Author: Zhu Yulong

Last month’s market information on charging facilities sparked a lot of controversy. I used data from car companies and the charging alliance to reflect the actual situation.

As the number of electric vehicles increases, the problem of public charging stations becomes prominent:

- In August, there were 702,000 DC charging stations and 921,000 AC charging stations in China, with an increase of 48,000 public charging stations in a single month. AC charging stations have lower prices and have a faster rate of increase than DC stations.

- From January to August 2022, there were 476,000 new public charging stations and 1,221,000 private ones, with a total increase of 1,698,000 charging facilities and 3.86 million new energy vehicles sold.

- The ratio of number of new charging stations to new EVs is 1:2.3 in China in 2022. If we exclude AC charging stations and only look at DC charging stations, this ratio becomes 1:8.1 (even less optimistic). If we further exclude AC stations, the ratio becomes 1:16.

I believe that as China further develops pure electric vehicles, public charging facilities will become a great challenge.

As shown in the figure below, there are currently 11.7 million new energy vehicles in China, of which 4.315 million have their own AC charging stations or use public ones. Overall charging convenience faces significant challenges.

Distribution of Charging Stations

As shown in Figure 3 below, because the construction of charging facilities requires support from local finances, the overall construction is mainly focused on coastal cities. From the charging volume of each charging station, it can be seen that high-frequency use is concentrated around certain cities. The average monthly output of each public charging station is about 1,000 to 2,000 kWh, generating an average monthly revenue of about 1,500 to 3,000 yuan (including charging fees). With a service fee of 0.8 yuan, the produced value is between 800 and 1,600 yuan, which is usually achieved by DC charging stations.

As shown in the figure below, different service providers had significant differences in their August growth rates.

This data can be compared with the data of DC charging piles below. Currently, DC charging piles are still mainly focused on commercial 2B vehicles, and there are relatively few fast charging facilities for household vehicles.

Self-built Charging Network of Auto Manufacturers

As for promoting to 2C consumers, the proportion of consumers who can install charging stations at home will not be higher than 50% in the long run, and is gradually decreasing. Solving the problem of how to provide charging facilities for the other half of consumers is a major issue that auto manufacturers need to address. The simplest solution is to create an aggregation platform for car owners to solve the problem by themselves. However, Tesla, NIO, XPeng and Kai Ma Si are still vigorously promoting their own charging networks.

For the comparison in Figure 6, I collected the data of different auto manufacturers separately. The first few auto manufacturers have exceeded 1000 supercharging stations, but there are still differences in the overall number of charging piles.

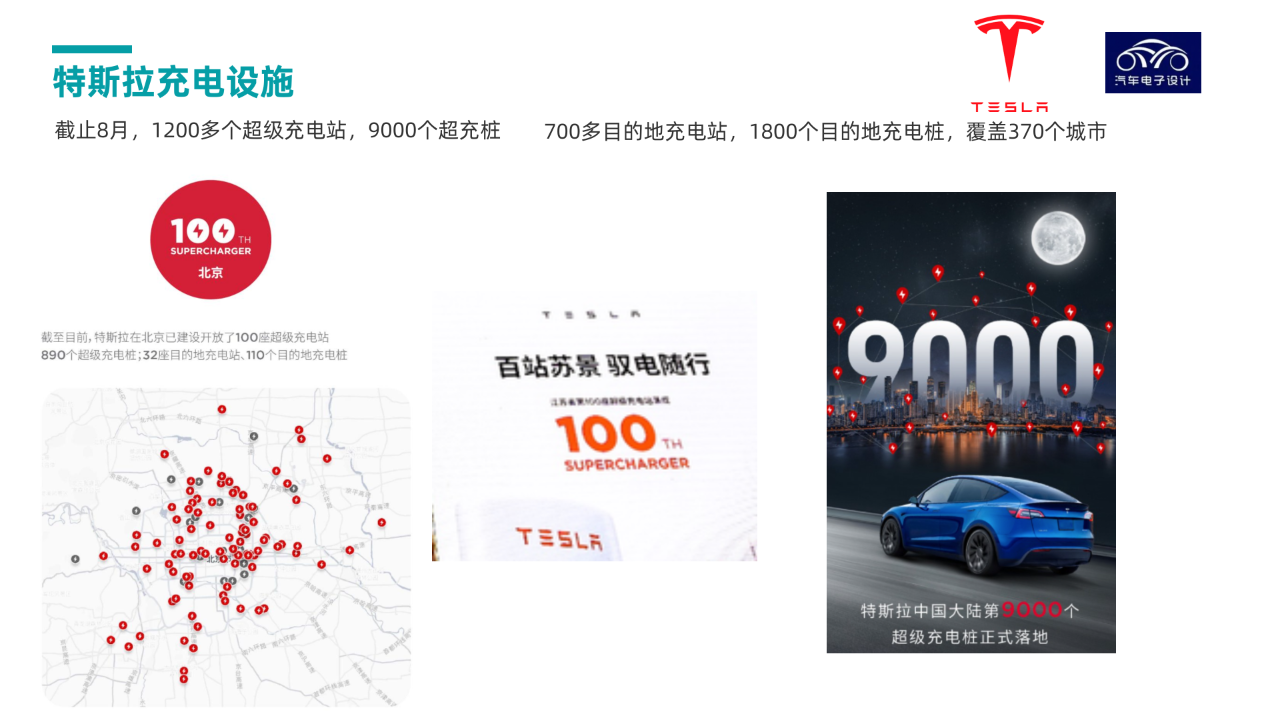

As of August, Tesla has built more than 1,200 supercharging stations and 9,000 supercharging piles in China. In Beijing and Jiangsu, more than 100 fast charging stations have been built respectively, and the overall development is still focused on fast charging.

NIO and XPeng are both actively developing fast charging stations, with NIO focusing on battery swapping and fast charging, while XPeng specializes in fast charging. Both have built more than 1,000 charging stations.

As for battery swapping stations, NIO has more data available and is beginning to expand to 2,000. With the launch of ET5, more fast swapping stations will also be added.“`

Summary: I have verified and confirmed the statistical data on charging and swapping infrastructure for August, for readers’ reference. Finally, I need your support on my Bilibili channel “朱玉龙的汽车电子设计”.

“`

This article is a translation by ChatGPT of a Chinese report from 42HOW. If you have any questions about it, please email bd@42how.com.