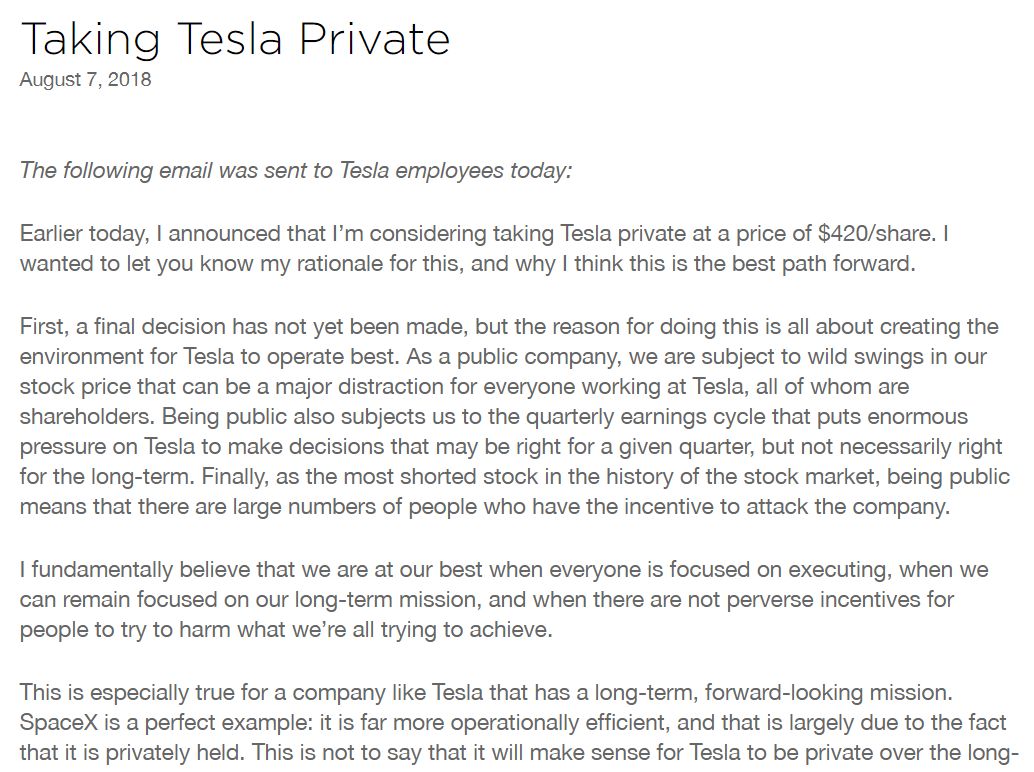

Elon Musk announced today a news even more significant than Tesla’s earnings report – I plan to privatize Tesla at a price of $420 per share, and the funds have been secured.

As the announcement was made on Twitter, many people remain skeptical. Moreover, due to Elon’s past actions (he once held a Tesla bankruptcy sign with tears in his eyes, leaning against a Model 3, announcing Tesla was completely bankrupt, which turned out to be an April Fool’s joke), most people adopt a cautious attitude towards privatizing Tesla.

Given Elon’s long-standing, fierce confrontation with Tesla shorts, many people still believe that this move is more likely to be a mischievous attempt to hit back at short sellers, ignoring his full disclosure of considerations.

In fact, except for April Fool’s Day, Elon has long been posting on Twitter some seemingly unattainable goals, most of which have been achieved (although delayed). Take today’s privatization, for instance. After his Twitter announcement, Elon immediately explained to shareholders and car owners that his role as CEO would not change after privatization, and he hoped all shareholders would continue to hold Tesla’s stocks after the delisting, promising that he would not sell Tesla’s stocks.

As Tesla is an all-employee-owned company, he even sent an all-employee email detailing the reasons why, and I believe the title of that email should be “Why you shouldn’t oppose my promotion of Tesla privatization.”

The core reason mentioned in the email is that the stock price of a public company will be affected by short-term performance fluctuations, and the all-employee stock ownership mechanism will prevent employees from going all in on their work. As a result, the company has to constantly make decisions favorable to short-term financial reports to maintain a stable stock price, which conflicts with long-term development.

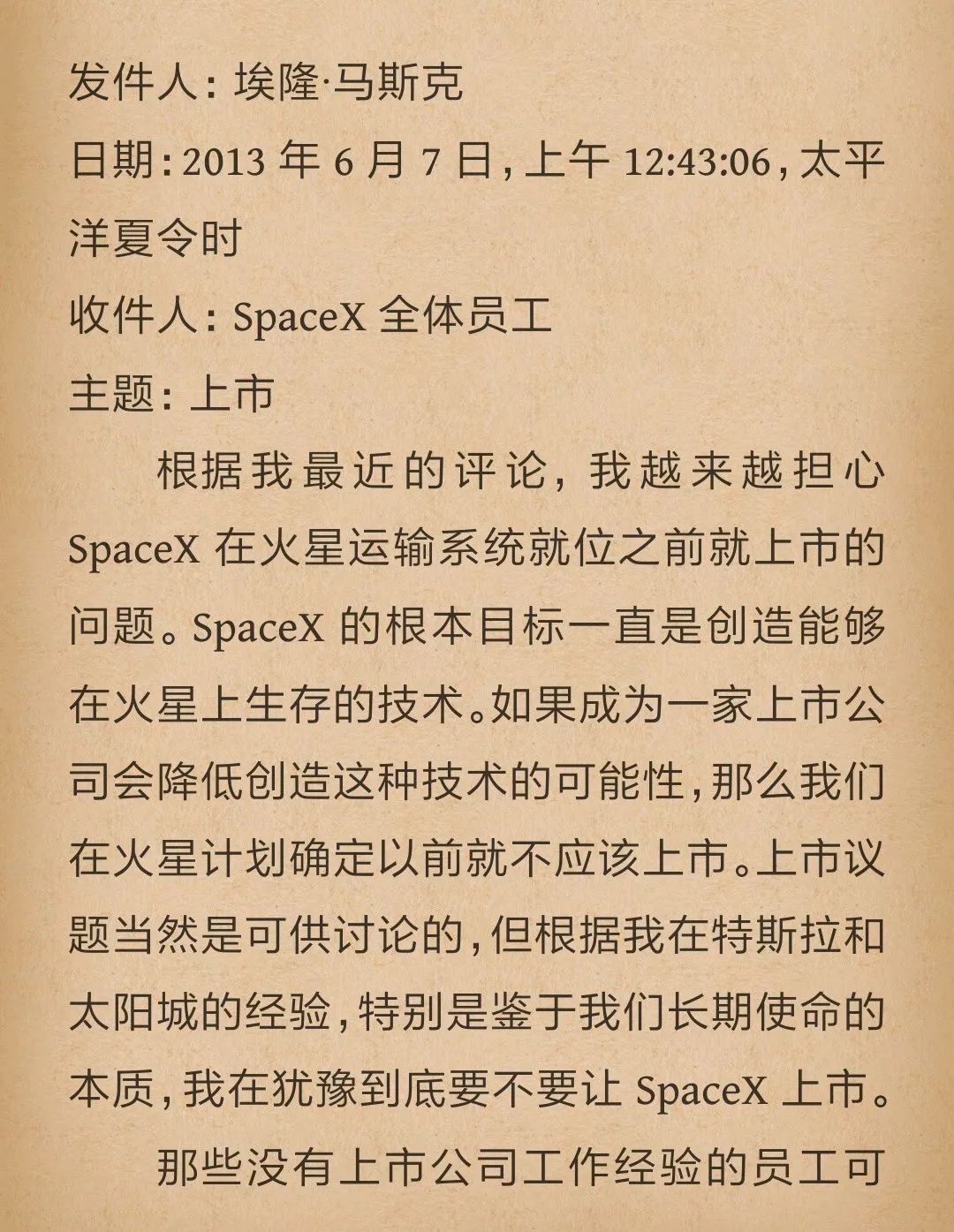

Similar all-employee emails were also sent to SpaceX employees on June 7th, 2013. The title was just changed to “Why we shouldn’t choose to go public like Tesla and Solarcity.”

For the question of whether or not to take the company public, and the pros and cons of doing so, he has thought it through thoroughly.

So it can be assured that Elon must have taken precautions. As for hitting the shorts, it can be considered a side effect of the privatization process.

The next question is, will Tesla go private as Elon wishes?

The Wall Street Journal’s questioning is very strange: because at a price of $420 per share, plus debts totaling over $80 billion, Tesla doesn’t have that much money, so they won’t go private.

Elon’s first words were, “the funding is secured,” and this kind of questioning happened last time when Elon bashed the analyst: “Your questions are so boring that I don’t want to answer them anymore. Just kill me.”

Considering the previous acquisitions of SolarCity, the election of the board of directors at the shareholder meeting, and the impeachment of the CEO, all of which went according to Elon’s wishes, many shareholders began to worry.

However, my judgment is that this time, it will be difficult for Elon to take Tesla private.

In the past, although Tesla was burdened with huge debts when it acquired SolarCity, and its cash flow was already tight, Elon successfully presented a story of an energy loop at the shareholder meeting, which more deeply bound the electric car-energy storage battery-solar panel for energy generation this one-stop energy solution.

From the perspective of the long-term development of the company, Tesla successfully convinced shareholders to vote in favor of the unprofitable acquisition.

But privatization is completely different, even if Elon mentioned that he hoped all shareholders would stay, not all shareholders will accept investing in private enterprise in the form of a special fund – after all, so far, only Space X has adopted a similar model in the world.

For example, many secondary market funds are very concerned about stock liquidity, and the model of trading every six months will create a lot of obstacles for them.

In simple terms, this time many shareholders are not in the same camp as Elon, and Elon and its affiliates as the largest shareholders do not have voting rights. So this is a showdown between Elon’s true fans and Tesla shareholders, although it’s very exciting, it should be Elon’s most difficult win.

However, from the perspective of the development of the smart electric vehicle industry, going public or going private is not that important. Even as a listed company, Tesla is constantly attacking and plundering with executing power and iteration speed that is not proportional to its size.

Li Xiang previously stated on Weibo that Tesla’s advantages in electric driving, assisted driving, and vehicle architecture are becoming greater and greater, and traditional manufacturers are not shortening this gap but are being rapidly surpassed.

What does that mean? Let me give you two simple examples.Tesla updated two pieces of information on its batteries for Q1 and Q2 respectively:

The cobalt content in our NCA batteries is already lower than the 8:1:1 ratio of other battery manufacturers in NCM batteries.

Gigafactory 1’s battery production capacity will reach 20 GWh/year by the end of July, making it the world’s largest battery factory in terms of production capacity.

Just two days ago, two South Korean power battery giants, SK innovation and LG Chemical, announced in unison to postpone the mass production time of the NCM 811 battery until 2019. The first models to be impacted will be Hyundai’s Kona and Mercedes-Benz’s EQC.

Tesla’s 2170 battery based on the 811 formula was mass-produced in January 2017, and seven months later the Model 3 was produced.

In summary, in the battery field, Tesla has been leading but without a “Generation Gap” advantage. This is the first time that Tesla has gained a “Generation Gap” advantage in the battery field, leading competitors by two years in technology and ensuring the lowest cost with the scale effect brought by the largest production capacity in the industry.

The other piece of information concerns Tesla’s self-driving AI chip. So far, we know little about this chip. Many people focus on the point that “computing power has been significantly improved”. However, as an autonomous driving chip, there will undoubtedly be improvements in redundancy fault-tolerant design, vehicle-level testing, and power optimization.

How much improvement has it made? Those who listened to the Q2 conference call from Tesla should have noticed something unusual. For the first time in Tesla’s history, all analysts were ignored and the three core team leaders of the AP department introduced their work one by one. Elon then rare praised the AP team at length and reiterated that because of this chip, Tesla will succeed in the field of autonomous driving. Only then did the analyst Q&A begin.

Prior to this, it wasn’t easy to answer the question of “where is Tesla’s strength compared to traditional car giants?” This was because Tesla did not have any black technology before, but it had reached a relatively advanced level for the key technologies required for intelligent electric vehicles. Only when it overall rose in various dimensions starting from Model 3, Tesla gradually established a “Generation Gap” advantage, making it more deserving of the title of “the Apple of the intelligent vehicle industry.” This is what the entire car industry and shareholders should pay attention to.

The performance that Tesla achieved while pursuing beautiful financial results and short-term benefits in the dilemma as a listed company. What if it goes private? Firstly, the management will no longer have to sleep in the factory and set up tents to produce cars. In theory, the resignation rate of executives will decrease, and a more stable team and work rhythm will bring higher execution force and better performance.

But as the saying goes, whether it goes private or not is not important, whether it’s shareholders or other car companies, observing and learning Tesla’s execution force and iteration speed, once it surpasses a certain threshold to establish a comprehensive differential advantage, the trend of rising stock prices will no longer be as gentle as today.

Q2 2018 Tesla earnings call – China, AP, Energy, and Model 3

Evolution of Tesla: the survival philosophy behind the dash for death

This article is a translation by ChatGPT of a Chinese report from 42HOW. If you have any questions about it, please email bd@42how.com.