Before the insurance data came out, I did some sorting out of the August data from the China Association of Automobile Manufacturers:

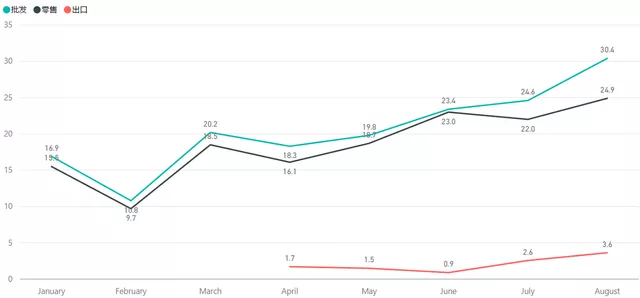

In August, the wholesale volume of new energy vehicles reached 304,000, and the wholesale volume of new energy passenger vehicles from January to August reached 1.64 million units.

In August, the retail sales of new energy passenger vehicles reached 249,000 units, which is a relatively strong figure.

In August, the number of new energy vehicles exported reached 36,000.

Based on this data, we can take a closer look at the situation of each company. What’s behind these good figures for August?

Interpretation of the Wholesale Increment

It is important to understand which part actually contributed to the increase.

From the data, plug-in hybrid electric vehicles (PHEV) increased from 47,000 to 55,000 units, with an increase of 7,339 units in August. The increase in battery electric vehicles (BEV) was mainly from 200,000 to 249,000, with an increase of 48,728 units.

Interpretation of Data According to Vehicle Classification

If we sort the data by different vehicle classifications, the largest change is that the A00-class vehicles increased from 61,490 units to 82,889 units, an increase of 21,399 units. According to the data classification provided by automakers, SAIC-GM-Wuling’s August production was 43,783 vehicles, an increase of 16,436 vehicles from July’s 27,347 vehicles. Therefore, although SGWM accounted for 52.8% of the A00-class market share in August, their increase accounted for 76.8%, and Wuling’s output directly boosted the growth data.

The A0-class vehicles also increased from 29,258 to 36,729 units, an increase of 7,471 units. Compared with that, the A-class increment still kept up the pace with 8,905 units, while the B-class increment was 11,304 units. The only decrease was in the C-class vehicles, which decreased by 351 units.

Looking at the data broken down by brand, most of the B-class increment comes from Tesla, which coincides with this data. Moreover, after subtracting Tesla’s export of 31,379 vehicles this month, the B-class increment is almost equivalent to Tesla’s sales in China.

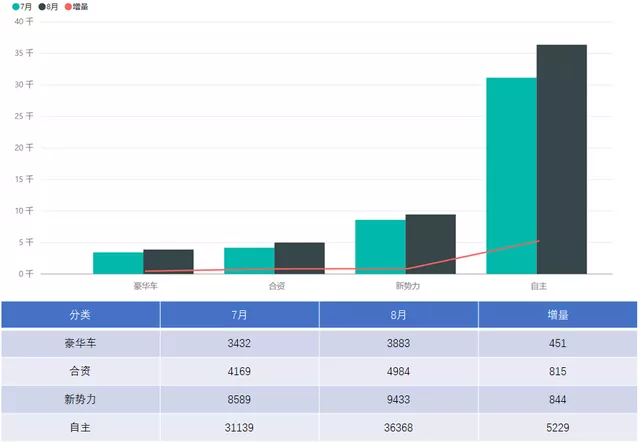

Comparison between July and August data

According to the chart below, the increase in August mainly came from the data added by independent car companies (33,500 units) on A00, A0, and A level cars. Pure electric vehicle models from joint ventures only increased by 3,681 units, while new energy vehicle start-ups remained almost unchanged. Independents added 33,555 units, and if we exclude the 16,400 units from Wuling, this increase amount is only 16,400.

The published data shows that SAIC passenger cars and GAC Aion both remain relatively stable, which also adds stability to the A-level market.

If we look at PHEV, it can reflect the problem more accurately.

In August, the overall increase in PHEV is mainly attributed to BYD’s models. The increase in other models can be ignored.

Conclusion: I feel that in August, Wuling, which was not affected by the shortage of ESP, contributed to the overall sales volume (16,000 units), while BYD’s increase of 10,000 units is basically the difference in retail sales. Tesla exported 30,000 units and sold over 10,000 units domestically, which also increased the overall batch sales data to 300,000 units. In fact, chip supply still greatly affected the data in August, but the 80,000 A00-level units already accounted for more than one-third (36%) of retail sales. If this trend continues for the next three months, the ratio of A00-level unit sales will further increase.

This article is a translation by ChatGPT of a Chinese report from 42HOW. If you have any questions about it, please email bd@42how.com.