Author | Lingfang Wang

Who still remembers that in June 2020, the price of lithium carbonate was less than 40,000 yuan.

And now?

On October 17th, Shanghai Steel Union released data showing that the spot price of battery-grade lithium carbonate has risen to 53.55 million yuan/ton.

According to Fastmarkets data, from the low point at the end of 2020 to the present, the price of lithium hydroxide has risen by about 850%, the price of lithium carbonate has risen by about 1090%, and the increase in lithium spodumene is as high as 1780%.

This increase is not yet at its peak. A senior consultant from an Australian lithium mine, “Mr. Sydney” (pseudonym), predicts that by the end of this year, the FOB price of 6% lithium spodumene is estimated to be between 8,000-9,000 US dollars/ton. Based on this estimate, the production cost of lithium carbonate is approximately between 550,000-580,000 yuan/ton. If you add 10% profit, the market price of lithium carbonate can be imagined.

Lithium carbonate is an essential raw material for lithium battery cathode materials and electrolytes. These price increases will eventually be transmitted to the entire vehicle industry and consumers, affecting the popularization of new energy vehicles.

When will the lithium price surge end?

“Mr. Sydney” predicts that based on global power battery capacity planning and the demand of the energy storage market, the gap may continue to expand in the next 2-3 years, the supply and demand contradiction will be most prominent in 2025-2026, and the price of lithium spodumene may reach 8,000-10,000 US dollars/ton. Converted to the price of lithium carbonate, it will be approximately 600,000-800,000 yuan/ton. Before 2030, the price of lithium spodumene may hover around 7,000 US dollars/ton.

In this solid upward period of lithium prices, it will definitely form a squeeze effect to many enterprises- the life and death of lithium salt processing enterprises, battery enterprises, and electric vehicle enterprises all depend on this.

Why the price surge?

The surge in lithium carbonate this time is caused by multiple factors, such as too rapid demand growth, long new mine opening and resumption cycle, and shortage of manpower and transportation capacity under the influence of the epidemic. In addition, the auction model of Australian lithium mine Pilbara Minerals has further accelerated the growth rate of lithium carbonate prices.

However, the significant growth in downstream demand is obviously the most important factor.

(1) The outbreak of downstream demand

Lithium carbonate is an important raw material for ion batteries, and the rapid growth of the lithium-ion battery market directly boosts the demand for lithium carbonate.

According to data from the China Automotive Power Battery Innovation Alliance, the cumulative output of China’s power battery production from January to September this year was 372.1 GWh, a cumulative year-on-year increase of 139.0%. The production in the first 9 months of this year has already exceeded 1.65 times the production of the entire previous year.The battery production in 2021 was 219.68GWh, 2.63 times higher than that in 2020, indicating that the downstream demand is the biggest driving force for the rise in lithium carbonate prices.

In 2021, the growth of new energy vehicles in China exceeded expectations, catching the upstream suppliers off guard. The large-scale capacity expansion of power battery companies is still continuing, which further drives up the growth expectations of lithium carbonate prices.

(2) Australia has had a long cycle of new capacity and recovery

In terms of lithium resources, the region with the largest global reserve is the South American Triangle (Bolivia, Argentina, Chile), accounting for as much as 56%, mainly in salt flats; followed by Australia with 8%, which is mainly composed of hard-rock lithium deposits (such as spodumene, lepidolite, and petalite).

The resource endowment of the three South American countries is the best, but because they are developing countries, resource development is often restricted by many conditions. For example, Bolivia, which has the best resource endowment, not only has a large reserve but also has high grade, but the local social security condition is poor and the risk of mine operation is high, so there are hardly any companies willing to go there.

Moreover, Bolivia has established a National Lithium Mining Company with the aim of jointly developing its domestic salt flat resources with overseas mining giants. However, due to local residents’ protests (because they did not receive any lithium mining concession fees or more revenue from lithium mining development), and the uncertainty of national policies, relevant cooperation has been cancelled, which makes Bolivia, with the largest global reserve of salt flat resources, far behind the other two lithium triangle countries in terms of production capacity and supporting facilities.

Argentina has a relaxed economic environment, and many mines are restricted in the use of water and electricity. The local social situation is also relatively complicated, and mining is therefore often restricted.

In Chile, the government is promoting the nationalization of mineral resources. In order to improve residents’ welfare and income, the Chilean government will also put forward mining taxes, which will increase the cost of lithium resource development in the country.

The biggest problem facing lithium mines in Africa is the huge difficulty in infrastructure construction.

Therefore, Australian lithium mining resources currently have the best development conditions. The lithium mines in this region are of high quality, the development environment is friendly, and the mining technology is relatively mature. Australian lithium mines have long been the main source of global lithium resources, accounting for about 55% of global production in 2021.

Unfortunately, the potential of lithium mines in Australia has not been fully tapped, which is related to the previous cycle of mineral adjustment.

Since 2018, Australian mineral production has experienced a cycle of ups and downs due to changes in downstream demand. From 2018 to 2020, Western Australia’s lithium mines were put into operation. Influenced by factors such as the decline in new energy vehicle subsidies and consumer electronics demand, lithium concentrate prices fell to a low level, and upstream profits were compressed to losses. At that time, many lithium mining companies faced bankruptcy and production suspension, and production capacity gradually cleared.

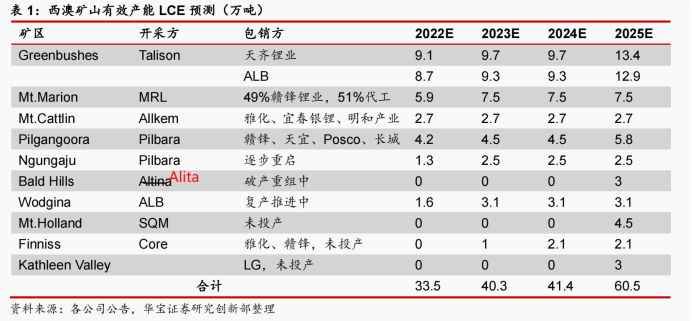

Among the major mines in Australia, Kathleen Vally, Mt.Holland, and Bald Hill did not produce this year. The theoretical production capacity of lithium spodumene in Pilbara is 750,000 tons with 6% grade. According to last year’s plan, Pilbara should supply 680,000 tons with 6% grade to the off-taker in 2022. However, the actual production after the guidance reduction only reached 400,000 tons this year.

In March of this year, according to the conversion of a research report by Huabao Securities, the equivalent amount of lithium carbonate converted from lithium concentrate is shown in the figure below.

In addition, Core Lithium provided a guidance of 79,000 tons of lithium concentrate production in the Finniss project in 2023 at the Australian exploration and trading conference, which was reduced from 183,000 tons before; Allkem also lowered its production guidance for the 2023 fiscal year, expecting the Mt.Cattlin lithium concentrate production to be 140,000-150,000 tons, which is lower than the 160,000-170,000 tons guidance provided in July this year, with a decrease of 20,000 tons.

In addition, the development of new mines also faces the problem of a longer cycle.

“Mr. Sydney” told the “Electric Vehicle Observer” that if everything goes smoothly, it usually takes 6-7 years to explore and develop new mines in Australia, and there are many challenges to be solved in between, such as pollution emissions, power and water supply, and even road construction.

On the one hand, with the increasing demand, and on the other hand, the growth of Australian supply is lower than expected, which may cause the gap to continue widening.

(3) Impact of the epidemic on manpower and transportation

The above difficulties have been further amplified under the epidemic. Except for China, overseas countries have basically given up control of the epidemic, and there are employees taking continuous leaves at every stage, disrupting the supply rhythm of the entire market.An expert familiar with Australia’s mining industry said that although the Australian government has given up control over the epidemic and companies can operate normally, infected employees have the right to demand economic compensation from the company if they infect other employees, and there is no upper limit on the economic compensation awarded by the court. This has resulted in business owners actively requiring infected employees to take sick leave.

Employees who take sick leave due to infection with COVID-19 will also receive generous government subsidies, which has made infected employees willing to take leave, ultimately leading to shortages of mature labor and skilled personnel, as well as insufficient transport capacity.

(4) Pilbara introduces an auction model for iron ore, further accelerating the increase of long-term prices

As most domestic lithium resources in China are located in high-altitude areas with difficult extraction and low grades, as well as facing pressure from environmental and national issues, progress has been slow.

Therefore, in the seller’s market, overseas suppliers have pricing power.

This pricing power is mainly reflected in Pilbara’s spodumene spot auction. Pilbara has introduced an iron ore auction model into the lithium industry, and this auction price has gradually become a new benchmark and pricing system for spodumene spot prices.

The production capacity of Pilgan, located in Pilbara’s main area, has been locked by downstream lithium salt factory customers (producing 360,000-380,000 tons of concentrate per year). Therefore, the auctioned source mainly comes from the resumption of production at Ngungayu (formerly Altura capacity, producing 180,000-200,000 tons of concentrate per year). After its resumption of production, all the output is auctioned and no longer covered by sales contracts.

The effect is that Pilbara has changed the “rules of the game” through auctions. In the seller’s market, a small number of auctions have effectively pushed up long-term contract prices.

In addition to price, the quality of lithium concentrate has also declined. In the view of “Mr. Sydney,” in the seller’s market, lithium concentrate has long not been able to meet the 6% grade requirement. According to the standard before 2016-2018, spodumene sold in the market today is unqualified. Various low-quality products can also be circulated.

“Mr. Sydney” told the “Electric Vehicle Observer” that in the early years, buyers had high standards for lithium concentrate, at least meeting the following three standards. First, the lithium content in spodumene was above 6%. At that time, it was priced at USD 450 per ton, and for every 0.1% decrease, a deduction of USD 15 per ton was made. Buyers refused to receive goods with a lithium content below 5.6%. “Spodumene with a 6% lithium content requires about 8 tons to produce 1 ton of lithium carbonate, and spodumene with a 5.6% lithium content requires about 9 tons to produce 1 ton of lithium carbonate.”Two, the coarser the particles, the better. Currently, most lithium ore suppliers in Australia cannot reach a 6% content. The raw ore of Pilbara, the largest lithium ore supplier, is brittle, and it is already difficult to process raw ore with a 1.14% content to a 5.6% content through processing. If the “oscillating beneficiation technology” is required to raise the content of raw ore from 1.14% to 6%, it will become as fine as flour, and the lithium carbonate plant will not be able to process it, even if it is sold to customers at the normal standard price with a 5.6% content.

Three, the requirement is that the iron element content does not exceed 1.0%. High iron content will cause furnace slag and affect the yield of lithium carbonate. Currently, lithium ore suppliers cannot meet this standard.

This is the downside of the seller’s market, recycling inferior goods as good ones and skyrocketing prices. “Mr. Sydney” deeply regrets this issue.

How long will the price increase last?

How long the price increase will last is another issue that the industry is very concerned about.

After communicating with “Electric Vehicle Observer” and several industry insiders, they unanimously believe that the lithium price will continue to rise for some time.

Luo Xiaoli, manager of the lithium battery department of Longzhong Information, believes that the lithium price is still on the rise from what is currently seen, but she does not make any judgments on how long the increase will last.

The person in charge of the positive material company stated that this mainly depends on downstream demand. Currently, the trend is still increasing.

“Mr. Sydney” predicts that by the end of the year, the FOB price for 6% content spodumene will rise to $8,000-$9,000 per ton. Based on this estimate, the production cost of lithium carbonate will be approximately 550,000-580,000 yuan per ton.

“Mr. Sydney” analyzed that currently, lithium resources face two aspects of demand: one is the high-speed growth of global power battery production capacity. According to market forecasts, China’s power battery production capacity will reach 3,000 GWh by 2030, and the European, Japanese, and Korean regions may have 500 GWh. Although not all will reach full production, the momentum of doubling every year has not decreased for the time being; the other is the huge growth potential of global energy storage, especially the Russia-Ukraine war, which has accelerated the demand of the European market for energy storage batteries, with a potential growth rate of even more than tenfold.

Therefore, “Mr. Sydney” believes that the contradiction between supply and demand of lithium resources will reach its peak in 2025-2026, and the FOB price for 6% content spodumene may reach $8,000-$10,000 per ton. After that, it will maintain a price of $7,000-$8,000 per ton until 2030.

At the 2021 Energy Storage Conference, Zhongwei Chen, a member of the Canadian Academy of Engineering and the Royal Society of Canada, stated that the entire energy storage battery will be more than 100 times larger than the amount of batteries used in electric vehicles in the future.Perhaps Chen Zhongwei may have exaggerated with suspicion, but at the very least it demonstrates that the market size for energy storage batteries far exceeds that of power batteries, and its demand for lithium resources should not be underestimated.

According to a study released on May 9, 2022 by Wood Mackenzie, global demand for energy storage is expected to continue to grow rapidly over the next decade. Despite the risks posed by the COVID-19 pandemic and the unfavorable factors brought about by rising commodity costs, it is expected that global demand will double by 2022. The strong growth momentum will continue over the next decade, with the market expected to grow up to nine times the current demand.

From the current supply situation, the supply growth of lithium resources has not increased significantly.

According to a research report by Haitong International, many projects planned for production in 2023 have encountered uncertainties in both larger and smaller projects. For example, Allkem has lowered its 2023 fiscal year concentrate production guidance by nearly 20,000 tons due to uncertainties such as the relocation of the main mining area and the low-grade of ore, and has adjusted the Olaroz salt lake expansion time to the end of the previous guidance, which was previously said to be in the second half of 2022 and is now in December 2022.

The construction of the Core Australian Mine project has also been delayed due to unfavorable factors such as the ongoing absenteeism caused by the COVID-19 pandemic, supply chain disruptions, and inflationary pressures.

In addition, Sigma’s Brazilian project has also progressed lower than expected. First, there is equity. Second, there are pre-approvals such as mining permits and environmental assessments. Third, there is the impact of the pandemic on personnel mobility and skilled workers. Fourth, there are policy changes in different countries. Fifth, related enterprises may have had overly optimistic expectations.

Currently, as the project progresses, the difficulties that were not adequately forecasted in the early stages will gradually become apparent.

According to industry insiders, lithium resource supply has only increased by about 20% this year. When comparing this data with the growth rate of power battery production data and the doubling of energy storage demand, the difference is huge.

Where is the profit?

With the rising trend of lithium prices, integrated mining and metallurgical companies have earned the largest share of profit, while downstream battery and vehicle companies have experienced the most difficulties in the industry chain.

Although it was foreseen that mining companies would make money, the specific gross profit margin is still shocking.

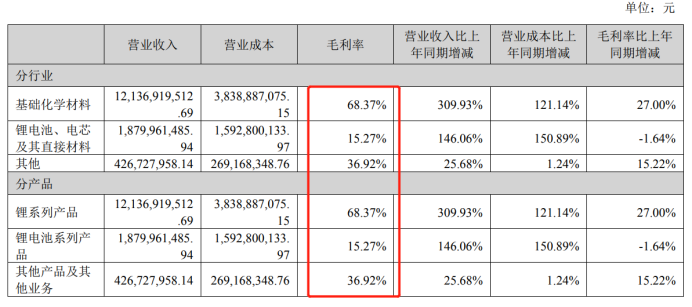

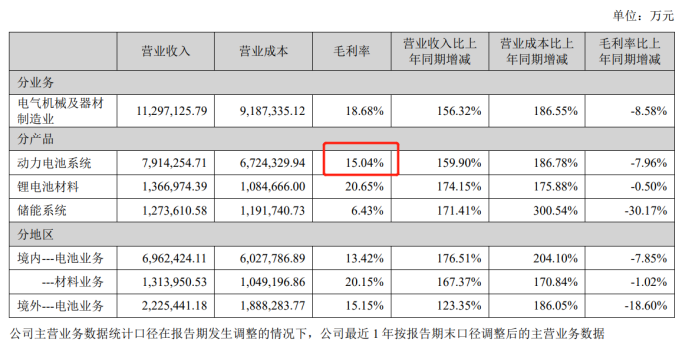

The typical companies with “mines in their own homes” include Ganfeng Lithium and Tianqi Lithium. In the half-year report of Ganfeng Lithium in 2022, the gross profit margin of lithium series products reached as high as 68.37%.

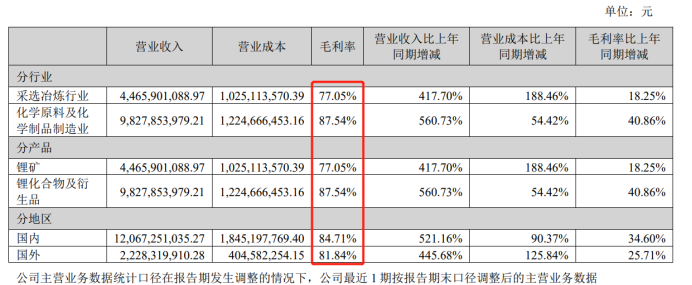

Tianqi Lithium is also a typical production enterprise with both lithium mines and lithium salts. In the first half of the year, the gross profit margin of Tianqi Lithium’s lithium mining products reached 77%, and the gross profit margin of its lithium salt products reached 87.5%.

In addition, the gross margin of Cobalt Metals Co., Ltd. in the first half of 2022 was 83.8% for mining and selecting, and 19.3% for lithium salt.

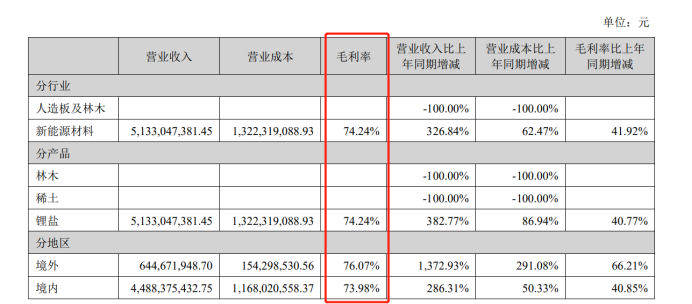

According to the half-yearly report of Shengxin Lithium Energy Group Co., Ltd. in 2022, its gross margin for lithium salt reached 74%.

Tianqi Lithium Industries, one of the important domestic lithium salt producers, also has some upstream mining resources. According to the half-yearly report of Tianhua Ultra-clean Holdings in 2022, the gross margin of its Lithium Salt products also reached 78.8%.

In contrast, the gross margin of the lithium battery leader – Contemporary Amperex Technology Co., Ltd. (CATL) is relatively bleak, with a gross margin of only 15% for power battery systems, a year-on-year decrease of nearly 8%. Perhaps this is data obtained from a return of profits accumulated over the years.

As for BYD, the leader of new energy vehicles, the gross profit margin of its vehicle-related business in the first half of the year was only 16%. It should be noted that the business of automobiles, related products and other products includes a series of products such as automobile manufacturing and sales, automotive power batteries, photovoltaics, rail transportation and epidemic prevention materials.

Based on data released by Yicai, the gross profit margin of BYD’s vehicle sales was only 13.51%.

It can be seen that with the rise of lithium prices, enterprises that have mines and those that produce lithium salts are making a fortune.

The dilemma facing the car industry is not only the rising cost of batteries, but also other raw materials such as chips, which are also increasing significantly. Car companies will inevitably squeeze profit margins.

With the continuous rise in lithium ore prices, the long-term agreements between lithium salt companies, lithium resource companies, and lithium producers have gradually evolved into a mode where the amount is locked, but not the price. The cost prices of lithium salt production companies without mines have also risen, while high costs occupy middle-stream lithium salt and positive electrode material companies, resulting in pressure from both ends.

According to Baichuan Yingfu data, as of September 1st, the long-term contract price for lithium carbonate had reached 493,600 yuan/ton, an increase of 3.8% compared to the lowest price in May. Currently, the mainstream long-term contract price is between 490,000 yuan/ton to 500,000 yuan/ton.

It is foreseeable that the continuing rise in lithium carbonate prices will lead to a round of reshuffling among lithium salt processing companies, and companies with integrated mining and metallurgy have a significant survival advantage.

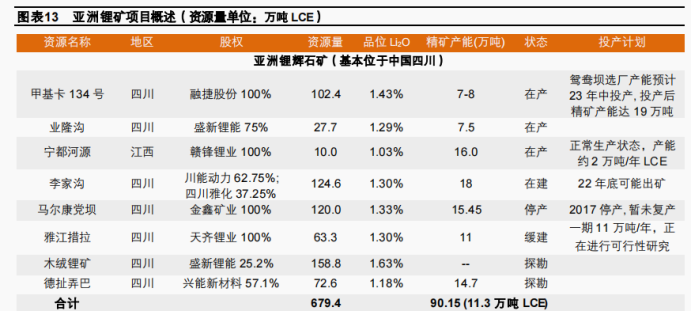

How is China’s Local Lithium Resource Progressing?

China is also rich in lithium resources, ranking sixth in the world in terms of total reserves. Unfortunately, overall yield and impurity content are not outstanding, and progress in mining development is slow due to various factors.

Taking Sichuan’s lithium mine as an example, mine development requires four stages: survey, project approval, design, and construction, with a total time frame of at least 3-5 years. The mining approval process may be constrained by various factors such as environmental protection and national politics.

For example, Rongjie’s methic kaolinite mine has been mined for more than ten years but has yet to reach production. In the first half of the year, the production volume of lithium concentrate was 23,700 tons, with sales of 23,000 tons, equivalent to 6% with a yield of 18,900 tons for 1.89 gigs. The Yangyangba 2.5 million tons of lithium ore selection project has not yet been approved for environmental assessment, and it is impossible to predict when it will begin construction.

Another example is Lijia Gou Mine, in which Chuanneng Power Control and Yahua Group participates. It was approved in 2018, and the original plan was to be completed in three years. It has been postponed to the end of this year and has recently been postponed again to early next year before it can be put into production.

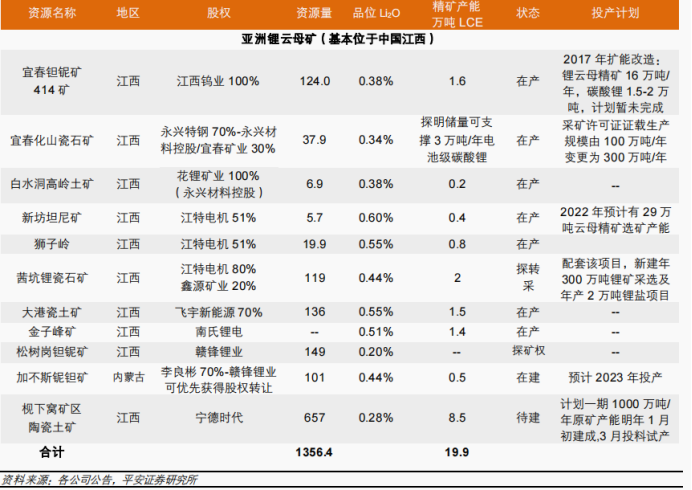

Of course, apart from Chuan’s mines and salt lakes, Jiangxi Yichun also has lithium-bearing mica mines. However, the lithium-bearing mica mine in Jiangxi has a low grade, high impurity content, and high tailings processing costs. However, compared with other resources in the plateau, it is relatively easy to develop, and it is also an important area for companies to lay out.

According to the data provided by Luo Xiaoli, China’s self-sufficiency rate in lithium resources is approximately 23% in 2021, and the self-sufficiency rate will gradually increase in the future.

This means that no matter what, the majority of the lithium still comes from overseas.

What preparations have Chinese companies made?

With insufficient lithium resources, the only option is to compete for them.

A person in the lithium mining industry revealed to “EV Observer” that “currently, two leading domestic battery companies have quietly sent out multiple groups of people to Africa to search for lithium mines. The responsible persons for the exploration have had their salaries increased several-fold and have been ordered to not return if they fail to find the mines.”

The price of lithium concentrate is hard to fall significantly in the short term, and the price of electric vehicles cannot increase indefinitely, or even decreasing is the main trend.

With the dual pressure from both ends, whether they have their own mines or not has already determined the life and death of power battery companies and automakers.

Data shows that since the beginning of 2021, BMW, Volkswagen Group, General Motors, Ford, Tesla, Renault, Toyota, and other automakers have invested in 21 upstream raw materials, among which 16 are related to the lithium industry.

Chinese electric vehicle companies have also established their own strategies, with BYD being the earliest one as it invested and cooperated with Tibet Mining in 2010, and acquired 18% of the shares of its subsidiary Zhabuye Lithium, and later invested in Shengxin Lithium and Rongjie Shares to lock in lithium resources.

Great Wall Motors entered into a partnership with Pilbara in Australia in early 2017 and gained partial reimbursement rights, and signed a framework agreement with Ganfeng Lithium for resource security.

SAIC and GAC are relatively latecomers to the lithium resource sector and have invested in second-tier lithium companies, such as Jiuling Lithium in Jiangxi.

Below is a summary of some Chinese automakers’ resource layout:

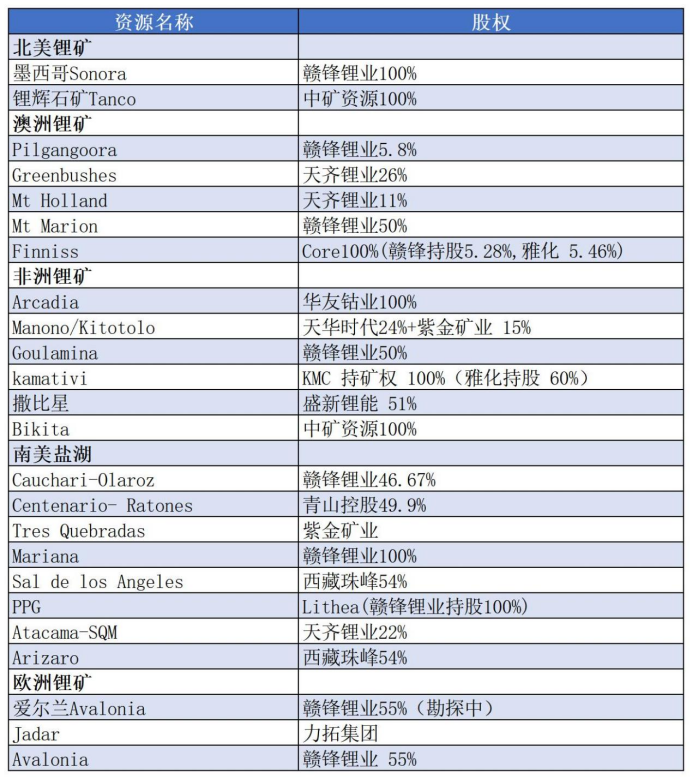

In addition, Chinese lithium companies are also increasing their investment in mines and salt lakes, with Tianqi Lithium and Ganfeng Lithium holding lithium resources globally.

Below is a summary of the lithium resources held by some Chinese lithium companies in different continents:

In the eyes of senior lithium mining experts, Chinese companies were very late to invest or acquire stakes when many lithium mine owners in Australia and the South American Lithium Triangle faced survival difficulties in 2018-2019. The huge price difference clearly caused significant losses.

In the eyes of senior lithium mining experts, Chinese companies were very late to invest or acquire stakes when many lithium mine owners in Australia and the South American Lithium Triangle faced survival difficulties in 2018-2019. The huge price difference clearly caused significant losses.

“Throughout, the author believed that it should be cost-performance, quality, and product power that decide the survival of lithium battery companies or car companies, rather than upstream lithium resources.”

Perhaps the crazy increase in lithium prices this time can sound an alarm for Chinese companies. In the development of emerging industries, appropriate foresight will bring higher benefits to companies, industries, and even the whole society, and pave the way for the smooth development of later industries.

For Chinese new energy automobile industry chain companies, they can only strive for more lithium supply resources and better prices, while actively deploying in China’s relatively leading power battery recycling, so that the inflection point of lithium price acceleration can come sooner.

This article is a translation by ChatGPT of a Chinese report from 42HOW. If you have any questions about it, please email bd@42how.com.