Author: Zhu Yulong

Continuing with the first part of our passenger car December report:

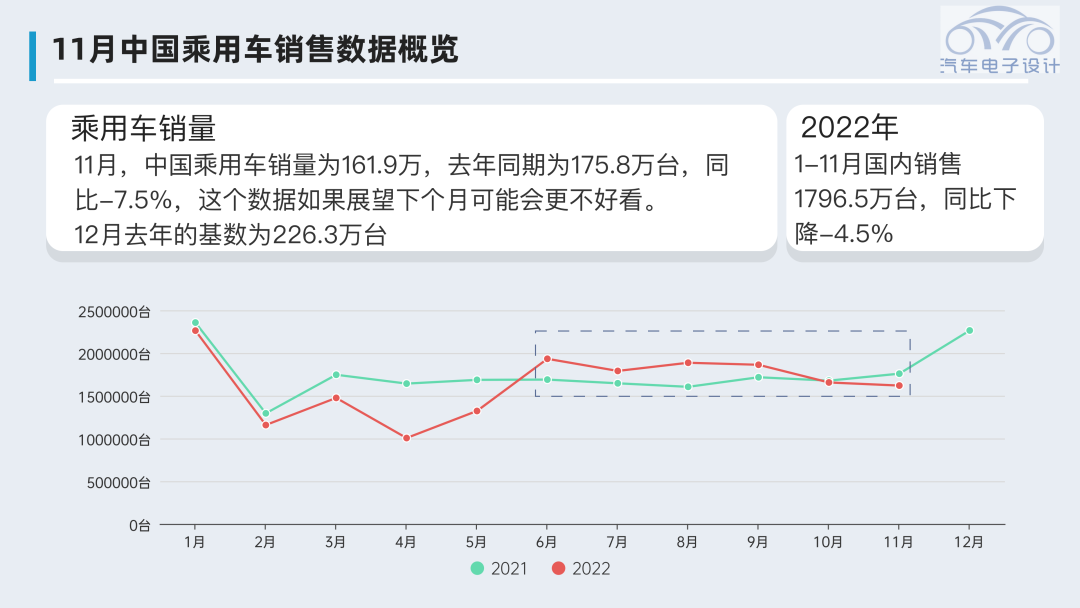

In November, Chinese passenger car sales reached 1.619 million, compared to 1.758 million during the same period last year, a decrease of 7.5%. This data might look even worse next month, considering that the baseline for December of last year was 2.263 million units. Currently, the year-on-year data for car sales does not look good. From an industrial point of view, this has been a tough year for the automotive industry.

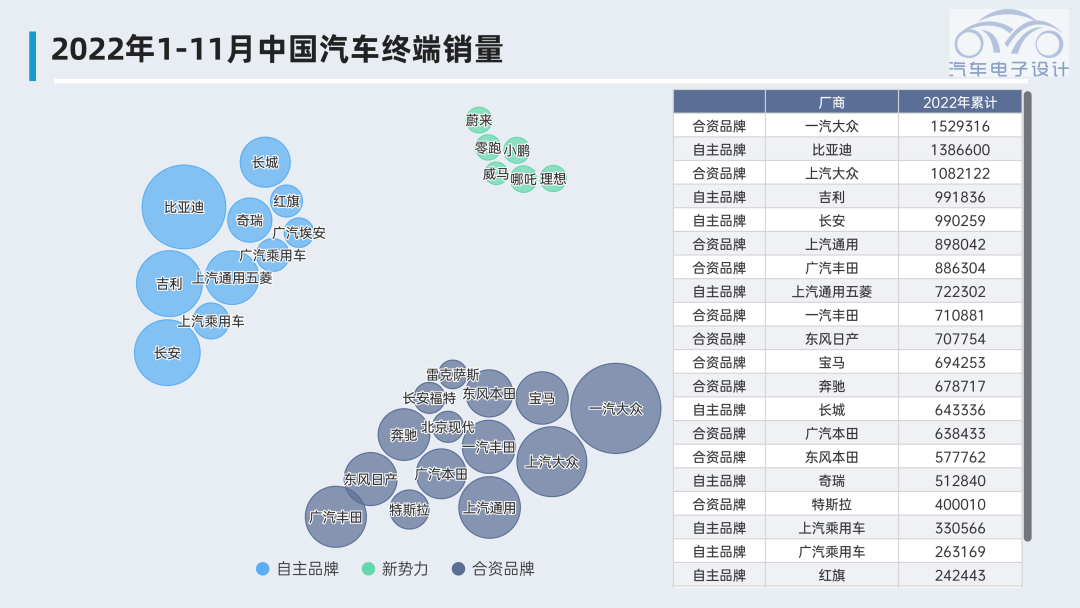

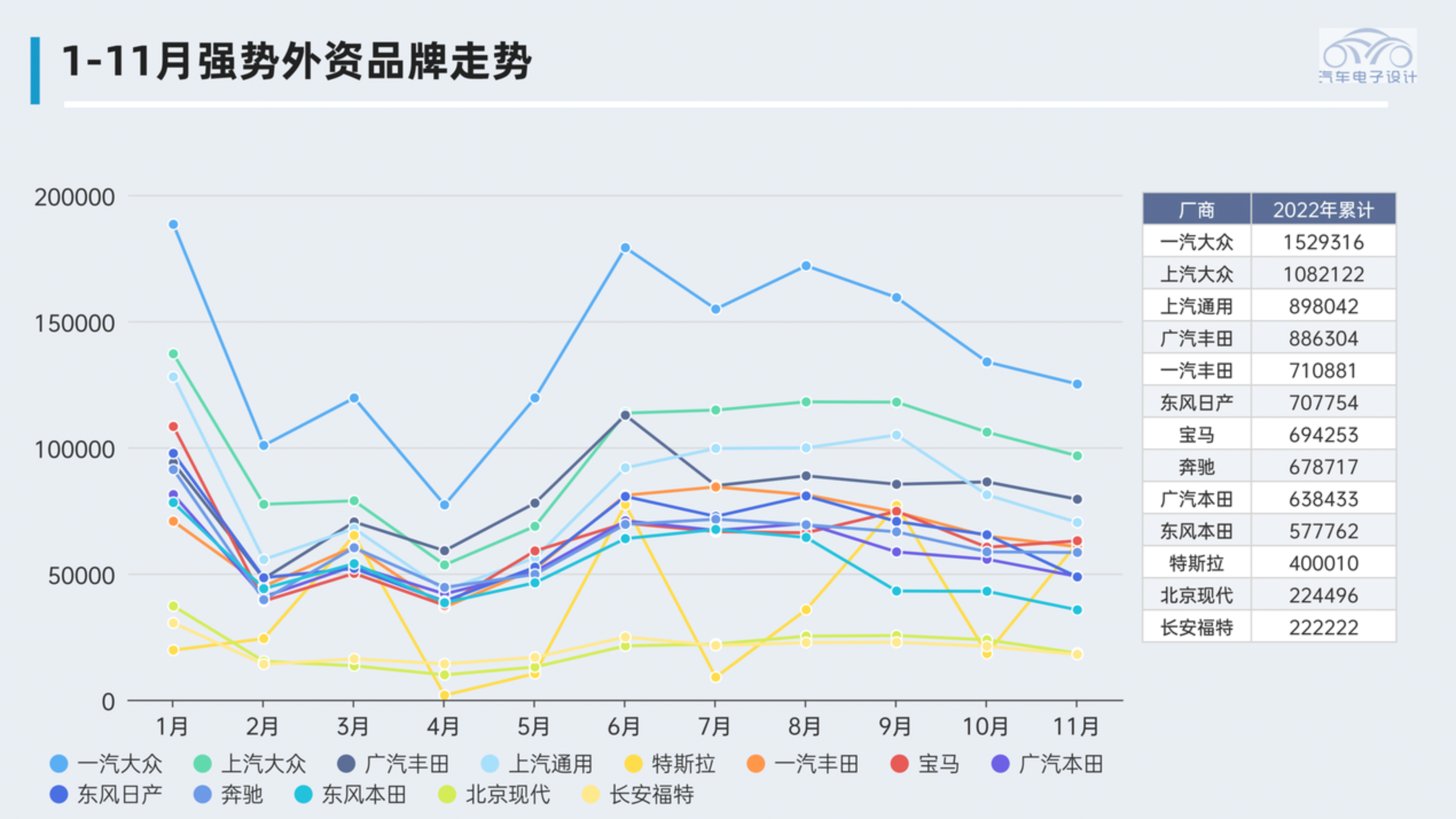

An overview of China’s domestic terminal automobile sales in the first 11 months can be seen in the following graph. We can see that during the economic adjustments, whether it is domestic brands, foreign-funded brands, or new players, all have gained market shares.

Overview of Automotive Enterprises

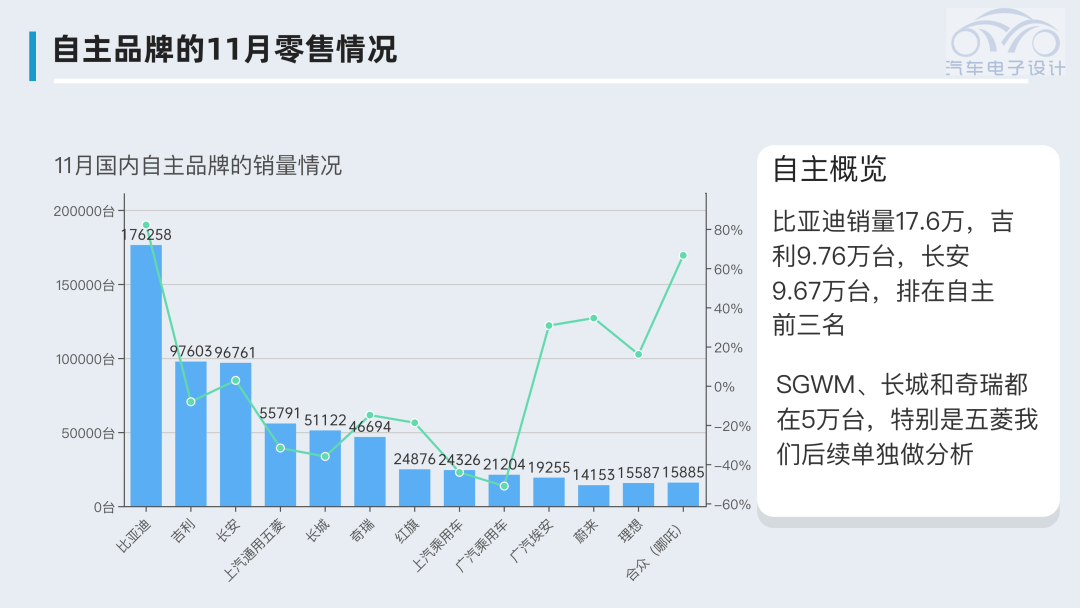

Domestic Brands

BYD, with a sales volume of 176,000, ranks first among domestic brands that are currently shifting towards new energy vehicles. Geely sold 97,600 units, and Changan sold 96,700 units, ranking second and third. SGWM, Great Wall, and Chery all sold around 50,000 units, and in particular, Wuling is mainly focusing on pure electric vehicles. We can see that traditional automotive enterprises with sales volumes of over 20,000 units are now competing with new energy vehicle enterprises with the same sales volume.

Next year will be the year of hybrid vehicles. Currently, domestic car companies focused on traditional fuel SUVs see the advantages of the DM-i powertrain (fuel efficiency, lower prices, and acceleration characteristics) and will likely follow this path. In the field of powertrains, wasted time can be compensated by adjusting the model cycle. The sales volumes of several companies below the third tier, less than 30,000, quickly reached a peak comparable to that of new energy vehicle companies. They are now in the elimination stage, and in order to maintain sales channels, product strength must be improved. If 4S stores do not make money, it is impossible to maintain continuous operation.“`markdown

备注:This series of figures does not include pickup trucks, which is also a very profitable market.

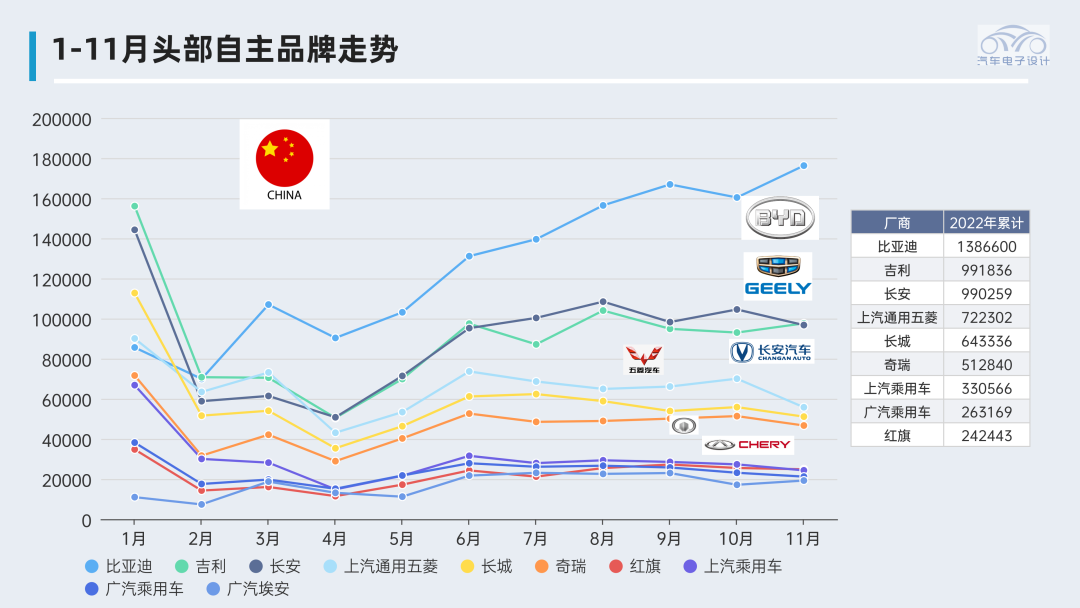

From the perspective of sales, BYD has shown a relatively independent trend after September, and the entire industry is facing challenges in Q4 terminal sales. This is just as President Qiu said, something we can all feel around us.

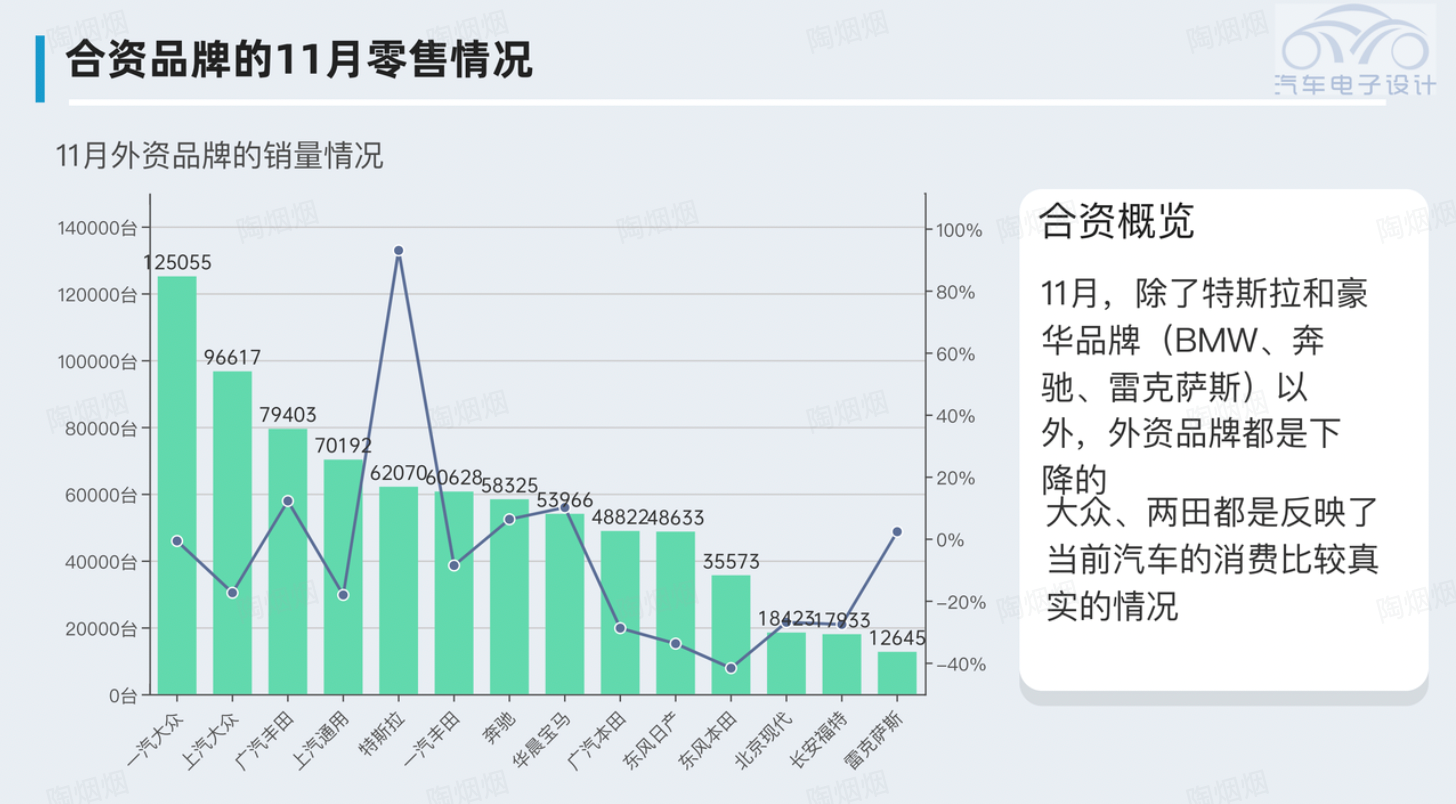

Foreign Brands

In January, except for Tesla and luxury brands (BMW, Mercedes-Benz, Lexus), foreign brands are all declining. Volkswagen and Toyota reflect the current situation of car consumption, and some things really need to be said. The entire Chinese auto industry, including the entire supply chain, is under enormous pressure. According to current conditions, it is possible that the entire auto sales will gradually recover after March 2023.

I understand that in the past three years, the management and execution planning of foreign companies, as well as product development, have not been sufficient in response to the Chinese market. Currently, fuel cars that can sell globally require significant localization in terms of fuel consumption, power, and technology in China. From the current observations, if joint ventures can undertake local development, there is still a chance. If we continue to wait for foreign product line updates, the market share of foreign brands may continue to decline.

“`

Actually, the process of the penetration rate of new energy vehicles is irreversible, and the high share of self-owned brands is also irreversible. Based on the current trend, we can see that more and more foreign brands will gradually withdraw from the Chinese market, and may clash again in Southeast Asia and the global market.

Thinking of Key Enterprises

BYD

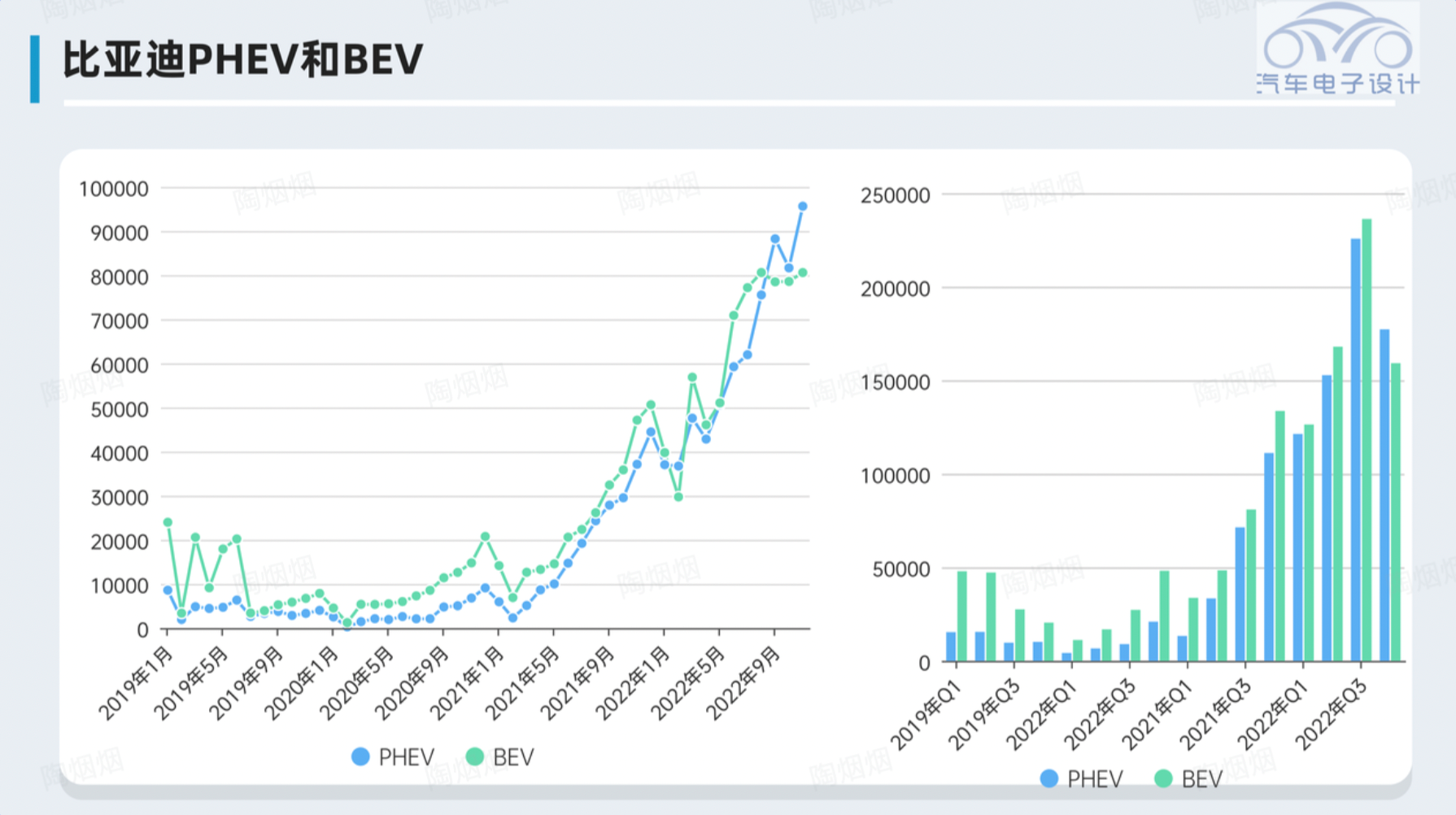

The most important thing about reviewing the rise of the current plug-in hybrid electric vehicle is to focus on the PHEV battery pack with lithium iron phosphate. The breakthrough here is to keep the cost of the 8kWh battery pack at a price of 1.1 yuan / Wh, which means the realization of a price of more than 10,000 yuan. This price, combined with an OBC, is almost the same as the price of Toyota’s HEV. Then this round of pricing mechanism, together with the fluctuations of oil prices, ignited the entire market. The original strategy of focusing on cities such as Shanghai, Hangzhou and Shenzhen has been completely overturned. Of course, the place where others cannot achieve it is to stop using gasoline cars. After losing the comparison of prices, consumers either choose PHEV or BEV.

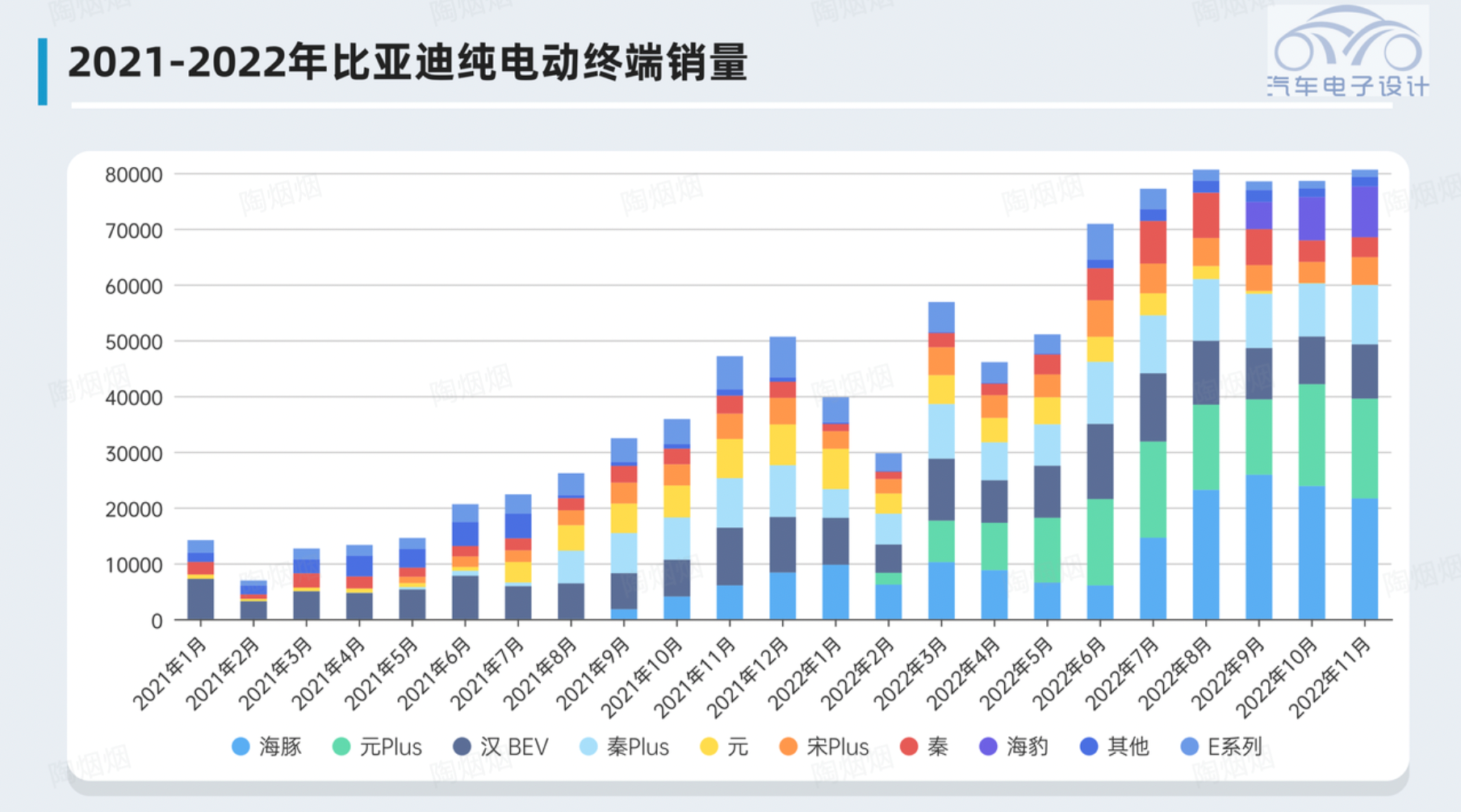

BYD’s sales of pure electric vehicles have a unique strategy.

◎ First of all, all batteries use a type of battery. In other words, as the price range of the lower-priced Dolphin and Yuan Plus expands, the scale of the entire battery procurement is also expanding. This gives BYD’s battery volume some bargaining power in the entire power market procurement, especially in the field of LFP. Except for Ning Wang, there is no third company that can do it.

◎ Secondly, in the field of drive systems, I recently analyzed and dismantled the design of the 8-in-1 system of Dolphins with my friends, which is quite unique. I have the opportunity to tell you about the design of this drive system in detail.

In essence, it is also a cost reduction through integration. As everyone’s prices are rising, it does make the impression that pure electric vehicles are more expensive than fuel vehicles due to battery reasons, and the new forces are flying with pure electric vehicles, which also deepens the willingness of ordinary consumers to buy BYD. This logic is a bit like the comparison of value for money. This brand has the highest cost performance after comparison, so objectively, this round of promotion is similar to the overflow effect of Tesla and the new force, and the sales area and stores covered also support this expansion.Of course, the problem is that BYD has used the most diligent method so far, which is to lower the price of Fudi to offer the most favorable price.

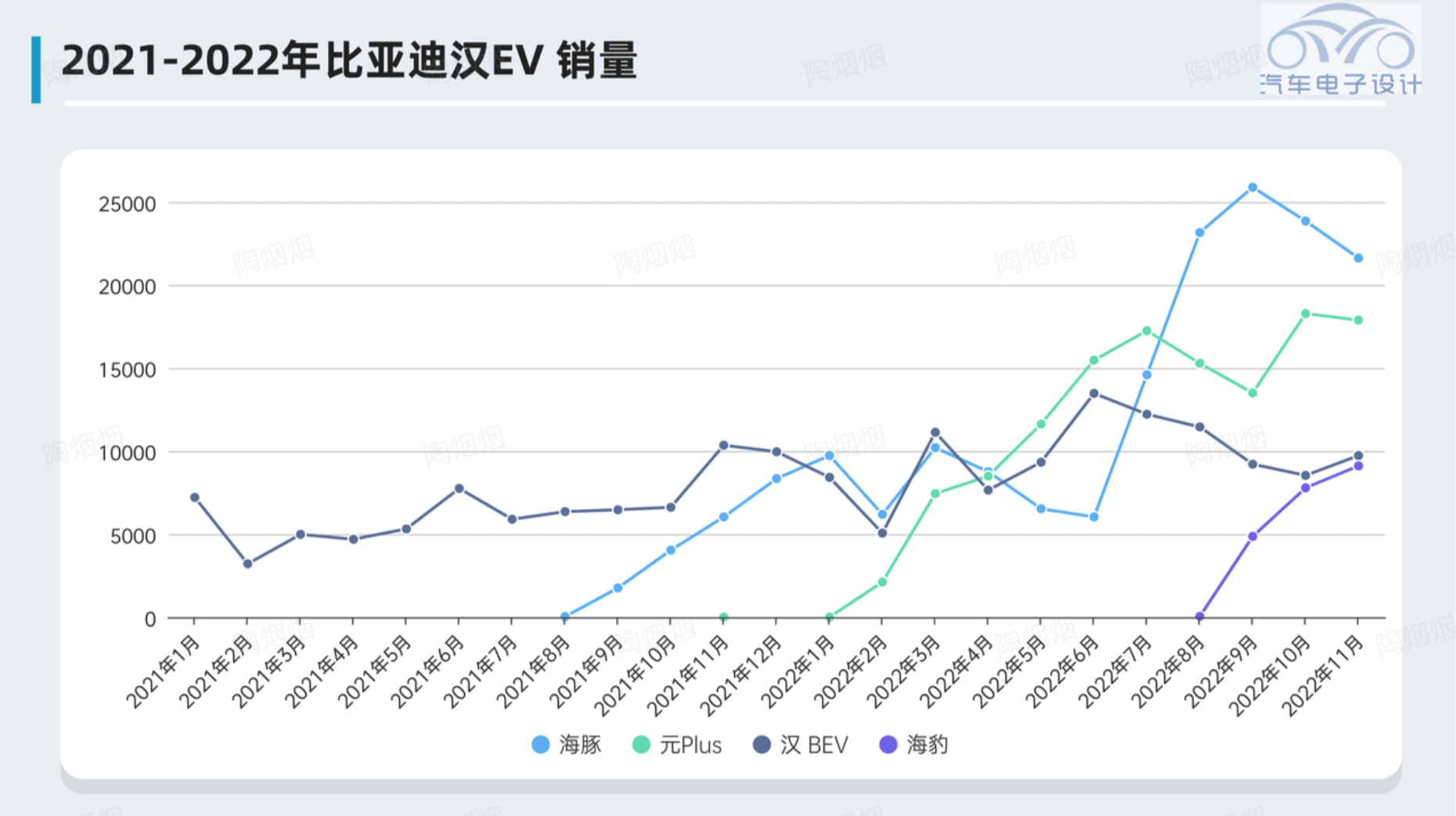

On the E3 platform model, to create differentiation, if we carefully compare, the sales volume of Han EV has not changed much. I put several other models together for a clearer comparison. I believe that for Chinese pure electric vehicles, further penetration requires a systemic solution, which is not just a matter for BYD as a single enterprise.

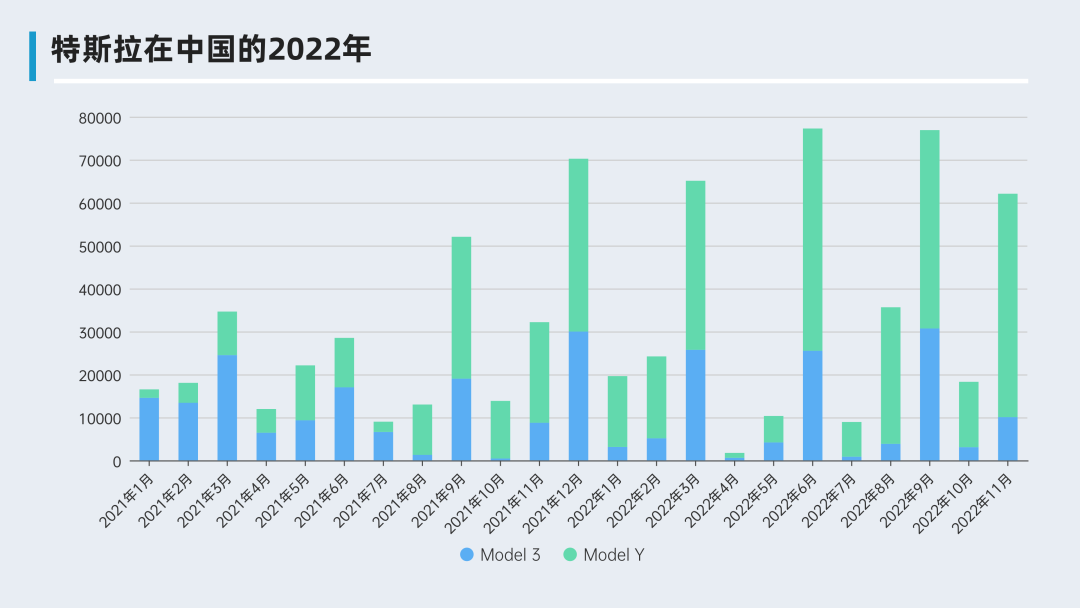

The biggest problem in the pure electric field in 2022 is that Elon Musk seems to be more concerned about other things this year and cannot bring breakthroughs to everyone in Tesla’s operations, especially since he lowered our expectations at the beginning of the year. If we remove the factors of subsidies and oil prices, where is the driving force for the next step of progress in pure electric?

In fact, everyone is looking for this. Previously, we looked for new things by studying Tesla’s product design and supply chain aspects. In 2022, we cannot rely on studying Tesla to make progress. This is my biggest feeling in 2022. The biggest sword has rusted, while new forces such as NIO and XPeng are trying to forge their own path and making gradual efforts.

Summary: This is the first half of the monthly report. For now, I am writing something on Weibo and gradually organizing it. In 2023, we need to work even harder!

This article is a translation by ChatGPT of a Chinese report from 42HOW. If you have any questions about it, please email bd@42how.com.