Author: Zhu Yulong

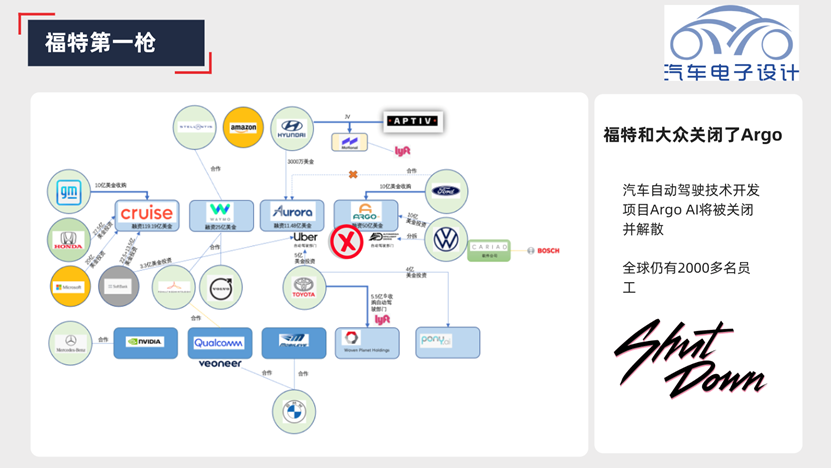

Recently, I just finished a video trying to explore the future of the entire L4 autonomous driving industry after the correction in the US stock market (https://www.42how.com/v2video/2601). Well, Ford fired the first shot right away–the autonomous driving technology project Argo AI, jointly invested by Ford and Volkswagen, will be shut down and disbanded. The start-up company led by former Google and Waymo engineer Bryan Salesky disbanded and notified its 2,000 employees, providing some of them with opportunities to work at these two automobile manufacturing companies.

On the track of autonomous driving, the first wave of foreign companies appeared around the idea of Mobility-as-a-Service (MSSB), with operations such as Waymo, Uber, and Lyft; following are General Motors, Ford, and later Toyota in the US, as well as US IT companies such as Amazon and Microsoft.

However, the overall situation is not very optimistic at the moment:

- Waymo is still struggling

- Argo AI disbanded

- Cruise: lost 1.4 billion US dollars from January to September

- Aurora: net losses in the first half of the year increased from 182 million US dollars last year to 1.231 billion US dollars.

The Beginning of Technology Companies

Based on logic, this wave of autonomous driving is mainly led by Waymo, regardless of whether it is Robot Taxi or Truck, followed by Uber and Lyft who see the expansion of their own business models.The commercialization of autonomous driving taxi services led by Waymo (the leader in the field) can be divided into five steps:

- Creating prototype autonomous vehicles for operation on specific roads.

- Obtaining autonomous driving testing licenses and conducting road tests with safety drivers.

- Launching a small fleet for testing passenger service, gradually expanding the geographic fence.

- Mass producing autonomous vehicles, upgrading first and second generation models, and supporting large-scale robot taxi services.

- Building and operating a robot taxi network, expanding to more service areas.

The core strategy of the robot taxi launch is to test and release services within a restricted geographic fence, and then continually expand the area to add more vehicles to the operating fleet. Waymo’s first-generation vehicles were based on traditional mass-produced models, retrofitted with perception sensors and computing platforms to achieve L4 autonomous driving.

The story of Waymo began with a focus on first-generation vehicles, establishing a factory in Michigan for retrofits of autonomous driving vehicles, starting with 60,000 Pacifica Hybrids and 20,000 Jaguar I-Pace EVs. This plan proved to be unfeasible, specifically because the I-Pace EV had already reached the end of its lifecycle. Waymo then began searching for second-generation robot taxi vehicles, designed for autonomous driving services (removing steering and braking), albeit with a slow progress. General Cruise is relatively fast in this aspect, as carmakers have their own advantages.

Currently, the biggest problem is that players continue to exit the market, while there are no new entrants showing continuous expansion.# Autonomous driving exit list

Uber was the first to exit, abandoning the burning, fiercely competitive, and still unprofitable autonomous driving service to Aurora; then Lyft also left the game, selling its autonomous driving service to Toyota’s Woven. Apple, Amazon, Microsoft, and other tech companies that were expected by the market continued to focus on investment and did not participate in this game. In the United States, Waymo and Cruise lead the way, followed by some followers, while most European automakers have withdrawn from the competition of Robot Taxi.

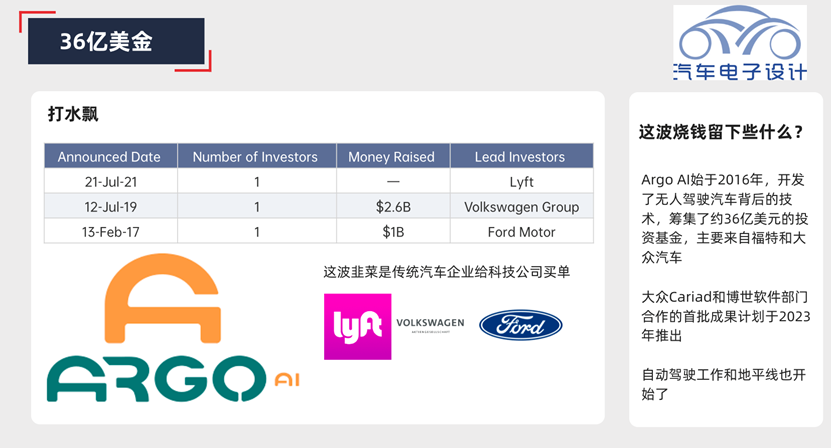

The liquidation of Argo has a significant impact on the investment in autonomous driving in Europe and America.

The flawed $3.6 billion plan of Volkswagen and Ford vs. The Tesla approach

From the perspective of investment logic, this wave of exits has indeed hurt Volkswagen and Ford.

The Robot Taxi service network released by Tesla in 2019 opened up a new way of thinking for this idea through the iterative path of its already sold car models. That is to say, the enterprise does not need to transform the autonomous driving car so thoroughly; by adopting a shadow mode to obtain more data around the existing car model, it can achieve iteration.

Therefore, as things stand, we see that all companies ultimately start from mass-produced cars, and the competition in autonomous driving assistance has returned to L2+. Whether they can improve the upper limit of the original functions through the iteration of autonomous driving computing power by running algorithms through the existing and available functions is the key.The change in this logic directly affects the speed of investment in autonomous driving beyond 2020. The most significant changes include:

-

Controllable cost of perception hardware: This revolves around whether expensive mechanical LiDAR is needed for panoramic scanning, whether multiple redundant perceptions are needed, and what the cost of the entire perception suite should be set at.

-

Balance between on-board computational power and cloud computational power: With last year’s Tesla Auto-Driving Day, a clear idea was given that on-board computational power can be iterated to a certain extent for cooperation with cloud servers.

-

Software development: Algorithms can be pruned from suppliers, and automakers need their own integration and optimization departments. Following this train of thought, similar to Volkswagen’s cooperation with Bosch and Horizon.

Conclusion: Everyone is now wondering whether traditional car companies can operate their software centers well, and this is a big question mark.

This article is a translation by ChatGPT of a Chinese report from 42HOW. If you have any questions about it, please email bd@42how.com.