Jia Haonan Posted from the Copilot Temple

Reference to Intelligent Cars | WeChat Official Account AI4Auto

Leapmotor Auto landed and became the fourth new force to go public following NIO.

Just passed the HKEx hearing. The IPO globally issued 130.8 million shares, with a planned fundraising of HKD 1 billion.

Based on the planned maximum sale price of HKD 62 per share (approximately RMB 55), the market value of Leapmotor Auto is about HKD 62.85 billion.

There is still a gap from the dream of the founder’s “trillion-dollar market value.”

However, with Leapmotor’s IPO, a group of wealthy and free individuals have emerged.

“Elderly Happiness” Supports the Fourth New Force to Go Public

Leapmotor is listed on the Hong Kong stock market, with the sale price per share ranging from HKD 48 to 62.

In comparison, when NIO was listed on the Hong Kong stock market, the sale prices per share were 160 HKD, 165 HKD, and 118 HKD, respectively.

Correspondingly, the market value of NIO was more than twice that of Leapmotor’s 60-plus-billion market value.

This is related to Leapmotor’s positioning and current operating status.

According to the latest IPO disclosure, Leapmotor’s car delivery volume has shown a rapid growth trend in recent years:

However, among all cars delivered by Leapmotor, the microcar T03, whose price is in the range of 70,000 to 90,000 yuan, accounts for the vast majority, and T03 is also a car that users ridicule as the “elderly happiness” model.

The newly launched C11 model, which mainly targets the mainstream market with prices around 200,000 yuan, is still in the initial stage of climbing, with a monthly delivery volume of 5,000 to 6,000 units, accounting for about 50%.

From a historical and overall perspective, the sales volume of C11 is still very low.

Therefore, T03 is still the best-selling model of Leapmotor at the time of going public, and the biggest contributor to Leapmotor’s 68 billion market value.

However, this also caused the current situation of low single-car profit in Leapmotor’s performance table:

Low single-car profit and fierce competition in the microcar market make the development of this category lack momentum.

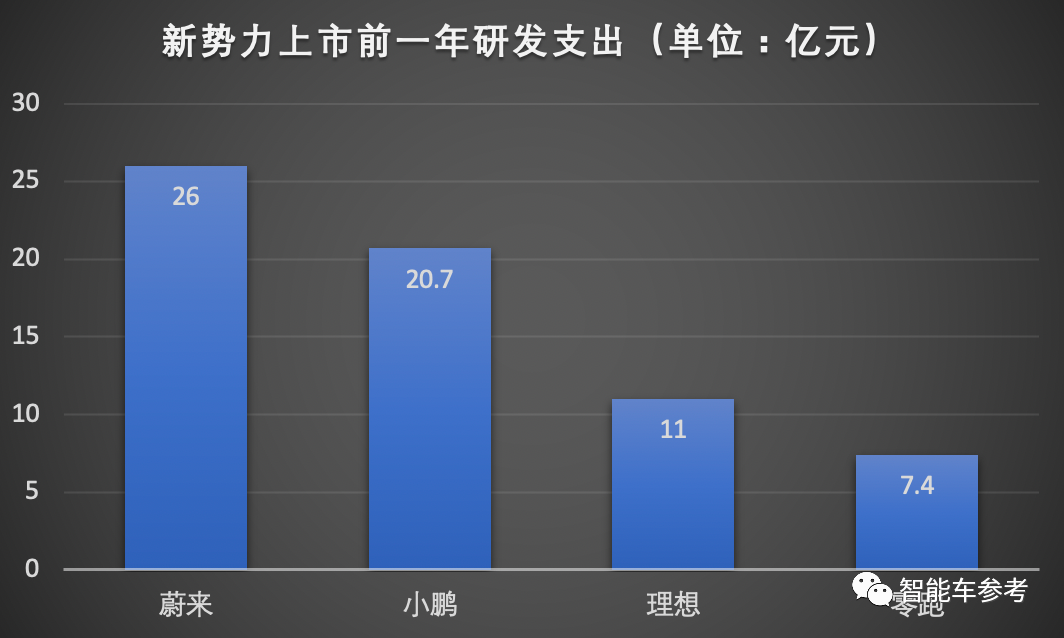

The total revenue is not enough, and financing is not as smooth as NIO’s. Leapmotor has been lagging behind in research and development investment.# Zero Run 2019-2021

R&D expenditures totaled ¥1.387 billion from 2019 to 2021, with ¥740 million spent in 2021, accounting for 23.62% of the revenue for the accounting period.

The low profitability due to selling small cars with low R&D investment is why Zero Run’s market value and stock price is much lower than other new forces in the industry, despite the sharp increase in sales.

However, the prospectus shows that Zero Run has achieved remarkable breakthroughs in its brand.

In the latest disclosed data for the first quarter of 2022, Zero Run’s gross profit margin rebounded to -26.6% due to the expansion of C11 deliveries.

Looking at the trend of the C11 deliveries accounting for more than half of deliveries in July and August, this mid-size SUV with a price range of ¥180,000-¥230,000 will soon replace the T03 as the main delivery model.

C11 has become the mainstay of Zero Run’s business and is growing rapidly, while C01, a sedan of the same level, has started delivery. This trend makes the potential of Zero Run’s performance this year very significant.

In addition to almost certainly surpassing300,000 total deliveries this year, the most important thing is that Zero Run is likely to turn its gross profit margin positive, and get rid of the situation of “selling one at a loss”.

At a market value of ¥68 billion, would you like to board the Zero Run’s train?

Who will gain financial freedom from Zero Run’s listing?

When Zero Run submitted its prospectus, we detailed the exploration of Zero Run’s equity structure.

The top ten shareholders are:

Among them, the two key core figures of Zero Run, Fu Liqun and Zhu Jiangming, and their families, directly and indirectly hold 31.01% of the shares, making them the largest shareholder group and holding the most voting rights for Zero Run.

Zero Run’s founder and CEO Zhu Jiangming is the largest individual shareholder, holding 11.89% of the shares (including indirect holdings of affiliated companies). Including his family’s shareholding, he holds a total of 16.33%.

Using the same formula, Fu Liqun and his family hold 14.68% of the shares.

In addition, Zero Run’s other two executives holding public positions and shares, including Wu Baojun, in charge of market sales, and Cao Li, in charge of technical research and development, hold 0.17% and 1.12% of Zero Run’s shares, respectively.With this information, we can roughly calculate how much wealth was created by the listing of LI.

Based on the market value at the highest offering price per share, and combining family holdings and indirect holdings, the following were calculated:

Founder Zhu Jiangming’s net worth surged by RMB 11.145 billion due to the listing of LI. Prior to LI’s listing, Zhu’s net worth was already RMB 5 billion, thanks to his shares in security giant Dahua.

Co-founder Fu Liquan’s net worth rose by RMB 10.02 billion. Fu, who was also a co-founder of Dahua, already had a net worth of RMB 27.1 billion.

Executive Cao Li’s net worth unlocked RMB 819 million.

Another executive, Wu Baojun, obtained RMB 116 million.

According to the prospectus, there were 9 other independent individual shareholders, with the highest shareholding being 0.9% and the lowest being 0.21%. Correspondingly, the theoretical returns on the Hong Kong stock market at the highest and lowest shares are RMB 616 million and RMB 144 million, respectively.

That means that with LI’s Hong Kong IPO, 13 new billionaires were created directly, with even the minimum theoretical profit being around RMB 100 million.

Of course, strictly speaking, the two core figures, Zhu Jiangming and Fu Liquan, weren’t truly “made rich” by this IPO.

Their shared background is linked to the founding of Dahua Technologies, which made them financially independent well before LI.

This historical context also leads us into the past and present of LI Automotive.

“Investors’ last ticket,” what kind of new force is LI?

LI Automotive was founded in 2015, stemming from Dahua Technologies, a global AI security company second only to Hikvision.

Both key figures are original founders of Dahua.

Fu Liquan, founder of Dahua and alumnus of Zhejiang Electronic Industry School, started from scratch and built Dahua into the second-largest AI security company in the world. He had a dream of reaching a market cap of RMB 100 billion, but the global security market is only worth a few hundred billion, so he turned his attention to the automotive industry.

Zhu Jiangming, co-founder of Dahua, began his journey with Fu Liquan with only RMB 5,000, and the two fought through hardships together as close comrades.

Zhu Jiangming, a graduate in electronic engineering from Hangzhou University (now part of Zhejiang University), has a technology background and was the CTO of Dahua, where he led the development of key products during Dahua’s growth, breakthrough and high-speed development stages, including automotive security products.

After the founding of Leapmotor, Zhu gradually resigned from his duties related to Dahua and took full responsibility for Leapmotor’s management and operation. He is also the chairman and founder of Leapmotor.

Fu Liquan, on the other hand, has stepped back and is now an executive director.

Zhu and Fu, along with their families, are the largest shareholder group of Leapmotor. They have reached an agreement to act in solidarity and, in case of disputes, Zhu Jiangming has the final say.

Therefore, Zhu Jiangming is currently the actual controller and highest decision-maker of Leapmotor.

Other important names in Leapmotor’s management include Wu Baojun and Cao Li, who are both executive directors.

Wu Baojun, born in 1970, graduated from the Automobile and Tractor major at Geelyn University of Technology.

Wu Baojun is currently the President of Leapmotor. His career has mainly focused on automotive sales, market services and automotive insurance. He has long served at Guangzhou Automobile Group, holding different positions as a brand market head.

Cao Li graduated from Zhejiang Sci-Tech University and is Vice President of Leapmotor and General Manager of the Vehicle Research and Development Department. He is currently responsible for the technology and products of Leapmotor. He comes from Dahua Group and has been engaged in design work for a long time.

Since 2021, Leapmotor’s sales have started to turn around, replacing WM Motor and entering the top tier. In the whole year, 43,121 new cars were delivered, ranking fifth after Li Auto.

However, Leapmotor has always been troubled by a lack of funds.

Since its establishment, Leapmotor has raised a total of 8 rounds of financing, totaling RMB 11.86 billion, which is not much for making cars.

Apart from Zhu and Fu and Dahua’s blood transfusions, Leapmotor has almost been supported by the “circle of friends” of local wealthy businessmen in Zhejiang.

For example, individual shareholder Chen Jinxia is the head of the once-dominant “Yongjin Group”, and many other institutions under Yongjin Group have participated in investing in Leapmotor.

In each round of investment, the most commonly seen names are Hangzhou Hanzhi, Hangzhou Fanlian, Huzhou Heninghai, Zhoushan Haohai, Hangzhou Chunsheng, and so on. These are all investment institutions and private enterprises that have come from Zhejiang.For LINGPAI, the business of making cars can be described as “perseverance leads to success.”

After six arduous years, sales took off and reputation gradually increased, causing investors to take notice.

Starting last year, LINGPAI passed the infancy period and entered a phase of rapid growth.

The company’s strategy, technological development, strengths, and challenges are gradually becoming clearer.

As for product layout, the next three years will be the “jiaozi-making” phase.

By the end of 2025, LINGPAI will launch eight new models, including three sedans (coupe/hatchback and subcompact cars), four SUVs, and one MPV.

If we combine LINGPAI’s 2.0 product layout chart, the three new sedans mentioned above, in addition to the known LINGPAI C01, LINGPAI will also launch two new sedans, codenamed A01 and D01, positioned between RMB 100,000 and RMB 150,000 and between RMB 250,000 and RMB 300,000, respectively.

It can be seen that LINGPAI’s vehicle layout is becoming larger and more high-end, and covers the entire range from RMB 100,000 to RMB 300,000.

In the prospectus, LINGPAI believes that its advantage lies in self-research and development and cost.

According to LINGPAI itself, it is a fully stacked self-research smart car company, with hardcore capabilities such as Tesla and XPeng.

Hardware includes vehicle development, design, wire-controlled chassis, battery pack (except for battery cells), drive motor, high-voltage charging technology, etc.

Software includes self-driving algorithm, intelligent cockpit OS, etc.

There are even chips. LINGPAI and Dahua jointly established a chip subsidiary last year to develop car AI chips. The latest flagship model, C11, depends on LINGPAI’s self-research Lingxin 01 chip with an 8.4TOPS computational capability for autonomous driving.

Although LINGPAI’s annual R&D investment currently only equals the level of one quarter of other new players and the team scale is not large, this does not prevent LINGPAI from laying out with Tesla’s technological standards.

LINGPAI believes that the advantage of full-stack self-research can be further extended to form the industry’s best vertical integration capability.

In other words, LINGPAI’s self-developed technology, coupled with investment or control supply chain companies within Dahua’s ecosystem, can minimize the cost of car manufacturing and maximize efficiency.

One example is the security system on LINGPAI cars.

So what are the challenges for Leapmotor?

Obviously, the R&D investment is not enough. It is a great challenge to surpass Tesla in three years.

When rumors of Leapmotor’s listing were circulating last year, Zhu Jiangming said:

“Leapmotor is likely to be the investors’ last ticket.”

Now, Leapmotor’s technology, products, strategies, and prospects are all in the open.

“Last ticket,” would you get on board?

- End –

This article is a translation by ChatGPT of a Chinese report from 42HOW. If you have any questions about it, please email bd@42how.com.