Author: Zhu Yulong

Yesterday, a friend approached me to discuss the alliances between car companies and chip enterprises in the chip industry. Combining with the PPT made by automotive research today, I would like to give a simple summary of the four types of strategic layout patterns adopted by domestic car companies in the chip industry from a broad perspective.

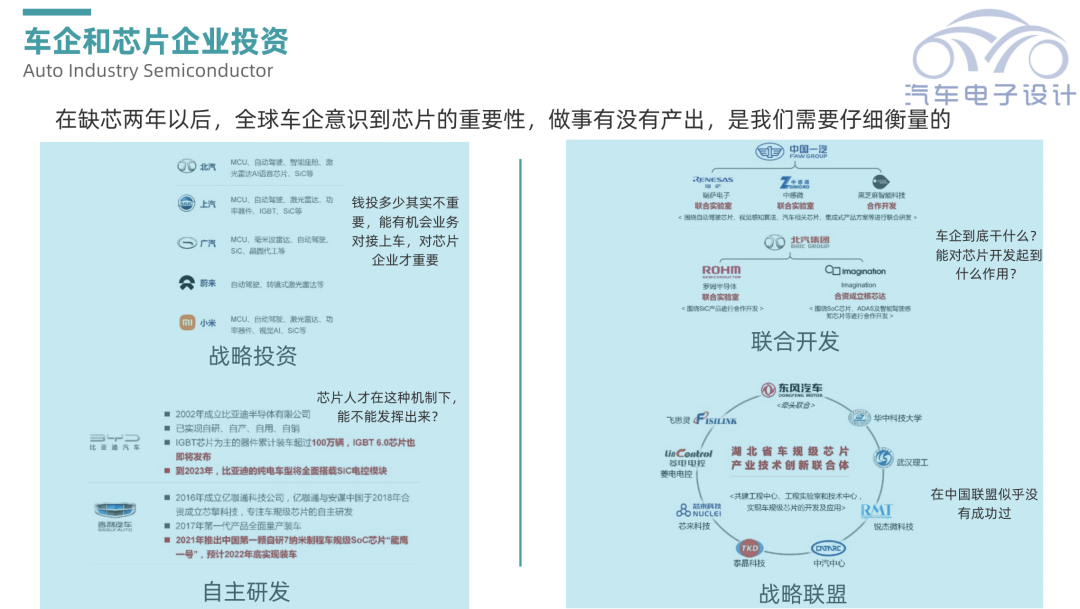

◎ Strategic Investment: Investing money through investment platforms.

◎ Self-research: Recruiting teams to develop chips. This approach is relatively challenging, since the investment in SOCs, even at a level of 10 million units, is too high for car companies. Currently, it is still feasible to make some progress at the power semiconductor level.

◎ Joint R&D: Customizing orders like crowning.

◎ Strategic Alliance: This is a type of strategy where, under the regional leadership, comprehensive management is conducted.

Different Strategies for Chip Layout

Let’s take a closer look at the different strategies:

Strategic Investments in Chip Startups by OEMs

Car companies choose their layout strategy based on the needs and resources of the chips themselves. Strategic investment is currently the most popular choice, and can also complete the tasks assigned by leaders. I think this type of investment cannot seize chip resources because the logic of investing in startups is different from that of mature enterprises like Infineon and NXP. The investment itself requires help in expanding channels, and taking over the startup would lead to failure.

However, this strategy has a low risk, as it has already produced results and is indeed the preferred tool for most car company groups.## Self-developed Chips in Automotive Industry

This strategy is less commonly used by traditional car companies and more commonly adopted by new startup companies. The core logic is that, through this wave, new startup companies expect to understand what needs to be done for chip development by conducting a thorough investigation. The benchmarking direction is companies like Tesla, which have done a lot of work in the semiconductor chip industry, and independent control of core chip technology is not realistic in the current stage.

Joint Development

This is a more common choice among domestic car companies. It is like sponsoring, combining with their own product needs (expressing their needs), and the development work is mostly completed by chip design companies. The overall risk is relatively small. This matter is also a business and procurement department-led initiative outside of the investment department. In my understanding, this is indeed a feasible way.

Strategic Alliances

In fact, from the current perspective, only the Yangtze River Delta and the Pearl River Delta have the potential for this area, with many car companies and semiconductor companies. Dongfeng Motor Group and eight other enterprises/institutions jointly established an innovation alliance to form a joint R&D force and to accelerate the development of chips. I believe that this matter is also a collaborative initiative on a meaningful level.

Strategic Choices of Different Companies

BYD

BYD Semiconductor is engaged in the research and development, production and sales of power semiconductors, intelligent control ICs, intelligent sensors, and optoelectronic semiconductors, covering the sensing, processing, and control of signals such as electricity, light, and magnetism. From the current perspective, power semiconductors sales accounted for the highest proportion due to the demand for electric vehicles, and self-sales account for the main factor, with TOP5 customer revenue accounting for nearly 70%. The small chips in the back, the product series that have been incubated, actually have no significant differentiation level in the entire Chinese chip field for automotive regulations.

Geely AutomobileThrough strategic investment and joint ventures, from the perspective of Xinqing, as an independent company, it aims to promote the development of large-scale SOC chips for autonomous research and development (cockpit and subsequent intelligent driving) to achieve self-control of Geely’s core technology for high-performance chips. This product direction includes a variety of chips such as intelligent cockpit, autonomous driving, and central processing units.

In my personal opinion, on the one hand, we need to keep up with the competition demand in the automotive industry from a product level, and on the other hand, we need enough chip talent to incubate and develop advanced products. The path is indeed difficult. However, we can see that this approach is feasible and impressive, after all, the investment in 7nm is costly, with a research and development cost of $100 million. Whether it can be achieved or not is another matter, but the money is definitely being invested.

SAIC Group

When it comes to SAIC, I believe we need to look at it from two perspectives. On the business level, the entire joint venture model is being challenged, which is inevitable. However, after so many years of joint ventures, they have accumulated some capabilities, starting from 2018, they began to lay out on a large scale in the field of chips, working with Infineon in the power semiconductor field initially, and then by investing in nearly 20 domestic top chip companies including Jingli Semiconductor, Xintai Technology, Cambricon, Sige Semiconductor, Zhanxin Electronics, Horizon Robotics, and Black Sesame Technologies through its subsidiaries SAIC Capital, Shangqi Capital, and Hengxu Kaplan, and reached a strategic cooperation with Shanghai Microelectronics Technology Industrial Research Institute. In terms of subsequent layout in manufacturing and design, I believe this approach still has value.Summary: Personally, I think the chemical reaction between the automobile industry and the semiconductor industry is still unclear. If it’s the traditional chips that support domestic alternatives in a chip-shortage environment, the requirements for chips have changed due to the transformation of EE architecture. On one hand, you need to ensure that previous car models have chips, and on the other hand, you need to develop chips for new car models. It takes a lot of effort to figure this out!

This article is a translation by ChatGPT of a Chinese report from 42HOW. If you have any questions about it, please email bd@42how.com.