Author: Zhu Yulong

Recently, topics have been abundant. In terms of the overall data for new energy vehicles in September, the effect of the end of the quarter was great. As we begin October, the fourth quarter as a whole is worth observing. The overall insured data in September was 1.8624 million, increasing by 8.5% year-on-year, but decreasing by 1.25% on a month-on-month basis. Due to support from automotive policies and exportation, we haven’t yet seen domestic market sales affected by macroeconomic factors. This is a fairly long-term variable.

The Chinese automobile market itself is at a demand bottom, and just like buying a house, it is necessary to track the driving force for purchasing cars continuously. The new car purchasing population is divided into first-time buyers and replacement buyers. In China, replacement buyers have been focused on for a long time.

Industry fragmentation

From the terminal data in September, BYD sold 166,882 units, far ahead of Changan’s 98,266 units, Geely’s 94,889 units, FAW-Volkswagen’s 159,340 units, and SAIC-Volkswagen’s 117,898 units within independent brands, with clear differences in growth rates between different companies.

In new energy vehicles, I’ve separated pure electric and plug-in hybrid vehicles. In the pure electric field, BYD’s sales of 78,502 units are nearly equal to Tesla’s 76,882 units. However, BYD’s plug-in hybrid vehicles, with sales of 88,220 units, currently have an advantage.

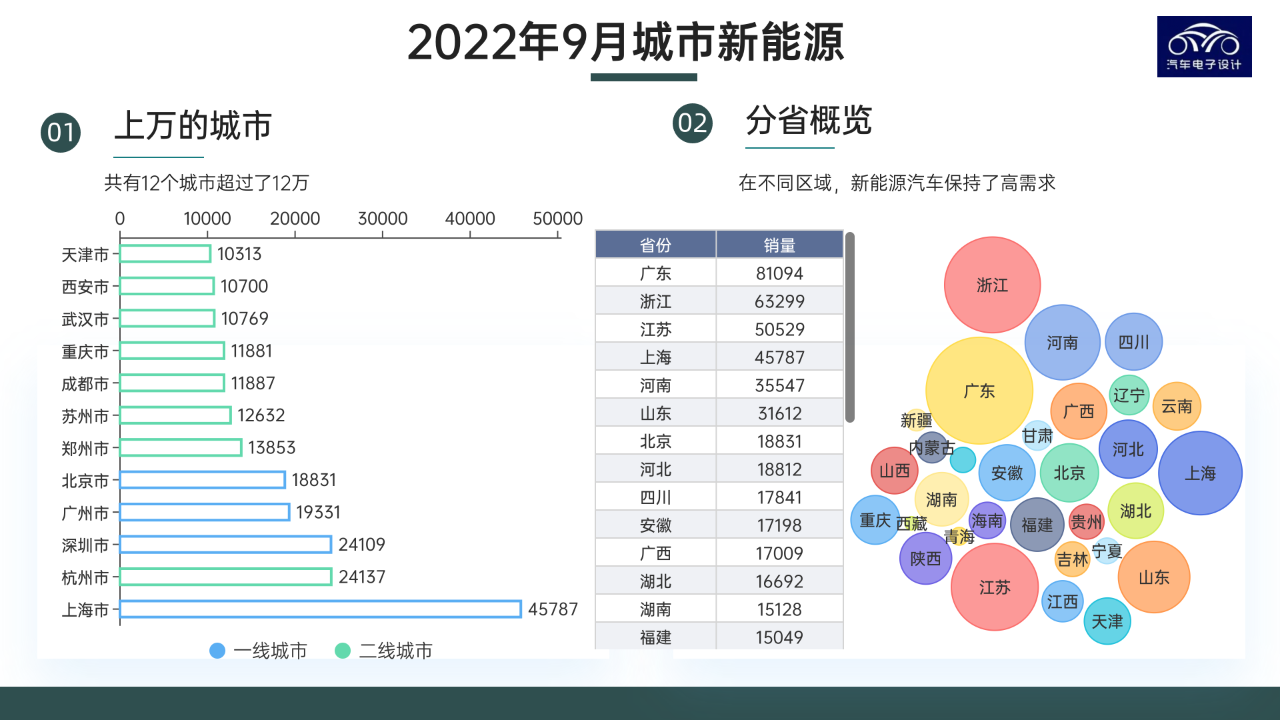

Overall growth rates of emerging forces have already been substantially disclosed at the beginning of the month, so I won’t describe them again here. We look forward to seeing the October data. In terms of cities, Shanghai once again leads in sales of new energy vehicles.

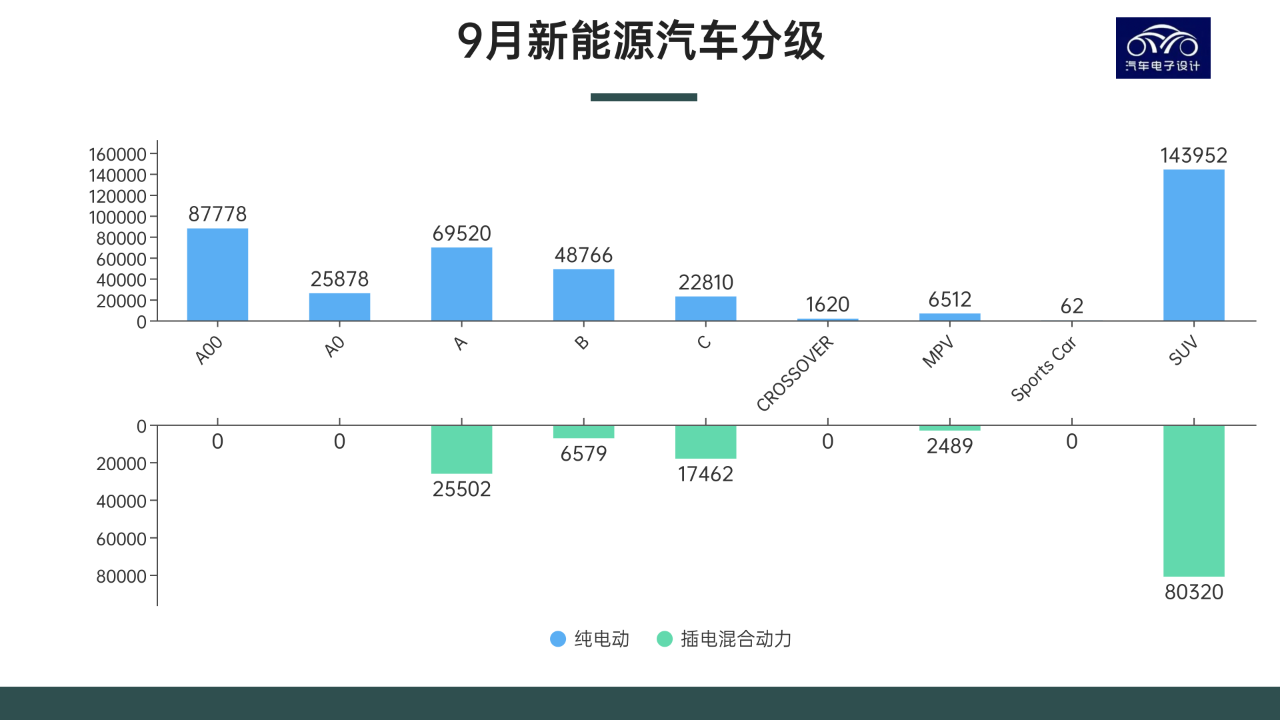

Currently, the A00 new energy vehicles have stopped rising, and the A0 level is mainly dominated by only one player, the Dolphin. The current market growth is mainly driven by pure electric SUVs and plug-in hybrid SUVs.

From 2022 to 2023, the market for A00 pure electric cars may further shrink. As far as SUVs are concerned, I understand that this wave of demand is still coming from conventional fuel cars, and buyers still consider the need for space.

Situation of Key Auto Companies

BYD

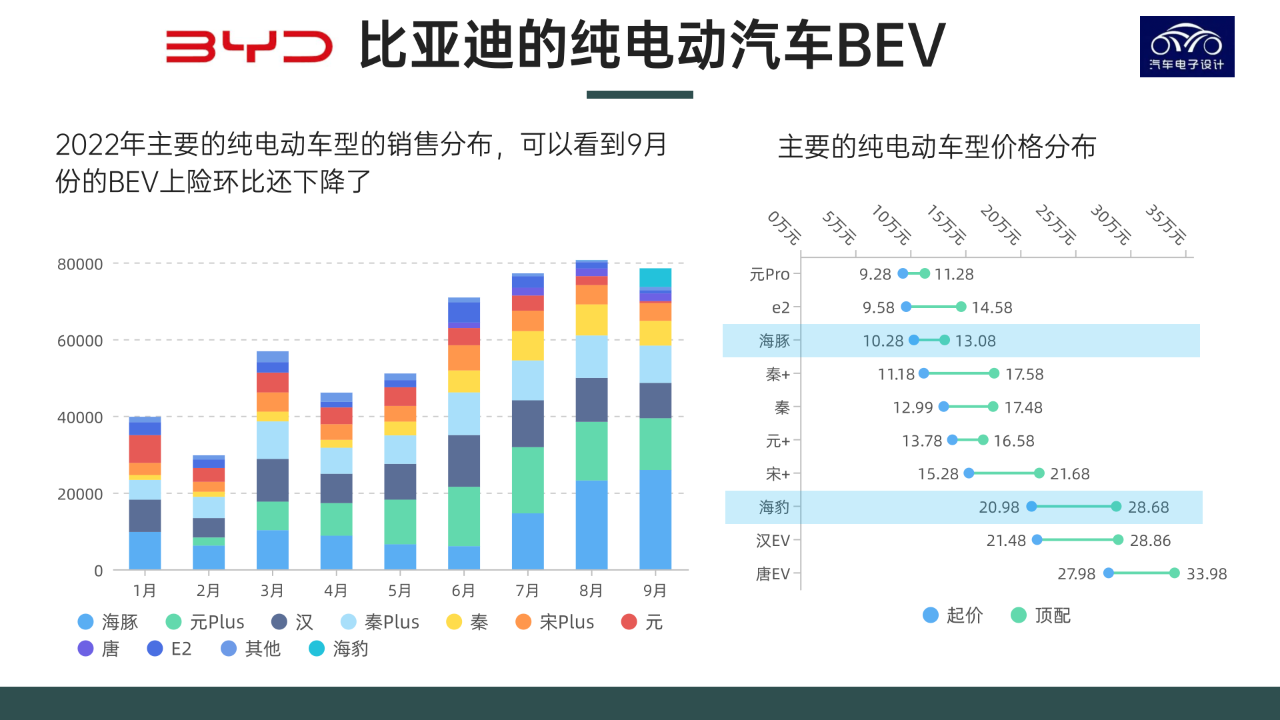

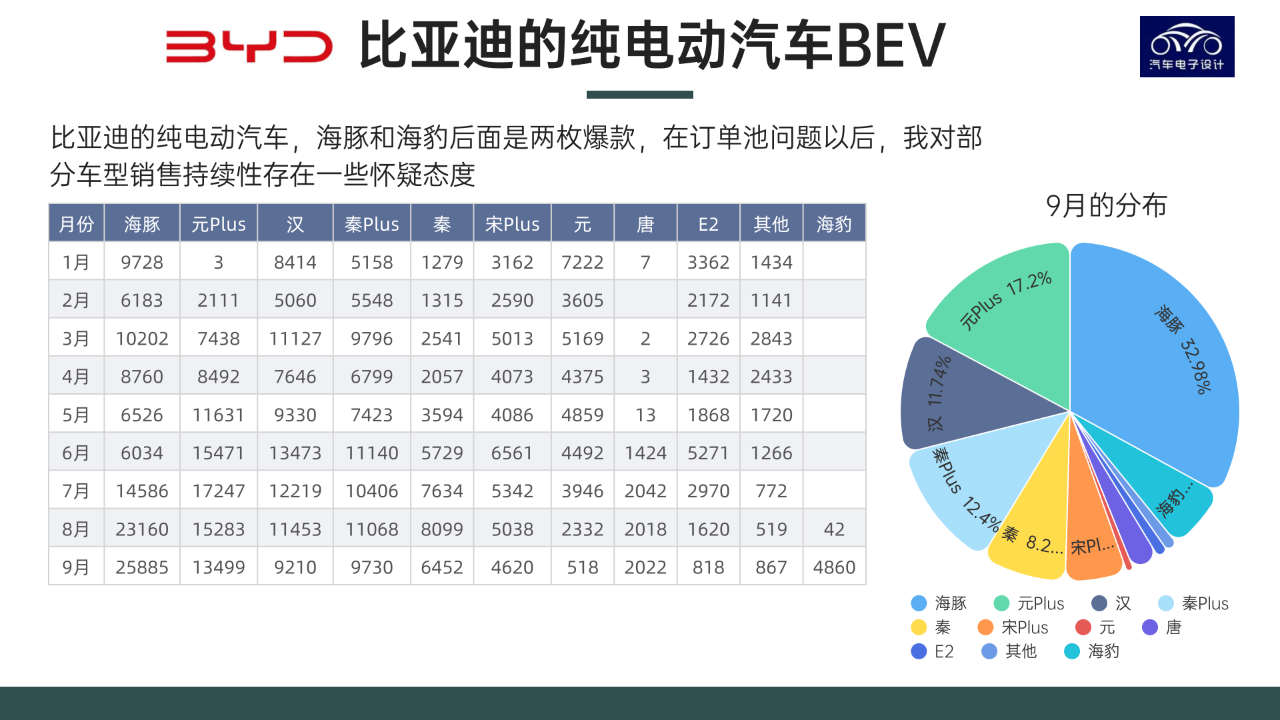

I did a segmentation of BYD’s data, and found that within the same model, the DM-i hybrid sells better than the pure electric version. There are many assumptions here. If a plug-in version of Yuan Plus is released, will the market for Yuan Plus and small SUVs also be taken over by DM-i? The fundamental question is whether the pure electric E3.0 architecture is feasible in the same level of car models? In fact, BYD’s Sea Lion is quite capable of determining whether the E3.0 architecture meets the demand.

Due to BYD’s overall good data, it can cover up many discussions and problems.

The sales of pure electric cars decreased by 78481 units compared to the previous month of 80590 units. In terms of distribution, the Dolphin sold 25885 units (100-150K RMB), Yuan Plus sold 13499 units (100-150K RMB), Han sold 9210 units (200-300K RMB), Qin Plus sold 9730 units (100-150K RMB), Qin sold 6452 units (100-150K RMB), and Song Plus sold 4620 units (150-200K RMB). The most significant point is that the sales momentum of the Sea Lion reached 4860 units.In the plug-in hybrid sector, the focus is mainly on the Song Plus with 29,433 units, Qin Plus with 17,719 units, Tang DM-i with 11,531 units, and Han DM-i with 14,017 units.

Tesla

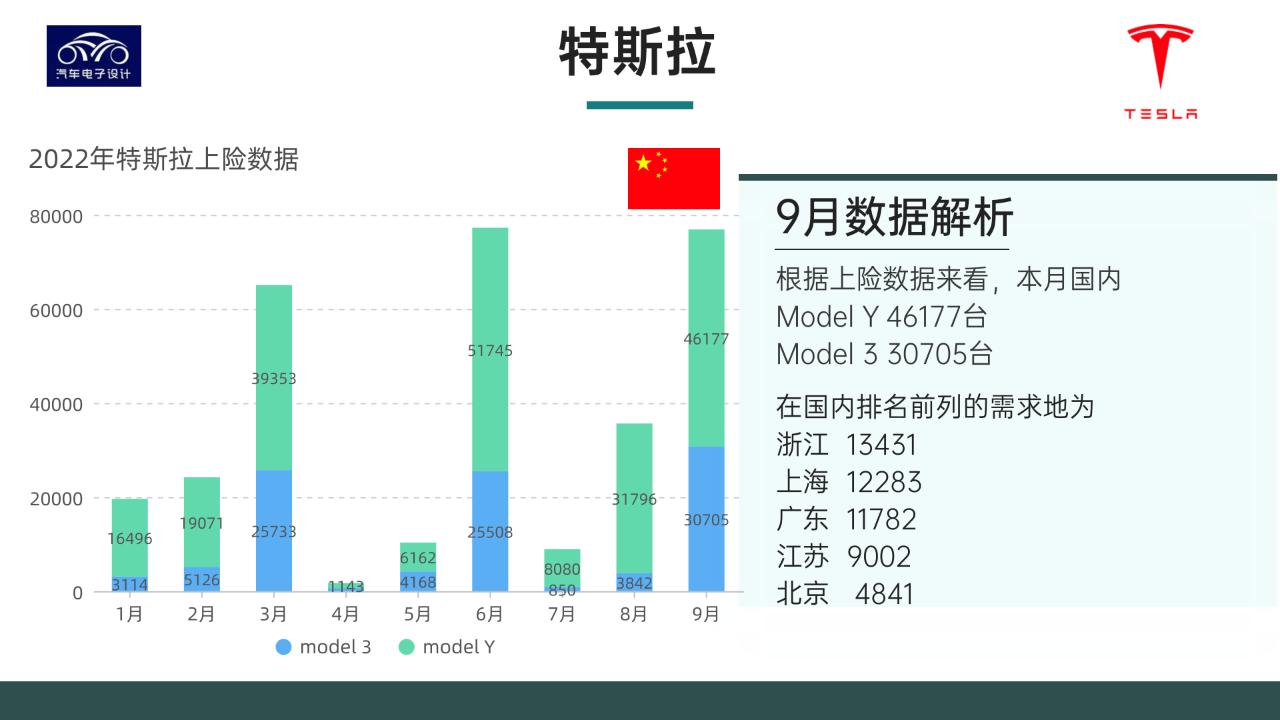

According to insurance data, Tesla delivered 46,177 Model Y units and 30,705 Model 3 units domestically this month. The main delivery areas are Zhejiang, Shanghai, Guangdong, Jiangsu, and Beijing.

Geely

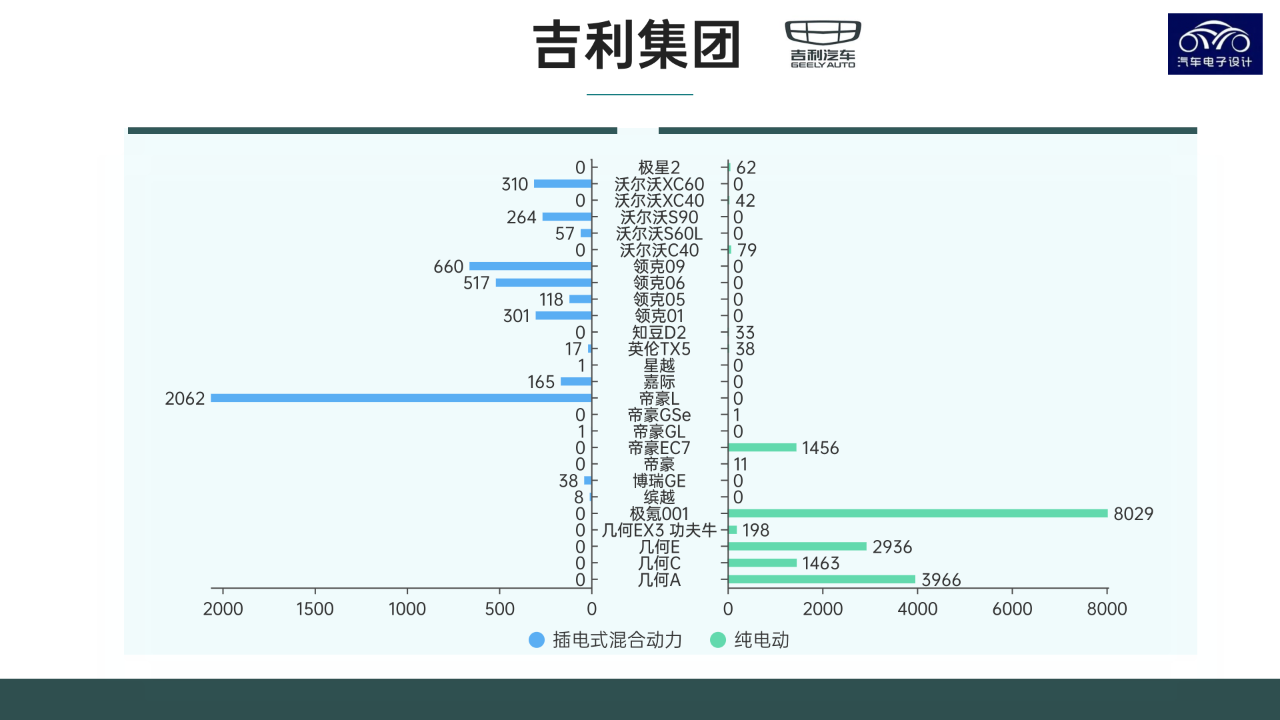

Geely’s data is split into plug-in hybrid and pure electric. Geely’s hybrids are also gradually transitioning. Geely’s new energy vehicle strategy has undergone major changes in 2022, with improvements made in both pure electric and plug-in hybrid areas.

At present, Geometry has gradually stabilized at over 8,000 units, and Zeekr (Jeep) has stabilized at around 8,000 units.

Changan and Great Wall

Compared with last month, Changan’s SL03 began delivery, with 1,629 pure electric and 1,321 extended-range units, totaling about 3,000 units. Of course, insurance data still revolves around the small-car strategy. As for Great Wall Motors, it will take a little time for Euler’s transformation, and the Hover is still the main force.

Volkswagen

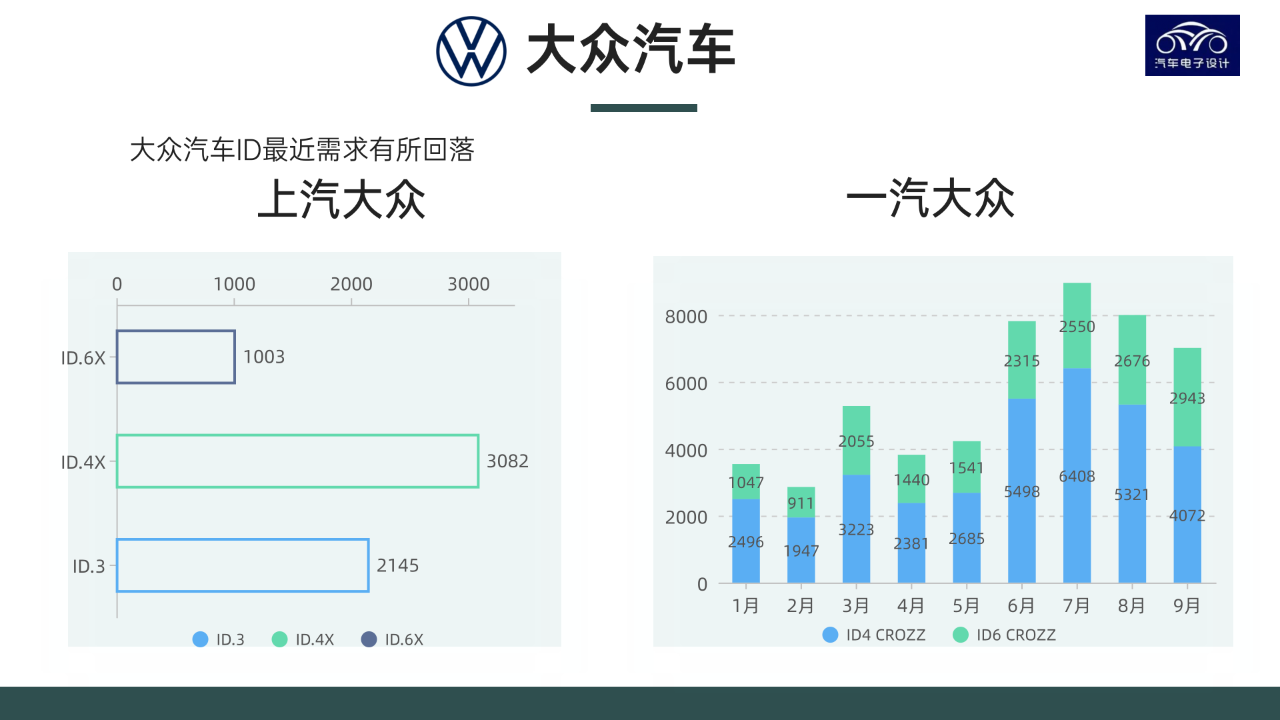

Finally, let’s talk about Volkswagen. We have indeed seen the recent urban driving effect, with massive support in major first-tier cities, which resulted in an increase in Volkswagen’s ID series. Both North and South Volkswagen had terminal sales of 8,000, which, while falling short of expectations, is still in line with overall sales expectations.

Conclusion: Due to the National Day holiday in October, it is uncertain whether this data is inflated. As usual for China, the data is usually reflected in the insurance data from November to December, followed by a significant decline in Q4 and Q1. Given the large base, this trend is unlikely to be as pronounced as in previous years.

This article is a translation by ChatGPT of a Chinese report from 42HOW. If you have any questions about it, please email bd@42how.com.