Author: Zhu Yulong

This article is a continuation of the battery industry report, focusing on the changes in the industry from the perspective of the supply chain.

I believe that for a car company to enter the battery industry, it is a long-term strategic move aimed at the ultimate goal. With CATL’s continuous investment in its customers (such as NIO, Aiways, Etergo, Xpeng, BAIC Blue Valley, Xiaokang, and Chery), and the highly concentrated structure of China’s power battery industry chain, automakers capable of producing 1-2 million vehicles need to seek second or even third sourcing options, or even directly invest in power batteries to change their bargaining position in the market. However, as in the case of Huawei’s decision not to build cars, this strategy has a deadline. With CATL’s downstream investments and dual direction of strategic movement, it is hard to say who will be China’s largest automaker in 2030, except for BYD.

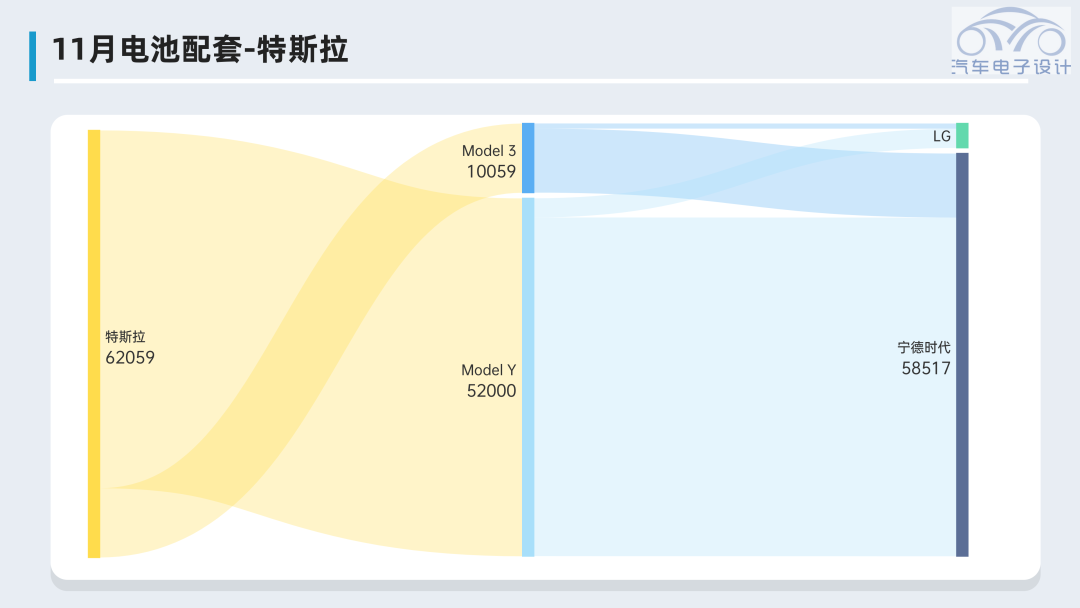

Lithium iron phosphate may indeed become the most important standardized product with regard to battery production costs. This is evidenced by the fact that Tesla uses it extensively and that various brands have made significant progress in its adoption, with the exception of joint ventures. In fact, for Tesla, the only thing it won’t be worrying about in 2022 is battery supply, since the 4680 battery’s mass production won’t be realized until 2023 (we’ve been watching Tesla experiment with it for a year).

BYD is 100%, Tesla is 94%, and Wuling and Changan are around 90%. While for companies in fierce competition, the level of adoption of lithium iron phosphate is very high.

The Situation of New Energy Vehicle Companies

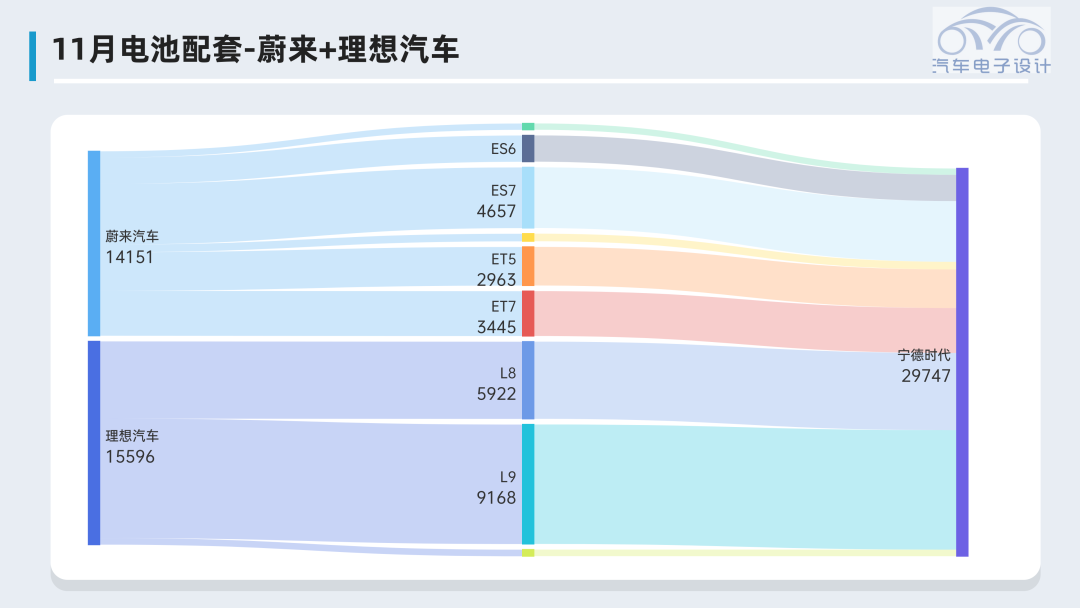

New energy vehicle (NEV) companies can be divided into three categories with respect to their relationship to CATL: those that are 100% affiliated with CATL (NIO and Xpeng), those that are highly affiliated with CATL (Hezhong), and those that are not affiliated with CATL (Lingpai and XPeng).### Single Supplier

Starting from 2023, there will be changes due to the adjustment of procurement relations. While the soaring battery prices were the first thing to burst out from the ideal vehicle side, it has been procured from a single supplier for so long in order to ensure supply chain stability, which is quite interesting.

Today, I went to see the range-extender series battery pack, which has a relatively large replaceable space.

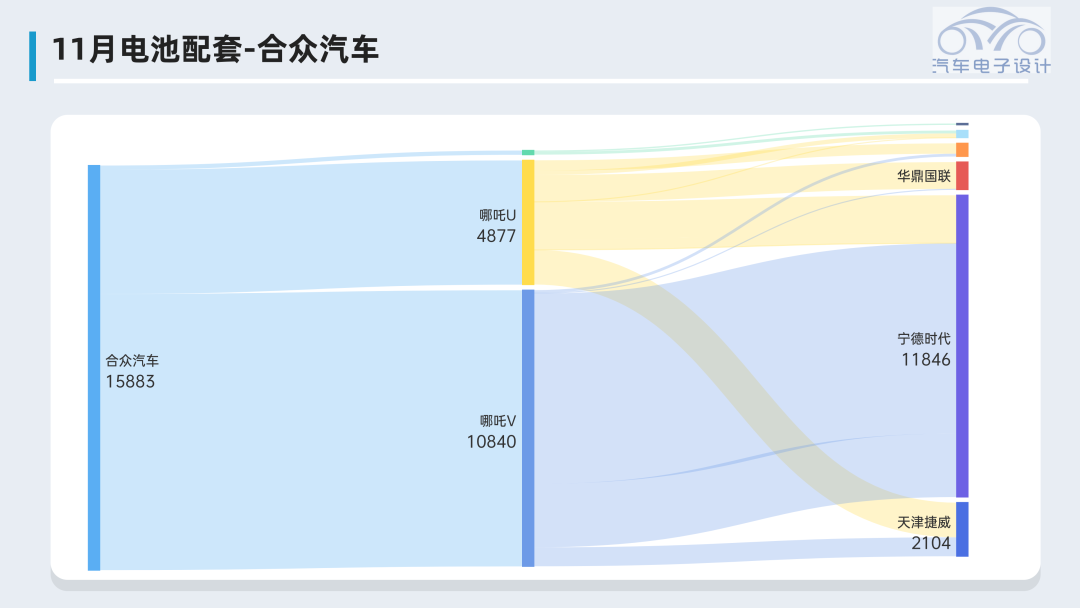

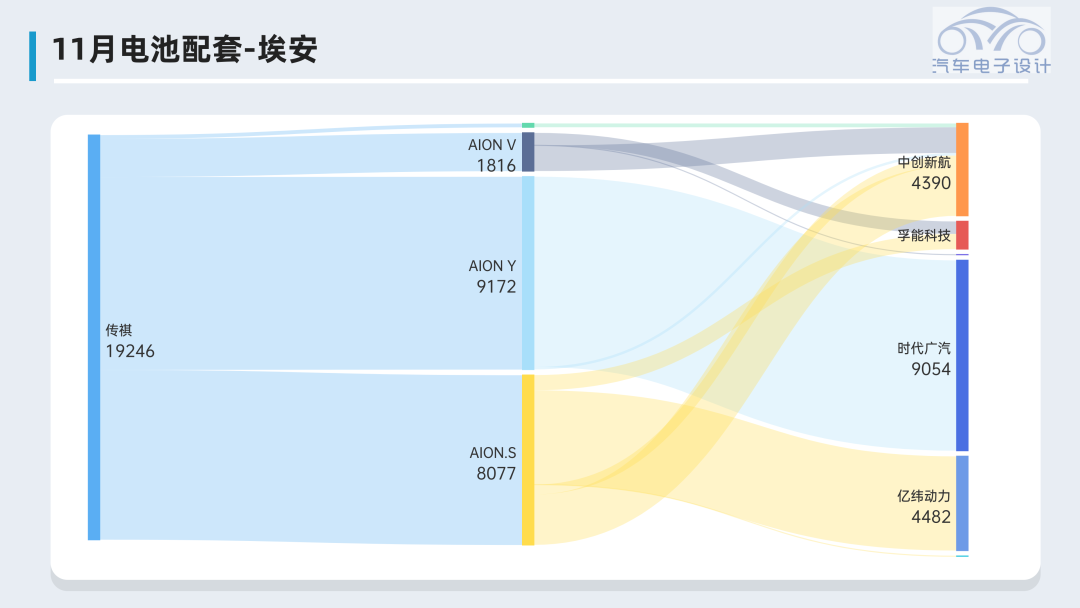

- Due to considerations from shareholders, while Hozon is striving for diversification, it is still supported by the shareholders.

- Both Leading Ideal One and Xpeng Motors are trying hard. Among the new forces, Leading Ideal One is the most thorough in the adoption of lithium iron phosphate.

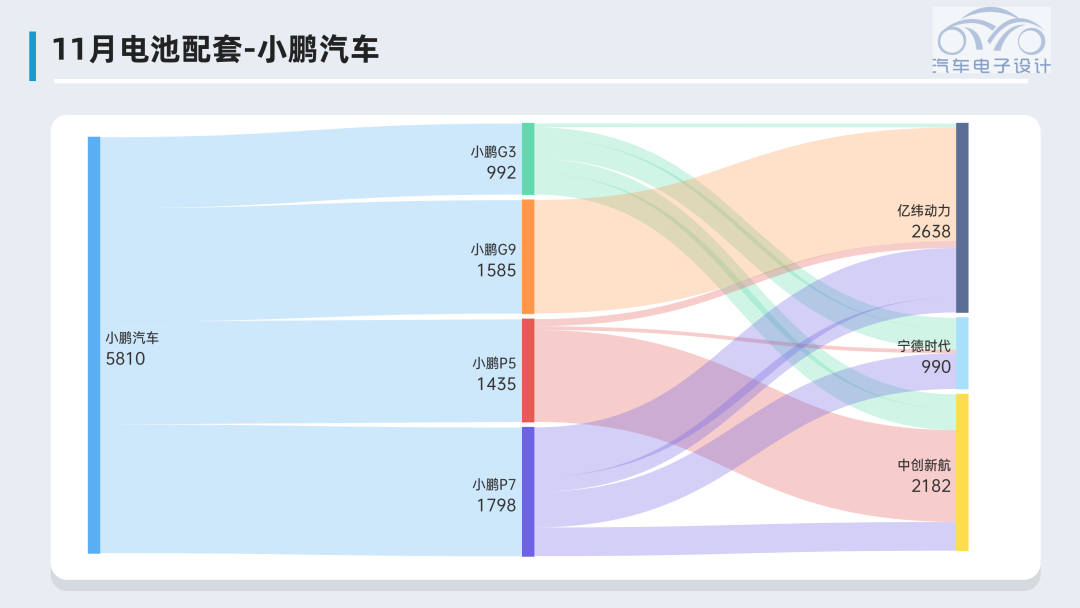

Further supply of G9 batteries will also increase, and there will be some changes in 2023.

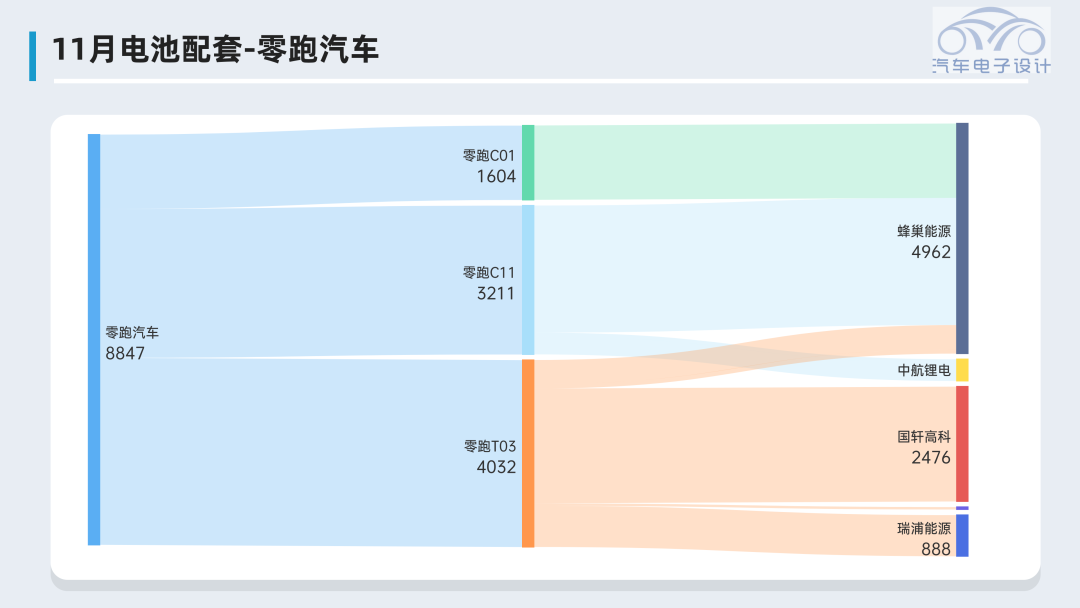

None of the new forces has formed a joint venture in the field of batteries. Their selection is relatively flexible, and it is something they consider a lot when growing towards a 500,000 scale. Competition is fierce, and balancing supply security and price is a dilemma. We also see that second-line battery companies are trying to bind some enterprises, and strive to use capacity and prices to grab some customers.

State-Owned and Private Enterprises

Let’s take a look at Enovate, which is a whole vehicle manufacturer that wants to make lithium iron phosphate by themselves. Currently, four battery cell companies allocate supplies.“`

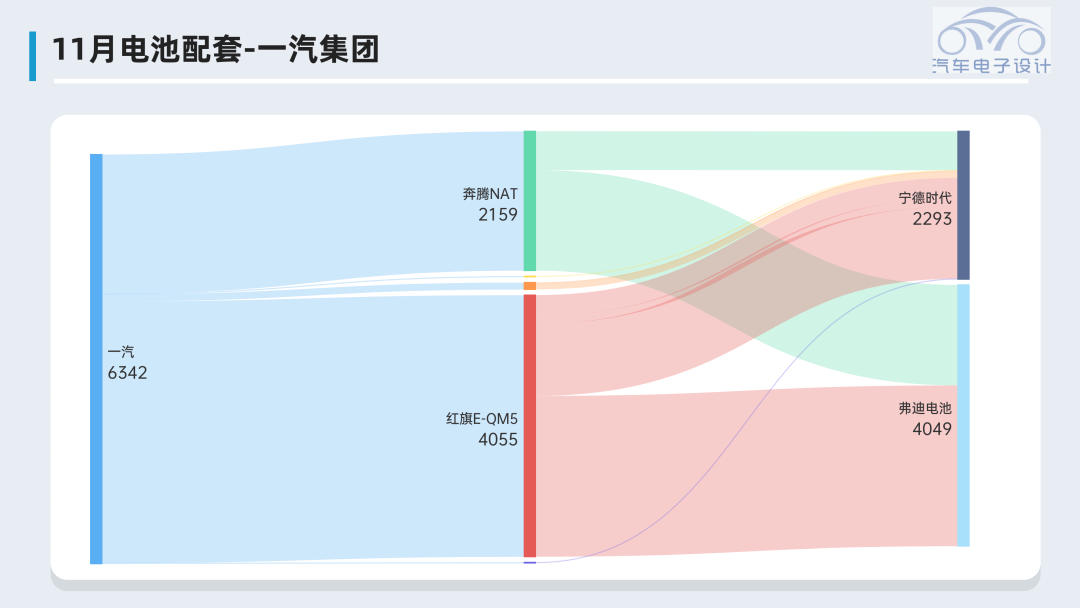

Next, let’s take a look at several state-owned enterprises that have achieved battery diversification despite rising battery costs. First Auto is mainly preparing for joint ventures with Ford.

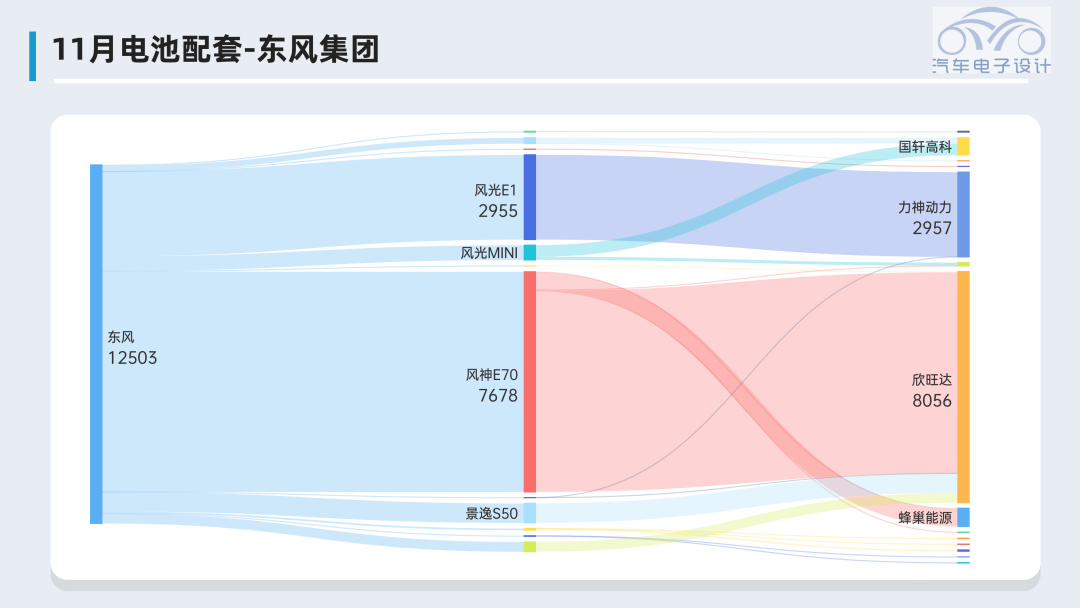

Dongfeng has introduced Xinwangda, Lishen, CATL, and Guoxuan and is also rapidly adopting iron-phosphate technology.

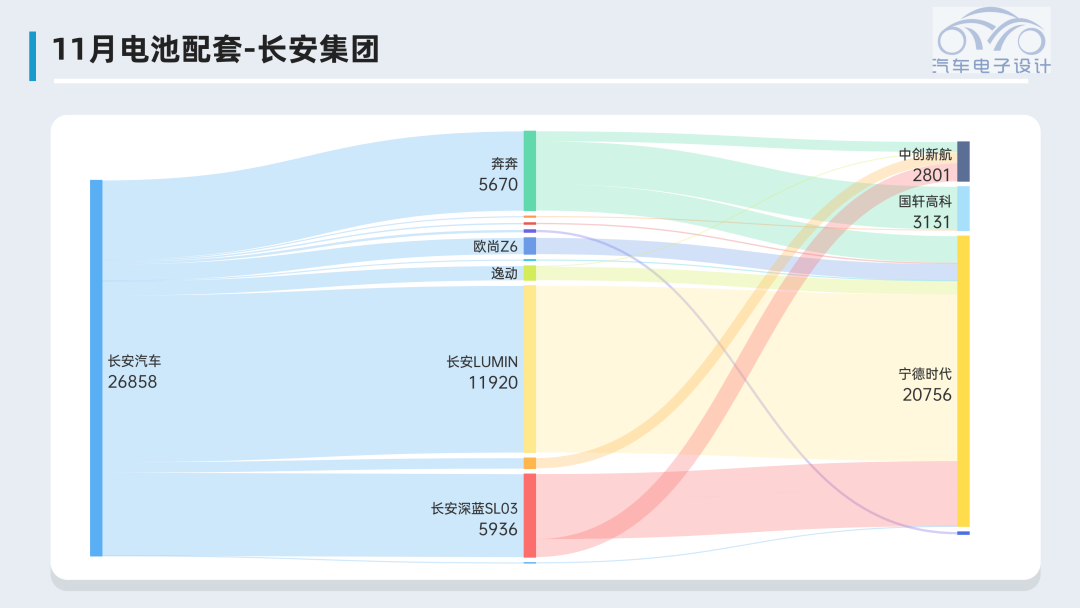

At public events, Changan complains that high battery prices are killing their business; however, in the second half of this year, Changan’s new energy vehicle sales have surged, and the company has been quickly adopting iron-phosphate batteries. It has also deepened cooperation with Ningde Times in 2022.

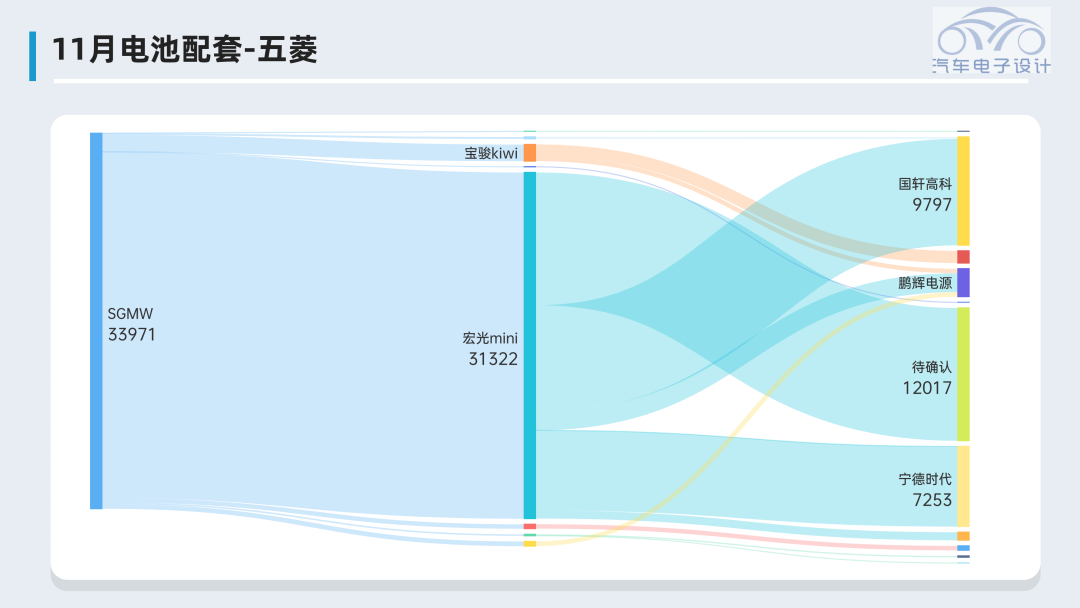

Wuling is a model of diversified procurement, with battery procurement needs evenly distributed each month.

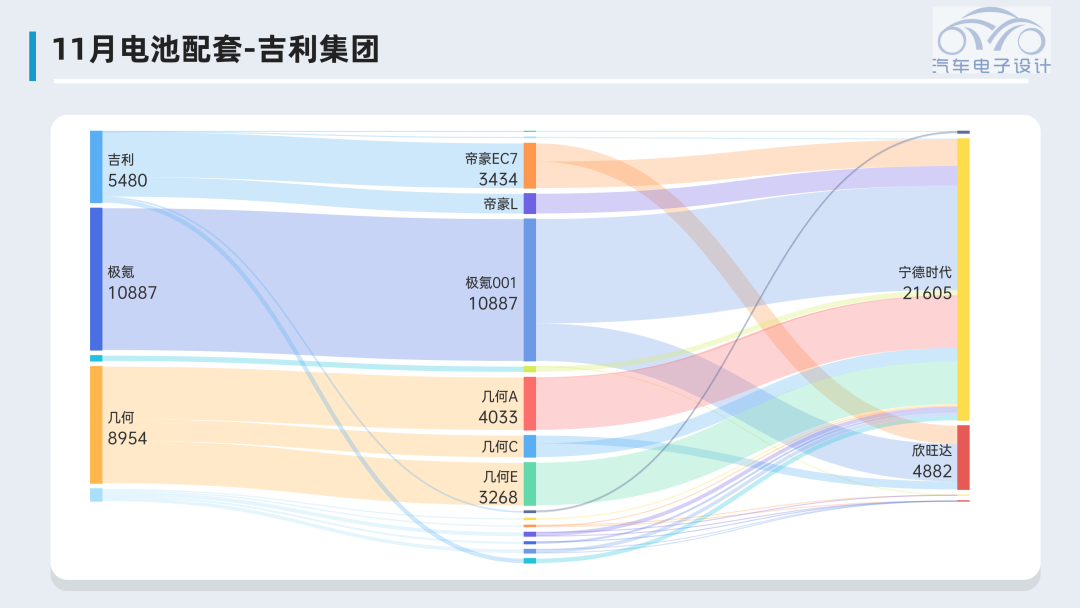

With the launch of the joint venture battery enterprise between Sichuan Auto and Ningde Times, Geely’s sales volume has increased rapidly this year.

“`

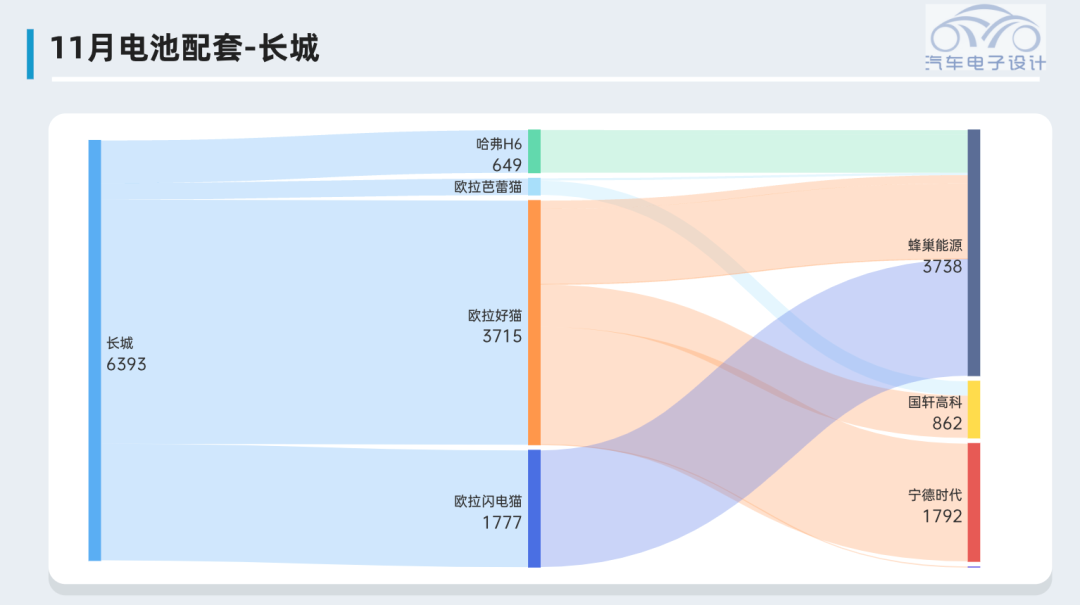

Longest part of PHEV on this side of the Great Wall is supplied with a considerable amount of honeycomb energy. Currently, Great Wall Motors’ battery honeycomb accounts for slightly more than half, and is supplied by Guoxuan High-tech and CATL.

Summary: I think 2023 is a big turning point. The problems that can be seen are very intense in the entire industry. The most important thing is that the previous long-tail customer model of battery factories cannot continue. It is impossible for most car companies to make a profit by making 100,000 pure electric vehicles. As the Matthew effect becomes more and more obvious, companies without bargaining power will eventually either fail or be acquired. Therefore, the pattern of the entire industry is facing who can make money and who can work. In the case of heavy internal competition, there are always winners and losers.

This article is a translation by ChatGPT of a Chinese report from 42HOW. If you have any questions about it, please email bd@42how.com.