Author: Zhu Yulong

Introduction: BMW’s third cylindrical battery supplier has arrived.

BMW Group announced a strategic partnership with Farasis Energy, which will provide high-quality, high-safety, and zero-carbon 46mm diameter cylindrical batteries for BMW’s next-generation models starting in 2026. Farasis Energy will also build a zero-carbon battery factory in South Carolina, USA, with a planned capacity of 30GWh.

Here are several interesting questions:

-

Why did BMW choose Farasis Energy, which mainly focuses on stacking technology, to build a battery factory in the United States?

-

Besides seizing the domestic market in China, are there any other breakthrough strategies for battery companies? – Farasis Energy’s overseas order provides a new solution to this problem.

-

With the advent of the “capacity is king” era, the era of power batteries has changed. What will be the basis of competition in the future?

I will try to explore these questions.

BMW’s choice of cylindrical batteries

As previously announced, BMW began using 46 series large cylindrical batteries in the “NEUE KLASSE” models in 2025. In BMW’s view, the advantages of cylindrical batteries are:

◎ Cylindrical batteries are standardized, and different battery companies can be compatible and switched.

◎ Cost target reduced by 50%.

◎ Energy density increased by 20%, and cruising range increased by 30%.

◎ Charging time from 10% to 80% reduced by 30%.

◎ 400V and 800V can be switched and compatible.

◎ High-nickel materials reduce cobalt by 50% and copper by 40%.

◎ Cylindrical batteries have significant advantages in safety, especially in the ability to degrade single cell failures (NP4).

What we know is that in China and Europe, BMW has provided over billions of euros of battery production demand contracts to CATL and EVE Energy, two joint venture companies. BMW is seeking a partner in the North American Free Trade Zone to build battery cells, and Farasis Energy has replaced BMW’s previous battery manufacturer in North America. Previously, BMW mainly produced PHEV vehicles in North America, and PHEV batteries were sent from South Korea’s SDI to the United States. With the US tax rebate regulations, establishing a local battery supply in North America is imperative.

This time, BMW will invest $1.7 billion in its US business, mainly for the construction of the Spartanburg electric vehicle factory and battery factory. Farasis Energy will establish a new battery factory in South Carolina to provide BMW’s Spartanburg factory with the sixth-generation cylindrical lithium-ion battery for the next generation of electric vehicles. To gradually occupy the US market, by 2030, the BMW Group will produce at least six full-electric vehicle models in the United States, all using cylindrical batteries.

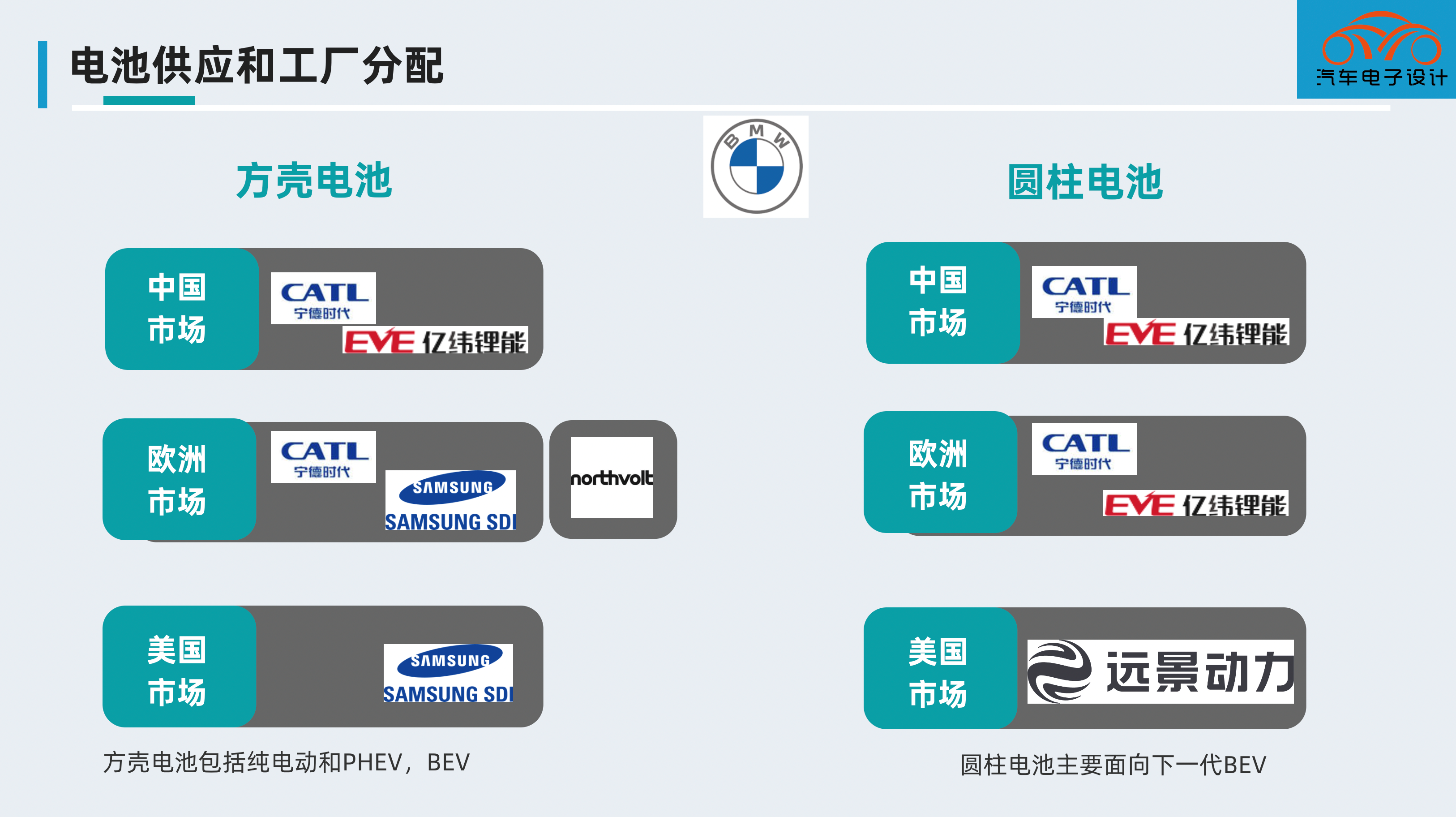

BMW’s global battery distribution is as follows for now:

Prismatic Battery

In 2022, it is estimated that BMW’s market for pure electric vehicles will reach 240,000 units, mainly in China, Europe and the United States. The supply in China is provided by CATL, while that in Europe is mainly provided by CATL+SDI. The United States is supplied by SDI. Northvolt may join the European market, while EVE Energy may join the Chinese market.

Next-Generation Cylindrical Battery

◎ China Market: EVE Energy + CATL

◎ European Market: EVE Energy + CATL

◎ US Market: Farasis Energy

This is an overview of BMW’s power battery distribution for new energy vehicles worldwide.

According to the officially disclosed information, Farasis Energy will build a zero-carbon battery plant in South Carolina, USA, with a planned capacity of 30GWh. Farasis Energy will select cobalt and lithium from certified mines as raw materials for producing new generation batteries, and recycle them. In terms of recycling, Farasis Energy has cooperated with Redwood Material in the United States to jointly create a closed-loop system for recycling battery raw materials, gradually improving Farasis Energy’s recycling rate of raw materials, which also meets future demand.

So why is it Farasis Energy? Why is Farasis Energy, which mainly focuses on soft pack and stacked chip technology, able to take on BMW’s business?

Farasis Energy’s Business Differentiation and Trend of Large Cylindrical Battery

From mid-2021 to 2022, Farasis Energy’s overseas business was very targeted:

-

In June 2021, Farasis Energy reached a strategic partnership on dynamic batteries with Renault Group for 5 years, with a capacity between 40GWh to 120GWh.

-

In July 2021, Nissan’s new generation platform model selected Farasis Energy batteries, and its factory in Sunderland expanded its capacity to 25GWh.

-

At the end of 2021, Farasis Energy’s Ibaraki County factory will provide the latest zero-carbon power battery products for Nissan’s new generation electric vehicle platform starting from 2024.

-

In 2022, Farasis Energy expanded its base in the United States and announced the construction of a zero-carbon super battery plant in Bowling Green, Kentucky, with a planned capacity of 30-40GWh.- In March 2022, Mercedes-Benz announced a strategic cooperation with Farasis Energy to provide power battery products for Mercedes-Benz EQS and EQE.

-

In April 2022, Japan’s second-largest automaker Honda announced that it will purchase batteries from Farasis Energy for the Japanese market.

-

Unconsciously, Farasis Energy has focused on expanding overseas, based on its existing overseas bases, and has also become a core business layout to expand overseas enterprises.

From the industry’s perspective, currently, Farasis Energy’s battery positive and negative electrodes in the United States and the United Kingdom need to be supplied locally from Japan, while in China, the whole process of from positive and negative electrodes to battery cells and modules has been realized. Along with business expansion and capacity landing in Europe and the Americas, integrated production such as from positive and negative electrodes to battery cells and modules will become inevitable.

According to foreign media reports, Farasis Energy will focus on supply chain-related requirements, including localization strategies. Both raw materials and components will be comprehensively considered for achieving localization or related trends. The goal is to achieve local supply chain localization in Europe by around 2027.

In the United States, new factories will be launched successively in 2025, involving materials such as positive electrodes, cathodes, aluminum, and copper. Farasis Energy will gradually localize according to the implementation of the IRA policy, combined with strategic trends and its own operations.

As for the downstream end of product recycling, regardless of the Americas, Europe, China, or Japan, they can form an effect of closed-loop localization in combination with the upstream supply chain and downstream recycling.

For automotive manufacturers, there are several factors to consider when selecting cylindrical batteries:

Technical features

◎ Standardization of battery cells and flexible grouping

◎ Low equipment investment, difficult group design

◎ The biggest difficulty currently is that fast charging is hard to achieve 4C requirement

◎ Strong capacity for electrochemical systems and support for new processes and systems

In the manufacturing of power batteries, the technology of cylindrical battery cells is the earliest mature and has the highest degree of standardization. The winding technology of cylindrical battery cells has reached the level of 200 PPM (200pcs/min) with the gradual automation. In the manufacturing process, cutting the continuous electrode material coated with a layer into small electrode pieces can also improve the material utilization rate of the entire electrode material, and the material utilization rate of cylindrical battery cells is the highest.

Battery safety

◎ Can support cell failure and fault downgrade

◎ From a failure point of view, cylindrical battery cells have been rigorously tested.Due to the relatively low capacity of the battery cells, the energy released by thermal runaway is small, significantly increasing the safety of the battery system. The air gap of cylindrical batteries also reduces the heat transfer between the battery cells, which has a certain positive effect on the spread of thermal runaway, and there is a potential for improvement in this aspect of the design.

Therefore, the use of cylindrical batteries is a critical consideration for battery companies in the next stage. It is a highly versatile standardized battery that is highly malleable. From the perspective of the entire application, emphasis is placed on the enterprise’s own manufacturing capabilities, cost control capabilities, and quality systems.

Developing and producing large cylindrical batteries requires companies to have multiple capabilities:

- Firstly, research and development capabilities—strong technical capabilities for high-energy-density electrochemical systems.

◎ Energy density

◎ Fast charging capability

◎ Performance characteristics

-

Secondly, manufacturing system,a single cylindrical battery has a capacity of 20-30Ah, aimed at passenger vehicle manufacturing. A single vehicle requires about 1000 batteries, and 10 billion batteries are needed for 1 million cars. A high level of precision manufacturing is required for battery production.

-

Finally, quality and cost control. Due to the large quantity, the yield of the battery cells is critical to the cost. The introduction of new manufacturing technology is relatively friendly for cylindrical manufacturing.

I understand that Farasis Energy has the comparable capacity to CATL and SVOLT, in terms of the above-mentioned abilities. If we only look at the installed capacity, Farasis Energy may not appear outstanding, but in terms of development potential, it truly is a matter where time will tell.

Samsung SDI and LG Energy did not immediately obtain long-term orders for cylindrical batteries because, on the one hand, their investment scale was relatively large, and they were not so sure about their large cylindrical capacity. On the other hand, the overseas market also has diversified needs. For battery companies willing to explore, European and American automakers also offer opportunities.In the context of the impending wave of deglobalization, Farasis Energy has established its roots in the United States ten years ago and grown into a resilient enterprise, relying on a localized engineering team and a decade of experience in localized production, operation, and delivery of lithium-ion batteries.

Looking back, the outbreak of overseas business in mid-2021 is attributed to the DNA of a car manufacturer that has been nurtured by Nissan and the international collaboration capabilities that have emerged over the past few years after the integration of internal teams from Japan, China, the US, and the UK, which makes BMW believe that this company is trustworthy in all aspects, including product development, process manufacturing, and mass production delivery.

What is the key to success in the competition within the power battery industry in China? Who can stand out?

In China, we see:

-

Positive capacity growth: The lithium-ion battery supply in China is experiencing positive growth, with most companies focusing on aggressive expansion plans, and further capacity improvement is expected.

-

Future market consolidation: Second- and third-tier battery companies lacking large-scale supply experience may exacerbate supply-demand imbalances in the medium-term, which could trigger market consolidation. Auto manufacturers are also actively preparing to enter the battery field for vertical integration.

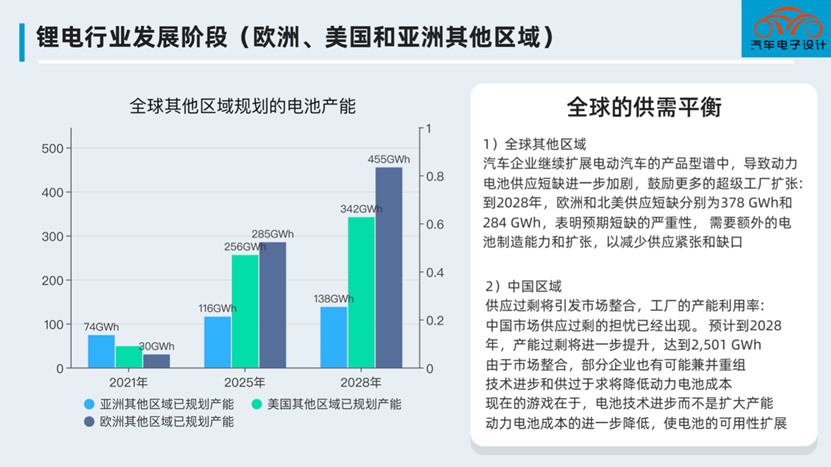

In fact, China’s lithium-ion battery industry has already entered a red sea. The concern about supply excess has arisen, and the factory capacity utilization rate in China is expected to further increase to 2,501 GWh by 2028. Due to market consolidation, some companies may also merge and reorganize, and technological progress and oversupply will lower the cost of power batteries. The current market strategy is to focus on battery technology advancement instead of capacity expansion, and further reduction in the cost of power batteries will expand battery availability.

Other regions in the world

Automakers continue to expand the product spectrum of electric vehicles, leading to a further shortage of power battery supply and encouraging more super factories to expand. By 2028, the supply shortage in Europe and North America will be 378 GWh and 284 GWh, respectively, indicating the seriousness of the expected shortage, and additional battery manufacturing capacity and expansion are needed to reduce supply tension and gaps.

Therefore, I believe that for domestic battery companies at this stage, if their strategy is solely focused on the domestic market, it will inevitably lead to a fierce price war. Only by finding their own position can they survive well.

Therefore, I believe that for domestic battery companies at this stage, if their strategy is solely focused on the domestic market, it will inevitably lead to a fierce price war. Only by finding their own position can they survive well.

Conclusion: This time Farasis Energy has unexpectedly and logically won the big order from BMW, which shows the development of the battery industry has undergone significant changes. The competition has shifted from the Chinese market to the global market, from a focus on production capacity to comprehensive capabilities. In fact, regarding the development of new energy vehicles, no one wants to lose globally, nor will they allow a single company to dominate. There will certainly be new variables in the overall situation.

This article is a translation by ChatGPT of a Chinese report from 42HOW. If you have any questions about it, please email bd@42how.com.