Special Author | Pleasure and Comfort

Editor | Zhu Shiyun

On August 29th, HKEX announced the listing news of Leapmotor, which means that Leapmotor may become the fourth “new force in car-making” to be listed on HKEX after WM Motor, Xpeng and Li Auto.

As the IPO is approaching, NETA and Leapmotor have both surpassed WmAuto in sales volume recently. But this does not mean that NETA, Leapmotor and WM Motor have gotten rid of the ICU state. On the contrary, these three second-tier new forces are still in a negative gross profit state and are always at risk of falling into a bigger quagmire.

The Two Core Highlights of IPO – Sales Volume + Self-Research and Development

In the prospectus, Leapmotor believes that its core competitiveness is first its overall self-research and development and vertical integration capabilities, and secondly, sales volume (essentially scale).

1. Leapmotor’s “Rising Quantity and Price”

In 2020, Leapmotor delivered 8,050 vehicles; in 2021, it launched a new C11 model priced between 150,000-200,000 yuan, while driven by hot sales, it delivered 43,748 vehicles for the whole year; in Q1 2022, it delivered 21,579 vehicles, and in Q2 2022, it delivered 30,415 vehicles. In the first half of the year, it delivered a total of 51,994 vehicles, an increase of 250.5% compared with 2021.

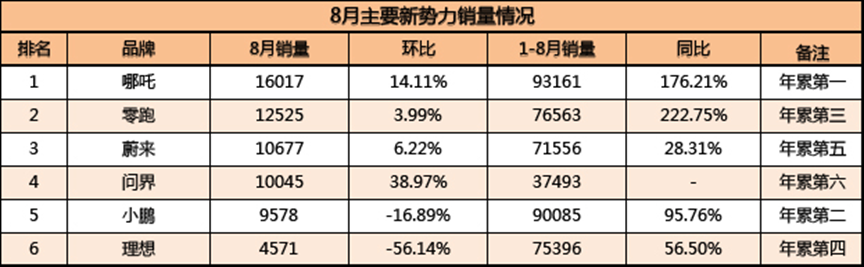

In August of this year, Leapmotor delivered 12,525 vehicles, becoming the second largest in the number of deliveries among all the new car-making forces. It also surpassed NIO and Xpeng to become the third largest in the cumulative delivery volume (76,563 vehicles) from January to August.

If we only look at sales volume, Leapmotor is indeed relatively successful. What it can continuously improve in the future is the sales structure of Leapmotor. From 2019 to H1 2022, the proportion of the T03 model with a price below 100,000 yuan in Leapmotor’s sales structure has exceeded 75%, while the proportion of the Leapmotor C11 in the 150,000-200,000 yuan price range is only 21% (the rest is the first model S01).

The high proportion of products in the middle and low price segments also directly leads to Leapmotor’s average unit price (calculated based on revenue) being around 100,000 yuan. At the same time, the unit selling price also shows obvious fluctuations with the product pace, from 113,000 yuan starting from 19 (S01), to 78,400 yuan and 71,600 yuan in 20 and 21 (mainly T03), to 92,200 yuan in Q1 22. Leapmotor is also constantly improving its average unit price.

2. The Tragedy of Self-Development# Zero Run hopes to use the two capabilities of “global self-development” and “vertical integration” to distinguish its brand. This feature is different from NIO’s “services”, XPeng’s “intelligence”, and Ideal’s “positioning”. It not only highlights its technological strength (backed by shareholders) but also hopes to use this label to form its own differentiation.

From the perspective of Tesla and BYD, the head enterprises of global new energy vehicles, full self-research can indeed provide sufficient control ability to the supply chain. However, full self-research also means huge R&D investment and a gap with the frontline of the industry in a short time.

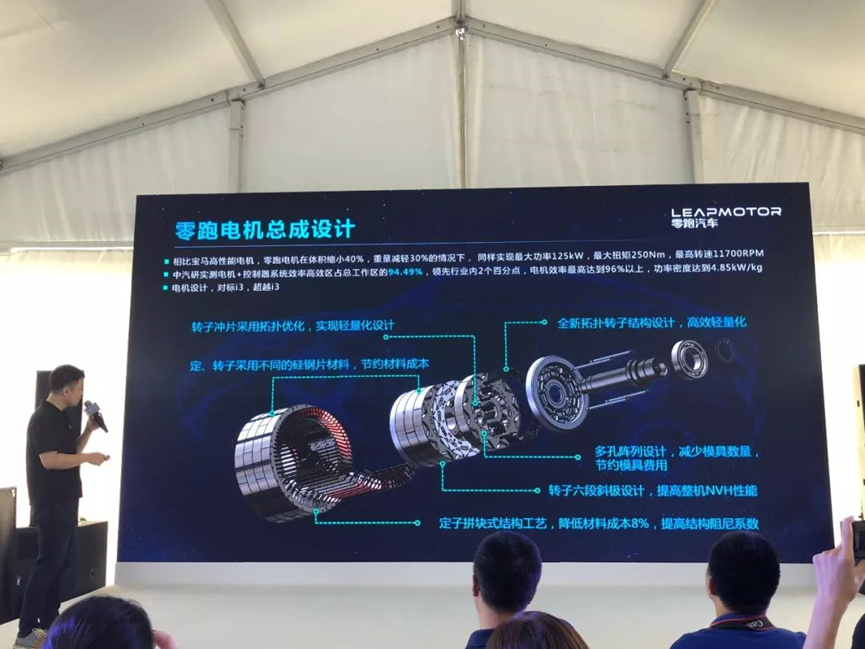

Taking the C11 released in 2021 as an example, the first batch of models adopted Zero Run’s self-developed water-cooled electric drive system, with an overall efficiency slightly lower than the industry mainstream level. Especially after delivery, the energy consumption is higher than that of the same level of pure electric models. By 2022, Zero Run has realized a more advanced Panggu oil-cooled electric drive, and both integration and energy conversion efficiency have been further improved. However, this means that part of the investment in the previous R&D of water-cooled electric drive may have been completely wasted.

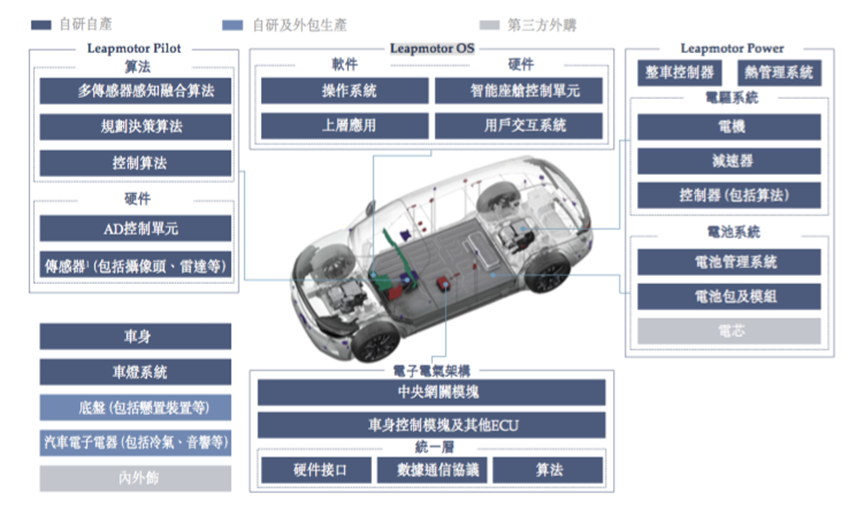

In addition to the electric drive, Zero Run’s R&D in the three-electric system also includes CTC batteries (Leapmotor Power), a brand-new electronic and electrical architecture and intelligent cockpit (Leapmotor OS) and autonomous driving system (Leapmotor Pilot).

The direct result of this is that in 2019, 2020, 2021, and as of March 31, 2022, Zero Run’s R&D expenses accounted for 306.4%, 45.8%, 23.6%, and 12.2% of total revenue, respectively. By 2021, the R&D cost per vehicle has reached as high as RMB 16,900, keep in mind that at that time the average selling price of Zero Run’s vehicles was only slightly over RMB 70,000.

A large amount of R&D expenses have not been able to form sufficient efficiency and differentiation in a short time, which is the dilemma of Zero Run’s full self-research model.

1. Negative gross profitAccording to the information released by the Zero Run IPO, due to being in the early stage of production, the sales cost during this period is high to accelerate production and delivery to achieve economies of scale. As a result, the gross profit increased from -112 million yuan in 2019 to -320 million yuan in 2020, and further increased to -1.388 billion yuan in 2021. The gross profit as of March 31, 2022 was -529.5 million yuan, and the decrease in Q1 2022 gross profit is mainly due to the increase in sales volume and the cost of purchasing dynamic batteries.

Overall, Zero Run’s gross profit margin improved from -95.7% in 2019 to -50.6% in 2020, and further improved to -44.3% in 2021, and improved from -49.4% in Q1 2021 to -26.6% in Q1 2022. In the future, as the product mix changes, the average selling price increases, and the scale economy effect increases due to the continuous increase in production and sales volume, the average manufacturing cost per bike will be significantly reduced. As production and sales scale expands and operational efficiency improves, it is expected that the company’s gross profit margin will further improve.

In short, the current negative gross profit is mainly due to the high amortization caused by the low production and sales rate, and in the future, the negative gross profit will improve as the production and sales rate and the average selling price increase.

Negative gross profit is not terrible, as around 2020, Wei Xiaoli also experienced a negative gross profit phase.

But what’s even more terrifying than negative gross profit is when the selling price cannot cover the BOM cost.

In the IPO document, Zero Run detailed the composition of the sales cost (P331), which is basically equivalent to the BOM cost we commonly use.

If we compare this cost with the sales revenue, we will find that Zero Run is still in the negative BOM cost stage.

In 2019, Zero Run’s selling price minus BOM was -60.8 thousand yuan, exceeding the selling price by 53.76%; in 2020, it was -19.8 thousand yuan, exceeding the selling price by 25.84%; in 2021, it was -26.1 thousand yuan, exceeding the selling price by 37.36%; in Q1 2022, it was -18.1 thousand yuan, exceeding the selling price by 19.67%.If the BOM cost is greater than the selling price, it means that only the material cost alone is a loss for every car sold! In Q1 of this year, the nearly 20% reduction in the single vehicle selling price minus the BOM loss means that NETA is still far from the “positive gross margin” road (achieving positive gross margin at least requires material cost to be calculated as positive). Not to mention the huge fixed asset depreciation and amortization. According to the financial report, the amount of fixed asset depreciation of Zongshen Power’s single car in Q1 of 2019-2022 was: 41,800 yuan, 15,800 yuan, 3,300 yuan, and 172,600 yuan, while the single car manufacturing cost including labor were: 66,000 yuan, 19,900 yuan, 5,100 yuan, and 6,900 yuan.

These manufacturing cost details once again illustrate that the essence of the automobile industry is still about scale: large-scale fixed assets need to rely on sales volume to quickly amortize.

How Long Can Zongshen Power Burn Through Its Cash Reserves?

1. What is the Financial Situation of Zongshen Power?

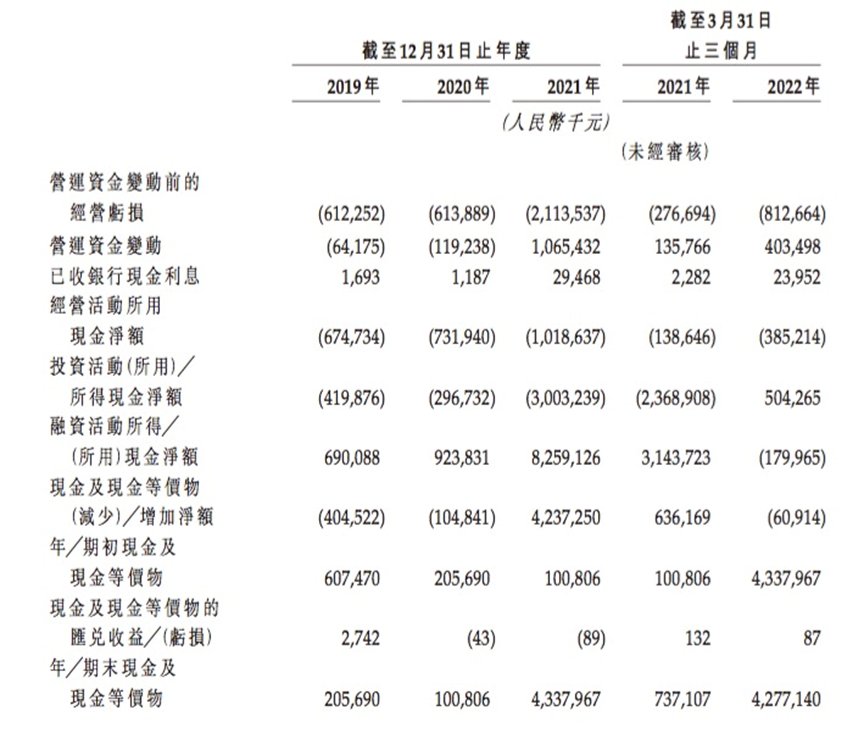

From 2019 to Q1 of 2022, Zongshen Power’s cash and cash equivalents were RMB 246 million, RMB 542 million, RMB 5.713 billion, and RMB 5.231 billion respectively, which is one order of magnitude lower than WmAuto Automobile’s RMB 50 billion cash reserve.

In 2019-2021, Zongshen Power completed RMB 690 million, RMB 924 million, and RMB 8.259 billion, and the RMB 8 billion financing in 2021, which supported Zongshen Power to survive until the night before the IPO.

2. How Long Can RMB 5.2 Billion Last at Its Current Burn Rate?

From 2019 to Q1 of 2022, the net operating cash flow (burn rate) of Zongshen Power were -RMB 675 million, -RMB 732 million, -RMB 1.018 billion, and -RMB 385 million, respectively. If the current burn rate of more than RMB 1.6 billion per year (RMB 385 million multiplied by 4 months) continues, the RMB 5.2 billion cash and its equivalents on the book can only support spending for approximately two years.

In other words, if Zongshen Power’s IPO fails this time, the current cash on its books can support only 24 months of expenditures and will no longer be able to support the development of subsequent new models.

Life and Death Speed of Second-tier New Challengers

From the perspective of the overall market performance, it is not just Zongshen Power that is facing such a severe challenge.

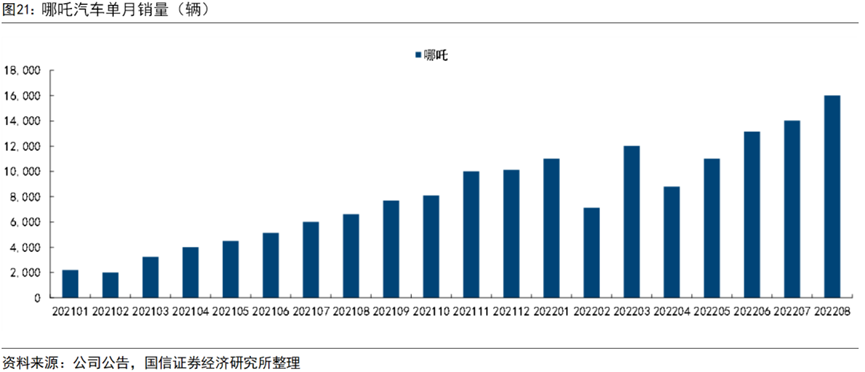

1. NETAIn 2022, NETA is definitely the best-performing second-tier new force in terms of sales (excluding the question realm). In August, it became the sales champion of new forces in that month with a sales volume of 16,017, and the cumulative sales volume from January to August also surpassed XPeng to become the sales champion of all new forces. At the Chengdu Auto Show at the end of August, NETA also announced that it would achieve the delivery of the 200,000th vehicle in September.

Regarding the strategic positioning of NETA, the company aims to become the VIVO of the automobile industry, and its products are targeted at young people in small towns in third-, fourth-, and fifth-tier cities. Currently, there are three main models on sale (the overall model matrix is more detailed and complete than that of Leapmotor). The NETA U (compact SUV, with a guide price of 102,800-179,800 yuan), NETA V (small SUV, with a guide price of 62,900-120,800 yuan), and NETA N01 (small SUV, with a guide price of 66,800-139,800 yuan). The average selling price of NETA’s main models is below 150,000 yuan, and the company focuses on high cost-effectiveness, positioning for the middle and lower-end market, competing differentially with first-tier automakers such as Nio. Additionally, the NETA S, which will soon be delivered, is the company’s first model priced over 200,000 yuan, and its sales performance still needs market validation.

Regarding NETA’s IPO market, rumors have been circulating for some time. In October 2021, 360 issued an announcement stating that it plans to use its own funds of 290 million yuan to acquire a stake in Hezhong New Energy Automobile Co., Ltd. (the automotive brand under which NETA operates), and after completing the investment, it will obtain a 16.59% stake, becoming its second-largest shareholder. According to data disclosed in the announcement, in the first half of 2021, NETA achieved operating income of 1.6 billion yuan, a net loss of 700 million yuan, and a profit margin of -43.75%. This performance was better than the -91.58% profit margin achieved by Leapmotor in 2021.In February of this year, NIO was once again reported to be preparing for an IPO. Some media reported that NIO was preparing to be listed in Hong Kong and had initiated a Pre-IPO round of financing with a target valuation of approximately 45 billion yuan. However, on June 27, 360 issued an announcement stating that its subsidiary plans to transfer 3.532% equity of Hezhong New Energy Automobile Co., Ltd. (hereinafter referred to as “NIO Automobile”) with a registered capital of 79,994,371.67 yuan (not actually invested) to Jiaxing Xinzhu Equity Investment Partnership Enterprise (Limited Partnership) and Shenzhen Jingcheng Kaikuo Enterprise Management Center (Limited Partnership) for a transfer price of 0 yuan. After the transfer is completed, 360 will still hold 11.4266% equity of NIO Automobile. 360 claimed that the main reason for this abandonment was to support and assist the (founder) team.

As of the time of publishing, there is no further news about NIO’s IPO.

2. WM Motor

As a new force born at the same time as NIO, its market performance in recent years has been declining. From multiple reports of vehicle self-ignition in 2020 to last year’s collective consumer complaints about the “lockout” problem, coupled with sluggish sales, WM Motor has already stood on the cliff of the market – although WM Motor submitted an IPO application to the Hong Kong Stock Exchange on June 1, three months have passed with no progress.

According to the data submitted by WM Motor to the Hong Kong Stock Exchange on June 1, 2019-2021, the company’s total revenue was RMB 1.762 billion, RMB 2.672 billion, and RMB 4.743 billion respectively; the annual losses were RMB 4.145 billion, RMB 5.084 billion, and RMB 8.206 billion, and the profit margins were -235.23%, -190.29%, and -173.03%, respectively.

From the data, it can be seen that WM Motor is also in a state of BOM cost loss per vehicle, with a BOM loss of 22,600 yuan per vehicle in 2022, and an increasing loss amount year by year. At the same time, WM Motor’s average selling price per vehicle decreased from 134,800 yuan in 2019 to 97,400 yuan in 2021, a decrease of 27.76%. From negative gross profit, negative BOM to continuous decline in average selling price per vehicle, coupled with only about 4.155 billion yuan in cash and cash equivalents, at the rate of operating cash flow expenditure of 3.187 billion yuan in 2021, it can only support WM Motor for 15 months.From the perspective of cash reserves, the cash reserves of second-tier new forces are generally at the level of 5 billion yuan (NETA is temporarily unknown), which is one order of magnitude lower than the cash reserves of NIO, XPeng, and Li with more than 50 billion yuan! At the same time, according to their current “burn rate”, if they cannot successfully complete the IPO and financing in 2022, they will inevitably face extremely tight cash flow.

In 2022, it will be the final hurdle for the IPO of second-tier new forces. If they can pass it, they will still be able to see the faint path ahead; once they fail, it will be difficult for them to have a way to rise again!

In conclusion

2022 is a magical year for new energy vehicle companies. The sales of leading enterprises in the first echelon are growing rapidly, traditional brands in the second echelon are resolutely transforming themselves, and the leading new forces in the third echelon are concentrated on updating their second-generation products/platforms. The second-tier new forces in the fourth echelon still face the life and death problem of “unable to cover BOM costs”.

Although this year is a year of the rise of second-tier new forces, it is also the year of the closing of “new innovative energy brands”. After entering 2023, it will be difficult for any new energy brand (Apple and Xiaomi are mature brands) to have sufficient financial resources and market space to create a completely new brand.

All of this is based on the underlying logic of the huge threshold for car manufacturing (starting at 20 billion yuan) and the scale effect of the manufacturing industry (300,000 vehicles), which applies to all major players in the market, whether it is Tesla, BYD, NIO, XPeng or Ideal!

Time is running out for second-tier new forces, and facing the “life and death speed of IPO”, they can only face an uncertain future with a “desperate run” attitude!

This article is a translation by ChatGPT of a Chinese report from 42HOW. If you have any questions about it, please email bd@42how.com.