Guest Author | Zhu Yulong

Editor | Qiu Kaijun

The COVID-19 pandemic has hit various industries, and the new energy vehicle industry cannot be immune.

End-of-November terminal insurance data shows that automobile consumption is closely related to macroeconomic conditions and the objective environment currently faced. From the perspective of terminal data, consumer confidence in car purchases is currently decreasing. It may take until next spring for things to turn around.

Overall data for passenger cars

1) Overall data for passenger cars

This week’s total sales of passenger cars was 365,000, down 19.1% from the same period last year and down 8.8% from the previous week. If we add up the numbers for the past four weeks, the total is 1,479,000, roughly the same as last month. November and December are traditionally high points for China’s automobile market, but based on what we see, we can expect to see an overall downward trend.

2) New energy vehicles

Sales this week were 122,000, up 29.1% from the same period last year (a lower growth rate than the 100% increase seen in the first half of the year) and down 5.7% from the previous week.

3) Fuel vehicles

Sales were 243,000, down 32% from the same period last year and down 10% from the previous week. From the perspective of fuel vehicle data, the pandemic and macroeconomic conditions have had a particularly large impact. If we look at data from the past several weeks, we can see that fuel vehicle sales have not seen a peak, while the trend for new energy vehicles is similar to that of the overall market.

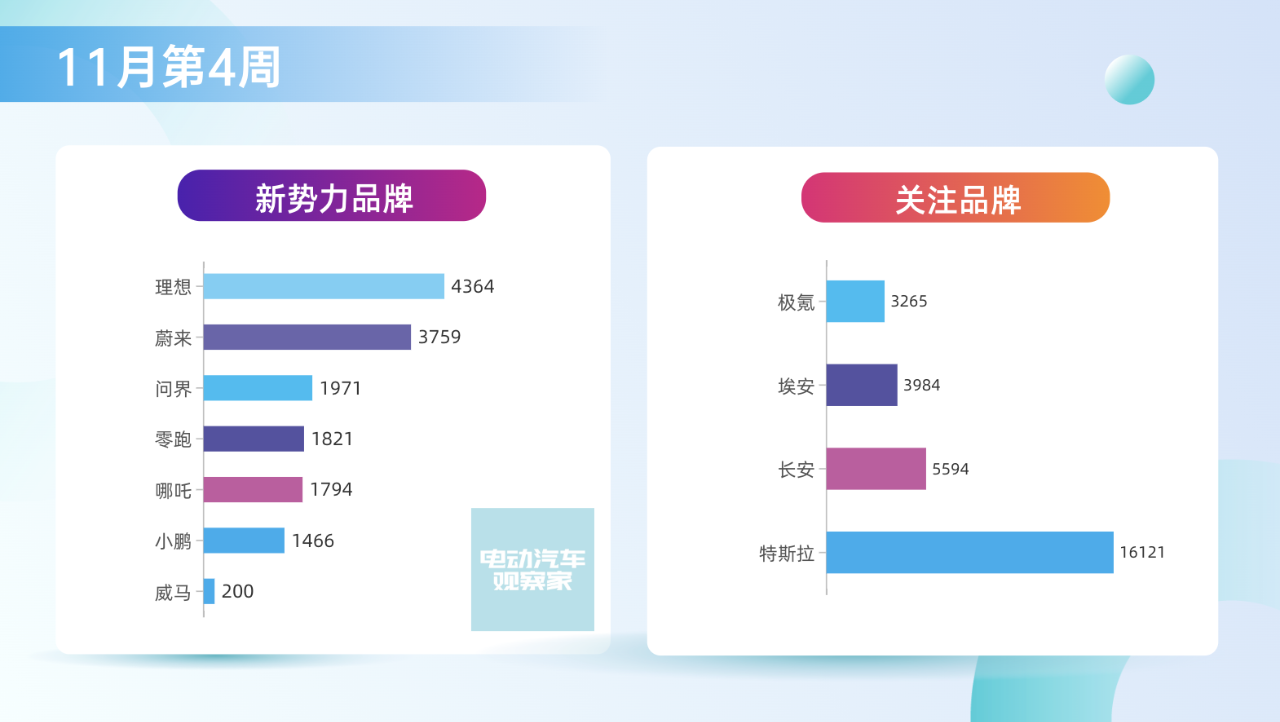

Major new energy vehicle brands

Here’s a look at the performance of major new energy vehicle brands.

BYD still leads the way, with 38,400 units sold in a single week and a total of 161,000 units sold over four weeks, with no challengers.

BYD still leads the way, with 38,400 units sold in a single week and a total of 161,000 units sold over four weeks, with no challengers.

Tesla sold 16,000 units in a single week and a total of 55,600 units over four weeks, which is still quite strong.

Wuling sold 7,253 units in a single week and a total of 31,000 units over four weeks, ranking in the top three and maintaining a relatively high level.

New Energy New Brand

Looking at the new forces, Ideal Auto is doing well this month, and NIO is in second place.

NIO sold 13,000 units in 28 days in November, and with the last two days added, it is estimated to sell 14,000 units in a single month. The weekly data for the ET5 model is starting to pick up, and the ES7 is currently the main selling model with few backorders. However, this depends on the brand’s production capacity.

Ideal Auto sold a total of 12,700 units in four weeks in November, and with two more days estimated to total 13,600 units. With the L8 ramping up, the overall structure is moving in a more normal direction. The L9 is priced high and is consuming the remaining orders, so the L8 will be the main model for Ideal Auto in the future.

In terms of other brands, WM Motor was greatly affected by the Chongqing epidemic; Leapmotor and Neta are currently in a period of model upgrades; XPeng’s G9 needs to be delivered quickly, otherwise it will fall behind; Tesla’s sales volume has not made a breakthrough in the short term; Zeekr has performed well this month, with weekly sales exceeding 3,200 units and monthly sales breaking 10,000.

Unfortunately, as the year-end approaches, there is no good news in the market. However, with the relaxation of epidemic control measures and the stimulus of buying cars at the end of the year, the situation may turn around.

This article is a translation by ChatGPT of a Chinese report from 42HOW. If you have any questions about it, please email bd@42how.com.