Monthly Analysis of Power Battery Industry by Zhu Yulong

It could be boring to just combine data to make a monthly column, so I would like to incorporate the situation of different battery companies to make a summary of monthly data and product releases. This can give a clearer understanding of the entire industry. I hope to continue this practice in the form of a monthly report on power batteries, which is also a good practice learned from Korean brokerage firms.

-

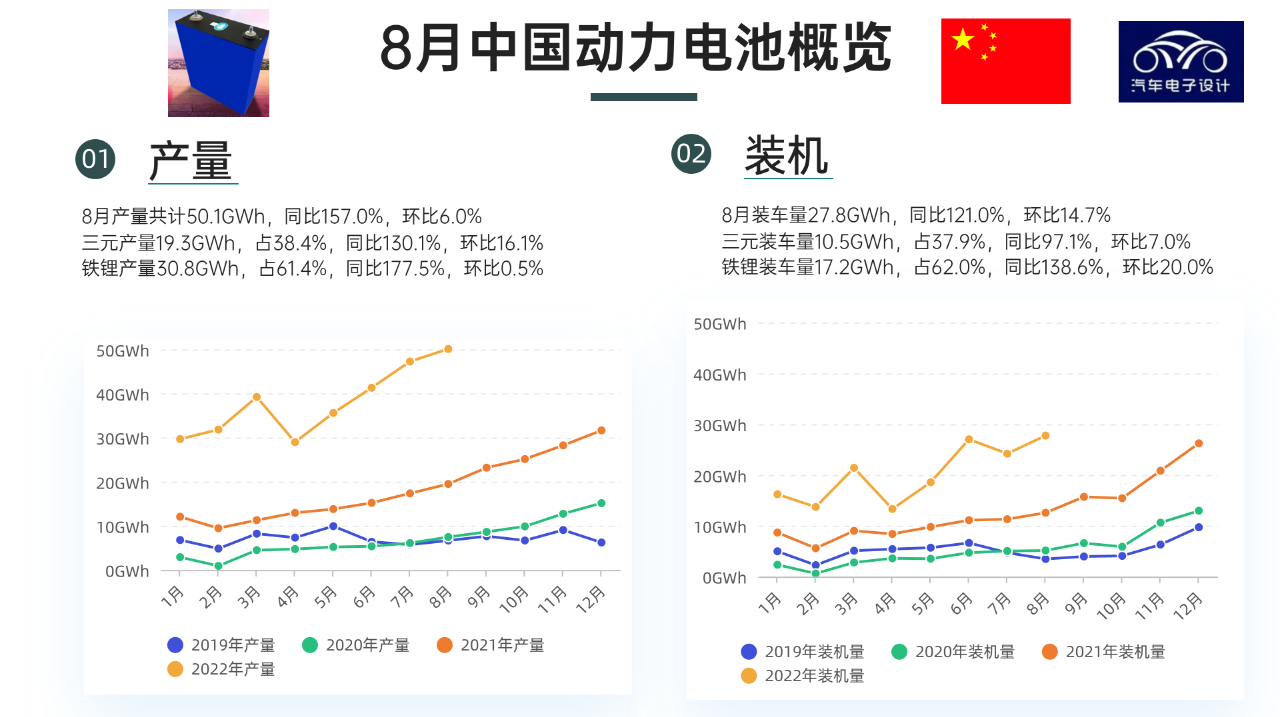

Production: In August, the total production was 50.1 GWh, up 157.0% year-on-year and 6.0% month-on-month.

-

The production of ternary batteries was 19.3 GWh, accounting for 38.4%, up 130.1% year-on-year and 16.1% month-on-month.

-

The production of lithium iron phosphate batteries was 30.8 GWh, accounting for 61.4%, up 177.5% year-on-year and 0.5% month-on-month.

-

Installation: In August, the installed capacity was 27.8 GWh, up 121.0% year-on-year and 14.7% month-on-month.

-

The installed capacity of ternary batteries was 10.5 GWh, accounting for 37.9%, up 97.1% year-on-year and 7.0% month-on-month.

-

The installed capacity of lithium iron phosphate batteries was 17.2 GWh, accounting for 62.0%, up 138.6% year-on-year and 20.0% month-on-month.

Data Analysis of Power Batteries

Many friends have been asking about the difference between production and installation. From the data of the past few years, it can be seen that the current production curve is clearly on the rise due to certainty at home and abroad.

-

Production: Due to certainty at home and abroad, except for special reasons, the upward trend of this curve is very obvious.

-

Installation: Domestic installation is subject to many factors fluctuation, but it is highly likely to be concentrated in Q4.

The difference here is indeed quite large. My understanding is that production = expected installation in the next few months + whole vehicle export + battery export + B-grade batteries. A part of it may be used for other purposes, especially the continuously rising lithium iron phosphate.

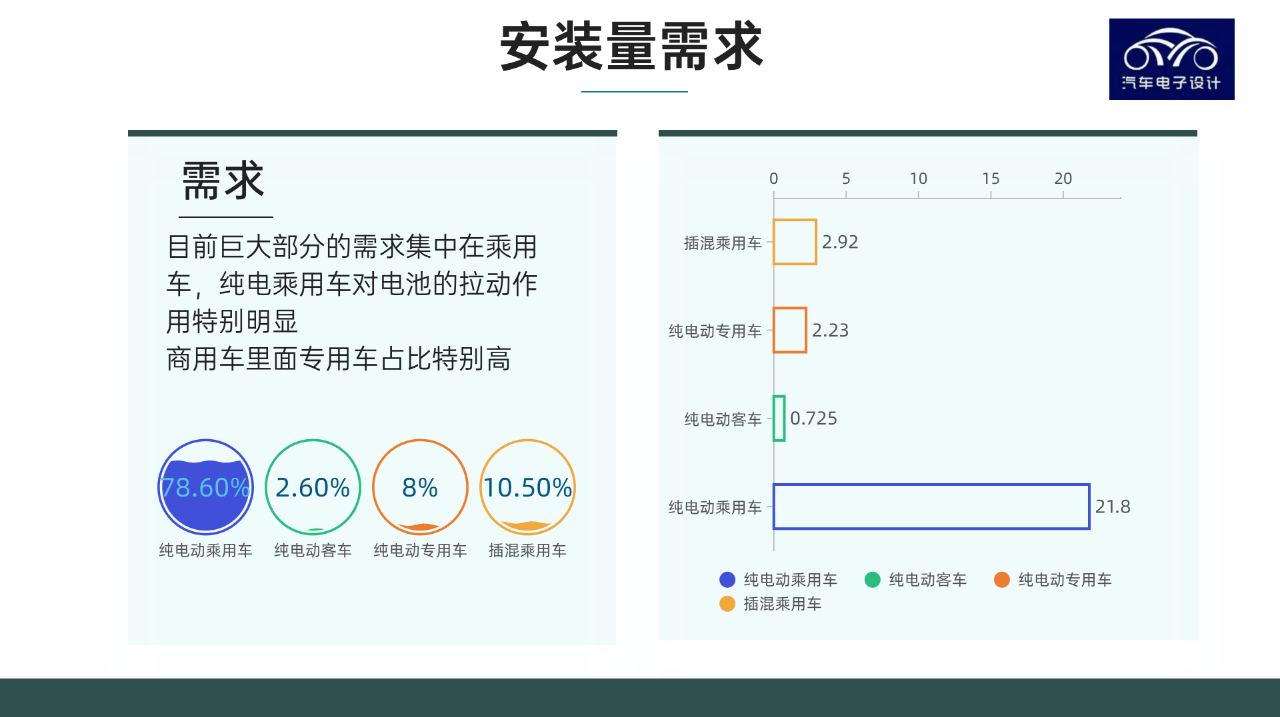

This year’s demand for power batteries is really concentrated in passenger cars, as the demand for buses continues to weaken, and passenger cars account for around 90%.

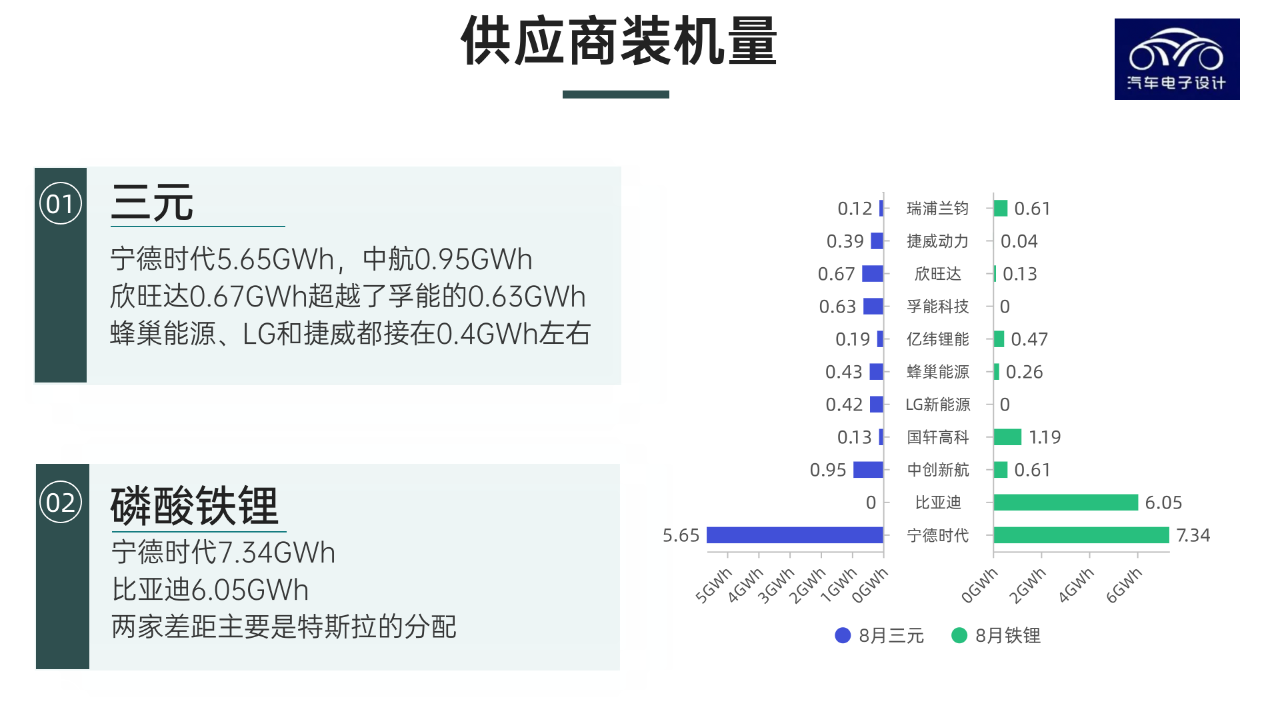

From the perspective of suppliers,

From the perspective of suppliers,

- On ternary materials:

CATL leads the market by supplying 5.65 GWh, followed by AVIC with 0.95 GWh, XWDE with 0.67 GWh, and Funeng with 0.63 GWh, while HEC, LG, and JW all produced around 0.4 GWh.

- On lithium iron phosphate:

CATL produced 7.34 GWh, while BYD produced 6.05 GWh. The difference is mainly due to Tesla’s allocation and production planning. It is estimated that NCM will have a larger output this year after upgrading its production capacity. AVIC’s production capacity for LFP has also increased, including Ruyi Pike’s output, which has risen to 0.61 GWh.

Monthly Industry News Review

This is not solely for August. I summarized the news up to today, and later I will provide a review of the monthly situation in China and abroad. BMW has transitioned from square to cylindrical batteries, which is a clear signal for 120 GWh. EVE Energy officially received the same amount of orders as CATL, which is rare.

- Rui’ou Battery and CATL released 480 Wh/L-based LFP batteries, which will be followed up with more detailed introductions.

- XWDE announced the release of a 4C super-fast charging battery, which was covered previously, and the output has increased rapidly recently.

- Funeng Technology continues to use soft pack batteries. However, we need to take a closer look at this plan and organize it when we are available.

- AVIC has taken a solid first step toward an IPO, which was held up due to patent issues, demonstrating its next approach. Indeed, Chinese power battery companies need to establish a fleet.

- HEC’s construction of the first overseas factory has been delayed, so they have gone ahead with the construction of the second factory.

Summary: Overall, the changes in the EV battery industry are quite fast. Combining data with enterprise news may increase the information and readability for reference.

This article is a translation by ChatGPT of a Chinese report from 42HOW. If you have any questions about it, please email bd@42how.com.