it takes time for the new car production to ramp up.

As “sub-flagship” models, they have rapidly surpassed the flagship model in sales, and their market recognition is evident. On the last day of Q3, with the delivery of the ET5, relatively low-priced products at the sedan level were covered in NIO’s product matrix, completing the process of “high-end covering low-end” internally, and the completeness of the process has been high.

As a result, NIO’s R&D cost in Q3 also reached RMB 2.9445 billion, which is relatively high. The problem of slow expansion progress relying on the existing product matrix and a long period of loss to profitability is expected to be completely resolved by the end of next year.

NIO’s decision to price its models high and then discount them to lower prices has determined that the models are born high-end and has refreshed the market’s psychological expectations for the price of new energy vehicles made in China. In Q3, NIO thoroughly went “low-end”.

In September, NIO’s third brand project was officially named “Ximalaya” and it is aimed at the entry-level market with a price of 100,000 yuan. The previous second brand “Alpine” targeted the 200,000-300,000 yuan market, combined with existing products priced over 300,000 yuan, NIO will cover high, middle, and low-end price ranges.

The three new cars and three brands will test NIO’s production capacity. In Q2, NIO signed an agreement with the Hefei government on the NeoPark Xinqiao Intelligent Industrial Park project, which has an initial investment of 50 billion yuan, an annual production capacity of 1 million vehicles and is used for the “Alpine” brand, including intelligent manufacturing and R&D.

The planned production start time is next year, which means that the increased expenses for NIO’s new brand product R&D and park construction will be amortized over the next few quarters from Q3 to completion and their costs will continue to rise.NIO, with an annual sales volume of more than ten thousand vehicles, plans to expand its production capacity to one million vehicles, targeting the mid-end market with prices ranging from 200,000 to 300,000 yuan. This may seem like a bold move, but in fact, it’s not. It took four years for China’s new energy vehicle penetration rate to increase from 2.8% in 2017 to 13.4% in 2021, and it reached 26% in the first nine months of this year. NIO is leaving some production capacity redundancy for its first sinking station to avoid duplicating the current situation, taking advantage of the accelerating market trend of penetration.

After all, if you miss this “fast train”, all car companies will gradually face the brutal competition of stock, which is not friendly to the relatively small new forces like NIO.

Ideal keeps launching new products, and XPeng has introduced SUVs priced above 300,000 yuan, among other factors. In this stage, the keyword is layout, and NIO’s battery swap feature inevitably requires a relatively large investment in pure electric and hybrid power in the early stage, especially with supporting services.

In July, at the NIO Power Day, NIO announced its three-year plan for a high-speed battery swapping network in 19 major city clusters across nine vertical and nine horizontal lines. This move clearly indicates its intention to pave the way for the three major brands, and to expand its energy storage business.

SAIC, Ningde, and two oil companies have entered the battery swapping track, which makes NIO not only a “teammate” but also a “competitor”: C-end battery swapping will no longer be lonely for NIO, and there may no longer be only NIO’s battery swap stations in the Sinopec sites. NIO’s “three-year plan” also has a certain defensive attribute.

Sinking requires volume, and production capacity and supporting services are important supports. In the third quarter, NIO’s financial data had bright spots and shortcomings, but horizontal expansion actions were quite frequent. The competition in China’s new energy track is getting more and more intense, and the entry of battery swapping giants has prompted NIO to choose to accelerate its growth. As for short-term gains and losses, it is not its top priority.

Looking back at Tesla’s development history, the Shanghai Super Factory undoubtedly has a milestone significance, and the Chinese market has become a turning point for Tesla’s return to profitability. NIO’s current series of actions can be seen as accumulating “quantity change” and preparing for the future. Going overseas is an indispensable part of the plan.

NIO Invests in the Future

NIO’s first offshore station is set in Norway, and it seems to be replicating past strategies. As of the first half of this year, Norway’s new energy penetration rate has reached 71%, continuing to lead the world. NIO is entering a relatively saturated market, but Norway’s per capita income and new energy infrastructure construction are all world-class.

NIO’s High-End Positioning requires High-Income Populations and a Strong New Energy Market Environment.

NIO has not disclosed overseas sales figures in its financial reports, but it is highly likely that sales are lower than those of BYD with 16,854 units. The latter has already left a brand impression on the European market with commercial vehicles, batteries, and other operations. In recent years, its brand has strengthened and its overseas business has expanded, making it no surprise that its sales are far ahead.

In contrast, NIO, which currently has operations in Germany, the Netherlands, Sweden, and other places, has a longer way to go. However, in terms of catering to European market users, NIO has caught up with the domestic market by moving from a “subscription model” to an open “buyout model”, thereby shortening the time it takes for the market to accept it as much as possible.

By increasing its expansion efforts in the second-largest new energy market in the world, NIO wants to establish a high-end image overseas as soon as possible. However, the second-generation model that NIO is promoting in Europe does not align with the local mainstream use of small and micro vehicles, which is clearly not the best “weapon”. Perhaps NIO’s mission does not lie here.

In the third quarter, NIO’s three major brand strategies were clear. In other words, the current actions of NIO’s main brand in Europe can be seen as an attempt to aim high, while the future second and third brands may be the backhand for sinking into Europe. NIO’s past tactics have been replicated, and last year, NIO surpassed its rival BBA in terms of sales of new energy vehicles in China, which confirms the feasibility of its tactics.

Next year, NIO will open NIO centers in Germany, the Netherlands, and other places. News of NIO being dismantled by Mercedes and sued by Audi has also been circulating in China. While expanding overseas, NIO has also encountered inevitable competition, maintaining its presence.

NIO has become the first domestic new force to go abroad, changing consumers’ stereotypes of domestic automakers, especially new forces.

Undoubtedly, this overseas strategy also has a positive effect on NIO’s domestic image, but the effect of boosting sales remains to be seen. After all, mature automakers have had to take this step in the history of the automotive industry. Global vehicle models are increasingly recognized by the market and are no longer “specially-made vehicles”.

Nowadays, the global penetration of new energy is accelerating, and foreign automakers are also accelerating their transformation to new energy. In response, domestic first-tier automakers such as BYD, Chery, Geely, and Great Wall are rapidly expanding their business in the domestic market and overseas. The living space left for new forces will become increasingly smaller. The third quarter can be seen as a critical point for NIO to accelerate its future layout.## NIO is Stepping Up Efforts in Power Battery Related Fields

In Q2, Li Bin stated that NIO was increasing its investment in power batteries. At the end of Q3, NIO subscribed to 12.6% of the shares of Australian mining company Greenwing Resources, amounting to AUD 12 million. Recently, NIO Battery Technology (Anhui) Co., Ltd. was established, integrating manufacturing, sales, and R&D.

By focusing on developing and manufacturing raw materials and batteries, NIO is intensifying its efforts to improve its self-built supply chain and mitigate third-party constraints. This is aimed at addressing the problem of fluctuating margins caused by the high cost of electric vehicles.

It is worth noting that in August, NIO Mobile Technology was established, with reports suggesting the launch of a mobile phone next year. NIO may have taken a preliminary step towards its “ecosystem,” rather than simply telling new stories in the saturated market, and it is possible that accessing its own product terminal chain may be its ultimate goal.

Amidst the accelerating “red sea” trend of new energy vehicles, no one can guarantee any unexpected turns of events. Therefore, taking proactive measures to prepare for the worst before achieving stability in production and sales is a necessary path for the maturity of a car company. It is more rational to proactively enter the “short and painful” cycle instead of being passively driven by the market.

This article is a translation by ChatGPT of a Chinese report from 42HOW. If you have any questions about it, please email bd@42how.com.