Zero Run submitted its prospectus to HKEX on the evening of March 17th. The joint sponsors are CICC, Citigroup, J.P. Morgan, and CCB International.

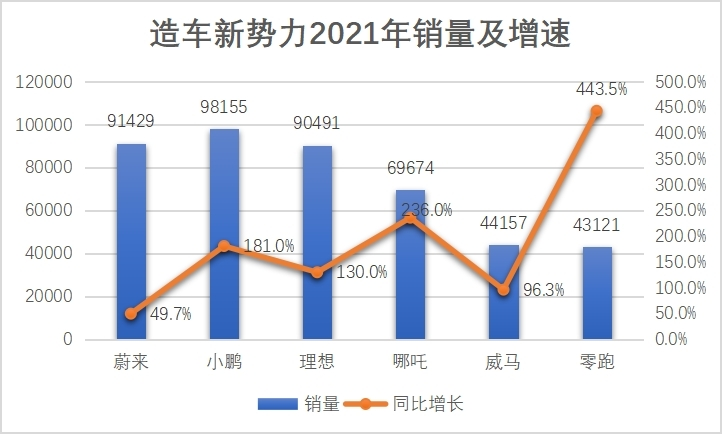

This is the fourth new car manufacturer to go public after NIO, and the first mid-market new car manufacturer to go public. However, according to last year’s sales data, Zero Run’s delivery volume was only at the bottom of the mid-market force, with low absolute values, hence the growth rate was fast.

Comparatively, mid-market forces did not have an easy time in the early stage. WM Motor and NIO were in a dilemma in the B-side market, while Zero Run’s first car model S01 had average sales.

However, Zero Run’s transformation was faster and more aggressive, starting in July 2019 with the delivery of S01, followed by T03 in May 2020 and C11 in October 2021, which was basically a one-year-one-car rhythm where its second A00-class electric car captured the dividend of micro-cars, quickly boosting Zero Run’s delivery volume.

In its prospectus, Zero Run also mentioned that “in terms of delivery volume, Zero Run is the fastest-growing company among China’s leading emerging electric vehicle companies.”

Of course, sales supported by micro-cars cannot stand firm in today’s new energy market. After going public, Zero Run may be able to continue to invest in the current competition, but its shortcomings will also be amplified. To gain capital recognition, Zero Run still has many problems that need to be solved.

In addition, Zero Run’s IPO at this time can be said to have missed the high premium era of the capital market for new energy. As of July 2020, when Ideal Automobile went public, Li Xiang, the founder, said it was the most successful IPO in China’s automotive industry. At that time, Wall Street gave high valuations to the new energy track where Tesla and NIO were located, and Ideal Automobile soared by 43% on the day of its IPO. One month later, XPeng Motors went public, and its stock price rose by 41% on the first day.

After the IPO, all three companies of NIO, XPeng, and Li Auto completed new fundraising in their respective ways, and their cash reserves reached the level of 30-50 billion yuan.

Today, compared to their highest stock prices, the three companies have seen a significant decline, and the high valuations of new energy are no longer there. Zero Run will inevitably have to sacrifice more equity to complete fundraising. The complexity and uncertainty of the macro environment will also make most capitalists become cautious, making it more difficult to achieve the predetermined fundraising target.

Casting a Wide Net, Catching More Fish

For the micro-car market, it has always been the favorite of traditional car companies. There are neither too many intelligent needs nor too many supply chain issues, and it can quickly create a high cost-effective product to occupy the market, as seen in Hong Guang MINI, Little Ant, and Ice Cream cars.These models also have fatal flaws. In the case of low profit, they are vulnerable to the impact of the supply chain and may incur losses. For example, the rapid rise in upstream raw material prices this year has led to the suspension of orders for ORA Black Cat and White Cat.

In addition, compared to traditional car companies, the disadvantage of relying on micro-cars to obtain new energy points to support their own large fuel vehicle system has been infinitely reduced. However, in new forces, this “superior” condition clearly does not exist.

Coupled with the poor debut of the first model, it is also expected that ZERORUN’s “bloody listing” will happen.

According to the prospectus, in 2021, ZERORUN’s revenue was 3.132 billion yuan, a year-on-year increase of 396.4%, but the net loss expanded as well. The net profit was -2.846 billion yuan, a year-on-year increase of 158.7%. The three-year gross profit margin was -95.7%, -50.6%, and -44.3%, showing a trend of gradual increase. However, compared with NIO and Ideal’s gross profit margin of about 20%, profitability is still a distant hope.

To improve the gross profit margin, getting rid of mid-to-low-end cars is the primary factor. ZERORUN also clearly stated in the prospectus that it will mainly focus on China’s mainstream new energy vehicle market with a price range of 150,000 to 300,000 yuan. That is, the T series and S series, and no new products should be launched in the future.

In October last year, the third model of ZERORUN, C11, was officially delivered. As a mid-size SUV with a price range of 15.98-19.98 million yuan, it performed well in terms of order data and had received over 22,000 orders by the end of 2021.

However, from the delivery side, C11 is not yet ZERORUN’s main model. A total of 3,964 C11s were delivered in the first three months of last year, while the insurance data for January and February of this year were 2,103 and 1,144 respectively.

On the one hand, C11 is still in the capacity ramp-up stage. At the same time, since August of last year, T03 is no longer produced by outsourcing, but is produced in the Jinhua factory. The planned production capacity of the factory is 200,000 per year, and ZERORUN also plans to build a new production base in Hangzhou to further expand its production capacity. On the other hand, the first quarter is traditionally a low season for car sales, which led to a decline in overall sales data. Therefore, the strength of C11 still needs to be verified by subsequent market reactions.

In addition to C11, the ZERORUN prospectus revealed that a mid-to-large-sized sedan C01 will be released in the second quarter of next year, and delivery will be realized in the third quarter.C01 and C11 are built on the same platform, with a body length of about 5 meters, equipped with Leapmotor power and a 90 kWh battery, NEDC700 km, zero to 100 km/h acceleration within 4 seconds, and will also adopt the design of battery-chassis integration (CTC).

According to the Leapmotor 2.0 strategy, C01 will also be in the price range of 150,000 to 200,000 yuan and will directly compete with XPeng P5. From the revealed body size, endurance, and performance data, perhaps C01 will adopt the same strategy as C11, taking high cost performance as its main selling point.

According to the prospectus, Leapmotor plans to launch 8 new models at a rate of one to three models per year by the end of 2025, covering cars, SUVs, and MPVs of various sizes.

Unlike most new forces’ early strategies of deepening in SUVs, Leapmotor has already covered four types of vehicles: coupes, mini-electric cars, mid-size SUVs, and soon-to-be-launched mid-to-large-size sedans, as well as MPVs. Through different price points and vehicle types, Leapmotor radiates its brand to every market as much as possible, making it the car company with the broadest involvement besides BYD.

The advantage is that it can quickly make up for the problem of weak brand perception, while avoiding the situation of left-right hand competition like ES6 and EC6 and improving overall sales.

The disadvantage is that as a new force stepping into multiple markets too quickly, it may be difficult to accurately grasp user needs.

Zhu Jiangming once said in an early interview that he didn’t even know that making cars required qualifications due to his lack of experience, and the “silence” of the first product S01 also proved the importance of laying a solid foundation, as Great Wall Motor’s decades-long focus on pickups and SUVs is also a good approach.

The premise for casting a wide net to catch fish is to be an experienced fisherman.

Boosting R&D and Expanding Channels

Among new forces, XPeng was the first to propose “full-stack self-reliance,” and Leapmotor has further proposed “full-range self-reliance.”

Zhu Jiangming said in a media interview that full-range self-reliance refers to the entire intelligent driving system and intelligent electric drive system being developed in-house from hardware to software. The hardware structure is built from the resistance level, and the software is written from the code level.

“Other new car makers rely more on third-party hardware, and they mainly do applications and algorithms, not hardware.”

Zero Run believes that its self-developed capability and vertical integration can improve its R&D efficiency and reduce costs. As of the end of last year, R&D personnel accounted for 33.9% of the 3190 employees of Zero Run.

However, according to financial report data, Zero Run’s R&D investment is not strong in absolute value. The R&D expenses in the past three years were 358 million yuan, 289 million yuan, and 740 million yuan respectively. In contrast, the three companies, NIO, XPeng, and Li Auto, had R&D expenses of 11.93 billion yuan, 12.64 billion yuan, and 8.89 billion yuan, respectively, only in the third quarter of last year. Therefore, Zero Run’s three-year R&D investment is only slightly higher than the single quarter expenditure of the top competitors.

Among them, capital factors occupy the dominant position. According to data from Qichacha, since its establishment, Zero Run has completed seven rounds of financing, with disclosed financing amounts of about 10 billion yuan. As of January 31, 2022, Zero Run’s current assets were RMB 6.332 billion yuan. According to the third-quarter financial report data of XPeng, NIO, and Li Auto, the three companies hold about RMB 40 billion yuan in funds each.

At the same time, Li Bin also raised the threshold for making cars at the end of last year. “Making cars requires a reserve fund of 20 billion yuan. A few years ago, I said that 40 billion yuan is necessary. Nowadays, it may not be possible to build a car with less than 40 billion yuan.”

On the other hand, at the beginning of making cars, Zero Run spent three years developing its own intelligent driving chip, the Lingxin 01, which has now been installed in the latest model C11. However, Zero Run also encountered the same embarrassing situation as smartphone manufacturers. Although Lingxin 01 had higher computing power than Mobileye Q4, which was released in 2018 when it was launched, it is not enough for today’s standards.

At the same time, the chip requires continuous investment of funds and time, which is difficult for a new force that has not yet generated positive cash flow.

Perhaps realizing the main direction of R&D investment, Zhu Jiangming stated in an interview last year that Zero Run had no plans to develop a new chip after Lingxin 01, and there were already many options on the market. This IPO prospectus should naturally not include intelligent driving chip plans.

By sorting out the main R&D directions, Zero Run can also reserve more “surplus” in the competition.

As R&D investment continues to increase and product lines continue to improve, Zero Run also needs to continue to improve its offline marketing network.

Currently, Zero Run adopts a sales model similar to XPeng, combining directly operated stores with channel partner stores. As of December 31, 2021, Zero Run had 23 directly operated stores and 286 channel partner stores.

In fact, Zero Run conducted a large-scale channel expansion last year, from 95 at the beginning of the year to 291 at the end of the year, representing a year-on-year growth of 215.4%.

Compared with XPeng, which is in the same price range, although Zero Run seems to be equally matched, there is a serious “unbalanced allocation” problem. According to XPeng’s third-quarter data last year, it had 167 directly operated stores and 104 authorized stores, which was more balanced.We have noticed that LINGPAO is continuously consolidating its third-party channel construction, and has rapidly expanded its sales network. Unfortunately, the disadvantage in the number of directly-operated stores may affect two aspects, incomplete collection of user information and insufficient control of user demands. Currently, it is clear that LINGPAO intends to climb uphill, and building directly-operated stores may be its main task this year.

Conclusion

Data shows that new energy vehicle sales in the price range of 150,000 to 300,000 CNY accounted for 39% in 2021, while those below 150,000 CNY and above 300,000 CNY accounted for 10.4% and 50.6%, respectively. As the penetration rate of new energy continuously increases, the new energy market will gradually change from a “barbell-shaped” structure to a more popularized one.

Most of the mid-tier players are also in this price range, and LINGPAO has already taken the lead, while among the head players, only Xpeng is in this price range for now.

However, under limited funding, the mid-tier players are all facing the same problem: whether to focus more on research and development or marketing.

We don’t know how the car companies preparing to go public will make their choices, but the listing of LINGPAO is like a charging signal, accelerating the market competition.

This article is a translation by ChatGPT of a Chinese report from 42HOW. If you have any questions about it, please email bd@42how.com.