Special author | Zhu Yulong

Editor | Wang Lingfang

The performance of China’s auto sales in October is significantly different from that in previous years, with a significant slowing down of growth momentum.

October is traditionally the peak season for car consumption in China. From the perspective of consumers who actually see cars, “golden September and silver October” delayed half a month of “golden September” sales were reflected in October. From the second week of terminal sales data, the growth of car consumption is not optimistic.

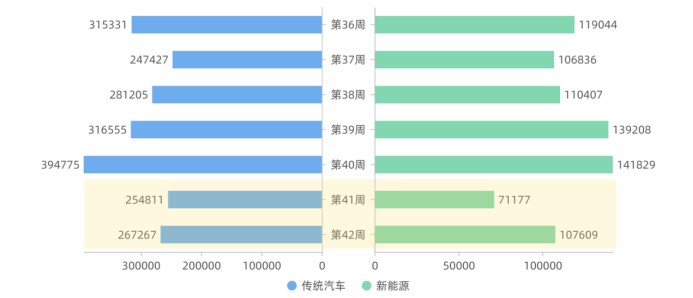

Overall, the sales volume of passenger cars was 375,000 this week, down 3.10% year-on-year and up 15.00% week-on-week. Although the overall data is recovering a bit compared to the previous week, the performance is much worse than that of September.

On the new energy passenger car front, the sales volume this week was 108,000, a year-on-year increase of only 59.20%, which is significantly lower than the previous increase of over 100%, and only 51.19% on a weekly basis. The sales volume this week is basically behind that of each week in September.

Sales of fuel vehicles performed even worse, with sales of 267,000 this week, down 16.3% year-on-year and only up 4.89% week-on-week, with demand continuing to shrink and basically no change.

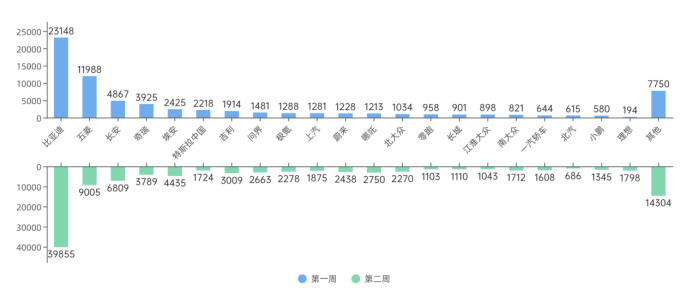

Overall, the data for the past 14 days is not particularly good.

Next, we will focus on commenting on some major companies.

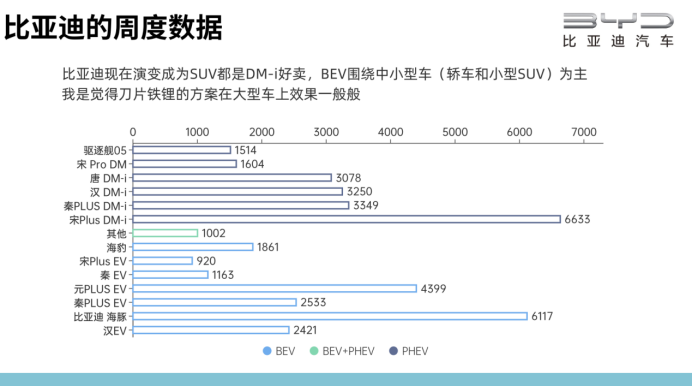

1) BYD Dolphin and Yuanhe Seal have significantly increased growth

The first week of October with 23,148 units was a bit strange, while the second week’s insurance data returned to normal levels with 39,855 units. The key now is whether BYD’s order backlog is valid and whether consumers are willing to wait until next year. With the increase in production capacity, pure electric BYD is now centered around the Dolphin, Yuan Plus, and the Sea Lion is also gradually increasing.

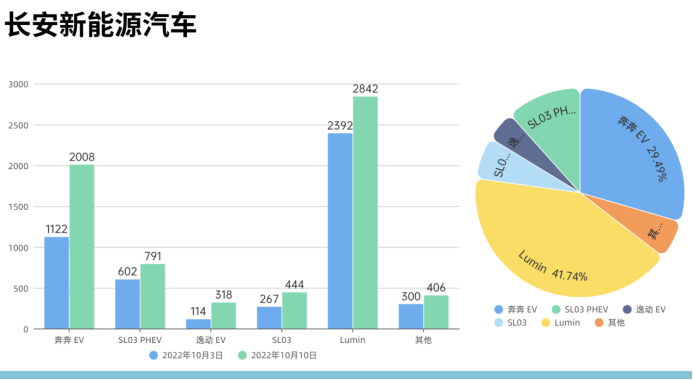

2) Changan’s performance has steadily increased

Changan’s performance in the second week of October was relatively stable. The new energy insurance data was 6,809 units, with Benben EV at 2,008 units and Lumin at 2,842 units, accounting for the majority. The SL03 series of pure electric vehicles had 444 units, and the extended-range version had 791 units, while the old model Eado EV had 318 units.

3) In October, Tesla China is mainly focused on exporting

2218 units were sold in the first week, and 1724 units in the second week. This month is mainly focused on exports. I think Tesla needs to adjust its prices to achieve Q4 sales target without reducing the price, just a matter of time.

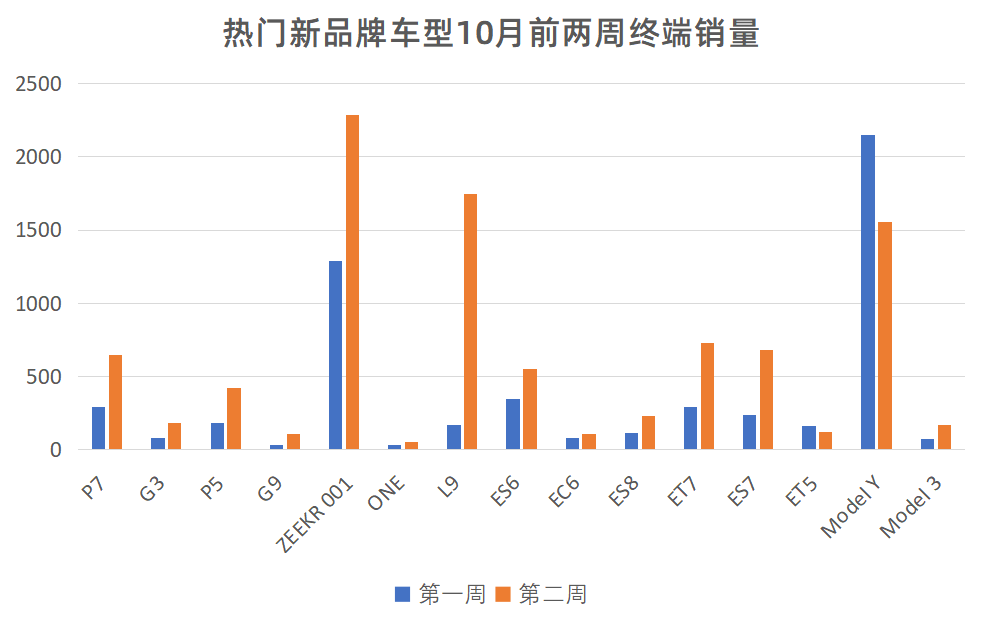

4) Wanjie and Zeekr show good performance

The number of Wanjie insurance policies this week was 2663 units, and Zeekr was 2278 units, which is performing very well.

5) New energy vehicles’ sales growth is relatively stable

This week, the number of insurance policies for NIO was 2438 units, and ET5 has just started delivering. The number of insurance policies for XPeng was 1345 units, and G9 is gradually making progress. The number of insurance policies for Li Auto was 1798 units, and sales of L9 have changed significantly.

Overall, October is expected to be a month of sales take-off. However, there is no sign of a take-off trend so far, which is a warning that car companies will face increased pressure in the future.

— END–

This article is a translation by ChatGPT of a Chinese report from 42HOW. If you have any questions about it, please email bd@42how.com.