The Iron West District’s Li Zi

I still remember at the beginning of the year when each car manufacturer set ambitious sales targets, some even reaching millions. At that time, it appeared to be a grand stage, but our concern was that there wasn’t enough of a market to go around. However, due to issues with masks, especially this year with chip shortages at the start of the year and supply chain issues in the middle of the year, it is already difficult to survive. Therefore, everyone’s courage and hard work should be encouraged first.

Now, it’s already past the traditional high purchasing period known as “golden September and silver October,” and as the year comes to a close, let’s take a look at the progress of each car manufacturer’s annual sales targets to see who is who.

No one can reverse destiny

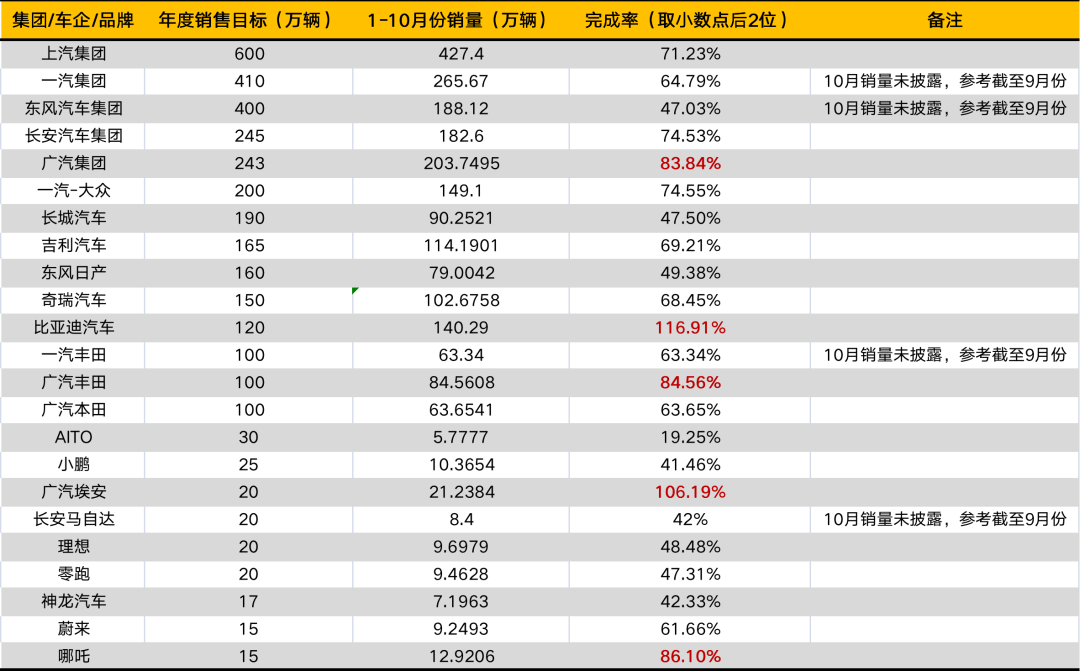

Below are some of the car manufacturers (including some brands) that we’ve collected and organized, with tables showing their annual KPI and sales from the first 10 months. Some of the sales values for October have not yet been announced, so September sales are used as a reference.

Firstly, two car manufacturers have exceeded their KPI. As of October, BYD and GAC Aeolus have respectively achieved their annual targets with 1.4029 million and 0.212 million vehicles sold, and even leaving school ahead of time.

Secondly, traditional car manufacturers are far more successful. In the rightmost column of the table, the excellent performers are all marked in red. If we don’t consider brands and only count car manufacturers, there are 3 companies with a completion rate of more than 80%: GAC Group and BYD, both of which are traditional car manufacturers, and NIO, which is a new car manufacturer. If we don’t consider manufacturers and only count brands, then there are 4 brands with a completion rate of more than 80%, and BYD, GAC Fengshen, GAC Aeolus, and NIO are all from traditional manufacturers.

Among excellent students, the advantages of traditional car manufacturers are already quite obvious. If we compare completion rates directly, the situation is even more one-sided.“`markdown

Looking at the completion rates in the new car industry, NIO has the highest completion rate, approaching 66.6%, while Xpeng and Li Auto both have completion rates below 50%, and even with Tesla included, its completion rate is just 60%, fixed at 61%. In contrast, traditional car companies, such as GAC, SAIC, FAW, Chery, and Geely, are all above 60%, not to mention BYD, which has already achieved its annual target 2 months ahead of schedule.

It can be predicted that by the end of this year, both GAC and NIO have a good chance of achieving their annual sales targets. GAC sold 212,000 vehicles in October, with cumulative sales of 2.0375 million, 400,000 units behind the annual KPI; NIO sold 18,000 vehicles in October, with cumulative sales of 129,200, 20,800 units behind the annual KPI. Based on the monthly sales volume in October, both companies have a good chance of making it.

In October, NIO sold 10,000, 5,000, and 10,000 vehicles respectively, all showing a month-on-month decline, with annual sales already having little to hope for.

Tesla has not yet released its October sales figures, but according to data from the China Passenger Car Association, Tesla China sold 72,000 units in October, down 14% from the previous month. Considering China’s huge share in its global market, its annual sales target of 150,000 vehicles is not optimistic.

Also worth mentioning is WM Motor, which has declared its annual sales target of 300,000 units to be hopeless, but sales in October exceeded 12,000 units, breaking the 10,000-unit mark for three consecutive months and becoming an important player in the new car camp.

With the dust having settled, where do traditional car companies win?

The huge channels and the unwavering support of dealers are a powerful assistance to traditional car companies.

“`Most people know that the sales model of new car manufacturing usually adopts direct sales plus agents, and agents only collect orders without buying and selling vehicles; while traditional car companies directly wholesale their products to dealers, which has laid the market advantage for this year. It is worth mentioning that the tension is a bit too high.

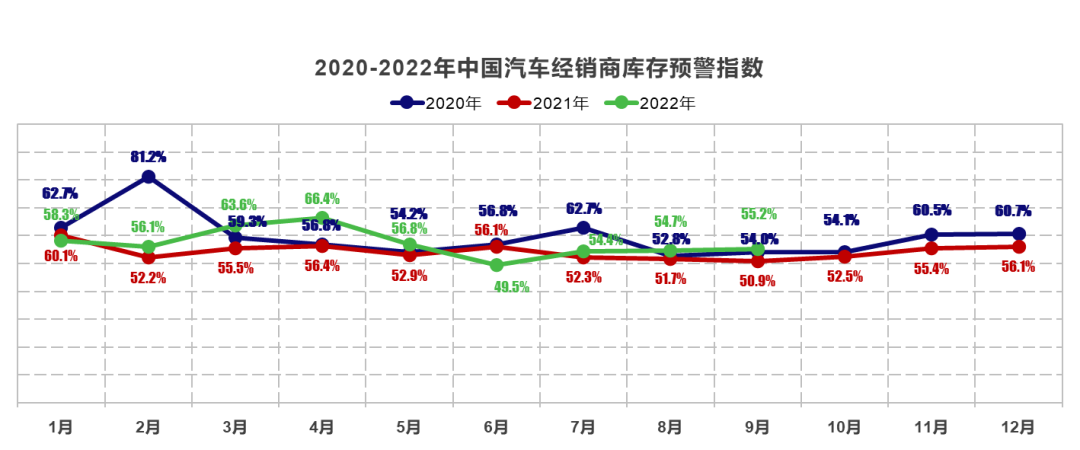

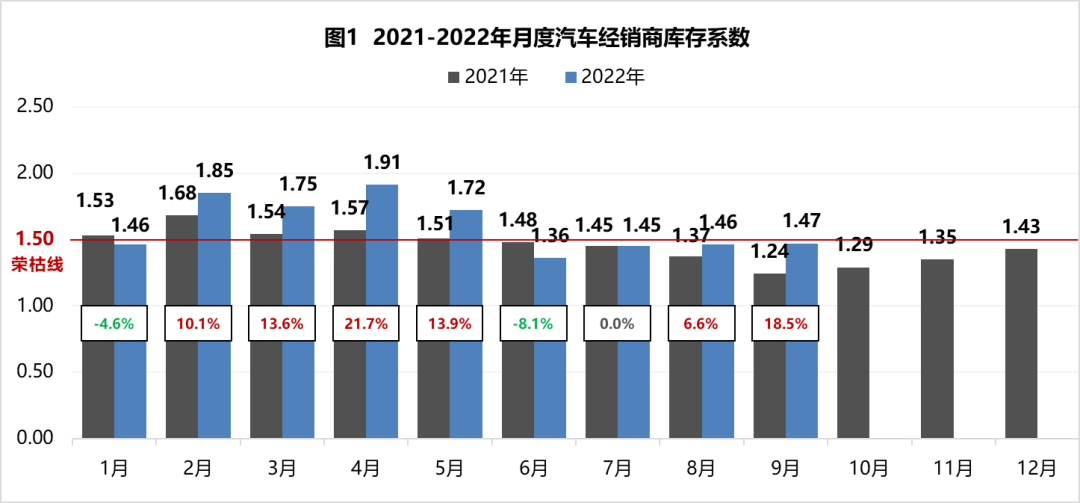

Let’s take a look at two statistical data from China Association of Automobile Manufacturers (CAAM):

By analyzing the statistical data of the inventory warning index and inventory coefficient, it can be clearly seen that dealers have undertaken greater pressure this year than last year. The impact of the epidemic is extremely critical. In 2021, car companies were worried about the epidemic recurrence and set conservative targets, easing the pressure on dealers. In 2022, car companies are generally optimistic, with growth targets exceeding 10%. However, the epidemic may reoccur unexpectedly.

It is worth mentioning that the reasonable range of the inventory coefficient in the internationally accepted cognitive standards should be between 0.8 and 1.2. However, the current situation in China is that a range below 1.5 can already be regarded as reasonable. In order to achieve the grand aspirations of the car companies, dealers have racked their brains.

The advantage of establishing the sales model is only temporary and the sales volume obtained by squeezing dealers may be inflated. The reason why traditional car companies have remained strong this year is their transformation into new energy. It can even be said that the real winner of the automotive market this year is neither traditional car companies nor new car manufacturers, but new energy vehicles.

Let’s take a look at the data from China Passenger Car Association (CPCA) as of this group (October statistics are not yet available, so let’s refer to September for now):

Among the top 15 gasoline car manufacturers in terms of sales from January to September, only GAC Toyota and Chery had a YoY growth of over 10%, while Changan, Geely, and GAC Honda had a slight YoY growth. The rest of the 10 companies experienced a decline, with a decline rate of over 10%.

Let’s take a look at the data from China Passenger Car Association:

Among the top 15 manufacturers of new energy vehicles in terms of sales from January to September, all of them are growing, and BYD, Geely, Chery, and Leapmotor have achieved at least double-digit growth. Both BYD and GAC, which have completed more than 70% of their annual KPIs, are ranked in the top 5 of this list of traditional automakers.

The dividend of firm transformation has already been released, but does this prove that traditional automakers have won?

No one can rest assured.

A new car is more able to define BYD’s future prospects than 1.4 million cumulative sales.

After a lukewarm first complete sales month, the sales of Hanbaobao skyrocketed in the past two months. In September and October, it achieved sales of more than 7,000 and 11,000 respectively. Together with the more-than-30,000 sales of the Han model, these two models contributed nearly 43,000 sales in October, and are expected to reach a monthly sales volume of over 50,000 in the future.

After an outstanding year, BYD’s true test is still ahead. Should it continue to extract dividends from previous generations of models like the Song, Qin, Yuan, and Tang, or should it tilt resources to develop the Han and Hanbaobao, the two models with true strategic significance? This is not a life-or-death decision, but it is enough to define its trend for the next few years.

In the “Li Xiao Wei” camp we often refer to, Ideal stands out as the indisputable winner. The first month after L9 delivery saw sales exceeding 10,000, with the October sales of the brand hitting 10,052 units. Considering ONE has been out of production since October, this means L9 has continued to sell in the thousands for the second consecutive month. For Ideal, the L9 model’s popularity not only means reaching the 400,000 sales mark, but more importantly, continuing the successful sales of the second model, laying a foundation for the brand’s image.

However, the real challenge will come after that, when Ideal faces the market of 200,000, or even 100,000 RMB level cars, and determines whether it can continue with its success. So far, only Tesla has achieved this.

In 2021, both NIO, Ideal, and Xpeng fell into the 90,000 annual sales range, setting targets for this year. NIO aimed at 150,000 sales, a growth of 50%; Idea aimed at 200,000 sales, a growth of 100%; Xpeng aimed at 250,000 sales, a growth of 150%. However, in the first 10 months of this year, their sales were only 92,493, 96,979, and 103,654, respectively, no match for their goals.

At least 50% growth was clearly defined, setting new car companies apart from traditional car manufacturers. Traditional car companies focus on growth while new ones aim to swallow up the market share of fuel cars with unprecedented speed, which was not yet achieved looking at the results of this year.But there’s no need to be surprised. Due to unstable production capacity and supply, sales fluctuations are common for XPeng and NIO. Thinking back, just last month everyone was saying “XPeng pulls ahead” and the next month they were saying “NIO meets crisis”. Such situations have occurred countless times. For them, this year’s disappointment can be fully endured; the real threat is Huawei’s strong entry into the market, which is as significant as expected. In the past, XPeng and NIO played the role of predators, but now they have to take on another role: prey.

Ultimately, insiders must be keen and not overlook any opportunities or loopholes, while we as spectators may as well be more dull. It’s only 2022 anyway.

This article is a translation by ChatGPT of a Chinese report from 42HOW. If you have any questions about it, please email bd@42how.com.