Report by Roomy

Edited by Zhou Changxian

Tesla’s hidden worries cannot be concealed, forcing Musk to eat his words.

Previously, Musk declared forcefully that he would “no longer attend earnings conference calls” and was even ridiculed by netizens, “always profitable, nothing to say”. It is true that Tesla has achieved profitability for 13 consecutive quarters, with a free cash flow of up to 3.3 billion US dollars.

His words still fresh, calculating the time, it has been less than a year when Musk had to make a comeback and personally preside over the Q3 2022 earnings conference call, and even uttered two boastful remarks.

“Tesla’s market value may surpass the total sum of Apple and Saudi Aramco” and “Tesla will have an epic year-end.”

However, the thunderous applause did not come as expected.

On October 20th, Tesla released its latest financial report. Behind Musk’s boastful talk was Tesla’s market value falling below 700 billion US dollars, with his own net worth evaporating more than 110 billion US dollars.

According to the Q3 2022 financial report, Tesla’s total revenue was 21.45 billion US dollars, a year-on-year increase of 56%, with a net profit of 3.65 billion US dollars, a year-on-year increase of 75%. Overall, this report card can be considered impressive.

However, Wall Street bankers still see some hidden worries. Tesla’s vehicle gross margin fell below 30% for the second time, with a single vehicle gross margin decrease of over 6%; and there is still a gap of 600,000 vehicles before the target of annual sales of 1.5 million is achieved.

Cowen & Co. analysts pointed out bluntly that capital market expectations for Tesla have been downgraded, mainly due to concerns about weakened market demand in addition to factors such as capacity and rising costs.

It seems that Musk also sees this. Therefore, his attendance at the earnings conference call is also to strengthen investor confidence.However, it’s not certain whether the market demand is declining and hidden worries can be concealed.

Let’s start by defending Tesla.

The reason why the capital market expects Tesla’s stock price to decline is not because of poor profits, but because “revenue is lower than analysts’ expectations”, which is the first time revenue has been lower than expected since the third quarter of last year.

The capital market has always maintained the requirement of being an “outstanding student” for Tesla. In Q3 2022, it put forward a revenue expectation of $22.09 billion. Tesla achieved revenue of $21.45 billion, with a difference of $600 million from the expectation. For other brands, this may not be a big deal, after all, there is still a 56% increase, but for Tesla, “if it does not meet expectations, it is a failure”.

This point can also be proved by the comments of Deutsche Bank analyst Emmanuel Rosner.

On the one hand, he said, “We believe that Tesla’s growth and profit margins may be more resilient than other industry players in the face of a global economic recession.” On the other hand, he lowered Tesla’s target price from $390 to $355.

Musk probably wants to say in his heart, “Listen to me, thank you.”

Of course, this is not the investors being unreasonable.

Actually, in early October, when Tesla announced its third-quarter delivery volume, the capital market had already made some movements. The delivery volume for Q3 was 343,800 vehicles, which was lower than the market’s expected 358,000 vehicles. Moreover, this was still the case after the delivery cycle had been shortened.

The capital market believes that if the delivery cycle is shortened, the delivery volume should increase or exceed expectations. But if it falls below expectations, it means that market demand may be declining.

This judgement put pressure on Musk. The stock price of Tesla plummeted 8.6% that day, and many investment banks lowered their target prices.

During the earnings conference call, Musk had to emphasize that “Tesla is moving towards a more stable delivery pace.” When asked about the annual growth rate of 50%, Musk said, “We will continue to grow,” and insisted that the market demand was still strong in the fourth quarter and deliveries would be good.

“Tesla will have an epic ending.”

Musk hopes that with this poetic statement, investors will feel sincerity and confidence. However, when investors have not fully felt the sincerity, Tesla CFO Kirkhorn poured cold water on the statement, saying that “one-third of the third-quarter deliveries were concentrated in the last two weeks, and the annual delivery growth rate is expected to be less than 50% this year.”

The “epic ending” defined by Musk is to achieve a delivery volume of 1.5 million vehicles this year. So far, Tesla has delivered a total of 908,000 vehicles in the first three quarters, leaving a gap of 600,000 vehicles.

It seems like a simple calculation, but it is not an easy task to complete 200,000 deliveries per month in the next three months. Besides, the highest monthly delivery record of Tesla in China market is only 83,000 vehicles. It is challenging to meet the annual goal, and the market is urging Musk to be “more realistic.” After all, in the year of 2021, Tesla’s production of the last three months only reached 305,000 vehicles, although Musk repeatedly emphasized the market demand.

However, the capital market does not believe it so much. As an extremely important market in China, Tesla faces more challenges in sales, and the monthly sales volume of some car models has dropped out of the top three.Of course, it doesn’t mean that Tesla’s sales in China have declined. Data shows that Tesla’s sales in China in the first nine months of the year were 318,000 units, a year-on-year increase of 55.4%, which is equivalent to the level of the whole of last year. It’s just that the new energy vehicle market in China is rapidly growing, and there are more and more choices outside of Tesla.

“I think they have a real challenger for the first time, and that challenger is called BYD.”

Former Tesla board member and founder of the Westlake Group, Steve Wesley, said in an interview that although Tesla’s “profitability and brand influence are difficult to replace”, the only challenger has emerged.

For Tesla, this may not be good news. Because in BYD’s model lineup, the market below 200,000 yuan is what Tesla lacks, and the BYD Qin PLUS, as a new energy vehicle model, has a price of more than 100,000 yuan and is the monthly sales champion in the A-class car market, which also illustrates some changes.

As we all know, this market, which occupies nearly a quarter of China’s passenger car market, is of great importance.

However, Tesla is blank.

A significant price reduction

Of course, Musk doesn’t think that Tesla’s revenue being lower than market expectations is due to a decline in consumer demand, but instead blames external factors. In addition to the economic situation, the biggest constraint is production capacity, which Tesla regards as a “real problem”.

“There are not enough ships, trains or trucks.”

Musk said so when responding to delivery issues, with an undisguised tone of frustration. After all, compared with future market demand, delivery is the biggest challenge right now.# Tesla’s Global Factories Running at Full Capacity

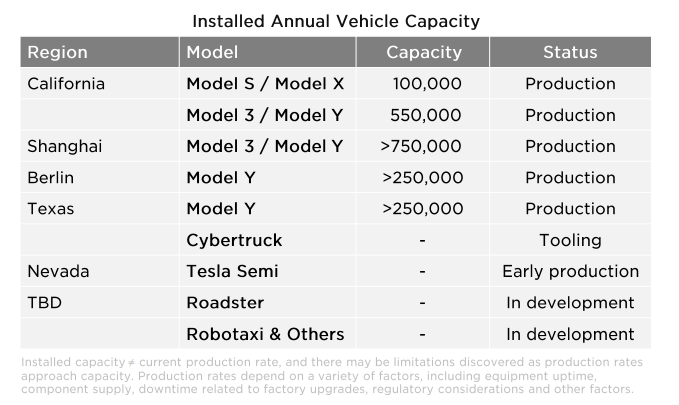

Tesla’s factories around the world are running at full capacity. The Shanghai Gigafactory has the highest production capacity, with over 750,000 vehicles after its expansion. The California factory can produce up to 550,000 vehicles. However, the Texas and Berlin factories, which started production less than half a year ago, are lagging behind and still in the ramp-up phase.

The Q3 earnings report notes that the ramp-up speed of the two new factories in Berlin and Texas is affecting the overall gross margin. Currently, the two factories and 4680 battery production are still in the ramp-up phase.

Although Tesla has tried to be positive about the two new factories, the 600,000 vehicle shortfall is still uncertain due to production capacity and delivery.

Tesla has decided to change the situation by focusing on closer deliveries. Therefore, in the earnings report, Tesla also states its main goal for the fourth quarter – to focus on increasing the weekly production capacity in California and Shanghai, as well as ramping up production capacity in Berlin and Texas.

However, this creates a slight dilemma.

“Closer deliveries” means that the production capacity of the Shanghai Gigafactory will be used more for deliveries in the Chinese market because Tesla has encountered significant challenges transporting vehicles from Shanghai to Europe. “This is something Tesla did not anticipate, or did not anticipate would be so severe,” Musk said.

Where is the dilemma? It all starts with the Chinese market.

Undeniably, Tesla’s sales in the Chinese market are still in a strong growth phase. At the same time, the important task of fulfilling the 600,000-car gap will also be carried out by the Chinese market. Data shows that this year, the contribution of the Shanghai factory to Tesla’s global production is still stable at over 50%, and the delivery volume in the Chinese market accounted for over 35% in the first three quarters.

However, there is currently a contradiction. Due to the shortening of the delivery cycle and the expansion of the Shanghai factory, the current order volume can no longer meet the production capacity demand. As the name suggests, this is the so-called “supply exceeds demand”.

The capital market also expressed some concerns about this. The Royal Bank of Canada Capital said, “The demand in the Chinese market is the most worrying at present, as Tesla’s delivery cycle in China seems to be shortening. The question is whether this is a temporary phenomenon or a sign of greater changes in consumers.”

In addition, sea transportation is facing huge challenges. Tesla’s adoption of “closer delivery” means that it must obtain more order demand in the Chinese market. Data shows that as of September, the reserve order volume of the Tesla Shanghai factory has decreased by 23%.

In the absence of new cars, Tesla chose the tactic of “price reduction” to obtain more orders, which is, of course, not a new trick.

On October 24th, Tesla suddenly chose to lower prices, with the highest price reduction of 10% for some models, which was interpreted by the market as “eager to increase sales in the Chinese market”. The capital market expressed that this was not unexpected.

Before and after the Q3 earnings conference call, the market had some anticipation for Tesla’s price cut, which became somewhat meaningful after the call.

Before and after the Q3 earnings conference call, the market had some anticipation for Tesla’s price cut, which became somewhat meaningful after the call.

Tesla announced that the adjusted starting price of Model 3 is 265,900 yuan, and the starting price of Model Y is 288,900 yuan. The starting price of Model 3 has been reduced by 14,000 yuan and that of Model Y has been reduced by 28,000 yuan. This price cut is clearly motivated by trading price for volume.

Those who like to see excitement have already gone to ask BYD and SAIC about whether they will follow Tesla in reducing prices. Although there is no clear answer, one thing is certain: with only two main models, Model 3 and Model Y, Tesla needs more chips to cope with the more intense competition.

Especially for Model 3, the main model, its sales in the first nine months have dropped by 11.4%. As high-end new energy vehicles overall price points are increasing, the advantages of Model 3 are decreasing. For example, there is a high degree of overlap in price range with BYD Han. However, the sales of Han are indeed something that Model 3 envies.

Moreover, the revenue structure of the Q3 earnings report also reflects a trend. The automotive business is still a key factor for Tesla’s performance not meeting expectations. The earnings report shows that Tesla’s automotive costs continue to rise, which has had a certain impact on profitability, and is also one of the factors for the capital market to lower target prices.

With the change in market demand, cost control, product structure adjustment, and the development of “cheap electric cars” have become urgent.

Musk revealed that “the next generation of models will be smaller and will exceed the total production of all of Tesla’s products.” He hopes that costs can be reduced by 50%.### Conclusion:

As for when the new car will arrive, Musk has not given a specific date.

During the Q3 earnings call, Musk made many promises, but he also knows that they will be difficult to achieve.

For example, Tesla’s market value is likely to surpass the combined market value of Apple and Saudi Aramco. Skeptics have already done the math.

Currently, Tesla’s market value is less than $700 billion, while Apple and Saudi Aramco have a combined value of more than $4 trillion, with Apple alone being worth $2.31 trillion. In other words, Tesla needs to increase its market value by $3.7 trillion, and its stock price needs to exceed $1,407 per share.

Musk’s vision of a $4 trillion market value is considered by investors to be unrealistic and ambitious.

“I know it’s difficult, but we need to work very hard, develop new and creative products, manage our expansion well, and have a bit of luck,” Musk replied, refusing to back down.

However, whether or not Musk is satisfied with the current situation is not the main issue. The main issue is that Tesla needs more leverage to gain the confidence of investors. It is clear that some investors’ long-term confidence in Tesla is less sufficient.

This year, Tesla’s stock price has fallen by about 40%, which has already provided some answers.

This article is a translation by ChatGPT of a Chinese report from 42HOW. If you have any questions about it, please email bd@42how.com.