Article | Financial Street Lao Li

Recently, there have been frequent lawsuits in the autonomous driving industry. Firstly, China’s leading autonomous driving company, Xiaoma Zhixing, sued Qintian Zhika, followed by Tesla being sued for false advertising about autonomous driving. Finally, on October 26th, with the successful listing of autonomous driving company Mobileye on NASDAQ, the lawsuit disputes have slightly subsided.

As a global leader in autonomous driving, Mobileye raised $861 million in this round of IPO, with a market value exceeding $23 billion. This was the fourth largest IPO on the US stock market this year and also the largest chip IPO. To be honest, this market value is not outstanding. Lao Li originally thought that Mobileye’s listing would bring a shot in the arm to the global autonomous driving industry, but the industry performance is not satisfactory. On the one hand, this is due to the “low tide” in the global capital market in recent years. On the other hand, the performance of the autonomous driving industry is “hard to lift”.

Compared with Mobileye, the road for Chinese autonomous driving companies is longer and more difficult. On this track, unicorns will be born, but trillion-dollar giants may not emerge. Today, Lao Li will share with us from the perspectives of capital and industry – what is autonomous driving? Where is the future of autonomous driving companies? What is the path to commercialization?

Complex Industry Chains, Diversified Products

The autonomous driving industry chain is more complex than the electrification industry chain, and the more complex the industry chain, the more difficult it is to achieve industrialization. This was Lao Li’s initial perception when entering the field of intelligent investment. After more than three years, this phenomenon has not changed.

When it comes to autonomous driving, we think of many companies, such as foreign companies like Tesla, Nvidia, Mobileye, Qualcomm, Luminar, and many more domestic companies, including vehicle manufacturers, Huawei, Baidu, Horizon Robotics, Xiaoma Zhixing, Weilan Zhixing, Yushiyuan Technology, Hesaitech, and others. The number of autonomous driving-related companies in the investment portfolio of Lao Li’s team alone exceeds 200.

The companies in this industry are generally divided into two directions that we are familiar with from a business perspective:

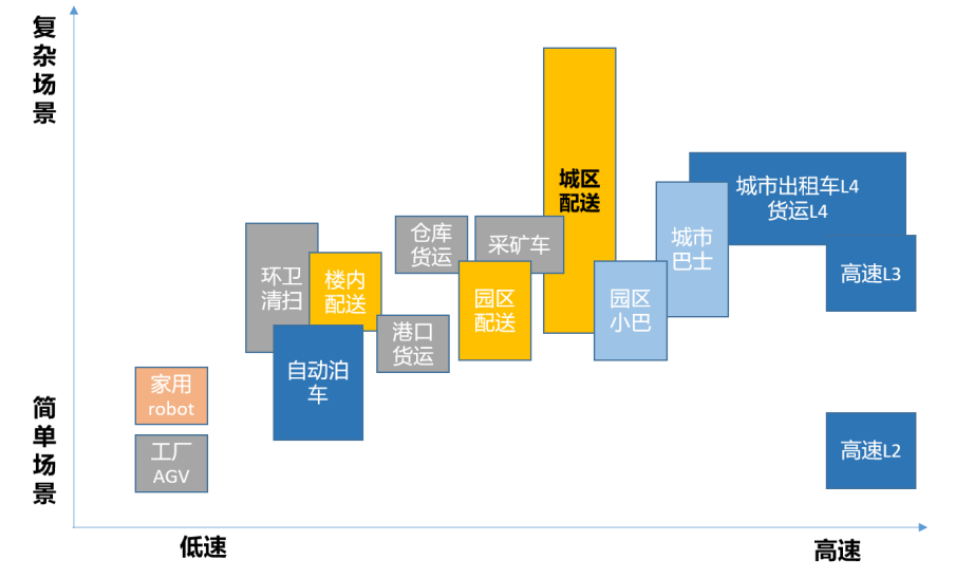

The first direction is the assisted driving direction. Generally refers to Level 3 and below of autonomous driving, which is currently the main layout direction of the entire vehicle industry, as well as the main selling point of new energy and intelligent vehicles. Compared to higher-level autonomous driving, the cost of carrying assisted driving equipment on a single vehicle is lower.

In this industry chain, there are a large number of mature foreign-funded companies, typical examples being ABCD – AutoLiv, Bosch, Continental, and Delphi. Although giants have split their businesses in recent years, they have always been dominating this field.

The second direction is higher-level autonomous driving. Generally refers to Level 4 and above of autonomous driving. This is currently the key development direction of domestic technology companies and autonomous driving companies. In fact, as of this year, domestic autonomous driving companies can only conduct trial operation services or testing services within a limited area and have not yet achieved industrialization.

From the perspective of the industry chain, autonomous driving includes the perception layer, decision-making layer, and execution layer. Broadly speaking, people are accustomed to collectively referred to the companies in the industry chain as autonomous driving companies, but narrowly speaking, only the companies in the decision-making layer can be considered as autonomous driving companies.

The decision-making layer is the most likely area for future giants to emerge, including whole vehicle companies, autonomous driving software companies, autonomous driving hardware companies, etc. The autonomous driving companies we are familiar with mostly focus on this area.

The decision-making layer is the most likely area for future giants to emerge, including whole vehicle companies, autonomous driving software companies, autonomous driving hardware companies, etc. The autonomous driving companies we are familiar with mostly focus on this area.

In this field, vehicle companies have the capital advantage, while start-ups have more innovative cells. In recent years, the capital market has mainly focused on start-ups. For example, companies such as Pony.ai, WeRide, UISEE, and AutoX mainly focus on autonomous driving solutions. Enterprises such as Momenta mainly focus on autonomous driving algorithms, while companies such as Geely and SAIC have also successively applied Momenta’s algorithms.

Some of these start-ups were born in Silicon Valley, and some were born in China. But overall, everyone has been developing for more than five years.

To be frank, compared with start-ups in the field of electrification, the development speed of autonomous driving is much slower. When CATL was founded for 5 years, it had already become a leader in the field of batteries at home and abroad. Even companies like EVE Energy and Guoxuan High-Tech have achieved industrialization more or less within 5 years.

Go left or right?

There are many companies in the decision-making layer. Today, Mr. Li mainly chats with you about several companies that develop autonomous driving solutions, such as Pony.ai, WeRide, UISEE, AutoX, and so on.

These companies are leaders in the field of autonomous driving solutions. Pony.ai is the largest in scale, Momenta is the most well-known, WeRide is more refined, and relatively speaking, the voices of UISEE and AutoX are weaker. In addition, there are also companies such as Great Wall Motor’s Hozon Auto. According to Mr. Li’s incomplete statistics, there are at least 30 companies developing L4 and above autonomous driving solutions in China under different scenarios.

Last year, Mr. Li was researching smart investing and overall, he found it difficult to evaluate these self-driving companies from a market value perspective. Regardless of the company, they have yet to achieve commercialization, and financial records show that their revenue is very poor. Many friends have said that this is a long-term track, but Mr. Li admits that this track is too long, so long that the capital market can no longer wait for an exit time. Therefore, Mr. Li believes that it is impossible for everyone to compare these companies horizontally based on market value.

In recent years, the capital market has put a lot of pressure on these companies, forcing them to engage in transformation and focus on achieving results. Currently, there are three main strategies:

- The first strategy focuses on developing L4 while also considering the development of L2;

- The second strategy still focuses on developing L4 and also aims to industrialize low-speed or segmented scenarios as it develops high-speed scenarios;

- The third strategy is to explore hardware development while developing software, because hardware is easier to industrialize than software.

The main representative of the first strategy is Momenta. From the year before last, Momenta established a “flywheel + double legs” dual-line layout, developing L4 self-driving while also taking into account L2 and ADAS businesses.

The second strategy is that of Pony.ai. When it comes to Pony.ai, people are most familiar with their Robotaxi for passenger cars. However, since 2021, Pony.ai has begun to enter new scenarios, such as researching and developing unmanned driving minibuses with Yutong, which are more easily implementable for commercial vehicles compared to passenger cars.

The third strategy is that of AutoX. Compared to the other companies, AutoX is the fastest growing and has the largest scale. AutoX was established in Silicon Valley in the US at the end of 2016 and for over 5 years, it has had a unique industry position in promoting technological innovation and promoting industrial development.

In April of this year, Pony.ai obtained the first “Unmanned Demonstration Application Road Test” notice for the intelligent connected vehicles policy pilot zone in Beijing. The company was allowed to provide “driverless travel services with no safety officer in the driver’s seat and a safety officer in the passenger seat” to the public, and gradually expand the testing range, time period and vehicle scale.

Moreover, unlike some L4 autonomous driving companies focusing on algorithm and software development when entering into the mass production of front-installed passenger cars, Pony.ai is the first L4 company to choose to start with self-researched domain controllers. Although entering the hardware field requires high investment, it is easier to demonstrate performance in financial reports.

Regardless of which strategy is adopted, the ultimate goal is to achieve commercialization.

The path to commercialization

For any industry to achieve development, mass production is undoubtedly the priority. At the beginning of 2021, when Waymo was preparing for an IPO, many analysts in the secondary market had a simple view at that time: if it could be mass-produced, the company’s market value would skyrocket; if it could not be mass-produced, everything would just be empty talk. To achieve full commercialization of autonomous driving, the first step is to solve technical problems, followed by mass production landing, and finally, cost-effectiveness considerations.

Using lithium batteries as an example, the industry achieved rapid development by solving technical problems, mass production landing, and cost-effectiveness. Hydrogen fuel cell vehicles are currently in the second stage – mass production landing, while autonomous driving is still in the first stage.

No matter Xiaoma Zhixing or Wenyuan Zhixing, the first problem they need to solve is the common challenge in the industry, which is to improve algorithm capability through road testing in different cities. Additionally, the front-loading production of autonomous driving technology requires a very complete development system and technical capabilities covering the entire core system of autonomous driving vehicles. To achieve successful mass production, the “barrel theory” must be followed, and there cannot be any shortcomings.

No matter Xiaoma Zhixing or Wenyuan Zhixing, the first problem they need to solve is the common challenge in the industry, which is to improve algorithm capability through road testing in different cities. Additionally, the front-loading production of autonomous driving technology requires a very complete development system and technical capabilities covering the entire core system of autonomous driving vehicles. To achieve successful mass production, the “barrel theory” must be followed, and there cannot be any shortcomings.

After achieving mass production, cost-effectiveness should be considered. Currently, the cost of high-level autonomous driving per vehicle is at the level of 300,000 yuan or even higher. At this cost level, it is difficult for autonomous driving to achieve commercialization, and the cost mainly comes from hardware. Therefore, the industry must work together to reduce system costs.

From the perspective of capital development, funds prefer small players rather than large players. Only in a track where small players compete with each other will the power of capital be amplified and achieve high returns.

For example, most funds do not want to see Huawei enter the field of autonomous driving. There are two reasons: First, giant companies like Huawei do not need financing and can quickly monopolize a certain subdivisional area with independent technology and funding; Second, giant companies mostly like to lay out the upstream industry chain, and investment opportunities for capital in upstream will be squeezed.

Since this year, many institutions, including Tsinghua University, have been promoting the “China solution” for intelligent connected vehicles. Many vehicle manufacturers also recognize this solution very well. The main reason is that the “China solution” has strong local and social attributes.

Intelligent connected vehicles are products with strong social and local attributes. When they are landed in China, they must meet and adapt to the requirements for the use and management of China’s transportation infrastructure and information and communication infrastructure, including traffic regulations, information communication standards, information security and data management, and relevant product standards.

This raises higher requirements for autonomous driving companies to pursue the full-stack R&D not only in algorithms, software, and autonomous driving domain controllers, but also to achieve end-to-end collaboration with “edge, management, and cloud”. Although this path is clear, there are still technical difficulties, mass production, and cost issues. Therefore, although the future is promising, autonomous driving still has a long way to go.

This raises higher requirements for autonomous driving companies to pursue the full-stack R&D not only in algorithms, software, and autonomous driving domain controllers, but also to achieve end-to-end collaboration with “edge, management, and cloud”. Although this path is clear, there are still technical difficulties, mass production, and cost issues. Therefore, although the future is promising, autonomous driving still has a long way to go.

This article is a translation by ChatGPT of a Chinese report from 42HOW. If you have any questions about it, please email bd@42how.com.