Special Contributor | Enjoyment

Editor | Zhu Shiyun

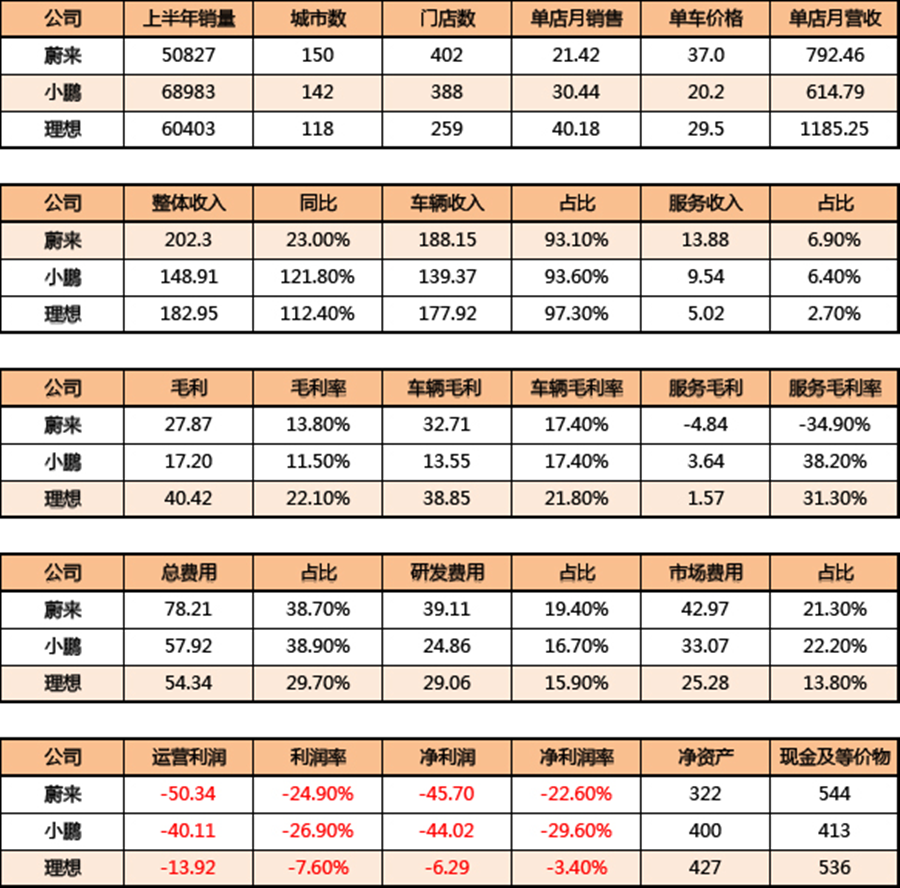

On September 7th, NIO announced a year-on-year increase in revenue of 21.8% to RMB 10.29 billion, reaching a new high of 2022 Q2 earnings. In addition, it gave a rather eye-catching Q3 guidance, with revenue reaching RMB 12.85 billion to 13.6 billion.

However, on the other hand, the core data is not optimistic: In Q2, NIO’s net loss belonging to shareholders was RMB 2.745 billion, a year-on-year increase of 316.4%. The per-car loss reached 140,000 yuan, still facing the state of “the more you sell, the more you lose”!

But NIO is not the only one not making money.

From financial data, neither NIO, XPeng, nor Li Auto has achieved a quarterly break-even. On the surface, Li Auto’s financial data looks the healthiest, followed by XPeng, while NIO’s performance is somewhat unsatisfactory.

However, from the post-financial report conference call, they all have ambitious and confident views on future development, no matter who they are.

But behind the prosperity of models, the top new forces also have their own hidden worries.

When Will High-end NIO Make Money?

Among the new car manufacturers, NIO’s products are the most high-end, with an average price per car reaching over RMB 400,000, surpassing Audi’s average price level of RMB 308,000 in China and comparable to BMW’s average price of over RMB 400,000.

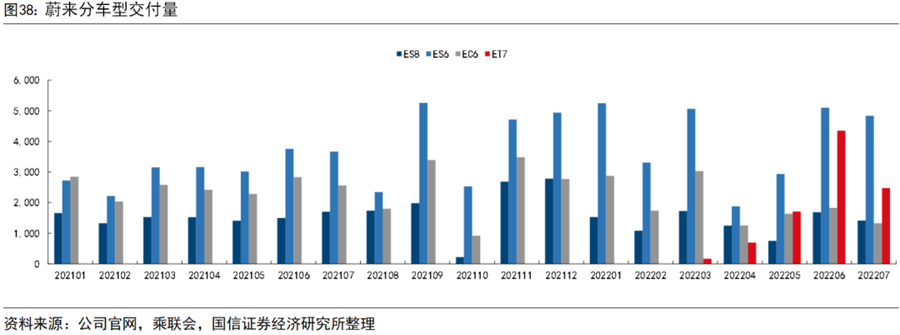

However, since the launch of the ES8 in 2018, NIO has introduced six products, including the ES8, ES6, EC6, ES7, ET7, and ET5, but none of them have achieved stable monthly sales of over 10,000 units so far.

Of course, for products priced at over RMB 400,000, it is not particularly easy to achieve monthly sales of over 10,000 units, and only BBA’s main products have been able to do so in the past.

However, with the commissioning of the new plant in Xinqiao (with a planned production capacity of 150,000 vehicles), NIO needs to launch more popular models.

And NIO’s approach to enriching its product matrix is not to directly explore the market of RMB 100,000 to 200,000, but to achieve price reduction through multi-brand.So there are two sub-brands, “Alps” and “Firefly”, plus the NIO brand that costs over 400,000 RMB, which together achieve full coverage in the mainstream passenger vehicle market. Within NIO, the three major brands are also seen as a ladder-like brand matrix, similar to Toyota’s “Suzuki, Toyota, Lexus.”

It is reported that “Alps” is positioned at the 200,000-300,000 RMB market segment. This brand has almost no presence of NIO, but provides similar services. Its products are comparable to Tesla’s Model 3 and Y, but 10% cheaper in price.

This brand will inherit NIO’s battery swap system (as well as its BAAS), and currently plans to use lithium iron phosphate batteries from BYD and China Aviation Lithium, already designated for usage. In the future, this will be an independently operated brand in terms of channels, communities, apps, and sales staff. The brand plans to achieve mass production of its first model as early as 2024.

On the other hand, “Firefly” is positioned in the 100,000-200,000 RMB market segment, and is a brand based on global market considerations. It has its own independent R&D system and will only be sold in the European market at the beginning.

It is reported that the first model will be an A0 entry-level sedan, positioned similarly to the BYD Dolphin, with a price range of 100,000-200,000 RMB, or about 20-30,000 euros. The new car will support battery swapping, be equipped with L2+ advanced driving assistance, but not include lidar or NOP.

Currently, the car is still in the research stage and will achieve mass production concurrently with the “Alps” brand in 2024. It is expected that it will undergo pilot sales in several European countries in the early stage but will not be sold domestically.

Many people have questioned, from the 100,000-200,000 RMB “Firefly” to the battery-swappable version of Model 3/Y at 200,000-300,000 RMB, and then to the NIO brand that costs over 400,000 RMB: NIO hasn’t achieved profitability even for its main brand, how can it suddenly manage so many brands? Can NIO handle it in terms of talent, service, R&D, and production capacity?

The larger issue is not how to manage multiple brands, but how to achieve positive quarterly profits as soon as possible. Even if NIO’s existing products sell 20,000 units per month, it still cannot achieve monthly profit and loss balance in the short term.

The biggest problem with NIO currently is brand dispersion, product matrix dispersion, lack of explosive products, and short-term difficulty in profit and loss balance.

Where can precision ideals expand?The Ideal Car Company precisely grasps the segmentation market among new carmakers. The market has to admit that Ideal’s product definition ability – Ideal ONE captured the smallest blue ocean market in the competition – the 6/7-seater family market, and achieved comprehensive sales leadership through ultimate cost-effectiveness (compared to joint venture or luxury brands at the same level and size). At its peak, Ideal ONE’s monthly sales almost exceeded the total sales of similarly-sized fuel cars in the same segment.

However, with the release of Ideal L9, the upgrade of Ideal ONE, the trailers of L8 (multiple versions), and the further information release of L7, we can find that Ideal has been eating the same segmentation market from the beginning to the end – simply put, it is rolling up its own coils.

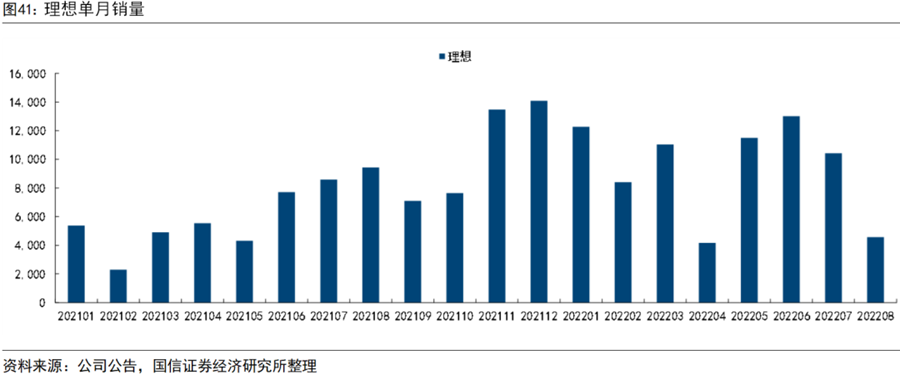

The substitution phenomenon caused by L9 after its launch has already demonstrated Ideal’s problem significantly. In July and August, lots of Ideal’s prospective customers turned to L9, and ONE was almost ignored, with a sales drop to 4571 units in August (including a small number of L9), down 56.14% month-on-month.

The rapid decrease of ONE’s customers directly caused Ideal to adjust its product release pace promptly, releasing the information of L8 ahead of schedule, and publicly announcing the news that ONE will be discontinued. This also caused great dissatisfaction among the customers who received their cars in August, especially those who were urged by sales to pick up their cars in the last two weeks of August. They not only faced the product discontinuation but also a discount of 20,000 yuan starting from September 1.

This directly led to many consumers organizing rights protection. On the one hand, this indicates the failure of consumer expectation management, but more importantly, it is the inevitable result of the product planning that too much centralized on the same segmentation market.

If we use Apple’s latest mobile phone products as an analogy, Ideal ONE = iPhone 13 pro, L9 = iPhone 14 pro, MPV = iPhone 14 pro max, L8 = iPhone 14 plus, L7 = iPhone 14. Essentially, these products are derivatives of a successful car model, and all face the mid-to-large 6/7-seater family market (the five-seater versions of L8 and L7 are essentially the same), so this market has become a highly competitive environment.After the release of L9, because the product outperformed ONE in all aspects, customers swarmed to L9. Once L8 is released, however, more consumers may realize that they don’t actually need a full-size SUV of 5.2 meters, and they probably will also swarm to L8.

The biggest risk of an overly centralized product matrix in a specific market segment is ideal.

Only when Ideal can come up with a completely new hit product that is completely different from L8/L9, can Ideal truly have the ability to create “sustained hit products.” Rather than, as is the current state, launching products based more on the CEO’s preferences and needs, which will truly achieve breakthrough sales of 300,000 units per year.

Who cares about XPeng’s intelligence?

Among the three new forces, XPeng is the most famous for its intelligence. In 2018, it launched the Xpilot 2.0 smart driving system, which has been implemented in the G3 model (priced at 149,800 – 187,800 yuan), achieving mass production of the L1 level adaptive cruise control system. In 2019, it launched Xpilot 2.5, which was first implemented in the P7 model (priced at 219,900-409,900 yuan), achieving mass production of the L2 driver assistance system. In 2020, it launched Xpilot 3.0, which first realized mass production of high-speed NGP on the P7 model. In 2021, it launched Xpilot 3.5, which implemented the laser radar version on the XPeng P5 model, also known as the P version (priced at 157,900 – 223,900 yuan).

The above three models are products targeting the mainstream market, but the problem is that none of these models can truly be called a hit product (monthly sales consistently exceeding 10,000 units). For NIO, it is difficult only because the overall average price exceeds 400,000 yuan. While Ideal, with an average price of only less than 250,000 yuan, has achieved consecutive monthly sales exceeding 10,000 units, but XPeng, whose average price is 35,000 yuan, hasn’t achieved sales exceeding 10,000 units for any of its models.

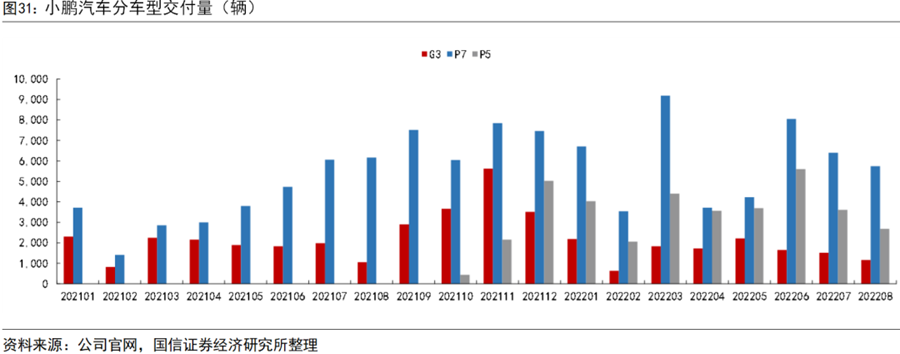

In August 2022, the delivery volumes of XPeng G3/P7/P5 were 1,155/5,745/2,678 units respectively. Among them, the sales of XPeng’s main model P7 had already fallen to 5 or 6 thousand units, and it has only been less than 6 months since the peak of 9,500 units.

While the P5 with advanced driver assistance system and laser radars, that XPeng had hoped for, has only sold around 5,000 units per month since its launch, and only 30% of sales were laser-equipped. This is much lower than XPeng’s original prediction, so XPeng revised its sales strategy in May by reducing charging benefits and instead directly providing different versions of Xpilot software and hardware capabilities. This has been reflected in XPeng’s Q2 report showing a decrease in vehicle gross margin of 1.34 percentage points.

XPeng has already proven that in the mainstream market of around 200,000 RMB, intelligent features can only be icing on the cake rather than game-changing. The group that is truly interested in paying for intelligent features is mainly concentrated in the high-end market of over 300,000 RMB. This is why G9, as XPeng’s next-generation product platform, is so important.

One of XPeng’s challenges is how to maintain overall manufacturing utilization rates as its factory capacity increases from 100,000 to 200,000 units with the upcoming Guangzhou and Wuhan factories totaling an additional 200,000 unit capacity. After all, such a significant fixed asset expenditure is dependent on the sales of each vehicle model to achieve amortization.

Intelligent features alone cannot bring XPeng to the forefront, combined with unclear product positioning, it becomes XPeng’s biggest risk.

Final Thoughts

At one point, the leading EV companies thought that the new energy vehicle industry was still in a period of “long-term dividend development with wide snowdrifts.” They believed they would not reach the “elimination race” until 2024. However, in just over two years, BYD and Tesla have already achieved the impressive feat of annual sales exceeding one million units. The entire industry is now rapidly accelerating, and an intense competition is on the horizon. Brands that have not yet launched or lack sufficient financial reserves will undoubtedly face enormous pressure.

For NIO, Ideal, and XPeng, although they each have unique features and strengths, they are still relatively prosperous while they are competing on their respective battlegrounds. However, since the debut of their new models this year, their product lineups begin to overlap and intersect.

For NETA and ZeroRun, even if they have surged in monthly sales to become the first or second among new start-up brands, they are still on the verge of collapse. With a cash reserve of only 5 billion RMB, manufacturing is too turbulent, and they may soon face bankruptcy if they stumble.

Without going public, they may sustain a loss for up to three years.

Even if they succeed in going public, it’s difficult to raise 30-40 billion RMB as easily as the top EV brands did in the previous market.

Weima Motors also submitted its IPO application three months ago with no significant progress.

(Regarding the IPO dilemma for second-tier new start-up brands, we will focus on it in the next article.)Expected to start in 2023, it will be a watershed not only for many new and old players, but also for NIO, Xpeng, and Li Auto. Slowly, a few will begin to pull away – and whoever can break through their own hidden worries first will emerge with a more independent market position.

This article is a translation by ChatGPT of a Chinese report from 42HOW. If you have any questions about it, please email bd@42how.com.