On May 1st and June 1st, everyone celebrated the festival delivery volume. However, the atmosphere was very different. In April, we faced the double constraints of supply and demand due to the impact of the epidemic. The automobile industry chain in the Yangtze River Delta was severely affected. Many OEMs and suppliers were shut down in the first half of the month. Consumer foot traffic also plummeted due to the lockdowns caused by the epidemic and economic downturn. According to data from the China Passenger Car Association, the wholesale sales volume of domestic passenger cars in April was only 965,000 units, a year-on-year decline of 43.2%, and a month-on-month decline of 48.1%. The national market has wholesaled 733,000 less cars compared to April of last year.

As some companies began to recover in mid-to-late April, the pressure on the supply side began to ease. Everyone began to look forward to whether the market in May can bring some positive signals. From the delivery results announced today by various new forces, the answer is yes.

Collective Warming Before Entering Summer

Among the manufacturers who announced their delivery volume on Children’s Day, 4 of them broke 10,000 units. It is worth noting that this number was 0 last month. In April, LI delivered a total of 9,087 units, the closest to breaking the 10,000 mark. Let’s take a look at each manufacturer’s data.

LI (Leading Ideal, Li Auto): 10,069 units

LI set a new monthly delivery record in May with 10,069 units, and the delivery performance increased by 215% year-on-year and 11% month-on-month.

It is worth noting that the currently available models for LI include T03, C11 and S01. Compared with May last year, while the year-on-year delivery volume has doubled, the product line has only added one C11 model, which is also the most expensive model in the LI product line. The month-on-month increase in LI’s delivery is due to the recovery of the production and supply chain, and partly due to the delivery of accumulated orders before the price increase. Overall, LI’s performance on the delivery side has steadily increased this year, accompanied by the market’s recognition of the LI brand. Recently, pre-sales of C01 and C11 are following the high-configuration and cost-effective route, but the pricing of C01 is more “normal” than the brutal price of C11 after various discounts. This also shows the confidence of LI in its own product power and brand strengths is “increasing compared to the same period”.

XPeng: 10,125 units# Market Performance of Three Newcomers

Among the three major new players, XPeng’s market performance in the past six months has been exceptionally outstanding, having won the monthly sales championship several times. However, XPeng only ranked second with a delivery volume of 10,125 units in May.

Compared with April, XPeng’s delivery volume in May increased by 12%, which seems not much, but it should be noted that last month, XPeng had the best data performance among the three major new players under the condition of running the dual factory. Among the 10,125 vehicles delivered this month:

- P7 delivered 4,224 vehicles

- P5 delivered 3,686 vehicles

- G3i delivered 2,212 vehicles

It can be seen that P7’s delivery volume has dropped compared to the XPeng of the 15,000 era, while the situation of P5 and G3i is relatively stable. Compared with the slight growth in May, XPeng’s recent trend is due to several more important information revealed in the Q1 2022 financial report:

- XPeng’s Zhaoqing factory resumed dual-shift production in mid-May;

- XPeng’s new orders in May have returned to pre-epidemic levels;

- XPeng will complete the multi-system switching of battery suppliers (cooperating with SKI and Xinyongda) in Q2.

In addition, XPeng officials also revealed that the user’s payment rate for advanced driving assistance has increased somewhat after the separation of hardware and software charges turned into unified charging, and all these factors will promote XPeng’s gross profit level to some extent.

NIO: 11,009 Vehicles

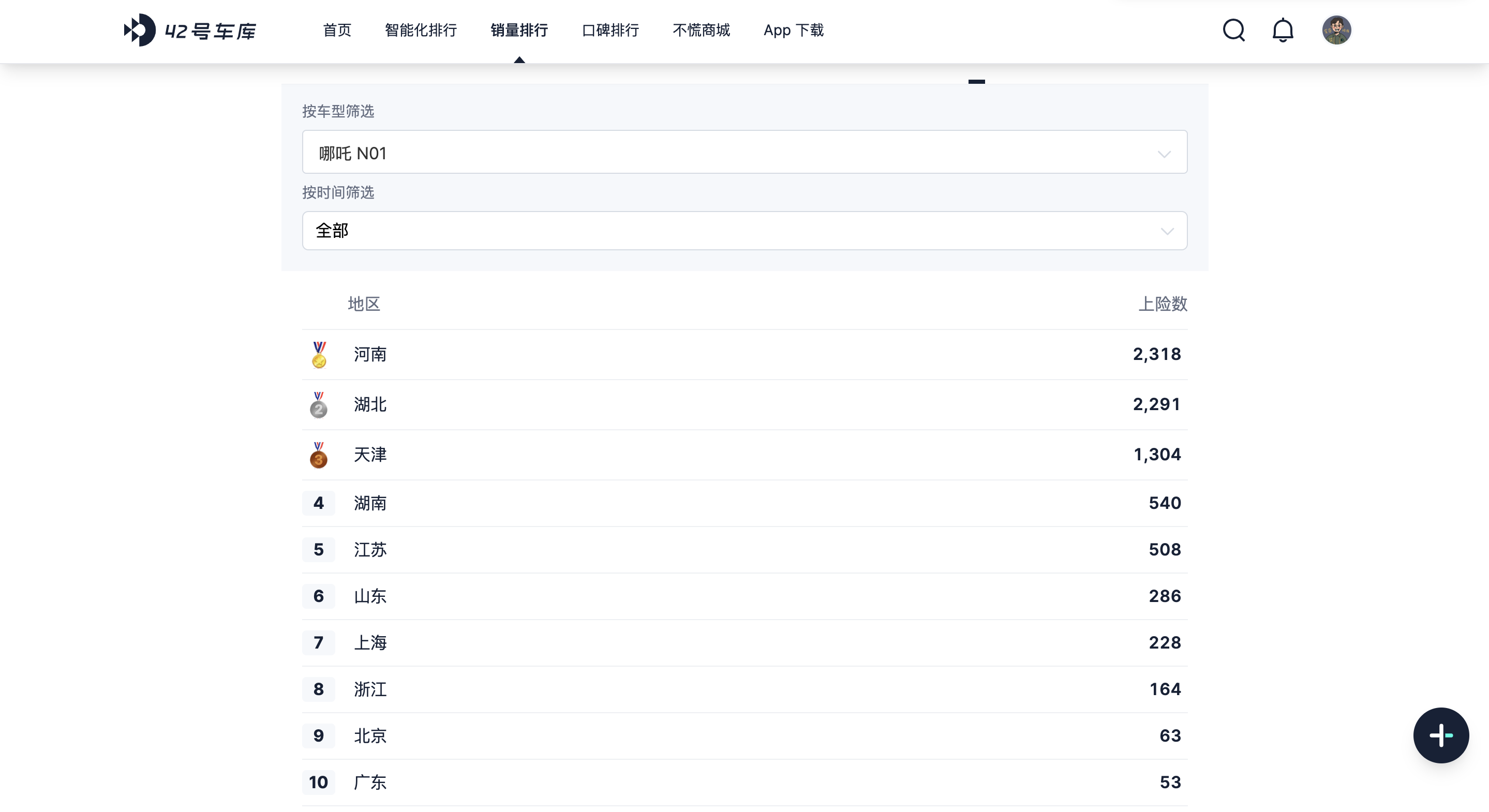

In May, NETA’s figure appeared again in the ten-thousand club. After seeing the poster, I believe many people will have two questions. First, what’s up with the green car in the picture?

It’s a little embarrassing to say, among the 11,009 vehicles delivered by NETA in May, there was no such scissors-style door NETA S, this new car has not yet been launched but will be released on June 6th. The reason why it appears in the poster mainly lies in the fact that it is NETA’s “face value model”. The second question is where did these more than ten thousand NETA cars go, as they seem to be seldom seen on the road?

Actually, I often see the NETA U in Shanghai, so I believe many people have seen it on the road but may not recognize this car. As for where it is sold, you can refer to the insured vehicle data on our 42 Garage website. The following three pictures show the top 10 provinces in terms of sales distribution of the three models of NETA U, NETA V, and NETA N01 from the past 12 months until April this year. Friends from corresponding regions can talk about their feelings.

Actually, I often see the NETA U in Shanghai, so I believe many people have seen it on the road but may not recognize this car. As for where it is sold, you can refer to the insured vehicle data on our 42 Garage website. The following three pictures show the top 10 provinces in terms of sales distribution of the three models of NETA U, NETA V, and NETA N01 from the past 12 months until April this year. Friends from corresponding regions can talk about their feelings.

After answering the two common questions on the NETA poster, let’s get back to the delivery volume of 11,009. NETA’s main sales are still in the two SUV models of NETA V and NETA U. Some people may question NETA’s industrial design and overall product strength for these models, but it must be said that these models are indeed mediocre. However, NETA’s main strength in penetrating the market is the ultimate price. The starting price of the NETA U, as a compact electric SUV with a not-so-small size, is less than 120,000 yuan, and the starting price of the NETA V is only 74,900 yuan. Models that can provide a similar range and space are generally much more expensive than NETA, which are reasons for B-side and C users to buy NETA. The reason why the sales distribution is not so focused on the Yangtze River Delta and first-tier cities is also one of the reasons why NETA was relatively less affected during the epidemic. In addition, June 1st is also the anniversary of the founding of NETA. This year is the fourth year of the company. After NETA stabilized its foothold with low-priced models in the past few years, it has also begun to develop upwards this year. The new car, NETA S, has already announced its appearance, interior, and various parameters, which have improved greatly compared to previous NETA models. Key content such as rear-wheel drive, long-range, and advanced intelligent driving technology all appear in this car. This easily reminds people of the XPeng P7 of the year.

XPeng P7 made the industry realize how much positive impact a good-looking and competitive car can bring to a brand and the market. Therefore, it is self-evident what expectations NETA has for NETA S now. Without talking much about the increase in sales, I believe that after NETA S is delivered, at least everyone can recognize this as a NETA car when they see it on the road.

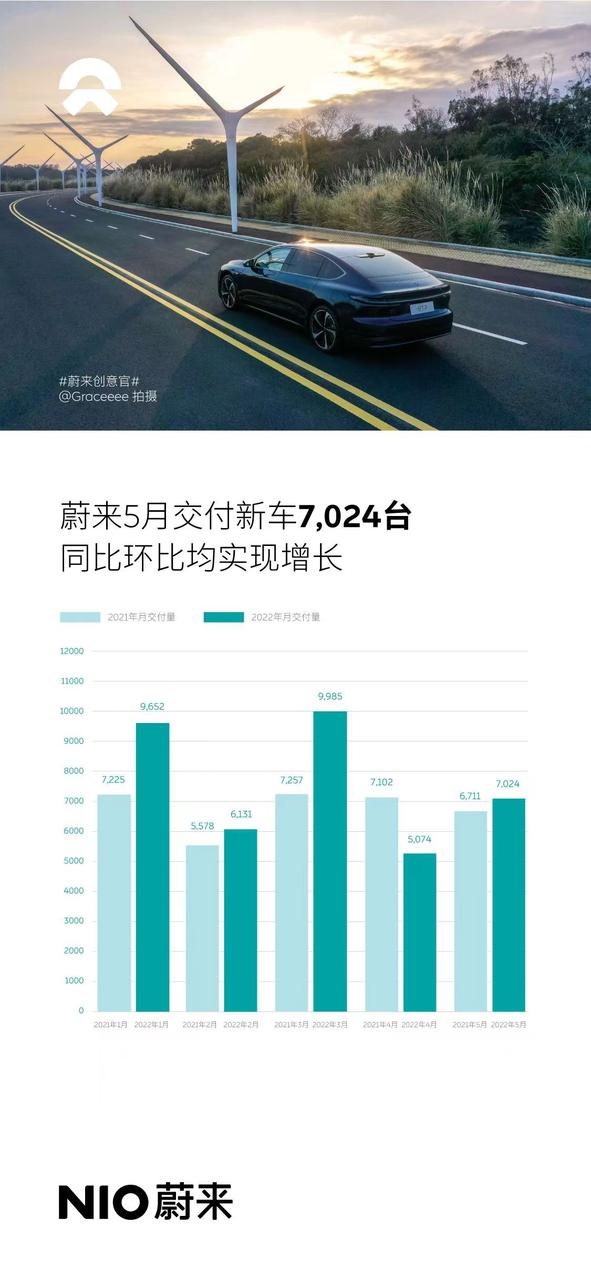

NIO: 7,024 vehicles# NIO’s May Deliveries Show Signs of Recovery

NIO’s deliveries in May saw a decent rebound compared to April, but overall it ranks last among the top three new forces in the industry. However, what I want to emphasize is that NIO’s delivery performance in the past few months is not particularly surprising or pessimistic, as it is a relatively normal stage performance in terms of products.

Let’s take a look at the delivery volume of NIO’s models in May:

- ES6: 2,936 units

- EC6: 1,635 units

- ES8: 746 units

- ET7: 1,707 units

ES6 is still the best-selling model among NIO’s product line, but this month’s second-in-command has changed from EC6 to ET7. The factors such as the pandemic and suppliers affecting the production side are one aspect, and the more important reason is actually due to the new car – the impact of NIO’s early announcement of the upgraded 866 model and the release of ES7 on the current 866 model is undoubtedly huge. According to NIO’s original plan, ES7 was supposed to be released at the Beijing Auto Show in April, and in May, the upgraded 866 model and the hardware upgrade of the current 866 model were to be pushed. From the perspective of consumers, these four products have a high degree of overlap with the existing models on sale, the sudden outbreak of the pandemic not only delayed the product launch rhythm, but also prolonged the observation period for prospective buyers. Therefore, NIO’s deliveries will still have a painful period in the next while, while the ET7, which is still in the stage of ramping up production capacity, can contribute to NIO’s new and old products, allowing for more buffer time in the transition period, but the real high tide of NIO’s deliveries is still waiting for the large-scale delivery of ET5.

Deliveries Target: 11,469 Units

In April, Ideal Vehicle’s deliveries ranked last among the top three new forces, and the severe supply problems caused by the pandemic in the Yangtze River Delta region were the main reason. In May, Ideal’s deliveries returned to the 10,000 mark, and once again rose to the top spot in the monthly deliveries among the top three new forces in two years.

The swift rebound of production undoubtedly achieved significant improvements, but even though it broke 10,000, Ideal’s official statement today still indicates that production at the Changzhou factory has not fully recovered, with some implications for delivery in its words. On the demand side, the situation for Ideal and NIO this time is somewhat similar to the month when they delivered over 10,000 vehicles for the first time last year: the short-term order growth before the price increase, and the order backlog caused by supply in the first month, helped drive the delivery performance in May. However, the Ideal ONE still has a strong competitive advantage at its price point, with relatively smaller impacts on sales. But as family-oriented products like the L9 and DENZA D9 continue to enter the market, some users at the edge of the price range in Ideal ONE’s target audience will shift. For Ideal, the real challenging period should be between the release and delivery of the L9.

The swift rebound of production undoubtedly achieved significant improvements, but even though it broke 10,000, Ideal’s official statement today still indicates that production at the Changzhou factory has not fully recovered, with some implications for delivery in its words. On the demand side, the situation for Ideal and NIO this time is somewhat similar to the month when they delivered over 10,000 vehicles for the first time last year: the short-term order growth before the price increase, and the order backlog caused by supply in the first month, helped drive the delivery performance in May. However, the Ideal ONE still has a strong competitive advantage at its price point, with relatively smaller impacts on sales. But as family-oriented products like the L9 and DENZA D9 continue to enter the market, some users at the edge of the price range in Ideal ONE’s target audience will shift. For Ideal, the real challenging period should be between the release and delivery of the L9.

JiKe 4,330 vehicles, WM Motor 5,006 vehicles

JiKe reached a new monthly delivery high in May, with a score of 4,330, doubling on a month-on-month basis. After months of decline, it finally had two consecutive strong gains.

According to feedback from JiKe car owners in the Garage JiKe group, some car owners who placed orders in December received their cars in May, while new users who placed orders with sales channels still need to wait for several months for their cars to be delivered – production capacity is still a major restriction for JiKe’s current delivery. Thanks to the price hike announcement, JiKe added over 12,000 orders last month. And even after the price increase, JiKe 001 still has excellent value for money, stability and driving experience compared to other options at the same price. After half a year of market validation, JiKe’s reputation has also begun to improve as car owners continue to increase and with several OTA upgrades. For a new brand, as user reputation exceeds the turning point, obstacles to spreading and growth resistance will decrease. Apart from production capacity, another unclear issue affecting JiKe is assisted driving. If the OTA upgrade can be completed as soon as possible, it will make up for JiKe 001’s biggest shortcoming. WM Motor M5’s sales performance in May broke 5,000, and the only currently available product, WM Motor M5, took only 87 days from delivery to selling 10,000 units. These two data points show Huawei’s terrifying marketing ability in the car field. Even the just-launched WM Motor has delivered more than JiKe’s cars for three consecutive months.

If we break down the performance of the WENJIE M5 achieved in May, Huawei stores played an indispensable role. Huawei broke the ground by bringing cars into mobile phone stores for sales, which has been reflected in the actual sales feedback that the majority of users who purchase WENJIE M5 at Huawei stores are Huawei users. This is definitely a traffic resource that any new brand envies.

In fact, Huawei had tried this approach when promoting the Ceres SF5. The reason why the SF5 failed to gain popularity while the WENJIE M5 succeeded lies mainly in product strength. Firstly, after a full-scale “decoration” of both the interior and exterior of the WENJIE M5, it now looks nothing like the SF5 and has a greatly reduced sense of cheapness, making it is no longer a weakness at the same price point. Secondly, Huawei’s “in-car smart ecosystem” creates a user-friendly “smart car” experience, which has already become a standardized advantage for the WENJIE M5. Finally, as a range-extended electric vehicle, the M5 possesses the low-threshold characteristic required to compete with gasoline vehicles in the current Chinese market. Additionally, the mid-size range-extended EV market with a price below RMB 300,000 is currently in high demand due to the lack of competitors. With the backing of Huawei and the personal influence of Richard Yu, the delivery performance achieved in May by the WENJIE M5 was within both expectations and feasibility. 5,000 monthly sales will not be the climax for this car. Furthermore, WENJIE will launch a 3-row SUV, the M7, which will compete directly with the IDEAL ONE. However, if we remove the last advantage mentioned above, the competition becomes a different story. If one wishes to replicate the success of the M5, they will need to make bold pricing decisions.

Summary

In summary, in May, regardless of whether they performed well or poorly in April, all manufacturers saw an increase in delivery numbers for the month, with some companies that had strong demand and obvious improvements in the production end having returned to pre-pandemic levels. The visible rebound performance has given the market valuable confidence. The recovery of the automotive industry’s production and supply side is making steady progress. Another concern raised by the more than two months of COVID-19 in Shanghai is the recovery of market demand. The decline of consumer desire due to the economic downturn may be the more lasting “side effect” of this epidemic on the auto market. Regarding this issue, we can look at the government’s recent efforts to promote sales.

Government leads promotionAt the beginning of the article, it was mentioned that the wholesale sales of domestic passenger cars in April decreased by 733,000 compared with the same period last year. Looking back at the Chinese auto market, the government has always attached great importance to auto consumption and has introduced bonus policies several times to promote consumption and bring the market back on track during critical times. In response to the plunging caused by the pandemic, the government quickly made positive responses. Guangdong took the lead on April 28th and issued the “Several Measures of Guangdong Province to Further Promote Consumption”, in which the most direct and effective car purchase subsidy for auto consumption was introduced: a subsidy of 10,000 yuan for scrapping old cars and buying new energy vehicles, and a subsidy of 8,000 yuan for replacing old cars and buying new energy vehicles; a subsidy of 5,000 yuan for scrapping old cars and buying fuel cars, and a subsidy of 3,000 yuan for replacing old cars and buying fuel cars. For new and additional users, Guangdong Province provided a subsidy of up to 8,000 yuan for the new energy vehicle models in the province’s promotion catalog for old-for-new replacement from May 1st to June 30th. From May to June, Guangdong Province increased the quota of small passenger car license plates by 30,000, and Shenzhen increased it by 10,000. One month later, on May 23rd, the Shenzhen government continued to increase its efforts in this policy and issued the “Several Measures of Shenzhen City to Promote the Continuous Recovery of Consumption”, the first of which is to “encourage auto consumption”. Compared with the policies of Guangdong Province, the efforts made by Shenzhen are obviously better:

- Provide subsidies of up to 10,000 yuan per unit for personal consumers who purchase new energy vehicles that meet the conditions and have been licensed in Shenzhen;

- Add 20,000 general small car indicators for those who participated in the 60th or higher period of the lottery system and did not win. The applicants who obtain indicators are required to purchase fuel vehicles or new energy vehicles that meet the conditions, and a subsidy of up to 20,000 yuan is offered to applicants who purchase new energy vehicles;

- Relax the application conditions for hybrid indicators and allow individuals who have one registered small car in Shenzhen to apply for hybrid car indicators;

In addition to the personal consumer market, the Shenzhen government also encourages companies to purchase new energy commercial vehicles. For companies that purchase new energy passenger cars, a subsidy of up to 50,000 yuan per unit is provided, with vehicle models including passenger transport, garbage cleaning vehicles, and port trailers. Other regions have also begun to introduce promotional policies for auto consumption.From June 1st to August 31st, Zhengzhou announced that nearly 20,000 car consumption vouchers will be issued, which can be used to purchase new cars and obtain license plates within Zhengzhou City’s automobile sales enterprises, with a maximum amount of 8,000 yuan. On May 27th, Qingdao announced that during the “Yihui Qingdao” car consumption event from May to October, individuals who purchase cars and obtain invoices from May 22nd to June 30th and complete the registration formalities by August 31st will receive car consumption vouchers. For individuals who purchase new energy vehicles priced above 200,000 yuan and complete the registration formalities, a subsidy of 6,000 yuan will be provided; for those in the 100,000 to 200,000 yuan price range, a subsidy of 4,000 yuan will be provided; for those below 100,000 yuan, a subsidy of 3,000 yuan will be provided. For fuel vehicles, the corresponding subsidies are 5,000 yuan, 3,000 yuan, and 2,000 yuan.

On May 29th, Shanghai issued the “Shanghai Accelerating Economic Recovery and Revitalization Action Plan”, which indicated that Shanghai will gradually reduce the purchase tax for passenger cars in stages according to national policies, and will increase non-operating passenger car license plates by 40,000 this year. An additional subsidy of 10,000 yuan will be provided for individuals who scrap or transfer a small passenger car registered in Shanghai and purchase a pure electric vehicle.

Other local policies in Shandong, Jiangxi, Hubei, Shenyang, Yiwu, and other places are mainly subsidy-based promotions for new energy vehicle consumption, and are not fully summarized here due to time constraints. On May 31st, the Ministry of Finance issued a nationwide automobile consumption tax reduction policy, reducing the purchase tax by half for passenger cars priced below 300,000 yuan (excluding VAT) and with a displacement of 2.0 liters or less from June 1st to December 31st. If calculated at a VAT rate of 13%, all models with a invoiced price below 339,000 yuan and a displacement of 2.0 liters or less will qualify for the tax reduction. After the purchase tax is reduced by half, the maximum savings is 16,950 yuan.

It is estimated that the China Association of Automobile Manufacturers’ policy will result in an increase of 2 million cars, and will have a good promotional effect on HEV hybrid models. Such a large-scale, low-threshold and multi-layered car market promotion policy is rare in the history of the Chinese car market. Everyone understands the reason: the tight supply and demand situation in April has been alleviated since May as supply and logistics have gradually recovered, but to make the market fully recover, demand stimulation is still needed. The market has inertia, and although the “head” of the May car market recovery has risen, what was actually completed was a backlog of orders. The promotion policy quickly entered and will continue to boost the recovery of the car market in June and beyond. At the same time, the rising fuel prices on the consumer side seem to have conspired to boost the heat of the new energy market. In short, the policies and traffic are in place.

In conclusion

According to the China Association of Automobile Manufacturers, the estimated retail sales of passenger cars in May will be 1.32 million units, a year-on-year decrease of 19%, but it has recovered significantly from the previous month of April. In addition to favorable factors such as production, supply, logistics, and policies, the stock market’s rebound in May has also indirectly catalyzed the subsequent rise in the automotive market. When the overall momentum returns to normal, those heavyweight new cars delayed by the epidemic still have the ability to bring new growth and vitality to the new energy market, accelerating the continued climb of penetration rate and returning to healthy supply and demand.

This article is a translation by ChatGPT of a Chinese report from 42HOW. If you have any questions about it, please email bd@42how.com.