Author: Vic

Turning from traditional fuel power to cleaner energy is the path that the global automobile industry must strive for. However, before truly shifting towards cleaner energy, “electrifying” cars has become a turning point, or a “temporary substitute.”

So, have you ever seen headlines like this when browsing news about new energy vehicles?

Indeed, with over 30% penetration rate of new energy retail sales and new forces selling over 10,000 units a month, all of these make the Chinese new energy vehicle market appear to be smooth sailing in recent years.

Perhaps this apparent “everything is fine” has led many to believe that China’s new energy vehicles have already achieved comprehensive overtaking. But is this really the case?

Winning consumer acceptance is the first step of overtaking

China implemented a development strategy for new energy vehicles a long time ago: promoting the actual production and landing of new energy vehicles through subsidies.

At that time, there were still many consumers who would say: Why buy new energy vehicles when you can buy fuel vehicles?

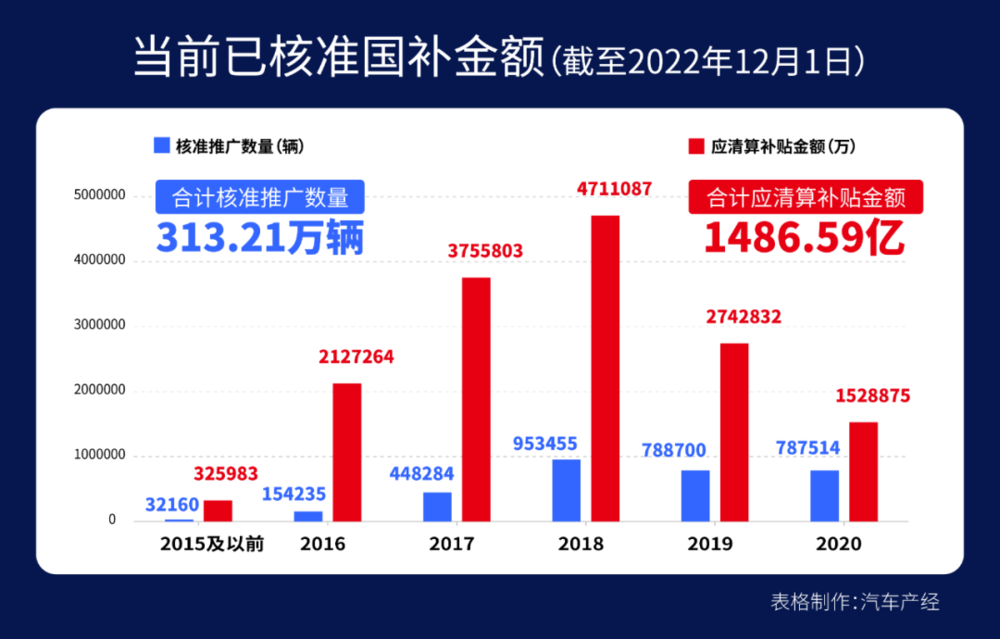

With only two weeks left, the ten-year subsidy for new energy is about to end. People’s understanding of new energy vehicles has also undergone tremendous changes since ten years ago. The most obvious manifestation of this sense of approval is that more and more people choose to purchase new energy vehicles. According to data from the Ministry of Industry and Information Technology:

From the end of 2012 to May of this year, the cumulative sales of new energy vehicles in China have surged from 20,000 to 11.08 million;

From 2016 to 2020, in the five-year period, the subsidy amount given to new energy vehicles in China has drastically increased from CNY 860 million to CNY 10.54 billion annually. The total amount of subsidies has exceeded CNY 30 billion.

“`

“`

Many people have complained about the subsidies for new energy vehicles, but it must be admitted that the ten-year subsidy policy has allowed China’s new energy vehicle industry to grow up from its infancy, and with this growth, the industry’s reliance on subsidies is gradually decreasing.

From 2017 to 2020, the per-vehicle subsidy has been reduced from 67,300 yuan to 23,000 yuan, which is also the time when the penetration rate of new energy vehicles is soaring. With the support of domestic policies and the development of the market, the development of new energy vehicles has been pushed to its peak.

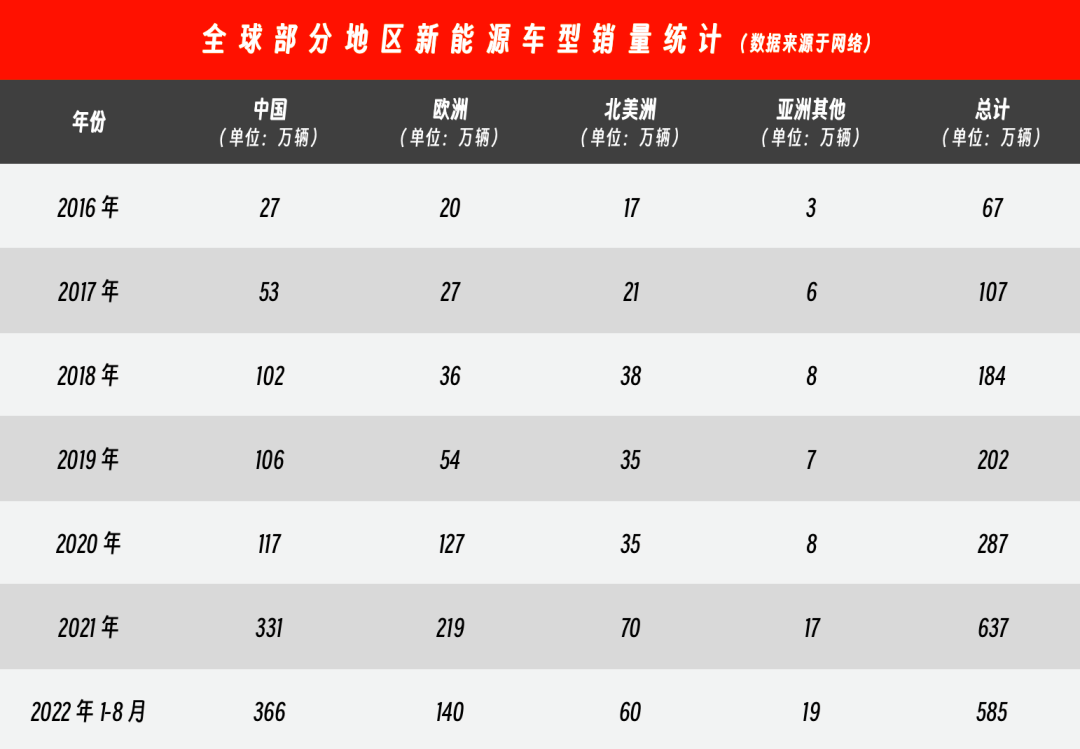

We can look at global sales statistics of new energy vehicles in recent years:

For example, in August of this year, sales for the first eight months of 2022 totaled 3.66 million vehicles, far exceeding the sales of 1.4 million in Europe and 690,000 in North America.

It is worth noting that the Chinese market is singled out and compared with several continents in this sales statistics. Therefore, many people are willing to take this sales statistic as evidence that we have already overtaken the curve in the new energy era.

But don’t forget one thing, China has a population of over 1.4 billion, while the total population of Europe is less than 750 million and North America has just surpassed 460 million.

The reason why we have been able to dominate the sales of new energy vehicles in recent years is inseparable from the environment:

-

First, policy guidance;

-

Second, a large population base;

-

Third, the economic development has continuously increased the purchasing power of domestic consumers.

Also, don’t forget that this sales data still includes the period when Tesla was the leader in the new energy vehicle market in China for several years. That is to say, in a period of time, China was the world’s largest market for new energy vehicles, but it was still dominated by a foreign car company.

Nevertheless, we have indeed achieved a transformation of recognition. In the first eleven months of this year, the total sales of new energy vehicles in China were 6.067 million, accounting for about 25% of the total sales. This data was only as high as 15% in the past two years. Especially for domestic brands, the penetration rate of new energy vehicles has exceeded 50% in November. People’s impression of new energy vehicles is no longer limited to ten years ago, such as being used for taxis, being low-end, or cheating subsidies. New energy vehicles are gradually becoming the mainstream in China’s automotive market.

“`Let more and more consumers recognize new energy vehicles, especially electric vehicles. We have achieved the first step.

How to Overcome the Curve When Straight Lines Are Impossible?

Let’s go back 20 years, when the concept of “independent brand” did not yet exist in the auto industry.

Whether it was BYD, Great Wall, Geely, or Chery, they either had not yet obtained an “automobile license” or were still in their traditional business of producing non-passenger cars before officially transitioning to passenger car production. Therefore, the passenger car market was basically dominated by joint venture brands and imported cars at that time.

As more and more people discovered the blue ocean of China’s passenger car market and policies gradually opened up, more and more brands obtained automobile licenses, and China’s auto market became active all of a sudden.

Even so, there was a huge technological gap between domestic independent brands and joint venture and overseas brands in the traditional “three major components” of engines, transmissions, and chassis. We even needed to adopt overseas technologies or reverse engineer with a sense of “tribute”.

The traditional three major components were like an invisible hand strangling the throat of independent domestic brands, making them breathless in front of the technologies of joint venture and overseas brands.

As we approach the past decade, the era of new energy has quietly arrived, and a new curve has appeared before our eyes. If the new energy track is compared to a “curve”, then the traditional energy era was a “straight line” by comparison.

Some people say that overtaking in curves is actually bypassing the two areas that require the most technological accumulation, which are engines and transmissions, in the era of new energy. This makes the advantages of traditional fuel giants no longer obvious, and the power technologies they have accumulated are no longer applicable to electric vehicles, just like film cameras gave way to digital cameras.

However, the fact is that traditional giants are not simply endowed with fuel power technology. Many decades ago, traditional giants had already attempted to develop electric cars. For example:

- BMW launched a pure electric car, the BMW 1602 Elektro-Antrieb, in 1972;

- Citroen developed the pure electric car AX Electrique in 1989 and began mass production in 1993.- Chevrolet launched the S-10 EV electric pickup in 1997 and officially launched it for sale;

- Honda launched the EV Plus electric vehicle in 1997;

- …

More recently, in the past decade, traditional automakers have also invested and experimented in electrification and intelligence. However, compared to the aggressive investment in innovative technology, they do not seem to be as aggressive in putting innovative technology into mass-produced products as new forces.

For example, the 800V high-voltage technology, which was a selling point on new models such as XPeng G9 and Avita 11 this year, had already been put into production on the Porsche Taycan in 2019. At that time, Porsche almost started from scratch, and it gradually perfected the supply chain of 800V platform components with the volume production of Taycan, and we have seen more and more brands using 800V technology in the past few years.

The overseas giants have obviously advanced faster in the upgrade from 400V to 800V on the pure electric technology platform.

The best example in intelligence may be the lidar. 2021 is known as the first year of the lidar to be installed on vehicles. Now, as a competitive intelligent electric vehicle, lidar is almost becoming a standard feature. Luminar, the first lidar technology company listed on Nasdaq in 2021, has become a supplier to many independent brands and new forces. As early as 2018, Volvo invested in this little-known start-up, and this year it was applied to the Volvo pure electric SUV EX90.

Similarly, on the EQXX that traveled 1,200 kilometers this year, we can see how Mercedes-Benz pursues extreme efficiency in the field of electrification; on the fifth-generation BMW eDrive six-phase topology motor mounted on the BMW’s new iX M60, we can see how the era of electrification plays with performance.

These accumulations and developments are based on the hundred-year experience, funds, and technical accumulations of traditional automotive enterprises. We are not discussing these things to boast about the accumulations of traditional brands and to attack new forces and independent brands; on the contrary, it is precisely with these facts in front of us that we can see more clearly that “overtaking on a bend” is not as easy and optimistic as we might imagine.

Moreover, what is needed for overtaking on a bend is not just new technologies and products, but also the accumulation of car-making itself. We often hear a sentence, “We should have awe for car-making”, which is not the preaching of the first entrants to the later ones, but rather the safety attributes of cars that make people have to hold awe and that require new players to accumulate understanding of cars.

Internal Rise is the Second Step to Overtaking on a Bend

The second step of overtaking on a bend, I believe, is the “internal rise”, which means that independent brands need to establish themselves firmly in the Chinese market. This not only refers to the automakers but also to the entire supply chain.

In recent years, we have gradually begun to achieve this goal. According to the sales data of new energy vehicles in China from January to September of this year, joint venture brands are no longer the first choice for most consumers, as they were in the era of fuel-powered cars:

Automakers are generally called “original equipment manufacturers” or “vehicle manufacturers,” because the production of a car model product relies on the support of a large number of suppliers to provide product support.

In new energy vehicles, power batteries are definitely one of the core components. Let’s take a look at the global power battery installation rankings for October of this year:

Ningde era and BYD, both from China, occupy the top two positions in the power battery industry, with installed capacities of 18.1GWh and 7.8GWh, and market shares of 37.6% and 16.2%, respectively, showing a significant improvement compared to the same period in 2021.The market share of CATL, occupying nearly 40% of the global market, is gradually taking on an increasingly dominant position. Further, not only does BYD rank second in terms of battery installation, but it also has consistently impressive sales in the new energy vehicle market, making it adept in both battery and electric vehicles.

Additionally, four other Chinese brands, CATL, CALB, XWD, and EVE Energy, have made the global top 10 in terms of power battery installation. In the production of power batteries, we have indeed made significant achievements. However, it is difficult to maintain a dominant monopoly in any field. Global technological development is so fast that carelessness can quickly lead to being surpassed.

Currently, CATL occupies a significant market share, and it seems that we have a decisive advantage in the battery field. However, it should not be forgotten that CATL owes its success to BMW’s support.

BMW was CATL’s first OEM customer, and provided us with a wealth of technical data and support. There are two cores here: on one hand, if it weren’t for BMW’s decisiveness, CATL wouldn’t have made it to where we are today; on the other hand, BMW also has a comprehensive power battery manufacturing technology.

BMW owns a battery factory in Germany and can produce complete high-pressure batteries. At the same time, it has also been researching solid-state batteries and has begun planning to establish a trial production line for solid-state batteries. BMW aims to launch prototype cars equipped with solid-state batteries by 2025, begin road testing vehicles outfitted with fully solid-state batteries by 2025, and achieve mass production by 2030.

Therefore, firstly, it supports what I just said, “traditional OEMs are not lagging behind us in electric vehicle R&D,” and secondly, traditional OEMs are likely to overtake the current pattern.

In the Chinese automobile industry, the one feat of “overtaking on the curve” has been its industrial chain.The rise of the domestic industrial chain may be most evident in Tesla. In 2019, the Shanghai Super Factory officially launched, with 60% of domestically-made Model 3 parts purchased from China; by the first half of 2021, the figure had reached nearly 90%; and recently, Tesla announced that the localization rate of parts has approached 100%. This change has helped Tesla further reduce costs; it also means that domestic parts suppliers have become mature in terms of quantity, coverage, and quality.

If you plan to build a new energy vehicle, all the accessories and products you need can be found in the Chinese market under Chinese brands. Therefore, China’s current advantage is having a complete new energy vehicle industrial chain, which provides a foundation for real “curve overtaking” in the future.

Going global is the third step of curve overtaking

From getting Chinese consumers to acknowledge new energy vehicles, to making Chinese consumers acknowledge domestic brands. The final step is to go abroad and capture overseas markets. Simply staying within China cannot be considered as “curve overtaking”.

Now, we can see that many domestic brands are expanding in overseas markets. This even includes many new forces, which have taken only a few years from birth to going abroad.

Take BYD as an example, in November of this year, BYD sold 230,000 new energy vehicles, which has continuously been the world’s top seller of new energy vehicles. However, of the 230,000 vehicles, only 12,000 were sold in overseas markets, meaning that the vast majority of buyers who purchased Chinese-made cars and recognized domestic brands are still Chinese consumers.

Expanding global markets is crucial for launching a “counterattack” campaign for self-owned brands in both fuel and electric vehicles. When we view global auto sales in the first half of this year, for example, Toyota sold 5.13 million vehicles, Volkswagen sold 4 million vehicles, and Hyundai sold 3.29 million vehicles… The greater the gap, the more difficult the challenges self-owned brands face: Going global.However, success in product or brand is not the only consideration for entering international markets; technology is equally important.

To achieve success in the field of automotive technology, beyond electrification, pure electric platforms and overall electronic and electrical architecture are crucial components. In this day and age, they are like the “soul” that seamlessly integrates intelligence, electric and vehicle.

Nowadays, traditional automakers in transition, independent brands and new forces are all developing their own pure electric platforms and electronic and electrical architectures, and planning their layout for future intelligent and electric development. However, most of them are “self-produced and sold”, meaning that they develop and use their own brands or brother brands.

Among them, the Geely SEA architecture is one of the popular intelligent electric vehicle architectures in the new energy vehicle market. It is not only a pure technology platform, but also an extendable system that includes a pure electric platform as well as hardware, system and ecosystem layers. Geely has also provided the SEA architecture to brother brands including Geometry, Lotus, Lynk & Co, and Smart.

Moreover, not long ago, Geely Automobile officially announced a strategic cooperation agreement with EMP, a Polish electric vehicle company. The IZERA brand under EMP has officially announced that they will use the SEA architecture to develop pure electric vehicle models.

This also indicates that the technology needs to be put on the agenda for independent brands, Chinese technology companies and suppliers.

The smart race of intelligence, no stone unturned

Intelligence has become one of the key words in the second half of electric vehicles, or rather, a new arms race. Nowadays, more and more automakers are willing to mention intelligence, and even use China as the stage for showcasing their intelligent functions.

So, have we successfully achieved a breakthrough in automotive intelligence?

Let’s look at the field of intelligent driving.

As for chips, not to mention overseas markets, even in the domestic market, the mainstream cockpit chips are the Qualcomm Snapdragon 8155, and the flagship intelligent driving chip is the NVIDIA Orin X. Overseas manufacturers still occupy the largest market in the world.

Although we have chip manufacturers such as Horizon Robotics, Huawei, and Black Sesame Technologies, who also have high-performance ADAS chip products and complete solutions… when facing the market, the number of installations and brand influence do not lie.

In terms of intelligent hardware, the lidar has become the new darling in the “arms race” of autonomous driving. The lidar, which was once difficult to break through in technology and expensive in price, is gradually entering the cars of consumers in China’s lidar companies.

This turmoil has put overseas lidar companies in a difficult position. Chinese lidar companies have begun to achieve large-scale mass production and installation of semi-solid-state lidars on cars.

From January to September this year, the number of passenger cars equipped with pre-installed lidars in the Chinese market reached 57,000, which is more than 8,000 in the whole of last year. According to data projections, the number of cars equipped with pre-installed lidars this year will exceed 120,000.

Among them, Hesai Technology occupies 27% of the global pre-installed fixed-point lidar market, ranking first in the world. The second is Valeo from France. Situated close behind is Idriverplus, with a 16% global pre-installed fixed-point lidar market share, ranking third in the world.

In mass-produced cars, domestic independent brands and new forces are obviously more aggressive and exploring high-end intelligent driving. Many independent brands have embarked on the road of full-stack self-research. In the models we have experienced, for example, XPeng NGP has excellent navigation-assisted driving capabilities. And the iAT 11, which uses Huawei HI, also performs well in the experience of multiple functions.

In contrast, overseas traditional large manufacturers pay more attention to the optimization of basic assisted driving functions. In our experience of intelligent driving products from traditional luxury brands such as BMW, Mercedes-Benz, and Cadillac, we found that they optimize the experience and capabilities of L2 assisted driving more meticulously. When facing completely driverless higher-level driving in the future, we also see the performance of Tesla’s vision-based FSD overseas, as well as Tesla’s Dojo supercomputer for the empowerment of autonomous driving.The second half of intelligent driving has just begun, and it is difficult to tell who the winner is at this point. The real “finals” will have to wait until the arrival of L4.

As for intelligent cockpits, it is the most bustling arena. There is no unified standard answer or approach, even consumer needs vary greatly.

On the in-vehicle OS, the HMI design of car machines now resembles that of mobile devices, making it easier to use and interact with, becoming the main theme of cockpit interaction design. More and more brands are adopting similar designs, making car machine HMI design increasingly homogenized. I think Tesla was the pioneer who opened this road, not Chinese brands.

As for the application layer, domestic independent brands and new powers have obviously explored more gameplay: more useful voice assistants, various virtual images, rich app markets, innovative application scenarios, etc…. Compared with this, foreign traditional car companies seem to be somewhat conservative in terms of application, focusing more on driving, but they still have some advantages in interaction. For example, Mercedes-Benz S has tried zero-level interaction and ambient light interaction.

It is lively and has many choices, but we cannot say that this is a better answer. It is said that China has the group of consumers with the highest acceptance of intelligent cockpit, but we cannot tell whether it is because users like it that car companies have derived such diverse cockpit functionality; or because domestic car companies have created these functions, users try to accept and like them.

Of course, both intelligent driving and intelligent cockpit are young new products for automobiles, and domestic car companies and foreign giants are starting from the same starting line, and there are no tricks to rely on. Strictly speaking, it is not overtaking on a bend. But now, the products that are shining on intelligence still have a long way to go.## 30 Years, We Missed a Lot

Qian Xuesen, known as the “Father of China’s two bombs and one satellite,” was a famous physicist and scientist in China, with a high level of achievement in fields such as aviation and aerospace.

As early as 30 years ago, in 1992, Qian wrote a letter suggesting that China should start developing new energy vehicles. Although this was not Qian’s field of expertise, he put forward his own views on expanding new energy travel in China.

At that time, Qian Xuesen found that many countries around the world were working on “high-efficiency batteries” and planning to develop “battery-powered cars”. Therefore, he pointed out:

- China’s automobile industry should skip the gasoline/diesel phase and directly enter the new energy phase to reduce environmental pollution;

- Under this situation, we should not wait any longer, and immediately draw up a plan for battery-powered cars and strive to catch up and surpass others.

At the same time, Qian Xuesen also mentioned that China’s hydrogen-nickel batteries for new energy vehicles could support 250-300 kilometers of range on a single charge, which was already practical. The more important sentence was that foreign countries were also in the same stage and not much ahead of us.

And the technological route proposed by Qian Xuesen was like what we now call “overtaking on a curve”. Everyone started from the same starting point and had the same ability. By seizing the opportunity, one could make a breakthrough.

One year later, in 1993, Qian Xuesen once again proposed that civil cars must be electrified and powered by batteries. And we had already made a breakthrough in hydrogen-nickel electrodes in “863” and were in the process of development. So why not make up our minds to develop electric cars and bypass the gasoline car phase?

Looking back now, Qian Xuesen not only had enough technical ability in his professional field, but also had a unique perspective in the automotive industry and new energy field at that time. However, it must be said that Qian Xuesen saw the “curve” ahead of time.

Final Words

Throughout the article, I am not trying to “demean” but we are all well aware that the development of intelligent and connected vehicles, as well as new energy sources, is the way forward.Our current success and achievements are also reflected in our lives. With the increase of new energy products, sales are growing steadily, endurance is becoming more solid, and intelligent capabilities are constantly improving. However, I believe that these are necessary demonstrations of technological breakthroughs, and immediate achievements do not represent long-lasting victory.

Because in the global automotive industry, we first need to “stand up”, then “go out”, and then we must “run”.

This article is a translation by ChatGPT of a Chinese report from 42HOW. If you have any questions about it, please email bd@42how.com.