Author: Zhu Yulong

In August 2022, US President Biden officially signed the “Inflation reduction act”, which plans to invest $369 billion to focus on supporting the development of clean energy industries such as electric vehicles and photovoltaics. This bill is obviously learning and drawing on the advantages of China’s new energy vehicle industry policy. It is good news for the US industry chain, but there are challenges and opportunities for China’s battery and parts industry chain.

Today, let’s talk about this topic.

Review of China’s New Energy Vehicle Industry Policy

First, let’s review China’s new energy vehicle industry policy. China’s new energy vehicle policy is a combination of policies, including: new energy vehicle subsidy policy; technology roadmap; whitelist.

New Energy Vehicle Subsidy Policy

◎ China’s new energy vehicle development process started from the “Ten cities and thousand vehicles” demonstration project in 2009.

◎ In 2010, new energy vehicles were listed as one of China’s seven strategic emerging industries.

◎ In June 2012, the State Council clarified that the central government would provide subsidies for pilot purchases.

◎ In 2014, it was proposed that “developing new energy vehicles is the only way to become a powerful automobile country” and exempt from vehicle purchase tax.

◎ Starting in 2017, the country began to raise the threshold for the recommended vehicle catalog and dynamically adjust it, and began to subsidize the decline.

◎ In the first half of 2020, affected by the COVID-19 pandemic, the new energy vehicle financial policy subsidy was extended to 2022.

Whitelist

In order to guide the standardized development of the automobile power battery industry, in March 2015, the Ministry of Industry and Information Technology formulated the “Regulatory conditions for the automobile power battery industry”, which is called the “Power Battery White List” by the industry, and only new energy vehicles using batteries on the “White List” can receive subsidies.The Chinese government’s financial subsidies and battery white list have effectively promoted sustained investment in China’s new energy vehicle industry and laid a foundation for China’s dominant position in the global battery industry chain.

The impact of IRA policy in the United States, and the eagerness of Japanese and Korean battery companies

After discussing Chinese policies, let’s take a look at how the United States plagiarizes:

- According to IRA regulations, only electric vehicles assembled in North America can enjoy tax credits.

- New electric vehicles can enjoy a tax credit of $7,500, while the subsidy for used new energy vehicles is $4,000.

- New energy vehicles put into use before 2024 must ensure that their battery raw materials come from the United States or countries in free trade agreements, and this proportion will gradually increase to 80% over the years.

This clause is similar to China’s “Power Battery White List” and can be called the American version of the “Power Battery White List.”

It can be seen that this policy is completely learning from China. The effect of the policy is also very obvious, directly stimulating the investment boom in American battery and electric vehicle super factories, with a planned investment of over 40 billion US dollars.

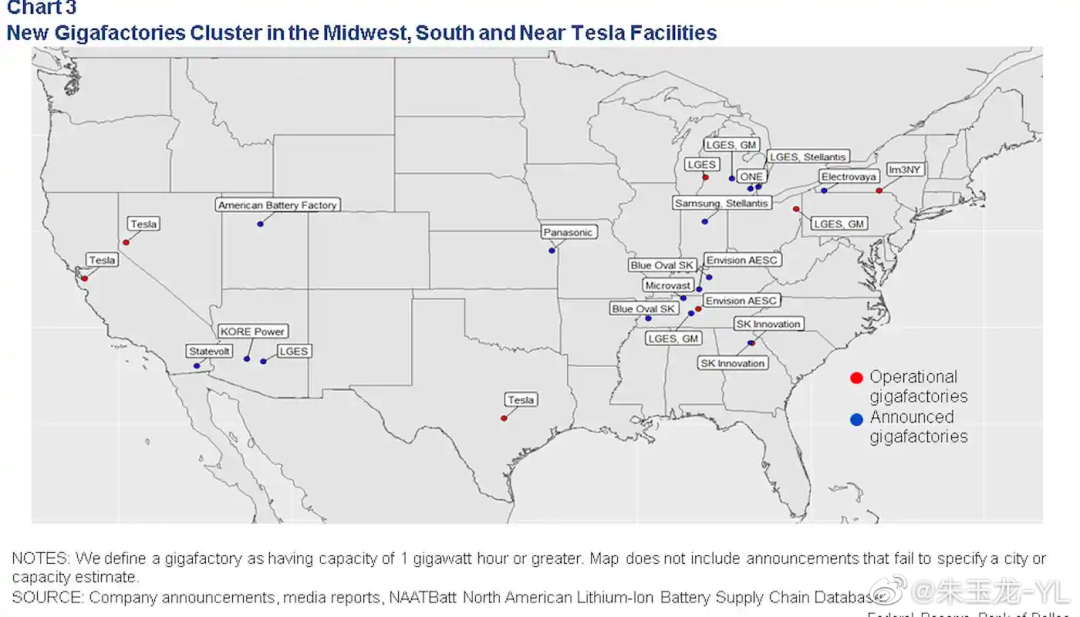

The early production capacity of the domestic battery industry in the United States was relatively weak. Since the beginning of 2021, there have been 15 battery projects in the United States, and the production capacity is expected to increase by more than five times by 2026. By 2031, the production capacity is expected to increase by 86%. Most of the newly announced super factories are located in the same geographical area, which is also called the “American Battery Belt.”

We can see that Japanese and South Korean battery companies and American auto companies are very active in the American Battery Belt.

According to this plan, the United States will develop an independent battery industry chain.

The brewing battery and material plans in Europe, and Volkswagen’s plan to build a self-owned battery plantAfter discussing the United States, it is clear that Europe has similar policies.

A total of 38 battery super factories have been built or are being constructed in Europe, with a total expected annual production capacity of 1TWh, equivalent to producing 16.7 million pure electric vehicles, with a total investment of over 40 billion euros. As these factories are put into operation, the production of batteries for electric vehicles in Europe is expected to increase significantly. It is estimated that by 2025, the annual production capacity will reach 462GWh, and exceed 1TWh by 2030.

To ensure battery independence, including the independent supply of critical raw materials such as lithium, nickel, and graphite, the EU has invested nearly 20 billion euros in a total of 70 projects.

Volkswagen (VW) expects that its battery demand in Europe will be 240GWh/year by 2030. To ensure the supply of batteries, the VW Group hopes to establish six battery factories in Europe in collaboration with partners.

Stellantis Group plans to increase its battery production capacity to 250GWh by 2030.

A fair view of IRA and global competition

The battery industry in the United States and Europe is flourishing. How should we fairly evaluate the IRA scheme and the global competition facing the Chinese battery industry?

First, it is understandable to develop our own industries and seek opportunities in the new era when we are at a disadvantage. The main issue is that we are not yet leading, with the United States, Europe, Japan, and South Korea ahead of us.

Second, China’s industrial chain has had a first-mover advantage. If we set our sights too high, we may be replaced because there is a risk of talent and technology overflow due to cost and technological advantages.

Finally, the most effective strategy is to participate in global competition. Establishing factories in Europe and the United States is a favorable participation strategy. Continuous and iterative improvements are the only hope for sustained leadership. From local manufacturing in China to global manufacturing bases, globalization of the industrial chain is an inevitable trend.

This article is a translation by ChatGPT of a Chinese report from 42HOW. If you have any questions about it, please email bd@42how.com.